Temenos PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, and rapid tech change are reshaping Temenos with our concise PESTLE analysis—designed for investors and strategists who need actionable context. This snapshot highlights regulatory risks, market opportunities, and social trends that matter now. Buy the full PESTLE report to access the complete, editable breakdown and make smarter decisions fast.

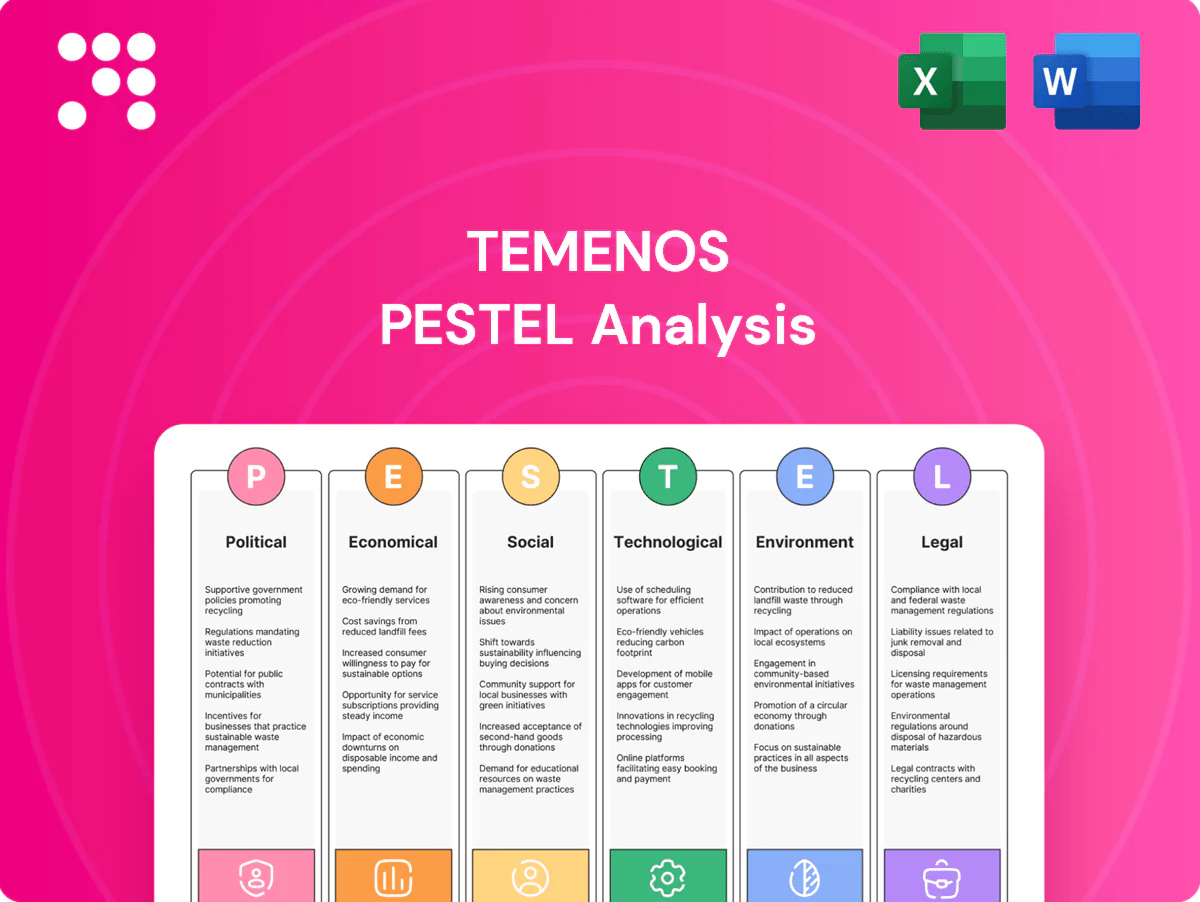

Political factors

Regulatory-driven banking agendas

Global policy priorities such as DORA (effective 17 Jan 2025) and Basel implementation timelines through 2028 shape banks’ IT roadmaps and budgets, directly impacting Temenos’ sales pipeline. Heightened supervisory focus on resilience, risk and consumer protection is accelerating compliance-driven upgrades, with EU banks earmarking multibillion euro spends for DORA. Political shifts can re-sequence initiatives, altering deal timing and scope; regional divergence demands highly configurable local solutions.

Geopolitical tensions and sanctions

Sanctions regimes and cross-border restrictions across 50+ countries constrain client eligibility and can halt project execution, forcing Temenos to pause implementations and license deliveries in affected markets.

Temenos must embed real-time sanction screening in its platforms and rapidly push updated rule sets to clients to avoid compliance failures and fines.

Sales in sanctioned jurisdictions may be delayed or prohibited, reducing addressable market and lengthening sales cycles.

Heightened geopolitical fragmentation raises supply-chain and partner risks, increasing vendor due diligence and contingency costs.

Data sovereignty and localization

Governments increasingly mandate local data residency, with over 60 jurisdictions enforcing localization rules, forcing banks to avoid single-region clouds. This shifts Temenos deployments toward sovereign cloud and on-prem variants and multi-region hosting to meet compliance. Such requirements raise implementation complexity and can push delivery costs into double-digit percentage increases. Policy reversals or tightening further amplify operational risk and cost volatility.

Public-sector digitalization initiatives

Public-sector digitalization programs expand addressable markets as state-backed inclusion and digital-payment schemes scale. National ID, RTGS modernization and instant payments (operating in over 100 countries by 2024) create integration opportunities for core and payment platforms. Vendor eligibility often depends on political ties and local partnerships; funding cycles shape procurement timing and pricing.

- Temenos: 3,000+ customers in 150+ countries

- Instant-pay systems: 100+ countries (2024)

- State programs drive large-scale deployments

- Procurement tied to funding cycles and local partners

Trade policy and market access

Changes in trade agreements, tariffs and 2024 US technology export controls on advanced semiconductors and AI chips can raise Temenos’s implementation and licensing costs and restrict partner supply chains. Cross-border services licensing limits staff mobility for on-site deployments. Political stability in key markets drives banking investment confidence; IMF projected 2024 global growth about 3.2%, shaping regional demand.

- Trade controls: 2024 US AI/chip export rules

- Tariff risk: raises operating costs

- Licensing: limits cross-border deployments

- Stability: IMF 2024 growth ~3.2% impacts demand

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Regulatory pushes (DORA effective 17 Jan 2025, Basel through 2028) and 60+ data‑localization laws force sovereign/multi‑region deployments, raising delivery costs; sanctions in 50+ countries and 2024 US tech export controls constrain market access and supply chains. Public-sector digitization (100+ instant‑pay systems by 2024) expands opportunities; Temenos’ 3,000+ customers in 150+ countries face longer sales cycles and higher compliance spend.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Increased IT spend | DORA 17‑Jan‑2025; Basel to 2028 |

| Data residency | Sovereign clouds | 60+ jurisdictions |

| Sanctions & trade | Market restrictions | 50+ countries; 2024 US export rules |

| Public programs | New deals | 100+ instant‑pay systems (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Temenos across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights and actionable implications to support executives, consultants and investors in strategy, risk management and fundraising.

A concise, visually segmented Temenos PESTLE summary that streamlines external risk and market-positioning discussions during planning sessions and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Bank IT spending cycles

Macro conditions shape banks’ capex-to-opex mix: downturns push cost takeout and accelerated core modernization while discretionary projects slow, whereas expansions drive digital growth and product launches. Global bank IT spend was estimated at USD 250–300bn in 2024, lifting demand in expansions. Temenos’ recurring SaaS revenue, which became the majority of its recurring mix by 2024, helps buffer this cyclicality.

Interest rates and credit cycles

Rate regimes affect bank profitability and transformation appetite; central bank policy rates remained elevated in mid‑2025 (US federal funds 5.25–5.50%), supporting higher NIMs for many lenders. Credit stress redirects budgets to risk and collections modules, while healthy NIMs enable broader platform investments. Implementation timelines typically elongate during stress periods as banks prioritise resilience over rollouts.

Currency fluctuations

Temenos' multi-currency revenues and costs across 150+ countries and 3,000+ banking customers expose it to FX translation risk; it reports results in US dollars, so EUR/GBP/CHF swings directly affect reported metrics. Pricing, hedging and local invoicing strategies become critical as client budgets shift with local-currency strength. Volatility can therefore compress reported growth and margins quarter-to-quarter.

Emerging market growth

Emerging market growth drives demand for Temenos as financial inclusion (World Bank Findex 2021: 1.4 billion unbanked) and a surge in new digital banks push modernization; price sensitivity favors modular, cloud and SaaS delivery, while local payment rails and regulation necessitate tailored core and payments solutions; political and credit risk elevate receivables and project risk.

- Financial inclusion: 1.4bn unbanked

- Delivery: modular/cloud/SaaS preferred

- Localization: payment rails + regs

- Risks: political/credit → higher receivables

Competition and consolidation

Consolidating banks and vendor consolidation are driving larger procurement rounds that favor platforms with scale, deep reference lists and rich integration ecosystems; global core vendors now compete for multi-year deals as pricing pressure intensifies and regional players undercut incumbents.

- Consolidation fuels bigger RFPs

- Scale and references win deals

- Pricing pressure rises

- Bank M&A triggers core replacements

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Macro cycles shift bank capex-to-opex and IT spend; global bank IT was USD 250–300bn in 2024, boosting demand for modernization while Temenos' recurring SaaS became majority of recurring revenue by 2024, buffering cyclicality. Elevated rates (US fed funds 5.25–5.50% mid‑2025) lift NIMs and transformation appetite; credit stress tilts budgets to risk modules. FX exposure across 150+ countries and 3,000+ customers amplifies reported volatility; emerging markets (1.4bn unbanked) drive price‑sensitive SaaS adoption.

| Metric | Value | Impact |

|---|---|---|

| Global bank IT spend (2024) | USD 250–300bn | Higher demand |

| Temenos SaaS mix (2024) | Majority recurring | Cyclicality buffer |

| Fed funds (mid‑2025) | 5.25–5.50% | ↑ NIMs, invest appetite |

| Unbanked (World Bank) | 1.4bn | EM growth opportunity |

| Geographic footprint | 150+ countries, 3,000+ clients | FX & local risk |

Preview the Actual Deliverable

Temenos PESTLE Analysis

The Temenos PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. You’ll receive this exact, professionally structured document immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, and rapid tech change are reshaping Temenos with our concise PESTLE analysis—designed for investors and strategists who need actionable context. This snapshot highlights regulatory risks, market opportunities, and social trends that matter now. Buy the full PESTLE report to access the complete, editable breakdown and make smarter decisions fast.

Political factors

Regulatory-driven banking agendas

Global policy priorities such as DORA (effective 17 Jan 2025) and Basel implementation timelines through 2028 shape banks’ IT roadmaps and budgets, directly impacting Temenos’ sales pipeline. Heightened supervisory focus on resilience, risk and consumer protection is accelerating compliance-driven upgrades, with EU banks earmarking multibillion euro spends for DORA. Political shifts can re-sequence initiatives, altering deal timing and scope; regional divergence demands highly configurable local solutions.

Geopolitical tensions and sanctions

Sanctions regimes and cross-border restrictions across 50+ countries constrain client eligibility and can halt project execution, forcing Temenos to pause implementations and license deliveries in affected markets.

Temenos must embed real-time sanction screening in its platforms and rapidly push updated rule sets to clients to avoid compliance failures and fines.

Sales in sanctioned jurisdictions may be delayed or prohibited, reducing addressable market and lengthening sales cycles.

Heightened geopolitical fragmentation raises supply-chain and partner risks, increasing vendor due diligence and contingency costs.

Data sovereignty and localization

Governments increasingly mandate local data residency, with over 60 jurisdictions enforcing localization rules, forcing banks to avoid single-region clouds. This shifts Temenos deployments toward sovereign cloud and on-prem variants and multi-region hosting to meet compliance. Such requirements raise implementation complexity and can push delivery costs into double-digit percentage increases. Policy reversals or tightening further amplify operational risk and cost volatility.

Public-sector digitalization initiatives

Public-sector digitalization programs expand addressable markets as state-backed inclusion and digital-payment schemes scale. National ID, RTGS modernization and instant payments (operating in over 100 countries by 2024) create integration opportunities for core and payment platforms. Vendor eligibility often depends on political ties and local partnerships; funding cycles shape procurement timing and pricing.

- Temenos: 3,000+ customers in 150+ countries

- Instant-pay systems: 100+ countries (2024)

- State programs drive large-scale deployments

- Procurement tied to funding cycles and local partners

Trade policy and market access

Changes in trade agreements, tariffs and 2024 US technology export controls on advanced semiconductors and AI chips can raise Temenos’s implementation and licensing costs and restrict partner supply chains. Cross-border services licensing limits staff mobility for on-site deployments. Political stability in key markets drives banking investment confidence; IMF projected 2024 global growth about 3.2%, shaping regional demand.

- Trade controls: 2024 US AI/chip export rules

- Tariff risk: raises operating costs

- Licensing: limits cross-border deployments

- Stability: IMF 2024 growth ~3.2% impacts demand

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Regulatory pushes (DORA effective 17 Jan 2025, Basel through 2028) and 60+ data‑localization laws force sovereign/multi‑region deployments, raising delivery costs; sanctions in 50+ countries and 2024 US tech export controls constrain market access and supply chains. Public-sector digitization (100+ instant‑pay systems by 2024) expands opportunities; Temenos’ 3,000+ customers in 150+ countries face longer sales cycles and higher compliance spend.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Increased IT spend | DORA 17‑Jan‑2025; Basel to 2028 |

| Data residency | Sovereign clouds | 60+ jurisdictions |

| Sanctions & trade | Market restrictions | 50+ countries; 2024 US export rules |

| Public programs | New deals | 100+ instant‑pay systems (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Temenos across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights and actionable implications to support executives, consultants and investors in strategy, risk management and fundraising.

A concise, visually segmented Temenos PESTLE summary that streamlines external risk and market-positioning discussions during planning sessions and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Bank IT spending cycles

Macro conditions shape banks’ capex-to-opex mix: downturns push cost takeout and accelerated core modernization while discretionary projects slow, whereas expansions drive digital growth and product launches. Global bank IT spend was estimated at USD 250–300bn in 2024, lifting demand in expansions. Temenos’ recurring SaaS revenue, which became the majority of its recurring mix by 2024, helps buffer this cyclicality.

Interest rates and credit cycles

Rate regimes affect bank profitability and transformation appetite; central bank policy rates remained elevated in mid‑2025 (US federal funds 5.25–5.50%), supporting higher NIMs for many lenders. Credit stress redirects budgets to risk and collections modules, while healthy NIMs enable broader platform investments. Implementation timelines typically elongate during stress periods as banks prioritise resilience over rollouts.

Currency fluctuations

Temenos' multi-currency revenues and costs across 150+ countries and 3,000+ banking customers expose it to FX translation risk; it reports results in US dollars, so EUR/GBP/CHF swings directly affect reported metrics. Pricing, hedging and local invoicing strategies become critical as client budgets shift with local-currency strength. Volatility can therefore compress reported growth and margins quarter-to-quarter.

Emerging market growth

Emerging market growth drives demand for Temenos as financial inclusion (World Bank Findex 2021: 1.4 billion unbanked) and a surge in new digital banks push modernization; price sensitivity favors modular, cloud and SaaS delivery, while local payment rails and regulation necessitate tailored core and payments solutions; political and credit risk elevate receivables and project risk.

- Financial inclusion: 1.4bn unbanked

- Delivery: modular/cloud/SaaS preferred

- Localization: payment rails + regs

- Risks: political/credit → higher receivables

Competition and consolidation

Consolidating banks and vendor consolidation are driving larger procurement rounds that favor platforms with scale, deep reference lists and rich integration ecosystems; global core vendors now compete for multi-year deals as pricing pressure intensifies and regional players undercut incumbents.

- Consolidation fuels bigger RFPs

- Scale and references win deals

- Pricing pressure rises

- Bank M&A triggers core replacements

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Macro cycles shift bank capex-to-opex and IT spend; global bank IT was USD 250–300bn in 2024, boosting demand for modernization while Temenos' recurring SaaS became majority of recurring revenue by 2024, buffering cyclicality. Elevated rates (US fed funds 5.25–5.50% mid‑2025) lift NIMs and transformation appetite; credit stress tilts budgets to risk modules. FX exposure across 150+ countries and 3,000+ customers amplifies reported volatility; emerging markets (1.4bn unbanked) drive price‑sensitive SaaS adoption.

| Metric | Value | Impact |

|---|---|---|

| Global bank IT spend (2024) | USD 250–300bn | Higher demand |

| Temenos SaaS mix (2024) | Majority recurring | Cyclicality buffer |

| Fed funds (mid‑2025) | 5.25–5.50% | ↑ NIMs, invest appetite |

| Unbanked (World Bank) | 1.4bn | EM growth opportunity |

| Geographic footprint | 150+ countries, 3,000+ clients | FX & local risk |

Preview the Actual Deliverable

Temenos PESTLE Analysis

The Temenos PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. You’ll receive this exact, professionally structured document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, and rapid tech change are reshaping Temenos with our concise PESTLE analysis—designed for investors and strategists who need actionable context. This snapshot highlights regulatory risks, market opportunities, and social trends that matter now. Buy the full PESTLE report to access the complete, editable breakdown and make smarter decisions fast.

Political factors

Regulatory-driven banking agendas

Global policy priorities such as DORA (effective 17 Jan 2025) and Basel implementation timelines through 2028 shape banks’ IT roadmaps and budgets, directly impacting Temenos’ sales pipeline. Heightened supervisory focus on resilience, risk and consumer protection is accelerating compliance-driven upgrades, with EU banks earmarking multibillion euro spends for DORA. Political shifts can re-sequence initiatives, altering deal timing and scope; regional divergence demands highly configurable local solutions.

Geopolitical tensions and sanctions

Sanctions regimes and cross-border restrictions across 50+ countries constrain client eligibility and can halt project execution, forcing Temenos to pause implementations and license deliveries in affected markets.

Temenos must embed real-time sanction screening in its platforms and rapidly push updated rule sets to clients to avoid compliance failures and fines.

Sales in sanctioned jurisdictions may be delayed or prohibited, reducing addressable market and lengthening sales cycles.

Heightened geopolitical fragmentation raises supply-chain and partner risks, increasing vendor due diligence and contingency costs.

Data sovereignty and localization

Governments increasingly mandate local data residency, with over 60 jurisdictions enforcing localization rules, forcing banks to avoid single-region clouds. This shifts Temenos deployments toward sovereign cloud and on-prem variants and multi-region hosting to meet compliance. Such requirements raise implementation complexity and can push delivery costs into double-digit percentage increases. Policy reversals or tightening further amplify operational risk and cost volatility.

Public-sector digitalization initiatives

Public-sector digitalization programs expand addressable markets as state-backed inclusion and digital-payment schemes scale. National ID, RTGS modernization and instant payments (operating in over 100 countries by 2024) create integration opportunities for core and payment platforms. Vendor eligibility often depends on political ties and local partnerships; funding cycles shape procurement timing and pricing.

- Temenos: 3,000+ customers in 150+ countries

- Instant-pay systems: 100+ countries (2024)

- State programs drive large-scale deployments

- Procurement tied to funding cycles and local partners

Trade policy and market access

Changes in trade agreements, tariffs and 2024 US technology export controls on advanced semiconductors and AI chips can raise Temenos’s implementation and licensing costs and restrict partner supply chains. Cross-border services licensing limits staff mobility for on-site deployments. Political stability in key markets drives banking investment confidence; IMF projected 2024 global growth about 3.2%, shaping regional demand.

- Trade controls: 2024 US AI/chip export rules

- Tariff risk: raises operating costs

- Licensing: limits cross-border deployments

- Stability: IMF 2024 growth ~3.2% impacts demand

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Regulatory pushes (DORA effective 17 Jan 2025, Basel through 2028) and 60+ data‑localization laws force sovereign/multi‑region deployments, raising delivery costs; sanctions in 50+ countries and 2024 US tech export controls constrain market access and supply chains. Public-sector digitization (100+ instant‑pay systems by 2024) expands opportunities; Temenos’ 3,000+ customers in 150+ countries face longer sales cycles and higher compliance spend.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Increased IT spend | DORA 17‑Jan‑2025; Basel to 2028 |

| Data residency | Sovereign clouds | 60+ jurisdictions |

| Sanctions & trade | Market restrictions | 50+ countries; 2024 US export rules |

| Public programs | New deals | 100+ instant‑pay systems (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Temenos across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights and actionable implications to support executives, consultants and investors in strategy, risk management and fundraising.

A concise, visually segmented Temenos PESTLE summary that streamlines external risk and market-positioning discussions during planning sessions and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Bank IT spending cycles

Macro conditions shape banks’ capex-to-opex mix: downturns push cost takeout and accelerated core modernization while discretionary projects slow, whereas expansions drive digital growth and product launches. Global bank IT spend was estimated at USD 250–300bn in 2024, lifting demand in expansions. Temenos’ recurring SaaS revenue, which became the majority of its recurring mix by 2024, helps buffer this cyclicality.

Interest rates and credit cycles

Rate regimes affect bank profitability and transformation appetite; central bank policy rates remained elevated in mid‑2025 (US federal funds 5.25–5.50%), supporting higher NIMs for many lenders. Credit stress redirects budgets to risk and collections modules, while healthy NIMs enable broader platform investments. Implementation timelines typically elongate during stress periods as banks prioritise resilience over rollouts.

Currency fluctuations

Temenos' multi-currency revenues and costs across 150+ countries and 3,000+ banking customers expose it to FX translation risk; it reports results in US dollars, so EUR/GBP/CHF swings directly affect reported metrics. Pricing, hedging and local invoicing strategies become critical as client budgets shift with local-currency strength. Volatility can therefore compress reported growth and margins quarter-to-quarter.

Emerging market growth

Emerging market growth drives demand for Temenos as financial inclusion (World Bank Findex 2021: 1.4 billion unbanked) and a surge in new digital banks push modernization; price sensitivity favors modular, cloud and SaaS delivery, while local payment rails and regulation necessitate tailored core and payments solutions; political and credit risk elevate receivables and project risk.

- Financial inclusion: 1.4bn unbanked

- Delivery: modular/cloud/SaaS preferred

- Localization: payment rails + regs

- Risks: political/credit → higher receivables

Competition and consolidation

Consolidating banks and vendor consolidation are driving larger procurement rounds that favor platforms with scale, deep reference lists and rich integration ecosystems; global core vendors now compete for multi-year deals as pricing pressure intensifies and regional players undercut incumbents.

- Consolidation fuels bigger RFPs

- Scale and references win deals

- Pricing pressure rises

- Bank M&A triggers core replacements

Regulation and sanctions drive sovereign cloud costs and longer sales cycles

Macro cycles shift bank capex-to-opex and IT spend; global bank IT was USD 250–300bn in 2024, boosting demand for modernization while Temenos' recurring SaaS became majority of recurring revenue by 2024, buffering cyclicality. Elevated rates (US fed funds 5.25–5.50% mid‑2025) lift NIMs and transformation appetite; credit stress tilts budgets to risk modules. FX exposure across 150+ countries and 3,000+ customers amplifies reported volatility; emerging markets (1.4bn unbanked) drive price‑sensitive SaaS adoption.

| Metric | Value | Impact |

|---|---|---|

| Global bank IT spend (2024) | USD 250–300bn | Higher demand |

| Temenos SaaS mix (2024) | Majority recurring | Cyclicality buffer |

| Fed funds (mid‑2025) | 5.25–5.50% | ↑ NIMs, invest appetite |

| Unbanked (World Bank) | 1.4bn | EM growth opportunity |

| Geographic footprint | 150+ countries, 3,000+ clients | FX & local risk |

Preview the Actual Deliverable

Temenos PESTLE Analysis

The Temenos PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. You’ll receive this exact, professionally structured document immediately after checkout.