Tengelmann Warenhandelsgesellschaft KG Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

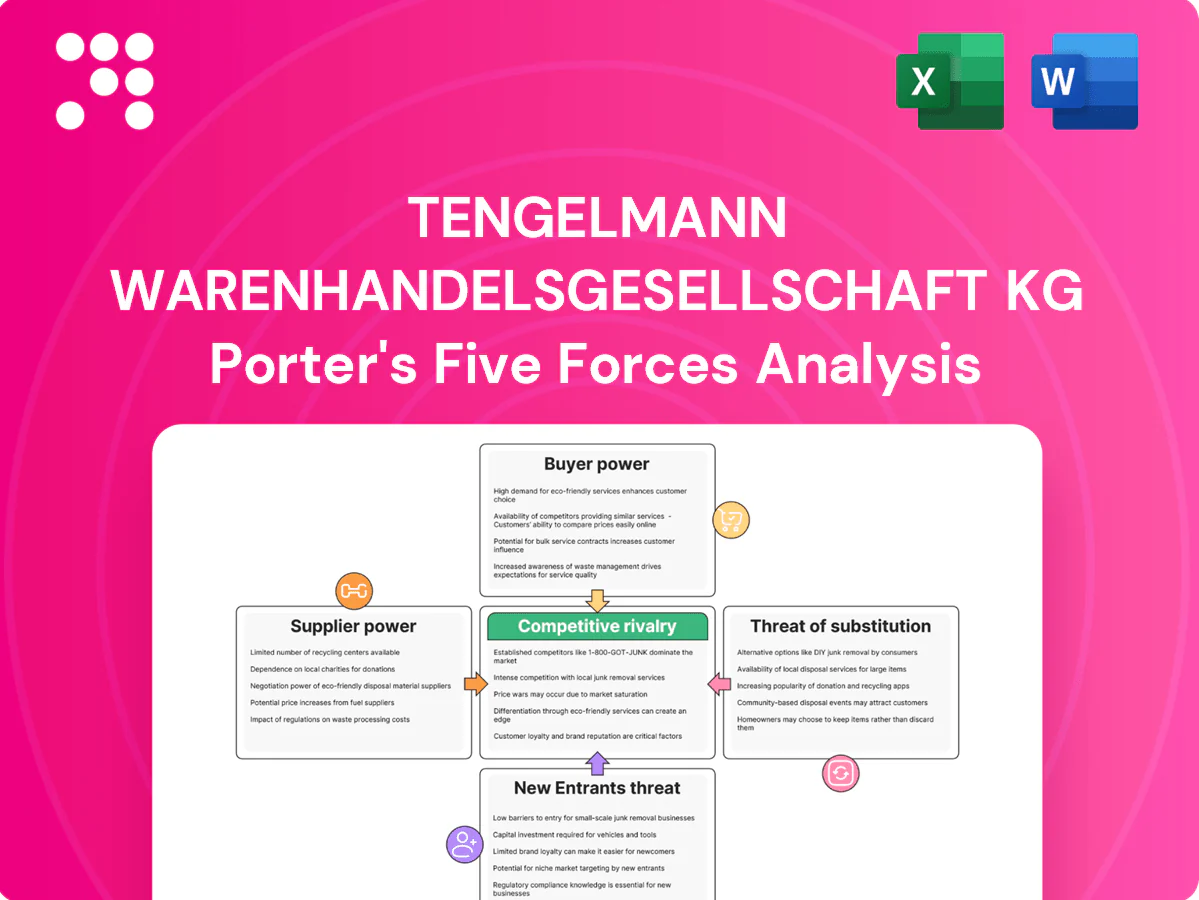

Tengelmann faces moderate buyer power, intense rivalry among German retailers, limited supplier leverage, manageable threat of new entrants, and rising substitutes from discounters and e‑commerce. This snapshot highlights competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated specialist partners

As a holding company, Tengelmann relies on niche partners—property developers, operating partners and sector experts—to source and manage deals, concentrating supplier power. In 2024 competition for prime urban sites and high-growth retail tech intensified, enabling these partners to command premium fees and stricter terms. Their leverage peaks in hot markets with limited capacity, though deep, long-term relationships often secure better pricing and priority access.

Capital and financing providers

Debt financiers and co-investors shape pricing, covenants and execution speed, with ECB policy rates around 4.00% in mid‑2024 increasing lender leverage and compressing equity returns. When credit tightens, lenders push stricter covenants and higher margins; in benign cycles, competition among banks eases those terms. Tengelmann’s strong balance sheet reduces reliance on any single capital provider and limits supplier leverage.

Advisors and intermediaries

Investment banks, brokers and legal/tax advisors control proprietary deal flow and execution quality, often charging advisory fees commonly in the 1–3% range for mid‑market deals (2024 market practice). In auction processes top intermediaries extract higher fees and prioritize preferred clients, boosting win rates for marquee teams while raising transaction costs. Reliance on external advisors improves outcomes but building in‑house M&A capabilities reduces fee exposure and dependence.

Technology and data vendors

Portfolio oversight and retail analytics at Tengelmann depend on software, data and cloud services, with vendor lock-in and integration complexity elevating supplier bargaining power. In 2024 global public cloud spend approached ~600B USD, underscoring concentrated supplier leverage. Restrictive licensing for best-in-class datasets further gates access while multi-vendor strategies and in‑house tooling can rebalance power.

Construction and facilities inputs

Construction and facilities inputs for Tengelmann’s real estate require contractors, building materials and facility managers; in 2024 supply-chain tightness and rising ESG retrofit standards have increased suppliers’ ability to push prices and alter timelines.

- Long-term framework agreements — stabilize cost and quality

- Diversifying contractors — reduces concentration risk

- ESG retrofit requirements — shift bargaining power toward specialist suppliers

Supplier power rises: lenders, advisors, cloud vendors demand premiums in 2024

Tengelmann’s niche partners, advisors and cloud/data vendors exert moderate-to-high supplier power in 2024, pushing premium fees, strict terms and vendor lock‑in. ECB rate ~4.00% mid‑2024 raises lender leverage; advisory fees 1–3% increase deal costs. Public cloud spend ~600B USD (2024) and construction input inflation ~5% y/y amplify supplier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Lenders | ECB ~4.00% | Higher covenants/margins |

| Advisors | Fees 1–3% | Raises transaction costs |

| Cloud/Data | Global spend ~600B USD | Vendor leverage |

| Construction | Input inflation ~5% y/y | Higher capex/timelines |

What is included in the product

Tailored Porter's Five Forces analysis for Tengelmann Warenhandelsgesellschaft KG, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Tengelmann Warenhandelsgesellschaft KG—instantly visualize competitive pressure with a radar chart, customize force levels to reflect supplier/retailer dynamics, and drop directly into decks for faster, board-ready strategy decisions.

Customers Bargaining Power

Exit-market acquirers

Exit-market acquirers — strategic buyers and financial sponsors — act as the primary customers for Tengelmann assets, with global private equity dry powder above $2.2 trillion in 2024 increasing deal competition but also heightening price sensitivity. In buyer-favourable markets acquirers have pushed multiples down toward low-double digits and demanded tougher warranties, while competitive auctions and multiple bidders have historically lifted realized prices by several turns of EBITDA. Clear value-creation proof points such as high-quality tenants, 90%+ occupancy and year-on-year KPI growth materially reduce buyer leverage and secure stronger exit multiples.

Tenants and lease counterparties

For Tengelmann's property holdings tenants negotiate rents, incentives and lease length; in 2024 German retail vacancy rates rose to roughly 5–6% in many secondary submarkets, strengthening tenant leverage and increasing concession levels for creditworthy anchors. In oversupplied areas anchors can secure rent-free periods or stepped rents, while in supply-constrained city-center locations landlord leverage improves. Proactive asset management and tenant-mix optimization reduce tenant bargaining power and limit downside exposure.

Consumers of portfolio companies

End-customers in retail and e-commerce are highly price sensitive with global e-commerce sales around $6.3 trillion in 2024, giving buyers abundant alternatives and low switching costs that amplify bargaining power and pressure margins. Strong brands, seamless convenience and loyalty programs can reduce sensitivity by improving retention. Tengelmann's diversification across formats and geographies spreads demand and margin risk.

Co-investors and JV partners

Co-investors and JV partners can push for governance rights, management fees, and defined exit pathways; when their capital is required to close a Tengelmann transaction their bargaining power increases. Clear alignment on strategy and economics—demonstrated in 2024 by tighter governance clauses across European retail deals—reduces friction, while Tengelmann’s track record helps secure partner-friendly terms.

- Governance rights

- Fees & exit pathways

- Higher power when capital is critical

- 2024: tighter governance clauses in EU retail JVs

Institutional renters and operators

Institutional renters and master-lease operators exert strong bargaining power over Tengelmann by negotiating fee structures and strict performance clauses; their scale and local operating know-how enhance leverage, often dictating service levels and rent indexing. Performance-linked contracts can align incentives and reduce rent risk, while cultivating multiple operator relationships limits dependency and preserves negotiating leverage.

PE dry powder, e-commerce surge and rising vacancies intensify retail deal competition

Exit-market acquirers face >$2.2T private equity dry powder in 2024, boosting competition but increasing price sensitivity. German retail vacancy rose to ~5–6% in many secondary submarkets in 2024, strengthening tenant leverage. Global e-commerce sales hit ~$6.3T in 2024, raising end-customer price pressure; tighter JV governance clauses in EU retail deals in 2024 increased partner bargaining power.

| Buyer type | 2024 metric | Impact |

|---|---|---|

| PE/Strategic | $2.2T dry powder | ↑ competition, ↓ price |

| Tenants | 5–6% vacancy (secondary) | ↑ concessions |

| End-customers | $6.3T e‑commerce | ↑ price sensitivity |

| JV partners | Tighter governance | ↑ negotiation power |

What You See Is What You Get

Tengelmann Warenhandelsgesellschaft KG Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tengelmann Warenhandelsgesellschaft KG evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. It includes market context, evidence-based scoring, and implications for pricing, sourcing, and growth. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

Tengelmann faces moderate buyer power, intense rivalry among German retailers, limited supplier leverage, manageable threat of new entrants, and rising substitutes from discounters and e‑commerce. This snapshot highlights competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated specialist partners

As a holding company, Tengelmann relies on niche partners—property developers, operating partners and sector experts—to source and manage deals, concentrating supplier power. In 2024 competition for prime urban sites and high-growth retail tech intensified, enabling these partners to command premium fees and stricter terms. Their leverage peaks in hot markets with limited capacity, though deep, long-term relationships often secure better pricing and priority access.

Capital and financing providers

Debt financiers and co-investors shape pricing, covenants and execution speed, with ECB policy rates around 4.00% in mid‑2024 increasing lender leverage and compressing equity returns. When credit tightens, lenders push stricter covenants and higher margins; in benign cycles, competition among banks eases those terms. Tengelmann’s strong balance sheet reduces reliance on any single capital provider and limits supplier leverage.

Advisors and intermediaries

Investment banks, brokers and legal/tax advisors control proprietary deal flow and execution quality, often charging advisory fees commonly in the 1–3% range for mid‑market deals (2024 market practice). In auction processes top intermediaries extract higher fees and prioritize preferred clients, boosting win rates for marquee teams while raising transaction costs. Reliance on external advisors improves outcomes but building in‑house M&A capabilities reduces fee exposure and dependence.

Technology and data vendors

Portfolio oversight and retail analytics at Tengelmann depend on software, data and cloud services, with vendor lock-in and integration complexity elevating supplier bargaining power. In 2024 global public cloud spend approached ~600B USD, underscoring concentrated supplier leverage. Restrictive licensing for best-in-class datasets further gates access while multi-vendor strategies and in‑house tooling can rebalance power.

Construction and facilities inputs

Construction and facilities inputs for Tengelmann’s real estate require contractors, building materials and facility managers; in 2024 supply-chain tightness and rising ESG retrofit standards have increased suppliers’ ability to push prices and alter timelines.

- Long-term framework agreements — stabilize cost and quality

- Diversifying contractors — reduces concentration risk

- ESG retrofit requirements — shift bargaining power toward specialist suppliers

Supplier power rises: lenders, advisors, cloud vendors demand premiums in 2024

Tengelmann’s niche partners, advisors and cloud/data vendors exert moderate-to-high supplier power in 2024, pushing premium fees, strict terms and vendor lock‑in. ECB rate ~4.00% mid‑2024 raises lender leverage; advisory fees 1–3% increase deal costs. Public cloud spend ~600B USD (2024) and construction input inflation ~5% y/y amplify supplier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Lenders | ECB ~4.00% | Higher covenants/margins |

| Advisors | Fees 1–3% | Raises transaction costs |

| Cloud/Data | Global spend ~600B USD | Vendor leverage |

| Construction | Input inflation ~5% y/y | Higher capex/timelines |

What is included in the product

Tailored Porter's Five Forces analysis for Tengelmann Warenhandelsgesellschaft KG, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Tengelmann Warenhandelsgesellschaft KG—instantly visualize competitive pressure with a radar chart, customize force levels to reflect supplier/retailer dynamics, and drop directly into decks for faster, board-ready strategy decisions.

Customers Bargaining Power

Exit-market acquirers

Exit-market acquirers — strategic buyers and financial sponsors — act as the primary customers for Tengelmann assets, with global private equity dry powder above $2.2 trillion in 2024 increasing deal competition but also heightening price sensitivity. In buyer-favourable markets acquirers have pushed multiples down toward low-double digits and demanded tougher warranties, while competitive auctions and multiple bidders have historically lifted realized prices by several turns of EBITDA. Clear value-creation proof points such as high-quality tenants, 90%+ occupancy and year-on-year KPI growth materially reduce buyer leverage and secure stronger exit multiples.

Tenants and lease counterparties

For Tengelmann's property holdings tenants negotiate rents, incentives and lease length; in 2024 German retail vacancy rates rose to roughly 5–6% in many secondary submarkets, strengthening tenant leverage and increasing concession levels for creditworthy anchors. In oversupplied areas anchors can secure rent-free periods or stepped rents, while in supply-constrained city-center locations landlord leverage improves. Proactive asset management and tenant-mix optimization reduce tenant bargaining power and limit downside exposure.

Consumers of portfolio companies

End-customers in retail and e-commerce are highly price sensitive with global e-commerce sales around $6.3 trillion in 2024, giving buyers abundant alternatives and low switching costs that amplify bargaining power and pressure margins. Strong brands, seamless convenience and loyalty programs can reduce sensitivity by improving retention. Tengelmann's diversification across formats and geographies spreads demand and margin risk.

Co-investors and JV partners

Co-investors and JV partners can push for governance rights, management fees, and defined exit pathways; when their capital is required to close a Tengelmann transaction their bargaining power increases. Clear alignment on strategy and economics—demonstrated in 2024 by tighter governance clauses across European retail deals—reduces friction, while Tengelmann’s track record helps secure partner-friendly terms.

- Governance rights

- Fees & exit pathways

- Higher power when capital is critical

- 2024: tighter governance clauses in EU retail JVs

Institutional renters and operators

Institutional renters and master-lease operators exert strong bargaining power over Tengelmann by negotiating fee structures and strict performance clauses; their scale and local operating know-how enhance leverage, often dictating service levels and rent indexing. Performance-linked contracts can align incentives and reduce rent risk, while cultivating multiple operator relationships limits dependency and preserves negotiating leverage.

PE dry powder, e-commerce surge and rising vacancies intensify retail deal competition

Exit-market acquirers face >$2.2T private equity dry powder in 2024, boosting competition but increasing price sensitivity. German retail vacancy rose to ~5–6% in many secondary submarkets in 2024, strengthening tenant leverage. Global e-commerce sales hit ~$6.3T in 2024, raising end-customer price pressure; tighter JV governance clauses in EU retail deals in 2024 increased partner bargaining power.

| Buyer type | 2024 metric | Impact |

|---|---|---|

| PE/Strategic | $2.2T dry powder | ↑ competition, ↓ price |

| Tenants | 5–6% vacancy (secondary) | ↑ concessions |

| End-customers | $6.3T e‑commerce | ↑ price sensitivity |

| JV partners | Tighter governance | ↑ negotiation power |

What You See Is What You Get

Tengelmann Warenhandelsgesellschaft KG Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tengelmann Warenhandelsgesellschaft KG evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. It includes market context, evidence-based scoring, and implications for pricing, sourcing, and growth. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Tengelmann faces moderate buyer power, intense rivalry among German retailers, limited supplier leverage, manageable threat of new entrants, and rising substitutes from discounters and e‑commerce. This snapshot highlights competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated specialist partners

As a holding company, Tengelmann relies on niche partners—property developers, operating partners and sector experts—to source and manage deals, concentrating supplier power. In 2024 competition for prime urban sites and high-growth retail tech intensified, enabling these partners to command premium fees and stricter terms. Their leverage peaks in hot markets with limited capacity, though deep, long-term relationships often secure better pricing and priority access.

Capital and financing providers

Debt financiers and co-investors shape pricing, covenants and execution speed, with ECB policy rates around 4.00% in mid‑2024 increasing lender leverage and compressing equity returns. When credit tightens, lenders push stricter covenants and higher margins; in benign cycles, competition among banks eases those terms. Tengelmann’s strong balance sheet reduces reliance on any single capital provider and limits supplier leverage.

Advisors and intermediaries

Investment banks, brokers and legal/tax advisors control proprietary deal flow and execution quality, often charging advisory fees commonly in the 1–3% range for mid‑market deals (2024 market practice). In auction processes top intermediaries extract higher fees and prioritize preferred clients, boosting win rates for marquee teams while raising transaction costs. Reliance on external advisors improves outcomes but building in‑house M&A capabilities reduces fee exposure and dependence.

Technology and data vendors

Portfolio oversight and retail analytics at Tengelmann depend on software, data and cloud services, with vendor lock-in and integration complexity elevating supplier bargaining power. In 2024 global public cloud spend approached ~600B USD, underscoring concentrated supplier leverage. Restrictive licensing for best-in-class datasets further gates access while multi-vendor strategies and in‑house tooling can rebalance power.

Construction and facilities inputs

Construction and facilities inputs for Tengelmann’s real estate require contractors, building materials and facility managers; in 2024 supply-chain tightness and rising ESG retrofit standards have increased suppliers’ ability to push prices and alter timelines.

- Long-term framework agreements — stabilize cost and quality

- Diversifying contractors — reduces concentration risk

- ESG retrofit requirements — shift bargaining power toward specialist suppliers

Supplier power rises: lenders, advisors, cloud vendors demand premiums in 2024

Tengelmann’s niche partners, advisors and cloud/data vendors exert moderate-to-high supplier power in 2024, pushing premium fees, strict terms and vendor lock‑in. ECB rate ~4.00% mid‑2024 raises lender leverage; advisory fees 1–3% increase deal costs. Public cloud spend ~600B USD (2024) and construction input inflation ~5% y/y amplify supplier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Lenders | ECB ~4.00% | Higher covenants/margins |

| Advisors | Fees 1–3% | Raises transaction costs |

| Cloud/Data | Global spend ~600B USD | Vendor leverage |

| Construction | Input inflation ~5% y/y | Higher capex/timelines |

What is included in the product

Tailored Porter's Five Forces analysis for Tengelmann Warenhandelsgesellschaft KG, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Tengelmann Warenhandelsgesellschaft KG—instantly visualize competitive pressure with a radar chart, customize force levels to reflect supplier/retailer dynamics, and drop directly into decks for faster, board-ready strategy decisions.

Customers Bargaining Power

Exit-market acquirers

Exit-market acquirers — strategic buyers and financial sponsors — act as the primary customers for Tengelmann assets, with global private equity dry powder above $2.2 trillion in 2024 increasing deal competition but also heightening price sensitivity. In buyer-favourable markets acquirers have pushed multiples down toward low-double digits and demanded tougher warranties, while competitive auctions and multiple bidders have historically lifted realized prices by several turns of EBITDA. Clear value-creation proof points such as high-quality tenants, 90%+ occupancy and year-on-year KPI growth materially reduce buyer leverage and secure stronger exit multiples.

Tenants and lease counterparties

For Tengelmann's property holdings tenants negotiate rents, incentives and lease length; in 2024 German retail vacancy rates rose to roughly 5–6% in many secondary submarkets, strengthening tenant leverage and increasing concession levels for creditworthy anchors. In oversupplied areas anchors can secure rent-free periods or stepped rents, while in supply-constrained city-center locations landlord leverage improves. Proactive asset management and tenant-mix optimization reduce tenant bargaining power and limit downside exposure.

Consumers of portfolio companies

End-customers in retail and e-commerce are highly price sensitive with global e-commerce sales around $6.3 trillion in 2024, giving buyers abundant alternatives and low switching costs that amplify bargaining power and pressure margins. Strong brands, seamless convenience and loyalty programs can reduce sensitivity by improving retention. Tengelmann's diversification across formats and geographies spreads demand and margin risk.

Co-investors and JV partners

Co-investors and JV partners can push for governance rights, management fees, and defined exit pathways; when their capital is required to close a Tengelmann transaction their bargaining power increases. Clear alignment on strategy and economics—demonstrated in 2024 by tighter governance clauses across European retail deals—reduces friction, while Tengelmann’s track record helps secure partner-friendly terms.

- Governance rights

- Fees & exit pathways

- Higher power when capital is critical

- 2024: tighter governance clauses in EU retail JVs

Institutional renters and operators

Institutional renters and master-lease operators exert strong bargaining power over Tengelmann by negotiating fee structures and strict performance clauses; their scale and local operating know-how enhance leverage, often dictating service levels and rent indexing. Performance-linked contracts can align incentives and reduce rent risk, while cultivating multiple operator relationships limits dependency and preserves negotiating leverage.

PE dry powder, e-commerce surge and rising vacancies intensify retail deal competition

Exit-market acquirers face >$2.2T private equity dry powder in 2024, boosting competition but increasing price sensitivity. German retail vacancy rose to ~5–6% in many secondary submarkets in 2024, strengthening tenant leverage. Global e-commerce sales hit ~$6.3T in 2024, raising end-customer price pressure; tighter JV governance clauses in EU retail deals in 2024 increased partner bargaining power.

| Buyer type | 2024 metric | Impact |

|---|---|---|

| PE/Strategic | $2.2T dry powder | ↑ competition, ↓ price |

| Tenants | 5–6% vacancy (secondary) | ↑ concessions |

| End-customers | $6.3T e‑commerce | ↑ price sensitivity |

| JV partners | Tighter governance | ↑ negotiation power |

What You See Is What You Get

Tengelmann Warenhandelsgesellschaft KG Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tengelmann Warenhandelsgesellschaft KG evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. It includes market context, evidence-based scoring, and implications for pricing, sourcing, and growth. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.