Teradata Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

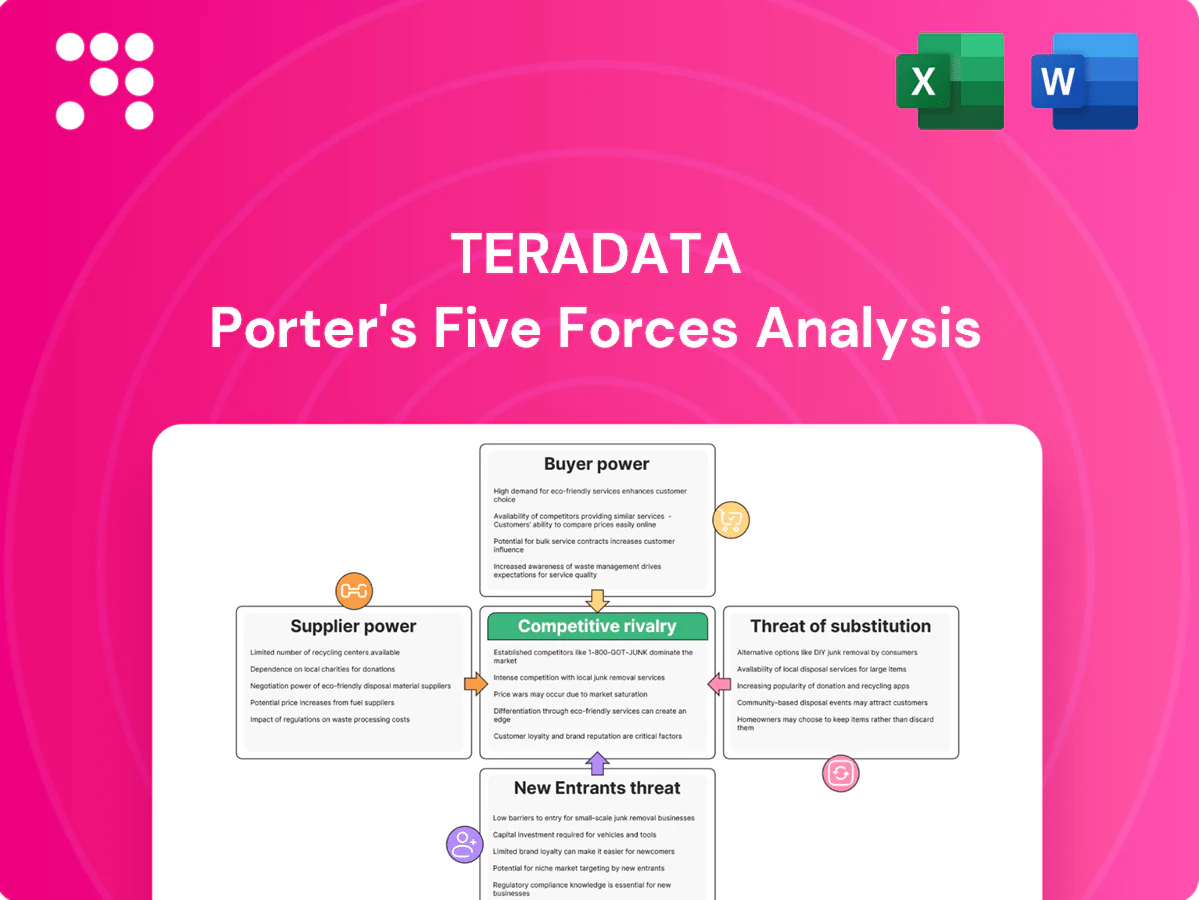

Teradata's Porter's Five Forces snapshot highlights moderate buyer power, intense competitive rivalry, rising threat from cloud-native entrants, limited supplier leverage, and evolving substitute threats from analytics platforms. This brief outlines strategic pressures and opportunities. Unlock the full Porter's Five Forces Analysis to explore Teradata’s competitive dynamics and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Teradata depends on AWS, Azure and Google Cloud to deliver Vantage in multi-cloud and as-a-service models, exposing it to the three hyperscalers that together held about 67% of the 2024 global IaaS/PaaS market. Concentration gives these partners leverage over pricing, roadmap alignment and go-to-market access, while co-selling incentives and marketplace terms can materially compress margins. Broad multi-cloud support mitigates but cannot eliminate supplier dependency risks.

Specialized hardware and chipset inputs

High-performance analytics relies on optimized CPUs, NVMe SSDs and high-throughput networking to deliver Teradata-class workloads, and supplier concentration in advanced chips and SSD controllers—with leading foundries and memory suppliers accounting for the majority of advanced-node and NAND capacity—creates price and lead-time pressure. Supply-chain volatility has historically pushed enterprise lead times into double-digit weeks, impacting delivery and service levels. Long-term procurement contracts and design abstraction (OEM flexibility) reduce exposure but cannot fully eliminate supplier power.

Open-source software ecosystems

Vantage integrates with and competes against open-source engines such as Apache Spark and Trino, and in 2024 these projects remained among the leading query/processing engines. While licensing costs are low, foundation stewards and community roadmaps materially shape interoperability and feature direction. Rapid OSS evolution forces Teradata to invest in compatibility, connectors and co-engineering, creating indirect supplier bargaining power via de facto standards.

Talent and specialized services

Expertise in distributed systems, cloud ops, and advanced analytics is scarce and highly mobile, giving engineers and data scientists strong negotiating leverage; median US data scientist base pay in 2024 hovered around 120,000–140,000 USD, pressuring margins and delivery timelines for Teradata. Offshore partners and services help diversify supply but retention and wage inflation remain material cost drivers.

- High bargaining power: skilled talent mobile

- 2024 pay range: US data scientists ~120k–140k USD

- Wage inflation increases delivery costs

- Offshore/partner ecosystems mitigate but do not eliminate risk

Third-party data center and network providers

Third-party colocation and network providers directly affect Teradata’s latency, resilience and unit costs: the global colocation market was about $75B in 2024 and the top 5 providers control roughly 60% of capacity, tightening pricing and SLA leverage.

Regional coverage and contractual SLAs constrain deployment flexibility, while carrier or facility consolidation has shifted bargaining power to fewer suppliers; cloud-first delivery reduces but does not eliminate dependency in hybrid setups.

- Latency/resilience impact

- Top-5 ~60% market share (2024)

- Global market ~$75B (2024)

- Hybrid still supplier-dependent

Hyperscaler and colocation concentration squeezes pricing, SLAs, and talent costs

Teradata faces concentrated supplier power: AWS/Azure/Google held ~67% of IaaS/PaaS (2024) and top-5 colocation providers ~60% of capacity, pressuring pricing and SLAs. Advanced chips/SSD supplier concentration and supply-chain lead times increase cost and delivery risk. OSS platforms and scarce analytics talent (US data scientist pay ~120–140k in 2024) add indirect leverage; contracts and OEM flexibility only partially mitigate.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | ~67% IaaS/PaaS | High pricing/go-to-market leverage |

| Colocation | $75B market; top-5 ~60% | SLA/pricing pressure |

| Talent | US pay $120–140k | Margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Teradata uncovering competitive drivers, buyer/supplier power, substitutes and entry risks, identifying disruptive threats and strategic defenses to protect market share.

Clean, one-sheet Teradata Porter’s Five Forces—instantly visualize competitive pressure with an editable radar chart and customizable force levels to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Concentrated enterprise customer base

Teradata’s concentrated enterprise customer base—chiefly Fortune-class global firms—drives strong buyer bargaining power; these customers account for over $1B in revenue in 2024 and commonly negotiate volume discounts of 10–20%, bespoke SLAs, and flexible consumption terms. High churn risk at renewal grants buyers added leverage. Referenceability needs often force additional concessions.

High but declining switching costs

Historic on-prem, proprietary workloads created strong stickiness for Teradata, but cloud-native architectures, open formats and ELT tools have lowered barriers; industry estimates in 2024 show enterprise cloud data migrations accelerating with roughly two-thirds of new analytics projects cloud-first. Buyers now phase workloads across platforms, boosting negotiating power and driving price sensitivity. Teradata reports 2024 cloud revenue and ARR growth in the low double digits and counters with migration tooling and workload portability to protect revenue and margins.

Price-performance and TCO sensitivity

Customers benchmark Vantage against Snowflake, Databricks and hyperscaler warehouses on unit economics—compute, storage and egress—and governance costs drive selection. Snowflake reported $2.07B revenue in FY2024, underscoring competitive scale buyers compare. Growing FinOps adoption makes cloud spend transparent and contestable, while outcome-based pricing and reserved-capacity discounts can blunt buyer leverage.

Demand for interoperability and openness

Enterprises demand open standards, multi-cloud flexibility and BI/AI integration, with 92% running multi-cloud (Flexera 2024); vendor lock-in concerns drive tougher contractual and technical requirements, while compliance and data sovereignty add negotiation leverage, often forcing vendors to trade margin for customer stickiness.

- Open standards & APIs

- Multi-cloud (92% multi-cloud use)

- Compliance/data sovereignty as bargaining chips

Criticality of analytics to business outcomes

Analytics platforms underpin revenue, risk and operations; with the global analytics market near USD 300 billion in 2024, Vantage is often mission-critical so buyers prioritize reliability and performance over pure price, limiting buyer power for high-stakes workloads. Non-critical workloads remain price-elastic and contestable, keeping some negotiating leverage.

- Mission-critical: high switching costs, premium SLAs

- High-stakes: lower buyer power

- Non-critical: price-sensitive, contestable

Enterprise-heavy analytics vendor faces buyer leverage from cloud-first and multi-cloud trends

Teradata’s concentrated enterprise base (>$1B customers) yields strong buyer leverage—10–20% volume discounts, bespoke SLAs and renewal churn risk. Cloud-first shift (≈66% of new analytics projects, 2024) plus 92% multi-cloud use raises price sensitivity vs mission-critical workloads. Buyers benchmark unit economics vs Snowflake ($2.07B FY2024) and Databricks, driving concessions on pricing and portability.

| Metric | 2024 Value |

|---|---|

| Top customers revenue | >$1B |

| Discounts | 10–20% |

| Cloud-first projects | ≈66% |

| Multi-cloud | 92% |

| Snowflake revenue | $2.07B |

Preview Before You Purchase

Teradata Porter's Five Forces Analysis

This preview shows the exact Teradata Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted and professionally written for immediate download and use. It provides a comprehensive assessment of competitive rivalry, threat of new entrants, buyer and supplier power, and substitution risk.

A Must-Have Tool for Decision-Makers

Teradata's Porter's Five Forces snapshot highlights moderate buyer power, intense competitive rivalry, rising threat from cloud-native entrants, limited supplier leverage, and evolving substitute threats from analytics platforms. This brief outlines strategic pressures and opportunities. Unlock the full Porter's Five Forces Analysis to explore Teradata’s competitive dynamics and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Teradata depends on AWS, Azure and Google Cloud to deliver Vantage in multi-cloud and as-a-service models, exposing it to the three hyperscalers that together held about 67% of the 2024 global IaaS/PaaS market. Concentration gives these partners leverage over pricing, roadmap alignment and go-to-market access, while co-selling incentives and marketplace terms can materially compress margins. Broad multi-cloud support mitigates but cannot eliminate supplier dependency risks.

Specialized hardware and chipset inputs

High-performance analytics relies on optimized CPUs, NVMe SSDs and high-throughput networking to deliver Teradata-class workloads, and supplier concentration in advanced chips and SSD controllers—with leading foundries and memory suppliers accounting for the majority of advanced-node and NAND capacity—creates price and lead-time pressure. Supply-chain volatility has historically pushed enterprise lead times into double-digit weeks, impacting delivery and service levels. Long-term procurement contracts and design abstraction (OEM flexibility) reduce exposure but cannot fully eliminate supplier power.

Open-source software ecosystems

Vantage integrates with and competes against open-source engines such as Apache Spark and Trino, and in 2024 these projects remained among the leading query/processing engines. While licensing costs are low, foundation stewards and community roadmaps materially shape interoperability and feature direction. Rapid OSS evolution forces Teradata to invest in compatibility, connectors and co-engineering, creating indirect supplier bargaining power via de facto standards.

Talent and specialized services

Expertise in distributed systems, cloud ops, and advanced analytics is scarce and highly mobile, giving engineers and data scientists strong negotiating leverage; median US data scientist base pay in 2024 hovered around 120,000–140,000 USD, pressuring margins and delivery timelines for Teradata. Offshore partners and services help diversify supply but retention and wage inflation remain material cost drivers.

- High bargaining power: skilled talent mobile

- 2024 pay range: US data scientists ~120k–140k USD

- Wage inflation increases delivery costs

- Offshore/partner ecosystems mitigate but do not eliminate risk

Third-party data center and network providers

Third-party colocation and network providers directly affect Teradata’s latency, resilience and unit costs: the global colocation market was about $75B in 2024 and the top 5 providers control roughly 60% of capacity, tightening pricing and SLA leverage.

Regional coverage and contractual SLAs constrain deployment flexibility, while carrier or facility consolidation has shifted bargaining power to fewer suppliers; cloud-first delivery reduces but does not eliminate dependency in hybrid setups.

- Latency/resilience impact

- Top-5 ~60% market share (2024)

- Global market ~$75B (2024)

- Hybrid still supplier-dependent

Hyperscaler and colocation concentration squeezes pricing, SLAs, and talent costs

Teradata faces concentrated supplier power: AWS/Azure/Google held ~67% of IaaS/PaaS (2024) and top-5 colocation providers ~60% of capacity, pressuring pricing and SLAs. Advanced chips/SSD supplier concentration and supply-chain lead times increase cost and delivery risk. OSS platforms and scarce analytics talent (US data scientist pay ~120–140k in 2024) add indirect leverage; contracts and OEM flexibility only partially mitigate.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | ~67% IaaS/PaaS | High pricing/go-to-market leverage |

| Colocation | $75B market; top-5 ~60% | SLA/pricing pressure |

| Talent | US pay $120–140k | Margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Teradata uncovering competitive drivers, buyer/supplier power, substitutes and entry risks, identifying disruptive threats and strategic defenses to protect market share.

Clean, one-sheet Teradata Porter’s Five Forces—instantly visualize competitive pressure with an editable radar chart and customizable force levels to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Concentrated enterprise customer base

Teradata’s concentrated enterprise customer base—chiefly Fortune-class global firms—drives strong buyer bargaining power; these customers account for over $1B in revenue in 2024 and commonly negotiate volume discounts of 10–20%, bespoke SLAs, and flexible consumption terms. High churn risk at renewal grants buyers added leverage. Referenceability needs often force additional concessions.

High but declining switching costs

Historic on-prem, proprietary workloads created strong stickiness for Teradata, but cloud-native architectures, open formats and ELT tools have lowered barriers; industry estimates in 2024 show enterprise cloud data migrations accelerating with roughly two-thirds of new analytics projects cloud-first. Buyers now phase workloads across platforms, boosting negotiating power and driving price sensitivity. Teradata reports 2024 cloud revenue and ARR growth in the low double digits and counters with migration tooling and workload portability to protect revenue and margins.

Price-performance and TCO sensitivity

Customers benchmark Vantage against Snowflake, Databricks and hyperscaler warehouses on unit economics—compute, storage and egress—and governance costs drive selection. Snowflake reported $2.07B revenue in FY2024, underscoring competitive scale buyers compare. Growing FinOps adoption makes cloud spend transparent and contestable, while outcome-based pricing and reserved-capacity discounts can blunt buyer leverage.

Demand for interoperability and openness

Enterprises demand open standards, multi-cloud flexibility and BI/AI integration, with 92% running multi-cloud (Flexera 2024); vendor lock-in concerns drive tougher contractual and technical requirements, while compliance and data sovereignty add negotiation leverage, often forcing vendors to trade margin for customer stickiness.

- Open standards & APIs

- Multi-cloud (92% multi-cloud use)

- Compliance/data sovereignty as bargaining chips

Criticality of analytics to business outcomes

Analytics platforms underpin revenue, risk and operations; with the global analytics market near USD 300 billion in 2024, Vantage is often mission-critical so buyers prioritize reliability and performance over pure price, limiting buyer power for high-stakes workloads. Non-critical workloads remain price-elastic and contestable, keeping some negotiating leverage.

- Mission-critical: high switching costs, premium SLAs

- High-stakes: lower buyer power

- Non-critical: price-sensitive, contestable

Enterprise-heavy analytics vendor faces buyer leverage from cloud-first and multi-cloud trends

Teradata’s concentrated enterprise base (>$1B customers) yields strong buyer leverage—10–20% volume discounts, bespoke SLAs and renewal churn risk. Cloud-first shift (≈66% of new analytics projects, 2024) plus 92% multi-cloud use raises price sensitivity vs mission-critical workloads. Buyers benchmark unit economics vs Snowflake ($2.07B FY2024) and Databricks, driving concessions on pricing and portability.

| Metric | 2024 Value |

|---|---|

| Top customers revenue | >$1B |

| Discounts | 10–20% |

| Cloud-first projects | ≈66% |

| Multi-cloud | 92% |

| Snowflake revenue | $2.07B |

Preview Before You Purchase

Teradata Porter's Five Forces Analysis

This preview shows the exact Teradata Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted and professionally written for immediate download and use. It provides a comprehensive assessment of competitive rivalry, threat of new entrants, buyer and supplier power, and substitution risk.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Teradata's Porter's Five Forces snapshot highlights moderate buyer power, intense competitive rivalry, rising threat from cloud-native entrants, limited supplier leverage, and evolving substitute threats from analytics platforms. This brief outlines strategic pressures and opportunities. Unlock the full Porter's Five Forces Analysis to explore Teradata’s competitive dynamics and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Teradata depends on AWS, Azure and Google Cloud to deliver Vantage in multi-cloud and as-a-service models, exposing it to the three hyperscalers that together held about 67% of the 2024 global IaaS/PaaS market. Concentration gives these partners leverage over pricing, roadmap alignment and go-to-market access, while co-selling incentives and marketplace terms can materially compress margins. Broad multi-cloud support mitigates but cannot eliminate supplier dependency risks.

Specialized hardware and chipset inputs

High-performance analytics relies on optimized CPUs, NVMe SSDs and high-throughput networking to deliver Teradata-class workloads, and supplier concentration in advanced chips and SSD controllers—with leading foundries and memory suppliers accounting for the majority of advanced-node and NAND capacity—creates price and lead-time pressure. Supply-chain volatility has historically pushed enterprise lead times into double-digit weeks, impacting delivery and service levels. Long-term procurement contracts and design abstraction (OEM flexibility) reduce exposure but cannot fully eliminate supplier power.

Open-source software ecosystems

Vantage integrates with and competes against open-source engines such as Apache Spark and Trino, and in 2024 these projects remained among the leading query/processing engines. While licensing costs are low, foundation stewards and community roadmaps materially shape interoperability and feature direction. Rapid OSS evolution forces Teradata to invest in compatibility, connectors and co-engineering, creating indirect supplier bargaining power via de facto standards.

Talent and specialized services

Expertise in distributed systems, cloud ops, and advanced analytics is scarce and highly mobile, giving engineers and data scientists strong negotiating leverage; median US data scientist base pay in 2024 hovered around 120,000–140,000 USD, pressuring margins and delivery timelines for Teradata. Offshore partners and services help diversify supply but retention and wage inflation remain material cost drivers.

- High bargaining power: skilled talent mobile

- 2024 pay range: US data scientists ~120k–140k USD

- Wage inflation increases delivery costs

- Offshore/partner ecosystems mitigate but do not eliminate risk

Third-party data center and network providers

Third-party colocation and network providers directly affect Teradata’s latency, resilience and unit costs: the global colocation market was about $75B in 2024 and the top 5 providers control roughly 60% of capacity, tightening pricing and SLA leverage.

Regional coverage and contractual SLAs constrain deployment flexibility, while carrier or facility consolidation has shifted bargaining power to fewer suppliers; cloud-first delivery reduces but does not eliminate dependency in hybrid setups.

- Latency/resilience impact

- Top-5 ~60% market share (2024)

- Global market ~$75B (2024)

- Hybrid still supplier-dependent

Hyperscaler and colocation concentration squeezes pricing, SLAs, and talent costs

Teradata faces concentrated supplier power: AWS/Azure/Google held ~67% of IaaS/PaaS (2024) and top-5 colocation providers ~60% of capacity, pressuring pricing and SLAs. Advanced chips/SSD supplier concentration and supply-chain lead times increase cost and delivery risk. OSS platforms and scarce analytics talent (US data scientist pay ~120–140k in 2024) add indirect leverage; contracts and OEM flexibility only partially mitigate.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | ~67% IaaS/PaaS | High pricing/go-to-market leverage |

| Colocation | $75B market; top-5 ~60% | SLA/pricing pressure |

| Talent | US pay $120–140k | Margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Teradata uncovering competitive drivers, buyer/supplier power, substitutes and entry risks, identifying disruptive threats and strategic defenses to protect market share.

Clean, one-sheet Teradata Porter’s Five Forces—instantly visualize competitive pressure with an editable radar chart and customizable force levels to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Concentrated enterprise customer base

Teradata’s concentrated enterprise customer base—chiefly Fortune-class global firms—drives strong buyer bargaining power; these customers account for over $1B in revenue in 2024 and commonly negotiate volume discounts of 10–20%, bespoke SLAs, and flexible consumption terms. High churn risk at renewal grants buyers added leverage. Referenceability needs often force additional concessions.

High but declining switching costs

Historic on-prem, proprietary workloads created strong stickiness for Teradata, but cloud-native architectures, open formats and ELT tools have lowered barriers; industry estimates in 2024 show enterprise cloud data migrations accelerating with roughly two-thirds of new analytics projects cloud-first. Buyers now phase workloads across platforms, boosting negotiating power and driving price sensitivity. Teradata reports 2024 cloud revenue and ARR growth in the low double digits and counters with migration tooling and workload portability to protect revenue and margins.

Price-performance and TCO sensitivity

Customers benchmark Vantage against Snowflake, Databricks and hyperscaler warehouses on unit economics—compute, storage and egress—and governance costs drive selection. Snowflake reported $2.07B revenue in FY2024, underscoring competitive scale buyers compare. Growing FinOps adoption makes cloud spend transparent and contestable, while outcome-based pricing and reserved-capacity discounts can blunt buyer leverage.

Demand for interoperability and openness

Enterprises demand open standards, multi-cloud flexibility and BI/AI integration, with 92% running multi-cloud (Flexera 2024); vendor lock-in concerns drive tougher contractual and technical requirements, while compliance and data sovereignty add negotiation leverage, often forcing vendors to trade margin for customer stickiness.

- Open standards & APIs

- Multi-cloud (92% multi-cloud use)

- Compliance/data sovereignty as bargaining chips

Criticality of analytics to business outcomes

Analytics platforms underpin revenue, risk and operations; with the global analytics market near USD 300 billion in 2024, Vantage is often mission-critical so buyers prioritize reliability and performance over pure price, limiting buyer power for high-stakes workloads. Non-critical workloads remain price-elastic and contestable, keeping some negotiating leverage.

- Mission-critical: high switching costs, premium SLAs

- High-stakes: lower buyer power

- Non-critical: price-sensitive, contestable

Enterprise-heavy analytics vendor faces buyer leverage from cloud-first and multi-cloud trends

Teradata’s concentrated enterprise base (>$1B customers) yields strong buyer leverage—10–20% volume discounts, bespoke SLAs and renewal churn risk. Cloud-first shift (≈66% of new analytics projects, 2024) plus 92% multi-cloud use raises price sensitivity vs mission-critical workloads. Buyers benchmark unit economics vs Snowflake ($2.07B FY2024) and Databricks, driving concessions on pricing and portability.

| Metric | 2024 Value |

|---|---|

| Top customers revenue | >$1B |

| Discounts | 10–20% |

| Cloud-first projects | ≈66% |

| Multi-cloud | 92% |

| Snowflake revenue | $2.07B |

Preview Before You Purchase

Teradata Porter's Five Forces Analysis

This preview shows the exact Teradata Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted and professionally written for immediate download and use. It provides a comprehensive assessment of competitive rivalry, threat of new entrants, buyer and supplier power, and substitution risk.