Teradyne Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

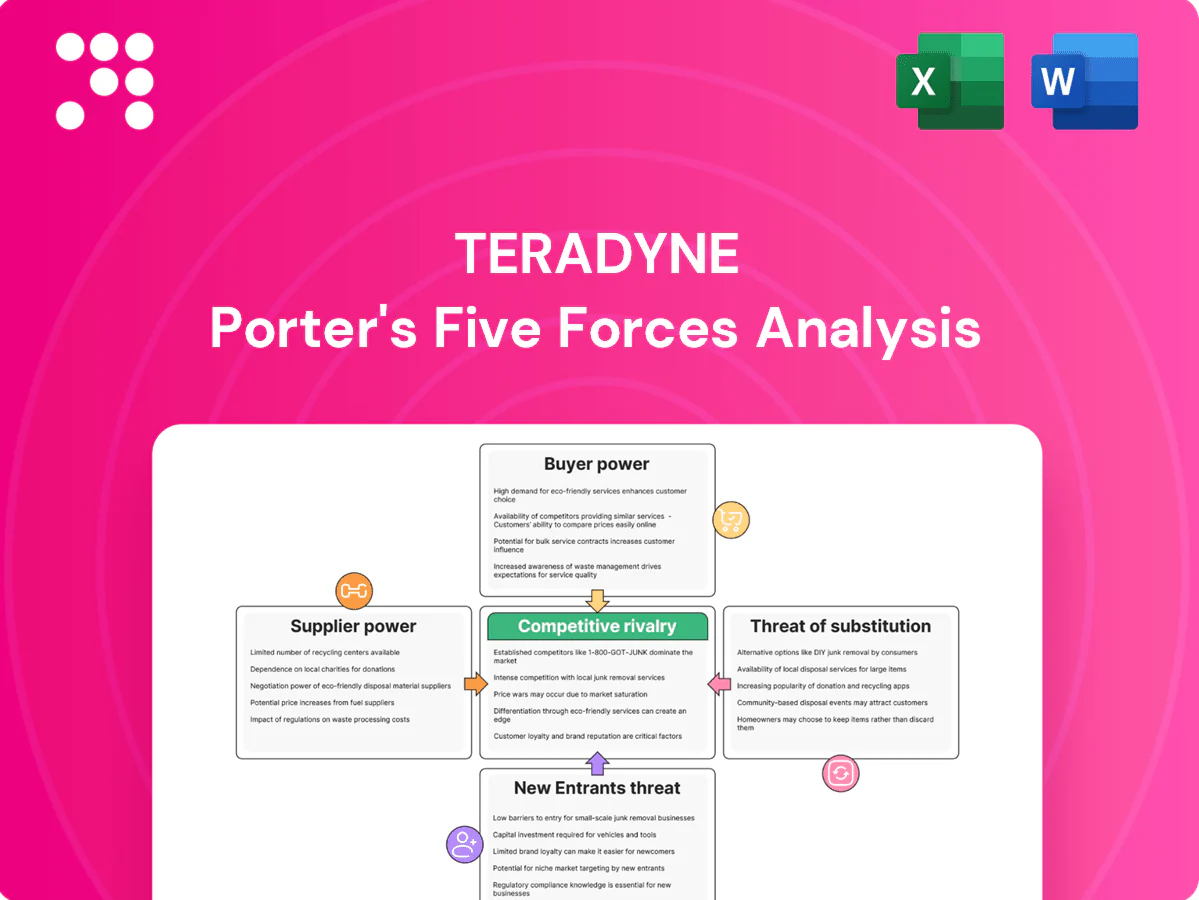

Teradyne’s Porter's Five Forces snapshot highlights strong buyer power, moderate supplier constraints, and significant rivalry driven by tech innovation and scale. It flags emerging substitute threats and the manageable risk of new entrants given capital intensity. This brief teases strategic implications—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

ATE and cobot designs demand high-spec ASICs, FPGAs, RF front-ends, precision analog and metrology parts from few qualified suppliers; in 2024 many such items faced lead times exceeding 26 weeks, pushing pricing and allocation pressure. Qualification cycles of 6–12 months make supplier switches costly, leaving concentrated vendors with moderate leverage over cost and availability.

Foundry and advanced packaging exposure

Teradyne’s custom silicon depends on leading foundries/OSATs where 2024 industry shares concentrate — TSMC ~56% of global foundry capacity and utilization near 100% — so wafer price/cycle-time shocks and slow, costly re-qualification across nodes raise upstream supplier bargaining power and squeeze product margins.

Geopolitical and compliance constraints

Export controls and sanctions through 2024—notably US restrictions on advanced AI and semiconductor exports—have tightened sourcing for test equipment components, narrowing vendor pools and complicating cross‑border logistics.

Compliance burdens raise due‑diligence costs and favor suppliers in compliant jurisdictions, letting those vendors command better terms and faster lead times.

Regulatory friction has effectively elevated supplier influence during procurement, increasing Teradyne’s supply risk and procurement margins pressure.

Mitigation via scale and long-term agreements

Teradyne’s global volume and multi-year supply agreements—supporting a 2024 revenue of about $3.1 billion—plus improved forecasting temper supplier leverage, while dual-sourcing and inventory buffers reduce single-point risk where feasible. Co-development partnerships align roadmaps and secure priority, yet suppliers of scarce process nodes and specialized test components retain significant bargaining power.

- Global volume: 2024 revenue ~ $3.1B

- Risk control: dual-sourcing, inventory buffers

- Strategic: multi-year agreements, co-development

- Limit: scarce technologies still hold leverage

High qualification and switching costs

Precision parts for Teradyne must pass rigorous reliability, temperature and signal-integrity tests, with supplier qualification typically taking 6–12 months in 2024. Redesigns to onboard new vendors can delay time-to-market and impair performance, creating switching frictions that lock incumbents, so supplier bargaining power is structurally higher in critical categories.

- qualification: 6–12 months (2024)

- redesigns add weeks–months to NPI

- incumbent lock-in → higher supplier power

Concentrated suppliers, >26-week lead times and 6–12m quals amplify supplier leverage; foundry ~56%

Critical ATE/cobot components come from few qualified suppliers; 2024 lead times >26 weeks and 6–12 month qualification cycles raise switching costs and supplier leverage. TSMC ~56% foundry share and near 100% utilization in 2024 amplify price and cycle risks despite Teradyne revenue ~$3.1B and multi‑year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $3.1B |

| TSMC share | ~56% |

| Lead times | >26 weeks |

| Qualify time | 6–12 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Teradyne that uncovers competitive intensity, supplier and buyer power, and risks from new entrants and substitutes, highlighting strategic levers to protect margins and sustain market position.

A concise one-sheet Porter's Five Forces for Teradyne that maps supplier and buyer power, competitive rivalry, substitute threats and entry barriers—perfect for quick strategic decisions, board decks, and adapting pressure levels as market or tech shifts occur.

Customers Bargaining Power

Concentrated, sophisticated customers

IDMs, foundries, fabless leaders, OSATs and top OEMs account for the bulk of Teradyne demand, with TSMC alone holding about 54% of global foundry revenue in 2024. These buyers run competitive tenders and rigorously benchmark total cost of test, not just equipment price. Their scale enables aggressive pricing, longer payment terms and service demands. Concentration amplifies buyer leverage in downturns, pressuring margins and order visibility.

High switching costs and installed-base lock-in

Test programs, handler interfaces, load boards and operator training embed customers in Teradyne platforms, making migration to rival ATE costly due to requalification, downtime and engineering effort. Lifecycle services and spares further deepen installed-base lock-in, reducing buyers' leverage. This dampens customer bargaining power when performance differentiation is critical.

Cyclical capex timing

Semicap cycles create feast-or-famine buying windows: in soft periods customers delay orders to extract discounts and stricter SLAs, while in tight markets delivery assurance can trump price. Buyer leverage swung with 2024 wafer demand recovery; SEMI estimated global WFE spending around $68 billion in 2024, so power shifts with wafer demand and node transitions where leading-edge nodes tighten supply.

Outcome-based value focus

Buyers prioritize throughput, parallelism, coverage, and cost of test per device, so demonstrable yield gains or faster time-to-ramp materially reduce price sensitivity and increase willingness to pay for Teradyne systems.

If Teradyne performance gaps vs competitors narrow, buyer price pressure intensifies as switching costs fall; strong outcome-focused messaging can blunt but not eliminate buyer leverage.

- Outcome focus: throughput, parallelism, coverage, test cost

- Buyer leverage rises as performance gaps close

- Yield/time-to-ramp improvements lower price sensitivity

- Value messaging mitigates but does not remove leverage

Alternative procurement via services/used gear

OSAT services and a growing secondary market of used testers gave buyers more negotiation leverage in 2024, with refurbished equipment meeting many mature-node test needs at discounts commonly cited between 30-60%, strengthening buyers' bargaining power against new-system pricing. Teradyne defends margins via bundled warranties, software subscriptions and turnkey integration that capture service revenue and stickiness.

- 2024: refurbished testers often 30-60% cheaper

- OSAT/aftermarket increased buyer optionality

- Teradyne offsets via warranties, SW, integration

Buyer leverage climbs as foundry concentration and refurbished testers boost optionality

Customer power is high: TSMC held about 54% of foundry revenue in 2024 and large IDMs/OEMs run aggressive tenders, squeezing price, terms and service. High switching costs from fixtures, load boards and services reduce leverage, but refurbished testers (30-60% cheaper) and OSATs raise buyer optionality. Cyclical WFE ($68B in 2024) shifts bargaining power with demand.

| Metric | 2024 value | Impact |

|---|---|---|

| TSMC share | ~54% | Concentrated buyer power |

| Global WFE | $68B | Power shifts with cycle |

| Refurb discount | 30-60% | Increases buyer leverage |

Preview Before You Purchase

Teradyne Porter's Five Forces Analysis

This preview shows the exact Teradyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file you’ll get—ready for download and use the moment you buy. You're viewing the final deliverable, ready for immediate application in due diligence or strategic planning.

A Must-Have Tool for Decision-Makers

Teradyne’s Porter's Five Forces snapshot highlights strong buyer power, moderate supplier constraints, and significant rivalry driven by tech innovation and scale. It flags emerging substitute threats and the manageable risk of new entrants given capital intensity. This brief teases strategic implications—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

ATE and cobot designs demand high-spec ASICs, FPGAs, RF front-ends, precision analog and metrology parts from few qualified suppliers; in 2024 many such items faced lead times exceeding 26 weeks, pushing pricing and allocation pressure. Qualification cycles of 6–12 months make supplier switches costly, leaving concentrated vendors with moderate leverage over cost and availability.

Foundry and advanced packaging exposure

Teradyne’s custom silicon depends on leading foundries/OSATs where 2024 industry shares concentrate — TSMC ~56% of global foundry capacity and utilization near 100% — so wafer price/cycle-time shocks and slow, costly re-qualification across nodes raise upstream supplier bargaining power and squeeze product margins.

Geopolitical and compliance constraints

Export controls and sanctions through 2024—notably US restrictions on advanced AI and semiconductor exports—have tightened sourcing for test equipment components, narrowing vendor pools and complicating cross‑border logistics.

Compliance burdens raise due‑diligence costs and favor suppliers in compliant jurisdictions, letting those vendors command better terms and faster lead times.

Regulatory friction has effectively elevated supplier influence during procurement, increasing Teradyne’s supply risk and procurement margins pressure.

Mitigation via scale and long-term agreements

Teradyne’s global volume and multi-year supply agreements—supporting a 2024 revenue of about $3.1 billion—plus improved forecasting temper supplier leverage, while dual-sourcing and inventory buffers reduce single-point risk where feasible. Co-development partnerships align roadmaps and secure priority, yet suppliers of scarce process nodes and specialized test components retain significant bargaining power.

- Global volume: 2024 revenue ~ $3.1B

- Risk control: dual-sourcing, inventory buffers

- Strategic: multi-year agreements, co-development

- Limit: scarce technologies still hold leverage

High qualification and switching costs

Precision parts for Teradyne must pass rigorous reliability, temperature and signal-integrity tests, with supplier qualification typically taking 6–12 months in 2024. Redesigns to onboard new vendors can delay time-to-market and impair performance, creating switching frictions that lock incumbents, so supplier bargaining power is structurally higher in critical categories.

- qualification: 6–12 months (2024)

- redesigns add weeks–months to NPI

- incumbent lock-in → higher supplier power

Concentrated suppliers, >26-week lead times and 6–12m quals amplify supplier leverage; foundry ~56%

Critical ATE/cobot components come from few qualified suppliers; 2024 lead times >26 weeks and 6–12 month qualification cycles raise switching costs and supplier leverage. TSMC ~56% foundry share and near 100% utilization in 2024 amplify price and cycle risks despite Teradyne revenue ~$3.1B and multi‑year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $3.1B |

| TSMC share | ~56% |

| Lead times | >26 weeks |

| Qualify time | 6–12 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Teradyne that uncovers competitive intensity, supplier and buyer power, and risks from new entrants and substitutes, highlighting strategic levers to protect margins and sustain market position.

A concise one-sheet Porter's Five Forces for Teradyne that maps supplier and buyer power, competitive rivalry, substitute threats and entry barriers—perfect for quick strategic decisions, board decks, and adapting pressure levels as market or tech shifts occur.

Customers Bargaining Power

Concentrated, sophisticated customers

IDMs, foundries, fabless leaders, OSATs and top OEMs account for the bulk of Teradyne demand, with TSMC alone holding about 54% of global foundry revenue in 2024. These buyers run competitive tenders and rigorously benchmark total cost of test, not just equipment price. Their scale enables aggressive pricing, longer payment terms and service demands. Concentration amplifies buyer leverage in downturns, pressuring margins and order visibility.

High switching costs and installed-base lock-in

Test programs, handler interfaces, load boards and operator training embed customers in Teradyne platforms, making migration to rival ATE costly due to requalification, downtime and engineering effort. Lifecycle services and spares further deepen installed-base lock-in, reducing buyers' leverage. This dampens customer bargaining power when performance differentiation is critical.

Cyclical capex timing

Semicap cycles create feast-or-famine buying windows: in soft periods customers delay orders to extract discounts and stricter SLAs, while in tight markets delivery assurance can trump price. Buyer leverage swung with 2024 wafer demand recovery; SEMI estimated global WFE spending around $68 billion in 2024, so power shifts with wafer demand and node transitions where leading-edge nodes tighten supply.

Outcome-based value focus

Buyers prioritize throughput, parallelism, coverage, and cost of test per device, so demonstrable yield gains or faster time-to-ramp materially reduce price sensitivity and increase willingness to pay for Teradyne systems.

If Teradyne performance gaps vs competitors narrow, buyer price pressure intensifies as switching costs fall; strong outcome-focused messaging can blunt but not eliminate buyer leverage.

- Outcome focus: throughput, parallelism, coverage, test cost

- Buyer leverage rises as performance gaps close

- Yield/time-to-ramp improvements lower price sensitivity

- Value messaging mitigates but does not remove leverage

Alternative procurement via services/used gear

OSAT services and a growing secondary market of used testers gave buyers more negotiation leverage in 2024, with refurbished equipment meeting many mature-node test needs at discounts commonly cited between 30-60%, strengthening buyers' bargaining power against new-system pricing. Teradyne defends margins via bundled warranties, software subscriptions and turnkey integration that capture service revenue and stickiness.

- 2024: refurbished testers often 30-60% cheaper

- OSAT/aftermarket increased buyer optionality

- Teradyne offsets via warranties, SW, integration

Buyer leverage climbs as foundry concentration and refurbished testers boost optionality

Customer power is high: TSMC held about 54% of foundry revenue in 2024 and large IDMs/OEMs run aggressive tenders, squeezing price, terms and service. High switching costs from fixtures, load boards and services reduce leverage, but refurbished testers (30-60% cheaper) and OSATs raise buyer optionality. Cyclical WFE ($68B in 2024) shifts bargaining power with demand.

| Metric | 2024 value | Impact |

|---|---|---|

| TSMC share | ~54% | Concentrated buyer power |

| Global WFE | $68B | Power shifts with cycle |

| Refurb discount | 30-60% | Increases buyer leverage |

Preview Before You Purchase

Teradyne Porter's Five Forces Analysis

This preview shows the exact Teradyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file you’ll get—ready for download and use the moment you buy. You're viewing the final deliverable, ready for immediate application in due diligence or strategic planning.

Description

A Must-Have Tool for Decision-Makers

Teradyne’s Porter's Five Forces snapshot highlights strong buyer power, moderate supplier constraints, and significant rivalry driven by tech innovation and scale. It flags emerging substitute threats and the manageable risk of new entrants given capital intensity. This brief teases strategic implications—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

ATE and cobot designs demand high-spec ASICs, FPGAs, RF front-ends, precision analog and metrology parts from few qualified suppliers; in 2024 many such items faced lead times exceeding 26 weeks, pushing pricing and allocation pressure. Qualification cycles of 6–12 months make supplier switches costly, leaving concentrated vendors with moderate leverage over cost and availability.

Foundry and advanced packaging exposure

Teradyne’s custom silicon depends on leading foundries/OSATs where 2024 industry shares concentrate — TSMC ~56% of global foundry capacity and utilization near 100% — so wafer price/cycle-time shocks and slow, costly re-qualification across nodes raise upstream supplier bargaining power and squeeze product margins.

Geopolitical and compliance constraints

Export controls and sanctions through 2024—notably US restrictions on advanced AI and semiconductor exports—have tightened sourcing for test equipment components, narrowing vendor pools and complicating cross‑border logistics.

Compliance burdens raise due‑diligence costs and favor suppliers in compliant jurisdictions, letting those vendors command better terms and faster lead times.

Regulatory friction has effectively elevated supplier influence during procurement, increasing Teradyne’s supply risk and procurement margins pressure.

Mitigation via scale and long-term agreements

Teradyne’s global volume and multi-year supply agreements—supporting a 2024 revenue of about $3.1 billion—plus improved forecasting temper supplier leverage, while dual-sourcing and inventory buffers reduce single-point risk where feasible. Co-development partnerships align roadmaps and secure priority, yet suppliers of scarce process nodes and specialized test components retain significant bargaining power.

- Global volume: 2024 revenue ~ $3.1B

- Risk control: dual-sourcing, inventory buffers

- Strategic: multi-year agreements, co-development

- Limit: scarce technologies still hold leverage

High qualification and switching costs

Precision parts for Teradyne must pass rigorous reliability, temperature and signal-integrity tests, with supplier qualification typically taking 6–12 months in 2024. Redesigns to onboard new vendors can delay time-to-market and impair performance, creating switching frictions that lock incumbents, so supplier bargaining power is structurally higher in critical categories.

- qualification: 6–12 months (2024)

- redesigns add weeks–months to NPI

- incumbent lock-in → higher supplier power

Concentrated suppliers, >26-week lead times and 6–12m quals amplify supplier leverage; foundry ~56%

Critical ATE/cobot components come from few qualified suppliers; 2024 lead times >26 weeks and 6–12 month qualification cycles raise switching costs and supplier leverage. TSMC ~56% foundry share and near 100% utilization in 2024 amplify price and cycle risks despite Teradyne revenue ~$3.1B and multi‑year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $3.1B |

| TSMC share | ~56% |

| Lead times | >26 weeks |

| Qualify time | 6–12 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Teradyne that uncovers competitive intensity, supplier and buyer power, and risks from new entrants and substitutes, highlighting strategic levers to protect margins and sustain market position.

A concise one-sheet Porter's Five Forces for Teradyne that maps supplier and buyer power, competitive rivalry, substitute threats and entry barriers—perfect for quick strategic decisions, board decks, and adapting pressure levels as market or tech shifts occur.

Customers Bargaining Power

Concentrated, sophisticated customers

IDMs, foundries, fabless leaders, OSATs and top OEMs account for the bulk of Teradyne demand, with TSMC alone holding about 54% of global foundry revenue in 2024. These buyers run competitive tenders and rigorously benchmark total cost of test, not just equipment price. Their scale enables aggressive pricing, longer payment terms and service demands. Concentration amplifies buyer leverage in downturns, pressuring margins and order visibility.

High switching costs and installed-base lock-in

Test programs, handler interfaces, load boards and operator training embed customers in Teradyne platforms, making migration to rival ATE costly due to requalification, downtime and engineering effort. Lifecycle services and spares further deepen installed-base lock-in, reducing buyers' leverage. This dampens customer bargaining power when performance differentiation is critical.

Cyclical capex timing

Semicap cycles create feast-or-famine buying windows: in soft periods customers delay orders to extract discounts and stricter SLAs, while in tight markets delivery assurance can trump price. Buyer leverage swung with 2024 wafer demand recovery; SEMI estimated global WFE spending around $68 billion in 2024, so power shifts with wafer demand and node transitions where leading-edge nodes tighten supply.

Outcome-based value focus

Buyers prioritize throughput, parallelism, coverage, and cost of test per device, so demonstrable yield gains or faster time-to-ramp materially reduce price sensitivity and increase willingness to pay for Teradyne systems.

If Teradyne performance gaps vs competitors narrow, buyer price pressure intensifies as switching costs fall; strong outcome-focused messaging can blunt but not eliminate buyer leverage.

- Outcome focus: throughput, parallelism, coverage, test cost

- Buyer leverage rises as performance gaps close

- Yield/time-to-ramp improvements lower price sensitivity

- Value messaging mitigates but does not remove leverage

Alternative procurement via services/used gear

OSAT services and a growing secondary market of used testers gave buyers more negotiation leverage in 2024, with refurbished equipment meeting many mature-node test needs at discounts commonly cited between 30-60%, strengthening buyers' bargaining power against new-system pricing. Teradyne defends margins via bundled warranties, software subscriptions and turnkey integration that capture service revenue and stickiness.

- 2024: refurbished testers often 30-60% cheaper

- OSAT/aftermarket increased buyer optionality

- Teradyne offsets via warranties, SW, integration

Buyer leverage climbs as foundry concentration and refurbished testers boost optionality

Customer power is high: TSMC held about 54% of foundry revenue in 2024 and large IDMs/OEMs run aggressive tenders, squeezing price, terms and service. High switching costs from fixtures, load boards and services reduce leverage, but refurbished testers (30-60% cheaper) and OSATs raise buyer optionality. Cyclical WFE ($68B in 2024) shifts bargaining power with demand.

| Metric | 2024 value | Impact |

|---|---|---|

| TSMC share | ~54% | Concentrated buyer power |

| Global WFE | $68B | Power shifts with cycle |

| Refurb discount | 30-60% | Increases buyer leverage |

Preview Before You Purchase

Teradyne Porter's Five Forces Analysis

This preview shows the exact Teradyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file you’ll get—ready for download and use the moment you buy. You're viewing the final deliverable, ready for immediate application in due diligence or strategic planning.