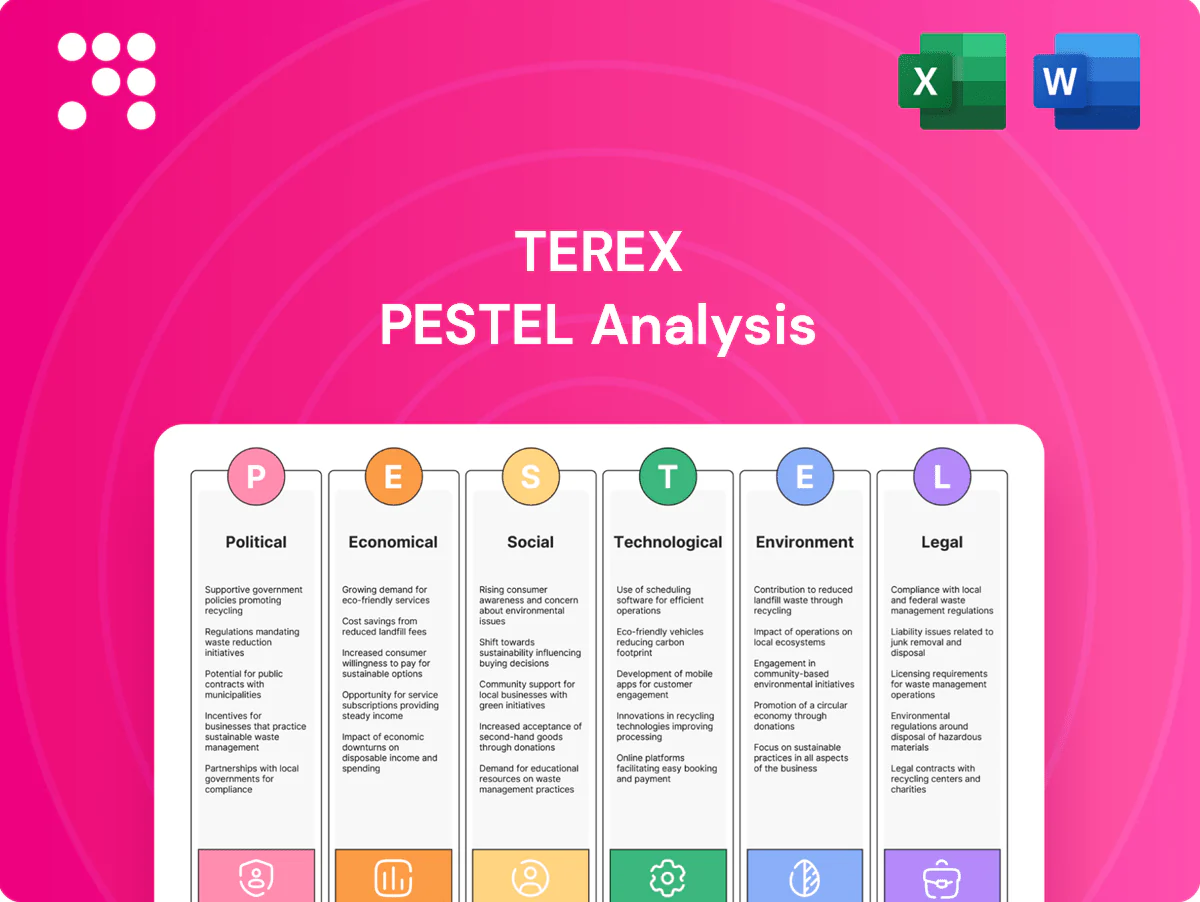

Terex PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological advances are shaping Terex’s strategic outlook in our concise PESTLE snapshot—vital for investors and planners. Dive deeper with the full, expertly researched PESTLE report to unlock actionable insights and make better decisions—download now.

Political factors

Geopolitics and trade policy

Shifting tariffs, export controls and sanctions—against a backdrop of US, EU and China tensions—raise component costs and market access for Terex aerial platforms and crushing/screening lines; Terex reported FY2024 revenue of about $4.6 billion, exposing significant exposure to supply shocks. Geopolitical friction has lengthened delivery times and increased costs, prompting dual-sourcing and localized production in key regions. Government trade incentives, including US CHIPS and industrial grants (~$280 billion federal support packages), can underwrite regionalization strategies.

Infrastructure spending priorities

U.S. and EU public infrastructure programs materially drive demand for work platforms and materials-processing machinery, with the U.S. Bipartisan Infrastructure Law providing roughly 550 billion dollars in new spending and NextGenerationEU allocating about 806.9 billion euros in recovery funds. Timing and size of appropriations in the U.S., EU and emerging markets directly affect backlog visibility and order cadence. Election cycles and fiscal constraints add volatility to project pipelines. Aligning product availability with funded sectors improves utilization and margins.

Industrial policy and localization

Policies promoting domestic manufacturing and supply-chain resilience materially shape Terex plant-footprint and sourcing choices; US IRA incentives ($369 billion) and India's PLI schemes (INR 1.97 lakh crore, ~ $24B as of 2024) tilt decisions toward local production. Local-content rules in key markets favor in-country assembly of Genie and MP equipment to secure public contracts. Incentives and tax credits shorten capex payback windows; non-compliance risks lost tenders and reputational damage.

Urban development and zoning priorities

Urban redevelopment drives recurring demand for compact, safety-focused aerial platforms as cities densify; UN projects about 56% of the global population will be urban by 2025. Political support for housing, utilities and grid modernization expands addressable projects, while moratoria or municipal budget cuts delay fleet refresh cycles. Public-private partnership frameworks influence procurement routes and favor vendors offering lifecycle financing and compliance support.

- City redevelopment → steady demand for compact aerials

- Housing, utilities, grid modernization → larger project pipeline

- Moratoria/budget cuts → delayed fleet refreshes

- PPP frameworks → procurement and financing advantages

Energy transition agendas

Government decarbonization targets (EU 55% GHG cut by 2030, net-zero by 2050; US IRA ~369 billion clean energy support) accelerate demand for electric/hybrid lifts and low-emission processing equipment, shifting procurement toward machines with lower operational emissions and total-cost-of-ownership advantages.

- Subsidies can cut upfront EV/equipment CAPEX by up to 20–30% in major programs

- Green procurement standards expand addressable market for low-emission units

- Policy clarity enables multi-year product and charging roadmaps

- Rapid policy reversals risk stranded inventory and R&D write-offs

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Geopolitical tensions, tariffs and export controls raise component costs and lengthen deliveries, hitting Terex FY2024 revenue ~$4.6B and prompting dual-sourcing and local production. Infrastructure and domestic industrial incentives (US $550B Bipartisan Law, EU €806.9B NextGenerationEU, US IRA $369B) drive demand but create timing risk; local-content rules favor regional assembly and affect bidding success.

| Risk | Impact | Key figures |

|---|---|---|

| Tariffs/sanctions | ↑ costs, delays | FY24 rev $4.6B |

| Infrastructure spend | ↑ demand, timing risk | US $550B, EU €806.9B |

What is included in the product

Explores how macro-environmental factors uniquely affect Terex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights and forward-looking implications to guide executives, investors and strategists.

A concise, visually segmented Terex PESTLE summary that can be dropped into presentations for quick alignment across teams, supports external risk discussions in planning sessions, and is easily annotated for region- or business-specific notes.

Economic factors

Construction cycle sensitivity

Terex order intake is highly tied to non-residential construction and quarrying cycles; group revenue was about $4.7bn in 2024, reflecting weakness in those end-markets. Slowdowns cut rental-fleet capex and pressured pricing and product mix, with management citing a roughly 15–20% pullback in rental investment in 2024. Backlogs near $1.1bn at year-end provided some cushion but can unwind quickly. Diversification across construction, mining and recycling smoothed revenue volatility.

Interest rates and financing

Higher interest rates (federal funds around 5.25–5.50% in 2024–2025) raise financing costs for rental firms and contractors, often delaying capital purchases and extending rental cycles. Tighter leasing and dealer floorplan terms squeeze channel inventory and slow sell-through. Easing rates can unlock deferred demand and accelerate aerial work platform replacements, while Terex Financial Solutions helps stabilize sales through credit facilitation and structured leases.

Commodity and input costs

Terex faces BOM volatility as steel (US HRC ~900 USD/ton in 2024), hydraulics, lithium‑ion battery packs (~132 USD/kWh in 2023 per BNEF) and semiconductors (global sales ~620B USD in 2024) swing input costs. Hedging and should‑cost engineering are critical to protect 2024 margins. Price realization must outpace lagging inflation without losing share; supplier negotiations and VA/VE programs bolster resilience.

FX and global exposure

Multi-currency sales and sourcing expose Terex earnings to FX swings; the U.S. dollar strengthened about 5% in 2024 (DXY), pressuring reported international revenues and dampening demand in FX-weak markets.

Natural hedges and financial instruments stabilize gross margins, while pricing discipline and localized sourcing reduce translation risk.

- FX exposure: multi-currency sales

- DXY +5% in 2024

- Mitigants: hedging, natural hedges, local sourcing

- Strategy: pricing discipline to protect margins

Rental market dynamics

Rental penetration (~40% in 2024) and average fleet age (typically 7–10 years) set AWP demand cadence, with older fleets prompting replacement spikes. Large rental players' capex cycles create order lumpiness, while utilization rates (60–70%) and time-on-rent drive replacement timing. Terex can capture share through lower total cost of ownership, higher uptime and telematics-enabled service analytics.

- rental-penetration: ~40% (2024)

- fleet-age: 7–10 years

- utilization: 60–70%

- Terex-edge: TCO, uptime, telematics

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Terex revenue ~$4.7bn in 2024 tied to nonresidential construction/quarrying; backlogs ~$1.1bn offer limited cushion. Fed funds ~5.25–5.50% (2024–25) and DXY +5% in 2024 raised financing and FX pressure, slowing rental capex (rental penetration ~40%). Input-cost volatility (US HRC ~900 USD/ton; semiconductors sales ~$620bn 2024) compresses margins; hedging, VA/VE and Terex Financial Solutions mitigate risk.

| Metric | Value (most recent) |

|---|---|

| Revenue | $4.7bn (2024) |

| Backlog | $1.1bn (YE 2024) |

| Rental penetration | ~40% (2024) |

| Fed funds | 5.25–5.50% (2024–25) |

| DXY | +5% (2024) |

Preview Before You Purchase

Terex PESTLE Analysis

The preview shown here is the exact Terex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. What you see is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same document.

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological advances are shaping Terex’s strategic outlook in our concise PESTLE snapshot—vital for investors and planners. Dive deeper with the full, expertly researched PESTLE report to unlock actionable insights and make better decisions—download now.

Political factors

Geopolitics and trade policy

Shifting tariffs, export controls and sanctions—against a backdrop of US, EU and China tensions—raise component costs and market access for Terex aerial platforms and crushing/screening lines; Terex reported FY2024 revenue of about $4.6 billion, exposing significant exposure to supply shocks. Geopolitical friction has lengthened delivery times and increased costs, prompting dual-sourcing and localized production in key regions. Government trade incentives, including US CHIPS and industrial grants (~$280 billion federal support packages), can underwrite regionalization strategies.

Infrastructure spending priorities

U.S. and EU public infrastructure programs materially drive demand for work platforms and materials-processing machinery, with the U.S. Bipartisan Infrastructure Law providing roughly 550 billion dollars in new spending and NextGenerationEU allocating about 806.9 billion euros in recovery funds. Timing and size of appropriations in the U.S., EU and emerging markets directly affect backlog visibility and order cadence. Election cycles and fiscal constraints add volatility to project pipelines. Aligning product availability with funded sectors improves utilization and margins.

Industrial policy and localization

Policies promoting domestic manufacturing and supply-chain resilience materially shape Terex plant-footprint and sourcing choices; US IRA incentives ($369 billion) and India's PLI schemes (INR 1.97 lakh crore, ~ $24B as of 2024) tilt decisions toward local production. Local-content rules in key markets favor in-country assembly of Genie and MP equipment to secure public contracts. Incentives and tax credits shorten capex payback windows; non-compliance risks lost tenders and reputational damage.

Urban development and zoning priorities

Urban redevelopment drives recurring demand for compact, safety-focused aerial platforms as cities densify; UN projects about 56% of the global population will be urban by 2025. Political support for housing, utilities and grid modernization expands addressable projects, while moratoria or municipal budget cuts delay fleet refresh cycles. Public-private partnership frameworks influence procurement routes and favor vendors offering lifecycle financing and compliance support.

- City redevelopment → steady demand for compact aerials

- Housing, utilities, grid modernization → larger project pipeline

- Moratoria/budget cuts → delayed fleet refreshes

- PPP frameworks → procurement and financing advantages

Energy transition agendas

Government decarbonization targets (EU 55% GHG cut by 2030, net-zero by 2050; US IRA ~369 billion clean energy support) accelerate demand for electric/hybrid lifts and low-emission processing equipment, shifting procurement toward machines with lower operational emissions and total-cost-of-ownership advantages.

- Subsidies can cut upfront EV/equipment CAPEX by up to 20–30% in major programs

- Green procurement standards expand addressable market for low-emission units

- Policy clarity enables multi-year product and charging roadmaps

- Rapid policy reversals risk stranded inventory and R&D write-offs

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Geopolitical tensions, tariffs and export controls raise component costs and lengthen deliveries, hitting Terex FY2024 revenue ~$4.6B and prompting dual-sourcing and local production. Infrastructure and domestic industrial incentives (US $550B Bipartisan Law, EU €806.9B NextGenerationEU, US IRA $369B) drive demand but create timing risk; local-content rules favor regional assembly and affect bidding success.

| Risk | Impact | Key figures |

|---|---|---|

| Tariffs/sanctions | ↑ costs, delays | FY24 rev $4.6B |

| Infrastructure spend | ↑ demand, timing risk | US $550B, EU €806.9B |

What is included in the product

Explores how macro-environmental factors uniquely affect Terex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights and forward-looking implications to guide executives, investors and strategists.

A concise, visually segmented Terex PESTLE summary that can be dropped into presentations for quick alignment across teams, supports external risk discussions in planning sessions, and is easily annotated for region- or business-specific notes.

Economic factors

Construction cycle sensitivity

Terex order intake is highly tied to non-residential construction and quarrying cycles; group revenue was about $4.7bn in 2024, reflecting weakness in those end-markets. Slowdowns cut rental-fleet capex and pressured pricing and product mix, with management citing a roughly 15–20% pullback in rental investment in 2024. Backlogs near $1.1bn at year-end provided some cushion but can unwind quickly. Diversification across construction, mining and recycling smoothed revenue volatility.

Interest rates and financing

Higher interest rates (federal funds around 5.25–5.50% in 2024–2025) raise financing costs for rental firms and contractors, often delaying capital purchases and extending rental cycles. Tighter leasing and dealer floorplan terms squeeze channel inventory and slow sell-through. Easing rates can unlock deferred demand and accelerate aerial work platform replacements, while Terex Financial Solutions helps stabilize sales through credit facilitation and structured leases.

Commodity and input costs

Terex faces BOM volatility as steel (US HRC ~900 USD/ton in 2024), hydraulics, lithium‑ion battery packs (~132 USD/kWh in 2023 per BNEF) and semiconductors (global sales ~620B USD in 2024) swing input costs. Hedging and should‑cost engineering are critical to protect 2024 margins. Price realization must outpace lagging inflation without losing share; supplier negotiations and VA/VE programs bolster resilience.

FX and global exposure

Multi-currency sales and sourcing expose Terex earnings to FX swings; the U.S. dollar strengthened about 5% in 2024 (DXY), pressuring reported international revenues and dampening demand in FX-weak markets.

Natural hedges and financial instruments stabilize gross margins, while pricing discipline and localized sourcing reduce translation risk.

- FX exposure: multi-currency sales

- DXY +5% in 2024

- Mitigants: hedging, natural hedges, local sourcing

- Strategy: pricing discipline to protect margins

Rental market dynamics

Rental penetration (~40% in 2024) and average fleet age (typically 7–10 years) set AWP demand cadence, with older fleets prompting replacement spikes. Large rental players' capex cycles create order lumpiness, while utilization rates (60–70%) and time-on-rent drive replacement timing. Terex can capture share through lower total cost of ownership, higher uptime and telematics-enabled service analytics.

- rental-penetration: ~40% (2024)

- fleet-age: 7–10 years

- utilization: 60–70%

- Terex-edge: TCO, uptime, telematics

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Terex revenue ~$4.7bn in 2024 tied to nonresidential construction/quarrying; backlogs ~$1.1bn offer limited cushion. Fed funds ~5.25–5.50% (2024–25) and DXY +5% in 2024 raised financing and FX pressure, slowing rental capex (rental penetration ~40%). Input-cost volatility (US HRC ~900 USD/ton; semiconductors sales ~$620bn 2024) compresses margins; hedging, VA/VE and Terex Financial Solutions mitigate risk.

| Metric | Value (most recent) |

|---|---|

| Revenue | $4.7bn (2024) |

| Backlog | $1.1bn (YE 2024) |

| Rental penetration | ~40% (2024) |

| Fed funds | 5.25–5.50% (2024–25) |

| DXY | +5% (2024) |

Preview Before You Purchase

Terex PESTLE Analysis

The preview shown here is the exact Terex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. What you see is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same document.

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological advances are shaping Terex’s strategic outlook in our concise PESTLE snapshot—vital for investors and planners. Dive deeper with the full, expertly researched PESTLE report to unlock actionable insights and make better decisions—download now.

Political factors

Geopolitics and trade policy

Shifting tariffs, export controls and sanctions—against a backdrop of US, EU and China tensions—raise component costs and market access for Terex aerial platforms and crushing/screening lines; Terex reported FY2024 revenue of about $4.6 billion, exposing significant exposure to supply shocks. Geopolitical friction has lengthened delivery times and increased costs, prompting dual-sourcing and localized production in key regions. Government trade incentives, including US CHIPS and industrial grants (~$280 billion federal support packages), can underwrite regionalization strategies.

Infrastructure spending priorities

U.S. and EU public infrastructure programs materially drive demand for work platforms and materials-processing machinery, with the U.S. Bipartisan Infrastructure Law providing roughly 550 billion dollars in new spending and NextGenerationEU allocating about 806.9 billion euros in recovery funds. Timing and size of appropriations in the U.S., EU and emerging markets directly affect backlog visibility and order cadence. Election cycles and fiscal constraints add volatility to project pipelines. Aligning product availability with funded sectors improves utilization and margins.

Industrial policy and localization

Policies promoting domestic manufacturing and supply-chain resilience materially shape Terex plant-footprint and sourcing choices; US IRA incentives ($369 billion) and India's PLI schemes (INR 1.97 lakh crore, ~ $24B as of 2024) tilt decisions toward local production. Local-content rules in key markets favor in-country assembly of Genie and MP equipment to secure public contracts. Incentives and tax credits shorten capex payback windows; non-compliance risks lost tenders and reputational damage.

Urban development and zoning priorities

Urban redevelopment drives recurring demand for compact, safety-focused aerial platforms as cities densify; UN projects about 56% of the global population will be urban by 2025. Political support for housing, utilities and grid modernization expands addressable projects, while moratoria or municipal budget cuts delay fleet refresh cycles. Public-private partnership frameworks influence procurement routes and favor vendors offering lifecycle financing and compliance support.

- City redevelopment → steady demand for compact aerials

- Housing, utilities, grid modernization → larger project pipeline

- Moratoria/budget cuts → delayed fleet refreshes

- PPP frameworks → procurement and financing advantages

Energy transition agendas

Government decarbonization targets (EU 55% GHG cut by 2030, net-zero by 2050; US IRA ~369 billion clean energy support) accelerate demand for electric/hybrid lifts and low-emission processing equipment, shifting procurement toward machines with lower operational emissions and total-cost-of-ownership advantages.

- Subsidies can cut upfront EV/equipment CAPEX by up to 20–30% in major programs

- Green procurement standards expand addressable market for low-emission units

- Policy clarity enables multi-year product and charging roadmaps

- Rapid policy reversals risk stranded inventory and R&D write-offs

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Geopolitical tensions, tariffs and export controls raise component costs and lengthen deliveries, hitting Terex FY2024 revenue ~$4.6B and prompting dual-sourcing and local production. Infrastructure and domestic industrial incentives (US $550B Bipartisan Law, EU €806.9B NextGenerationEU, US IRA $369B) drive demand but create timing risk; local-content rules favor regional assembly and affect bidding success.

| Risk | Impact | Key figures |

|---|---|---|

| Tariffs/sanctions | ↑ costs, delays | FY24 rev $4.6B |

| Infrastructure spend | ↑ demand, timing risk | US $550B, EU €806.9B |

What is included in the product

Explores how macro-environmental factors uniquely affect Terex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights and forward-looking implications to guide executives, investors and strategists.

A concise, visually segmented Terex PESTLE summary that can be dropped into presentations for quick alignment across teams, supports external risk discussions in planning sessions, and is easily annotated for region- or business-specific notes.

Economic factors

Construction cycle sensitivity

Terex order intake is highly tied to non-residential construction and quarrying cycles; group revenue was about $4.7bn in 2024, reflecting weakness in those end-markets. Slowdowns cut rental-fleet capex and pressured pricing and product mix, with management citing a roughly 15–20% pullback in rental investment in 2024. Backlogs near $1.1bn at year-end provided some cushion but can unwind quickly. Diversification across construction, mining and recycling smoothed revenue volatility.

Interest rates and financing

Higher interest rates (federal funds around 5.25–5.50% in 2024–2025) raise financing costs for rental firms and contractors, often delaying capital purchases and extending rental cycles. Tighter leasing and dealer floorplan terms squeeze channel inventory and slow sell-through. Easing rates can unlock deferred demand and accelerate aerial work platform replacements, while Terex Financial Solutions helps stabilize sales through credit facilitation and structured leases.

Commodity and input costs

Terex faces BOM volatility as steel (US HRC ~900 USD/ton in 2024), hydraulics, lithium‑ion battery packs (~132 USD/kWh in 2023 per BNEF) and semiconductors (global sales ~620B USD in 2024) swing input costs. Hedging and should‑cost engineering are critical to protect 2024 margins. Price realization must outpace lagging inflation without losing share; supplier negotiations and VA/VE programs bolster resilience.

FX and global exposure

Multi-currency sales and sourcing expose Terex earnings to FX swings; the U.S. dollar strengthened about 5% in 2024 (DXY), pressuring reported international revenues and dampening demand in FX-weak markets.

Natural hedges and financial instruments stabilize gross margins, while pricing discipline and localized sourcing reduce translation risk.

- FX exposure: multi-currency sales

- DXY +5% in 2024

- Mitigants: hedging, natural hedges, local sourcing

- Strategy: pricing discipline to protect margins

Rental market dynamics

Rental penetration (~40% in 2024) and average fleet age (typically 7–10 years) set AWP demand cadence, with older fleets prompting replacement spikes. Large rental players' capex cycles create order lumpiness, while utilization rates (60–70%) and time-on-rent drive replacement timing. Terex can capture share through lower total cost of ownership, higher uptime and telematics-enabled service analytics.

- rental-penetration: ~40% (2024)

- fleet-age: 7–10 years

- utilization: 60–70%

- Terex-edge: TCO, uptime, telematics

Geopolitics, tariffs and local-content rules raise costs, delay deliveries, spur regional sourcing

Terex revenue ~$4.7bn in 2024 tied to nonresidential construction/quarrying; backlogs ~$1.1bn offer limited cushion. Fed funds ~5.25–5.50% (2024–25) and DXY +5% in 2024 raised financing and FX pressure, slowing rental capex (rental penetration ~40%). Input-cost volatility (US HRC ~900 USD/ton; semiconductors sales ~$620bn 2024) compresses margins; hedging, VA/VE and Terex Financial Solutions mitigate risk.

| Metric | Value (most recent) |

|---|---|

| Revenue | $4.7bn (2024) |

| Backlog | $1.1bn (YE 2024) |

| Rental penetration | ~40% (2024) |

| Fed funds | 5.25–5.50% (2024–25) |

| DXY | +5% (2024) |

Preview Before You Purchase

Terex PESTLE Analysis

The preview shown here is the exact Terex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. What you see is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same document.