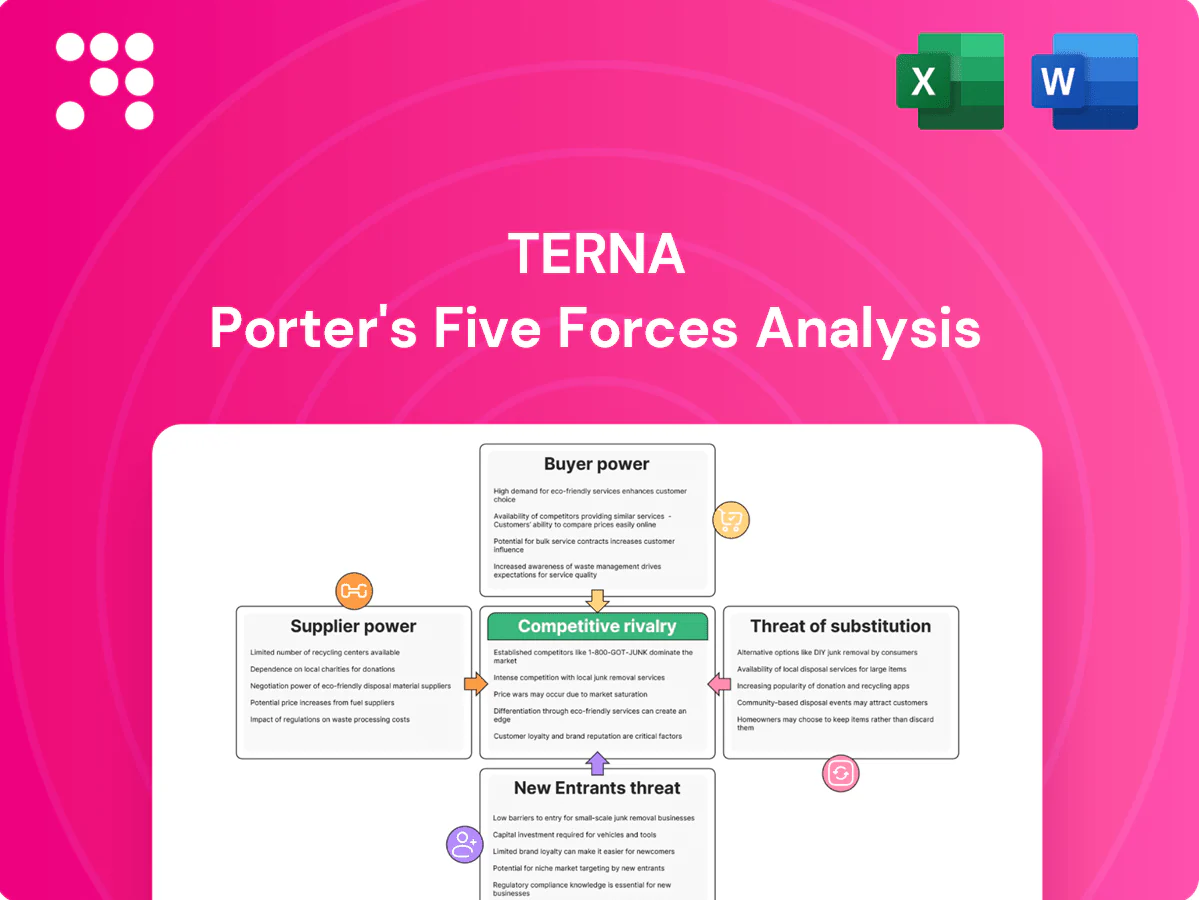

Terna Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Terna’s Porter's Five Forces snapshot highlights key pressures — regulated tariffs, concentrated suppliers, high infrastructure barriers, moderate buyer leverage, and evolving substitute risks from distributed generation. This concise view frames strategic challenges and value drivers for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Terna’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated equipment vendors

High-voltage cables and transformers are supplied mostly by a handful of specialists—Prysmian and Nexans for HV cables, ABB, Siemens Energy and GE for HVDC/converters—which raises switching costs and typical lead times of 12–36 months for HV equipment. Limited qualified vendors can extract favorable terms during tight markets; procurement leverage falls when capacity is constrained. Terna mitigates risk with multi-year framework contracts and competitive tenders, while scale and disciplined planning partially offset supplier bargaining power.

Long-lead manufacturing cycles

Core components for high-voltage transmission often have 12–24 month manufacturing and testing cycles, exposing Terna projects to delay risk; suppliers gain bargaining leverage when order backlogs spike and capacity is constrained. Early procurement and standardized specifications materially reduce exposure, while 2024 regulatory frameworks permit timing recognition of capex, helping absorb schedule slippage.

Specialized EPC and skilled labor

Complex high-voltage grid builds in Italy demand experienced EPC firms and scarce specialist crews, giving suppliers elevated bargaining power due to technical risk and limited contestability. Local permitting delays and challenging terrain further constrain bidders and support higher margins. Terna fragments contracts and enforces strict performance KPIs to contain supplier leverage. Active workforce development and training programs aim to widen the labor pool and reduce dependence on a few specialists.

Technology and interoperability lock-in

System protection, SCADA and digital substations must interoperate with legacy assets, and Terna—which operates roughly 98% of Italy’s high-voltage grid—faces this integration challenge across its network.

EU NIS2-driven interface and cybersecurity requirements raise switching costs; Terna promotes open standards and modular designs to curb lock-in, but software updates and license models can still embed vendor power.

- Interoperability burden: legacy integrations

- Regulation: NIS2 raises compliance costs

- Mitigation: open standards, modular design

- Residual risk: update/license-driven vendor lock-in

Land access and environmental services

Right-of-way acquisition, permitting and environmental studies for Terna often rely on niche consultancies whose 2024 Italian market rates typically range €150–€300/hour, giving them situational leverage through local knowledge and stakeholder networks.

Early engagement and framework agreements have reduced average permitting delays by an estimated 20% in 2024, but political and community acceptance remain gating factors that can still halt projects.

- Consultancy rates: €150–€300/hour (2024)

- Permitting delays reduced ~20% with early frameworks (2024)

- Local stakeholder control = situational supplier power

- Political/community acceptance = project gate

Concentrated HV suppliers, 12–36 month lead times; grid operator uses multi-year tenders

Concentrated suppliers (Prysmian, Nexans, ABB, Siemens Energy, GE) and 12–36 month lead times raise switching costs and bargaining power. Terna mitigates via multi-year frameworks, competitive tenders and scale; it operates ~98% of Italy’s HV grid. Consultancy rates €150–€300/hr and NIS2 compliance add situational leverage; permitting delays cut ~20% in 2024 with early engagement.

| Metric | Value | Impact |

|---|---|---|

| HV equipment lead time | 12–36 months | High supplier leverage |

| Manufacturing cycle | 12–24 months | Delay risk |

| Grid share | ~98% | Integration lock-in |

| Consultancy rates (2024) | €150–€300/hr | Situational power |

| Permitting improvement (2024) | −20% | Reduced delay |

What is included in the product

Tailored Porter's Five Forces analysis for Terna that uncovers key drivers of competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights regulatory and technological disruptors shaping its profitability.

Clear one-sheet Terna Porter’s Five Forces summary for quick decisions, with customizable pressure levels and an instant spider/radar visualization. Clean, no-macro layout ready for pitch decks, easy data swap, and seamless integration into Excel dashboards or Word reports.

Customers Bargaining Power

Regulatory authority as meta-buyer

ARERA's 2024 regulatory framework sets allowed returns, tariffs and service-quality targets, effectively determining Terna's regulated revenue and treating the regulator as a meta-buyer.

This confers very high buyer-like power despite inelastic end-demand, with incentive schemes in 2024 designed to reward or penalize operational performance and service continuity.

Terna’s strategic emphasis on reliability and cost efficiency directly aligns with ARERA incentives, linking its financial outcomes to measured quality and efficiency metrics.

Inelastic end-user demand

End-user demand for electricity is highly inelastic, with short-run price elasticities typically around -0.2 to -0.4, limiting consumers' direct bargaining power over Terna's transmission prices. Visible transmission tariffs make costs politically sensitive and amplify scrutiny during regulatory tariff reviews. Organized customer advocacy has demonstrably shaped regulatory resets in Europe, prompting tariff adjustments and service conditions. Continuity and reliability, not price, remain the primary customer value drivers.

Grid users: generators and DSOs

Producers and DSOs depend on timely access and connection: Terna operates approximately 74,000 km of high-voltage lines (2024), so generators cannot realistically switch TSO and instead lobby for clearer connection terms and transparency. Queue management and standardized processes implemented by Terna have reduced procedural friction, while published KPIs on connection lead times and grid availability directly shape stakeholder satisfaction. Performance metrics—connection lead-time targets and outage indices—drive negotiations and influence investment timing.

Large industrial off-takers

- Exposure: high interruption costs (often >€100k/hr)

- Leverage: demand response & on-site generation

- Constraint: single-TSO framework

- Engagement: Terna 2024 stakeholder councils, dozens of large users

Cross-border market participants

Cross-border interconnector users prize transparent capacity allocation and congestion management, as these directly affect dispatch and trading; Terna, which operates roughly 74,000 km of grid, must align with EU rules like CACM (Regulation 2015/1222) and ACER oversight that give customers indirect leverage. Harmonization with neighboring TSOs and efficient market coupling (day-ahead coupling across most EU borders) raises perceived service quality and reduces access disputes.

- Capacity allocation focus

- ACER + CACM leverage

- TSO harmonization impacts quality

- Market coupling lowers disputes

ARERA 2024 rules give regulators meta-buyer power over national grid operator

ARERA's 2024 framework gives regulators meta-buyer power over Terna, strongly shaping allowed revenues and service incentives. High buyer-like power persists despite inelastic end-demand (price elasticity ~ -0.2 to -0.4) and limited switching. Generators, DSOs and large off-takers rely on Terna's ~74,000 km grid but exert influence via connection rules, KPIs and demand-response options; interruption costs often exceed €100,000/hr.

| Metric | 2024 value |

|---|---|

| Grid length | ~74,000 km |

| Price elasticity (short run) | -0.2 to -0.4 |

| Interruption cost (industrial) | >€100,000/hr |

| Stakeholder engagement | Terna 2024 councils (dozens) |

Preview the Actual Deliverable

Terna Porter's Five Forces Analysis

This preview shows the exact Terna Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Terna’s Porter's Five Forces snapshot highlights key pressures — regulated tariffs, concentrated suppliers, high infrastructure barriers, moderate buyer leverage, and evolving substitute risks from distributed generation. This concise view frames strategic challenges and value drivers for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Terna’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated equipment vendors

High-voltage cables and transformers are supplied mostly by a handful of specialists—Prysmian and Nexans for HV cables, ABB, Siemens Energy and GE for HVDC/converters—which raises switching costs and typical lead times of 12–36 months for HV equipment. Limited qualified vendors can extract favorable terms during tight markets; procurement leverage falls when capacity is constrained. Terna mitigates risk with multi-year framework contracts and competitive tenders, while scale and disciplined planning partially offset supplier bargaining power.

Long-lead manufacturing cycles

Core components for high-voltage transmission often have 12–24 month manufacturing and testing cycles, exposing Terna projects to delay risk; suppliers gain bargaining leverage when order backlogs spike and capacity is constrained. Early procurement and standardized specifications materially reduce exposure, while 2024 regulatory frameworks permit timing recognition of capex, helping absorb schedule slippage.

Specialized EPC and skilled labor

Complex high-voltage grid builds in Italy demand experienced EPC firms and scarce specialist crews, giving suppliers elevated bargaining power due to technical risk and limited contestability. Local permitting delays and challenging terrain further constrain bidders and support higher margins. Terna fragments contracts and enforces strict performance KPIs to contain supplier leverage. Active workforce development and training programs aim to widen the labor pool and reduce dependence on a few specialists.

Technology and interoperability lock-in

System protection, SCADA and digital substations must interoperate with legacy assets, and Terna—which operates roughly 98% of Italy’s high-voltage grid—faces this integration challenge across its network.

EU NIS2-driven interface and cybersecurity requirements raise switching costs; Terna promotes open standards and modular designs to curb lock-in, but software updates and license models can still embed vendor power.

- Interoperability burden: legacy integrations

- Regulation: NIS2 raises compliance costs

- Mitigation: open standards, modular design

- Residual risk: update/license-driven vendor lock-in

Land access and environmental services

Right-of-way acquisition, permitting and environmental studies for Terna often rely on niche consultancies whose 2024 Italian market rates typically range €150–€300/hour, giving them situational leverage through local knowledge and stakeholder networks.

Early engagement and framework agreements have reduced average permitting delays by an estimated 20% in 2024, but political and community acceptance remain gating factors that can still halt projects.

- Consultancy rates: €150–€300/hour (2024)

- Permitting delays reduced ~20% with early frameworks (2024)

- Local stakeholder control = situational supplier power

- Political/community acceptance = project gate

Concentrated HV suppliers, 12–36 month lead times; grid operator uses multi-year tenders

Concentrated suppliers (Prysmian, Nexans, ABB, Siemens Energy, GE) and 12–36 month lead times raise switching costs and bargaining power. Terna mitigates via multi-year frameworks, competitive tenders and scale; it operates ~98% of Italy’s HV grid. Consultancy rates €150–€300/hr and NIS2 compliance add situational leverage; permitting delays cut ~20% in 2024 with early engagement.

| Metric | Value | Impact |

|---|---|---|

| HV equipment lead time | 12–36 months | High supplier leverage |

| Manufacturing cycle | 12–24 months | Delay risk |

| Grid share | ~98% | Integration lock-in |

| Consultancy rates (2024) | €150–€300/hr | Situational power |

| Permitting improvement (2024) | −20% | Reduced delay |

What is included in the product

Tailored Porter's Five Forces analysis for Terna that uncovers key drivers of competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights regulatory and technological disruptors shaping its profitability.

Clear one-sheet Terna Porter’s Five Forces summary for quick decisions, with customizable pressure levels and an instant spider/radar visualization. Clean, no-macro layout ready for pitch decks, easy data swap, and seamless integration into Excel dashboards or Word reports.

Customers Bargaining Power

Regulatory authority as meta-buyer

ARERA's 2024 regulatory framework sets allowed returns, tariffs and service-quality targets, effectively determining Terna's regulated revenue and treating the regulator as a meta-buyer.

This confers very high buyer-like power despite inelastic end-demand, with incentive schemes in 2024 designed to reward or penalize operational performance and service continuity.

Terna’s strategic emphasis on reliability and cost efficiency directly aligns with ARERA incentives, linking its financial outcomes to measured quality and efficiency metrics.

Inelastic end-user demand

End-user demand for electricity is highly inelastic, with short-run price elasticities typically around -0.2 to -0.4, limiting consumers' direct bargaining power over Terna's transmission prices. Visible transmission tariffs make costs politically sensitive and amplify scrutiny during regulatory tariff reviews. Organized customer advocacy has demonstrably shaped regulatory resets in Europe, prompting tariff adjustments and service conditions. Continuity and reliability, not price, remain the primary customer value drivers.

Grid users: generators and DSOs

Producers and DSOs depend on timely access and connection: Terna operates approximately 74,000 km of high-voltage lines (2024), so generators cannot realistically switch TSO and instead lobby for clearer connection terms and transparency. Queue management and standardized processes implemented by Terna have reduced procedural friction, while published KPIs on connection lead times and grid availability directly shape stakeholder satisfaction. Performance metrics—connection lead-time targets and outage indices—drive negotiations and influence investment timing.

Large industrial off-takers

- Exposure: high interruption costs (often >€100k/hr)

- Leverage: demand response & on-site generation

- Constraint: single-TSO framework

- Engagement: Terna 2024 stakeholder councils, dozens of large users

Cross-border market participants

Cross-border interconnector users prize transparent capacity allocation and congestion management, as these directly affect dispatch and trading; Terna, which operates roughly 74,000 km of grid, must align with EU rules like CACM (Regulation 2015/1222) and ACER oversight that give customers indirect leverage. Harmonization with neighboring TSOs and efficient market coupling (day-ahead coupling across most EU borders) raises perceived service quality and reduces access disputes.

- Capacity allocation focus

- ACER + CACM leverage

- TSO harmonization impacts quality

- Market coupling lowers disputes

ARERA 2024 rules give regulators meta-buyer power over national grid operator

ARERA's 2024 framework gives regulators meta-buyer power over Terna, strongly shaping allowed revenues and service incentives. High buyer-like power persists despite inelastic end-demand (price elasticity ~ -0.2 to -0.4) and limited switching. Generators, DSOs and large off-takers rely on Terna's ~74,000 km grid but exert influence via connection rules, KPIs and demand-response options; interruption costs often exceed €100,000/hr.

| Metric | 2024 value |

|---|---|

| Grid length | ~74,000 km |

| Price elasticity (short run) | -0.2 to -0.4 |

| Interruption cost (industrial) | >€100,000/hr |

| Stakeholder engagement | Terna 2024 councils (dozens) |

Preview the Actual Deliverable

Terna Porter's Five Forces Analysis

This preview shows the exact Terna Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Terna’s Porter's Five Forces snapshot highlights key pressures — regulated tariffs, concentrated suppliers, high infrastructure barriers, moderate buyer leverage, and evolving substitute risks from distributed generation. This concise view frames strategic challenges and value drivers for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Terna’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated equipment vendors

High-voltage cables and transformers are supplied mostly by a handful of specialists—Prysmian and Nexans for HV cables, ABB, Siemens Energy and GE for HVDC/converters—which raises switching costs and typical lead times of 12–36 months for HV equipment. Limited qualified vendors can extract favorable terms during tight markets; procurement leverage falls when capacity is constrained. Terna mitigates risk with multi-year framework contracts and competitive tenders, while scale and disciplined planning partially offset supplier bargaining power.

Long-lead manufacturing cycles

Core components for high-voltage transmission often have 12–24 month manufacturing and testing cycles, exposing Terna projects to delay risk; suppliers gain bargaining leverage when order backlogs spike and capacity is constrained. Early procurement and standardized specifications materially reduce exposure, while 2024 regulatory frameworks permit timing recognition of capex, helping absorb schedule slippage.

Specialized EPC and skilled labor

Complex high-voltage grid builds in Italy demand experienced EPC firms and scarce specialist crews, giving suppliers elevated bargaining power due to technical risk and limited contestability. Local permitting delays and challenging terrain further constrain bidders and support higher margins. Terna fragments contracts and enforces strict performance KPIs to contain supplier leverage. Active workforce development and training programs aim to widen the labor pool and reduce dependence on a few specialists.

Technology and interoperability lock-in

System protection, SCADA and digital substations must interoperate with legacy assets, and Terna—which operates roughly 98% of Italy’s high-voltage grid—faces this integration challenge across its network.

EU NIS2-driven interface and cybersecurity requirements raise switching costs; Terna promotes open standards and modular designs to curb lock-in, but software updates and license models can still embed vendor power.

- Interoperability burden: legacy integrations

- Regulation: NIS2 raises compliance costs

- Mitigation: open standards, modular design

- Residual risk: update/license-driven vendor lock-in

Land access and environmental services

Right-of-way acquisition, permitting and environmental studies for Terna often rely on niche consultancies whose 2024 Italian market rates typically range €150–€300/hour, giving them situational leverage through local knowledge and stakeholder networks.

Early engagement and framework agreements have reduced average permitting delays by an estimated 20% in 2024, but political and community acceptance remain gating factors that can still halt projects.

- Consultancy rates: €150–€300/hour (2024)

- Permitting delays reduced ~20% with early frameworks (2024)

- Local stakeholder control = situational supplier power

- Political/community acceptance = project gate

Concentrated HV suppliers, 12–36 month lead times; grid operator uses multi-year tenders

Concentrated suppliers (Prysmian, Nexans, ABB, Siemens Energy, GE) and 12–36 month lead times raise switching costs and bargaining power. Terna mitigates via multi-year frameworks, competitive tenders and scale; it operates ~98% of Italy’s HV grid. Consultancy rates €150–€300/hr and NIS2 compliance add situational leverage; permitting delays cut ~20% in 2024 with early engagement.

| Metric | Value | Impact |

|---|---|---|

| HV equipment lead time | 12–36 months | High supplier leverage |

| Manufacturing cycle | 12–24 months | Delay risk |

| Grid share | ~98% | Integration lock-in |

| Consultancy rates (2024) | €150–€300/hr | Situational power |

| Permitting improvement (2024) | −20% | Reduced delay |

What is included in the product

Tailored Porter's Five Forces analysis for Terna that uncovers key drivers of competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights regulatory and technological disruptors shaping its profitability.

Clear one-sheet Terna Porter’s Five Forces summary for quick decisions, with customizable pressure levels and an instant spider/radar visualization. Clean, no-macro layout ready for pitch decks, easy data swap, and seamless integration into Excel dashboards or Word reports.

Customers Bargaining Power

Regulatory authority as meta-buyer

ARERA's 2024 regulatory framework sets allowed returns, tariffs and service-quality targets, effectively determining Terna's regulated revenue and treating the regulator as a meta-buyer.

This confers very high buyer-like power despite inelastic end-demand, with incentive schemes in 2024 designed to reward or penalize operational performance and service continuity.

Terna’s strategic emphasis on reliability and cost efficiency directly aligns with ARERA incentives, linking its financial outcomes to measured quality and efficiency metrics.

Inelastic end-user demand

End-user demand for electricity is highly inelastic, with short-run price elasticities typically around -0.2 to -0.4, limiting consumers' direct bargaining power over Terna's transmission prices. Visible transmission tariffs make costs politically sensitive and amplify scrutiny during regulatory tariff reviews. Organized customer advocacy has demonstrably shaped regulatory resets in Europe, prompting tariff adjustments and service conditions. Continuity and reliability, not price, remain the primary customer value drivers.

Grid users: generators and DSOs

Producers and DSOs depend on timely access and connection: Terna operates approximately 74,000 km of high-voltage lines (2024), so generators cannot realistically switch TSO and instead lobby for clearer connection terms and transparency. Queue management and standardized processes implemented by Terna have reduced procedural friction, while published KPIs on connection lead times and grid availability directly shape stakeholder satisfaction. Performance metrics—connection lead-time targets and outage indices—drive negotiations and influence investment timing.

Large industrial off-takers

- Exposure: high interruption costs (often >€100k/hr)

- Leverage: demand response & on-site generation

- Constraint: single-TSO framework

- Engagement: Terna 2024 stakeholder councils, dozens of large users

Cross-border market participants

Cross-border interconnector users prize transparent capacity allocation and congestion management, as these directly affect dispatch and trading; Terna, which operates roughly 74,000 km of grid, must align with EU rules like CACM (Regulation 2015/1222) and ACER oversight that give customers indirect leverage. Harmonization with neighboring TSOs and efficient market coupling (day-ahead coupling across most EU borders) raises perceived service quality and reduces access disputes.

- Capacity allocation focus

- ACER + CACM leverage

- TSO harmonization impacts quality

- Market coupling lowers disputes

ARERA 2024 rules give regulators meta-buyer power over national grid operator

ARERA's 2024 framework gives regulators meta-buyer power over Terna, strongly shaping allowed revenues and service incentives. High buyer-like power persists despite inelastic end-demand (price elasticity ~ -0.2 to -0.4) and limited switching. Generators, DSOs and large off-takers rely on Terna's ~74,000 km grid but exert influence via connection rules, KPIs and demand-response options; interruption costs often exceed €100,000/hr.

| Metric | 2024 value |

|---|---|

| Grid length | ~74,000 km |

| Price elasticity (short run) | -0.2 to -0.4 |

| Interruption cost (industrial) | >€100,000/hr |

| Stakeholder engagement | Terna 2024 councils (dozens) |

Preview the Actual Deliverable

Terna Porter's Five Forces Analysis

This preview shows the exact Terna Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.