TerraVest Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

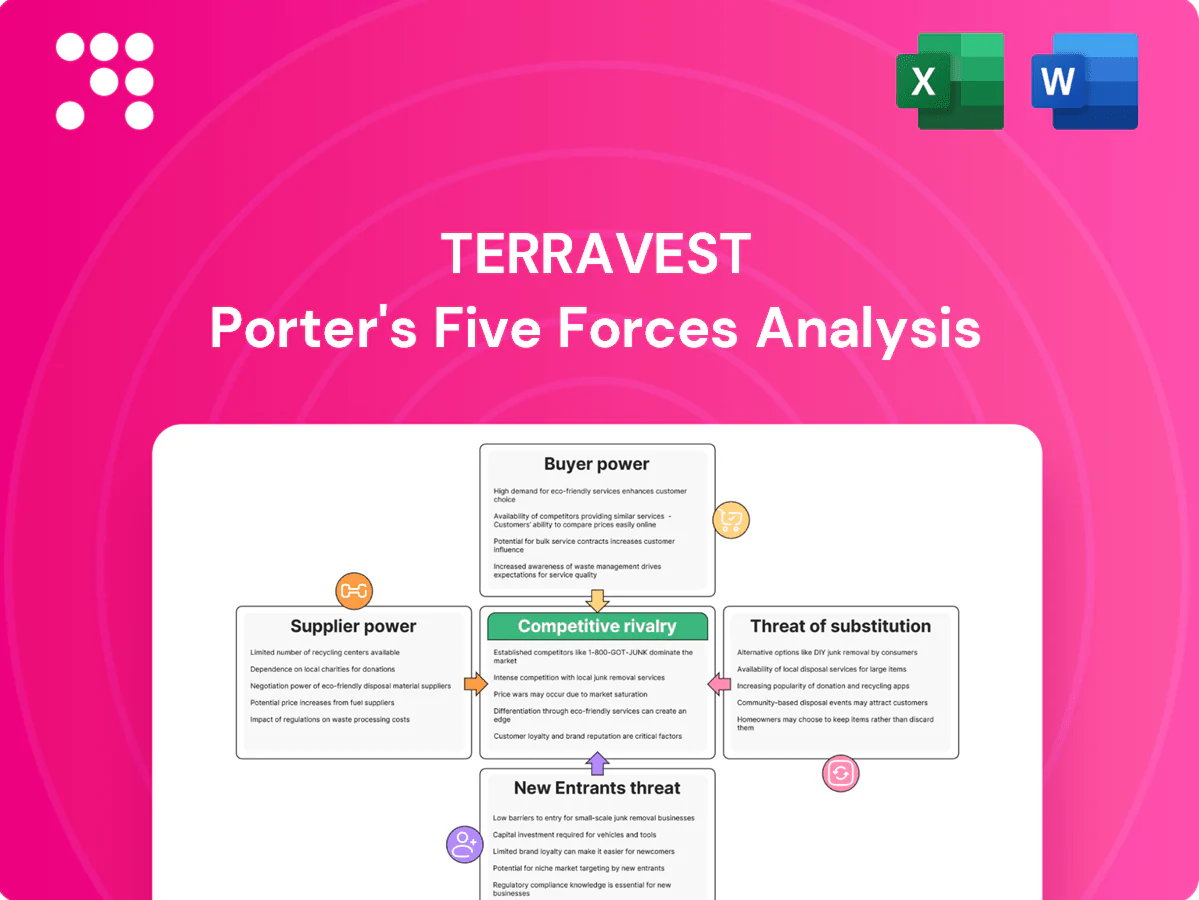

TerraVest’s Porter's Five Forces snapshot highlights moderate supplier power, fragmented buyer segments, strong rivalry among niche industrial competitors, low threat of substitutes, and meaningful scale-based entry barriers. These dynamics suggest steady margins but sensitivity to commodity costs and consolidation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Core inputs—steel plate, specialty alloys, valves and instrumentation—are concentrated among certified mills and OEMs, giving suppliers leverage; TerraVest’s scale improves pricing negotiation but certification and OEM approvals limit rapid switching. Metals price swings have pressured margins, and mill lead times can exceed 20 weeks in strong upcycles, tightening supply and allocation.

Supplier Power 2

Compliance with ASME, API and CRN narrows qualified supplier pools, concentrating leverage with high-spec vendors and slowing substitution; industry estimates in 2024 show qualified vendor lists shrink supplier universes by roughly 50-70% in pressure-equipment segments. Pre-approved vendor lists and weld procedure qualifications materially raise switching costs and procurement lead times. Audits and traceability requirements extend replacement timelines by months and increase costs, embedding power with certified component suppliers.

Supplier Power 3

Logistics, coatings and field-service subcontractors create multi-tier supplier exposure; freight alone can swing total delivered heavy-equipment cost by 10–15% and regional availability drives variance. Coordinating multi-site deliveries gives larger vendors negotiating leverage, while TerraVest’s diversified North American footprint across more than 20 operating locations in 2024 helps partially mitigate regional bottlenecks.

Supplier Power 4

Long-term contracts, volume bundling and hedging in 2024 cut input-price volatility materially, with procurement hedges and fixed contracts covering an estimated 60% of spend and reducing swing exposure roughly 20%; vendor-managed inventory and consignment for fasteners/valves smooth operations and free up working capital, but high customization for project-specific equipment limits standardization benefits and savings. Dual-sourcing remains constrained by qualification timelines, often taking 6–12 months to onboard a second supplier.

- Coverage: ~60% of spend under fixed/hedged contracts (2024)

- Volatility reduction: ~20% via hedging/bundling (2024)

- VMI/consignment: lowers inventory days and frees working capital

- Dual-sourcing lead time: 6–12 months

Supplier Power 5

Skilled labor—especially welders and NDE technicians—is a critical supplier for TerraVest; tight markets have elevated wage and overtime costs, and industry surveys through 2024 continue to report widespread hiring difficulty. Training pipelines and automation can mitigate shortages but require capital investment and lead times; during peak demand labor availability can become the primary gating constraint.

- Hiring difficulty: industry surveys 2023–24 report majority of firms constrained

- Wage pressure: sustained above‑average increases in fabrication sectors

- Mitigation: training + automation need upfront CAPEX and months to scale

High supplier power; hedges cover ~60%, volatility ~20%

Supplier power is high: certified mills/OEMs and labor scarcity constrain switching; TerraVest covers ~60% of spend with fixed/hedges reducing input volatility ~20% in 2024. Steel lead times often exceed 20 weeks; qualified-vendor pools shrink ~50–70%, and freight can add 10–15% to delivered cost.

| Metric | 2024 |

|---|---|

| Spend under fixed/hedges | ~60% |

| Volatility reduction | ~20% |

| Steel lead time | >20 weeks |

| Qualified vendor shrink | 50–70% |

| Freight impact | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for TerraVest that uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive threats, substitutes, and incumbent protections with strategic commentary suitable for investor reports and internal strategy decks.

A concise one-sheet Porter's Five Forces for TerraVest that distills competitive pressure into an actionable radar chart—ideal for rapid boardroom decisions. No macros, easy to customize with your data and ready to drop into pitch decks.

Customers Bargaining Power

Buyer Power 1

Customers range from oil and gas and chemical to transportation and agriculture, many backed by centralized procurement teams that run competitive RFPs; large EPCs and midstream operators often bid projects exceeding $10 million, heightening price sensitivity. Project scale lets buyers extract price and term concessions, while extended payment schedules and strict warranty demands shift cash-flow and performance risk onto suppliers.

Buyer Power 2

Custom-engineered tanks and pressure vessels for TerraVest are highly specialized, reducing direct comparability across vendors and limiting price-driven switching. Engineering complexity and site-specific requirements create material switching frictions mid-project, often requiring re‑engineering and re-certification under ASME codes. Performance guarantees and certification needs further reinforce vendor lock-in, which moderates buyer power after contract award.

Buyer Power 3

Cyclical end-markets amplify buyer leverage during downturns as capacity chases fewer projects, pressuring pricing and margins. In upcycles, tight lead times and constrained supply can shift power back to manufacturers, improving negotiation leverage. TerraVest’s diversification across industrial, energy, transportation and specialty sectors helps balance cycles, while improved backlog visibility strengthens pricing discipline.

Buyer Power 4

Lifecycle services, maintenance and retrofit work increase customer stickiness for TerraVest, shifting buying criteria from upfront price to aftermarket support and parts availability; multi-year service agreements and embedded relationships reduce pure price competition and soften buyer power where uptime is critical.

- Aftermarket-led purchasing: parts/support > upfront cost

- Multi-year service agreements embed customers

- Uptime-sensitive buyers less price-driven

Buyer Power 5

TerraVest's North American multi-plant footprint in 2024 enables meeting tight schedules and complex logistics, shifting buyer focus from lowest price to on-time delivery and compliance history. Prequalification and past-performance requirements routinely narrow bidder lists, increasing procurement leverage for suppliers with strong execution records. When execution risk dominates, this improves realized pricing and contract stability.

ASME-certified tanks and service-led uptime beat RFP price pressure across industrial buyers

Buyers span oil & gas, chemical, transport and ag with centralized procurement running competitive RFPs, driving price and term pressure on large projects.

Highly engineered tanks and ASME certifications limit vendor substitutability, increasing post-award lock-in and moderating buyer power.

Lifecycle services and TerraVest’s North American multi-plant footprint (2024) shift focus to uptime, delivery and service over pure price.

| Factor | 2024 Signal |

|---|---|

| Procurement | RFPs, large EPCs |

| Switching | ASME re-certification friction |

| Aftermarket | Service-led stickiness |

Preview the Actual Deliverable

TerraVest Porter's Five Forces Analysis

This TerraVest Porter’s Five Forces Analysis preview is the exact document you’ll receive after purchase—fully written, formatted, and ready to download. No placeholders, no mockups, and no edits required. Complete and professional, it’s the same file available instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

TerraVest’s Porter's Five Forces snapshot highlights moderate supplier power, fragmented buyer segments, strong rivalry among niche industrial competitors, low threat of substitutes, and meaningful scale-based entry barriers. These dynamics suggest steady margins but sensitivity to commodity costs and consolidation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Core inputs—steel plate, specialty alloys, valves and instrumentation—are concentrated among certified mills and OEMs, giving suppliers leverage; TerraVest’s scale improves pricing negotiation but certification and OEM approvals limit rapid switching. Metals price swings have pressured margins, and mill lead times can exceed 20 weeks in strong upcycles, tightening supply and allocation.

Supplier Power 2

Compliance with ASME, API and CRN narrows qualified supplier pools, concentrating leverage with high-spec vendors and slowing substitution; industry estimates in 2024 show qualified vendor lists shrink supplier universes by roughly 50-70% in pressure-equipment segments. Pre-approved vendor lists and weld procedure qualifications materially raise switching costs and procurement lead times. Audits and traceability requirements extend replacement timelines by months and increase costs, embedding power with certified component suppliers.

Supplier Power 3

Logistics, coatings and field-service subcontractors create multi-tier supplier exposure; freight alone can swing total delivered heavy-equipment cost by 10–15% and regional availability drives variance. Coordinating multi-site deliveries gives larger vendors negotiating leverage, while TerraVest’s diversified North American footprint across more than 20 operating locations in 2024 helps partially mitigate regional bottlenecks.

Supplier Power 4

Long-term contracts, volume bundling and hedging in 2024 cut input-price volatility materially, with procurement hedges and fixed contracts covering an estimated 60% of spend and reducing swing exposure roughly 20%; vendor-managed inventory and consignment for fasteners/valves smooth operations and free up working capital, but high customization for project-specific equipment limits standardization benefits and savings. Dual-sourcing remains constrained by qualification timelines, often taking 6–12 months to onboard a second supplier.

- Coverage: ~60% of spend under fixed/hedged contracts (2024)

- Volatility reduction: ~20% via hedging/bundling (2024)

- VMI/consignment: lowers inventory days and frees working capital

- Dual-sourcing lead time: 6–12 months

Supplier Power 5

Skilled labor—especially welders and NDE technicians—is a critical supplier for TerraVest; tight markets have elevated wage and overtime costs, and industry surveys through 2024 continue to report widespread hiring difficulty. Training pipelines and automation can mitigate shortages but require capital investment and lead times; during peak demand labor availability can become the primary gating constraint.

- Hiring difficulty: industry surveys 2023–24 report majority of firms constrained

- Wage pressure: sustained above‑average increases in fabrication sectors

- Mitigation: training + automation need upfront CAPEX and months to scale

High supplier power; hedges cover ~60%, volatility ~20%

Supplier power is high: certified mills/OEMs and labor scarcity constrain switching; TerraVest covers ~60% of spend with fixed/hedges reducing input volatility ~20% in 2024. Steel lead times often exceed 20 weeks; qualified-vendor pools shrink ~50–70%, and freight can add 10–15% to delivered cost.

| Metric | 2024 |

|---|---|

| Spend under fixed/hedges | ~60% |

| Volatility reduction | ~20% |

| Steel lead time | >20 weeks |

| Qualified vendor shrink | 50–70% |

| Freight impact | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for TerraVest that uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive threats, substitutes, and incumbent protections with strategic commentary suitable for investor reports and internal strategy decks.

A concise one-sheet Porter's Five Forces for TerraVest that distills competitive pressure into an actionable radar chart—ideal for rapid boardroom decisions. No macros, easy to customize with your data and ready to drop into pitch decks.

Customers Bargaining Power

Buyer Power 1

Customers range from oil and gas and chemical to transportation and agriculture, many backed by centralized procurement teams that run competitive RFPs; large EPCs and midstream operators often bid projects exceeding $10 million, heightening price sensitivity. Project scale lets buyers extract price and term concessions, while extended payment schedules and strict warranty demands shift cash-flow and performance risk onto suppliers.

Buyer Power 2

Custom-engineered tanks and pressure vessels for TerraVest are highly specialized, reducing direct comparability across vendors and limiting price-driven switching. Engineering complexity and site-specific requirements create material switching frictions mid-project, often requiring re‑engineering and re-certification under ASME codes. Performance guarantees and certification needs further reinforce vendor lock-in, which moderates buyer power after contract award.

Buyer Power 3

Cyclical end-markets amplify buyer leverage during downturns as capacity chases fewer projects, pressuring pricing and margins. In upcycles, tight lead times and constrained supply can shift power back to manufacturers, improving negotiation leverage. TerraVest’s diversification across industrial, energy, transportation and specialty sectors helps balance cycles, while improved backlog visibility strengthens pricing discipline.

Buyer Power 4

Lifecycle services, maintenance and retrofit work increase customer stickiness for TerraVest, shifting buying criteria from upfront price to aftermarket support and parts availability; multi-year service agreements and embedded relationships reduce pure price competition and soften buyer power where uptime is critical.

- Aftermarket-led purchasing: parts/support > upfront cost

- Multi-year service agreements embed customers

- Uptime-sensitive buyers less price-driven

Buyer Power 5

TerraVest's North American multi-plant footprint in 2024 enables meeting tight schedules and complex logistics, shifting buyer focus from lowest price to on-time delivery and compliance history. Prequalification and past-performance requirements routinely narrow bidder lists, increasing procurement leverage for suppliers with strong execution records. When execution risk dominates, this improves realized pricing and contract stability.

ASME-certified tanks and service-led uptime beat RFP price pressure across industrial buyers

Buyers span oil & gas, chemical, transport and ag with centralized procurement running competitive RFPs, driving price and term pressure on large projects.

Highly engineered tanks and ASME certifications limit vendor substitutability, increasing post-award lock-in and moderating buyer power.

Lifecycle services and TerraVest’s North American multi-plant footprint (2024) shift focus to uptime, delivery and service over pure price.

| Factor | 2024 Signal |

|---|---|

| Procurement | RFPs, large EPCs |

| Switching | ASME re-certification friction |

| Aftermarket | Service-led stickiness |

Preview the Actual Deliverable

TerraVest Porter's Five Forces Analysis

This TerraVest Porter’s Five Forces Analysis preview is the exact document you’ll receive after purchase—fully written, formatted, and ready to download. No placeholders, no mockups, and no edits required. Complete and professional, it’s the same file available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

TerraVest’s Porter's Five Forces snapshot highlights moderate supplier power, fragmented buyer segments, strong rivalry among niche industrial competitors, low threat of substitutes, and meaningful scale-based entry barriers. These dynamics suggest steady margins but sensitivity to commodity costs and consolidation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Core inputs—steel plate, specialty alloys, valves and instrumentation—are concentrated among certified mills and OEMs, giving suppliers leverage; TerraVest’s scale improves pricing negotiation but certification and OEM approvals limit rapid switching. Metals price swings have pressured margins, and mill lead times can exceed 20 weeks in strong upcycles, tightening supply and allocation.

Supplier Power 2

Compliance with ASME, API and CRN narrows qualified supplier pools, concentrating leverage with high-spec vendors and slowing substitution; industry estimates in 2024 show qualified vendor lists shrink supplier universes by roughly 50-70% in pressure-equipment segments. Pre-approved vendor lists and weld procedure qualifications materially raise switching costs and procurement lead times. Audits and traceability requirements extend replacement timelines by months and increase costs, embedding power with certified component suppliers.

Supplier Power 3

Logistics, coatings and field-service subcontractors create multi-tier supplier exposure; freight alone can swing total delivered heavy-equipment cost by 10–15% and regional availability drives variance. Coordinating multi-site deliveries gives larger vendors negotiating leverage, while TerraVest’s diversified North American footprint across more than 20 operating locations in 2024 helps partially mitigate regional bottlenecks.

Supplier Power 4

Long-term contracts, volume bundling and hedging in 2024 cut input-price volatility materially, with procurement hedges and fixed contracts covering an estimated 60% of spend and reducing swing exposure roughly 20%; vendor-managed inventory and consignment for fasteners/valves smooth operations and free up working capital, but high customization for project-specific equipment limits standardization benefits and savings. Dual-sourcing remains constrained by qualification timelines, often taking 6–12 months to onboard a second supplier.

- Coverage: ~60% of spend under fixed/hedged contracts (2024)

- Volatility reduction: ~20% via hedging/bundling (2024)

- VMI/consignment: lowers inventory days and frees working capital

- Dual-sourcing lead time: 6–12 months

Supplier Power 5

Skilled labor—especially welders and NDE technicians—is a critical supplier for TerraVest; tight markets have elevated wage and overtime costs, and industry surveys through 2024 continue to report widespread hiring difficulty. Training pipelines and automation can mitigate shortages but require capital investment and lead times; during peak demand labor availability can become the primary gating constraint.

- Hiring difficulty: industry surveys 2023–24 report majority of firms constrained

- Wage pressure: sustained above‑average increases in fabrication sectors

- Mitigation: training + automation need upfront CAPEX and months to scale

High supplier power; hedges cover ~60%, volatility ~20%

Supplier power is high: certified mills/OEMs and labor scarcity constrain switching; TerraVest covers ~60% of spend with fixed/hedges reducing input volatility ~20% in 2024. Steel lead times often exceed 20 weeks; qualified-vendor pools shrink ~50–70%, and freight can add 10–15% to delivered cost.

| Metric | 2024 |

|---|---|

| Spend under fixed/hedges | ~60% |

| Volatility reduction | ~20% |

| Steel lead time | >20 weeks |

| Qualified vendor shrink | 50–70% |

| Freight impact | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for TerraVest that uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive threats, substitutes, and incumbent protections with strategic commentary suitable for investor reports and internal strategy decks.

A concise one-sheet Porter's Five Forces for TerraVest that distills competitive pressure into an actionable radar chart—ideal for rapid boardroom decisions. No macros, easy to customize with your data and ready to drop into pitch decks.

Customers Bargaining Power

Buyer Power 1

Customers range from oil and gas and chemical to transportation and agriculture, many backed by centralized procurement teams that run competitive RFPs; large EPCs and midstream operators often bid projects exceeding $10 million, heightening price sensitivity. Project scale lets buyers extract price and term concessions, while extended payment schedules and strict warranty demands shift cash-flow and performance risk onto suppliers.

Buyer Power 2

Custom-engineered tanks and pressure vessels for TerraVest are highly specialized, reducing direct comparability across vendors and limiting price-driven switching. Engineering complexity and site-specific requirements create material switching frictions mid-project, often requiring re‑engineering and re-certification under ASME codes. Performance guarantees and certification needs further reinforce vendor lock-in, which moderates buyer power after contract award.

Buyer Power 3

Cyclical end-markets amplify buyer leverage during downturns as capacity chases fewer projects, pressuring pricing and margins. In upcycles, tight lead times and constrained supply can shift power back to manufacturers, improving negotiation leverage. TerraVest’s diversification across industrial, energy, transportation and specialty sectors helps balance cycles, while improved backlog visibility strengthens pricing discipline.

Buyer Power 4

Lifecycle services, maintenance and retrofit work increase customer stickiness for TerraVest, shifting buying criteria from upfront price to aftermarket support and parts availability; multi-year service agreements and embedded relationships reduce pure price competition and soften buyer power where uptime is critical.

- Aftermarket-led purchasing: parts/support > upfront cost

- Multi-year service agreements embed customers

- Uptime-sensitive buyers less price-driven

Buyer Power 5

TerraVest's North American multi-plant footprint in 2024 enables meeting tight schedules and complex logistics, shifting buyer focus from lowest price to on-time delivery and compliance history. Prequalification and past-performance requirements routinely narrow bidder lists, increasing procurement leverage for suppliers with strong execution records. When execution risk dominates, this improves realized pricing and contract stability.

ASME-certified tanks and service-led uptime beat RFP price pressure across industrial buyers

Buyers span oil & gas, chemical, transport and ag with centralized procurement running competitive RFPs, driving price and term pressure on large projects.

Highly engineered tanks and ASME certifications limit vendor substitutability, increasing post-award lock-in and moderating buyer power.

Lifecycle services and TerraVest’s North American multi-plant footprint (2024) shift focus to uptime, delivery and service over pure price.

| Factor | 2024 Signal |

|---|---|

| Procurement | RFPs, large EPCs |

| Switching | ASME re-certification friction |

| Aftermarket | Service-led stickiness |

Preview the Actual Deliverable

TerraVest Porter's Five Forces Analysis

This TerraVest Porter’s Five Forces Analysis preview is the exact document you’ll receive after purchase—fully written, formatted, and ready to download. No placeholders, no mockups, and no edits required. Complete and professional, it’s the same file available instantly upon payment.