TerraVest SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

TerraVest's SWOT snapshot highlights resilient operational strengths, cyclical commodity exposure, and opportunistic asset optimization—key for stakeholders tracking industrial consolidation. Want deeper strategic context and quantified risks? Purchase the full SWOT analysis for a professionally written, editable report with Excel tools to support investment, planning, and pitches.

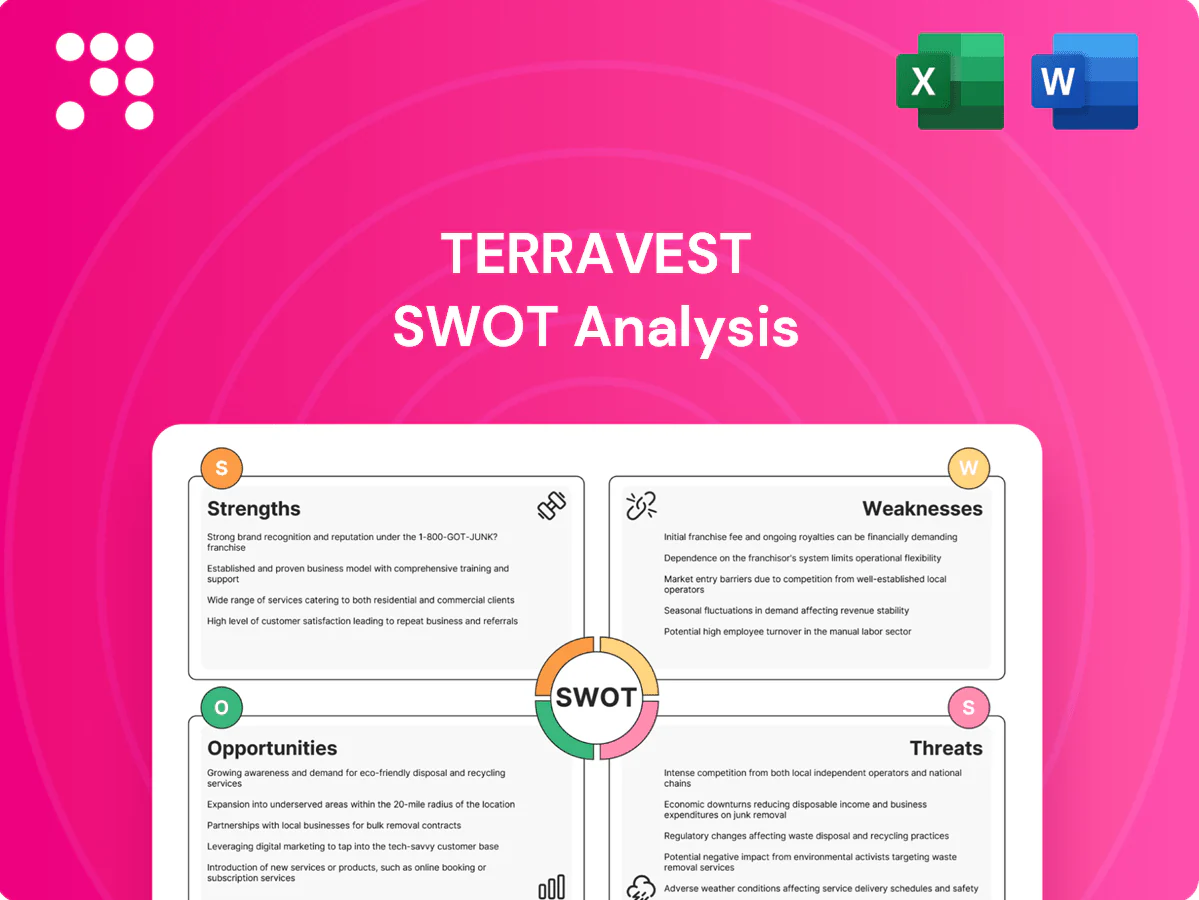

Strengths

Diversified industrial portfolio

Operating across energy, storage and handling, and processing equipment spreads TerraVest's exposure across multiple demand cycles, smoothing revenue volatility when one end market softens. Diversification enables resource sharing and transfer of best practices among units and strengthens negotiating leverage with suppliers and customers.

Deep fabrication and engineering know-how

TerraVest (TSX: TVK) leverages deep fabrication know-how in storage tanks, pressure vessels and specialized equipment to create high barriers to entry and support customized solutions that raise switching costs. Proven quality and regulatory compliance in critical sectors build trust with industrial customers. This technical foundation enables premium pricing in safety-critical applications.

Exposure to essential end markets

TerraVest's exposure to oil & gas, chemical, transportation and agriculture ties it to essential infrastructure sectors that contributed to an estimated global industrial maintenance market of roughly $630 billion in 2024, supporting predictable replacement cycles. These baseline needs generate recurring orders beyond greenfield projects and helped stabilize revenues through 2023–24 downturns. This end-market mix aids resilience across economic cycles.

Acquisition and operating discipline

TerraVest’s disciplined focus on acquiring niche manufacturers compounds capabilities and scale, enabling integration to deliver cost synergies, cross-selling opportunities and margin uplift across platforms.

Its repeatable M&A playbook—executed through dozens of add-on deals—accelerates entry into adjacent niches, while post-acquisition operational improvements have consistently enhanced free cash flow and cash generation.

- Acquisition-led scale

- Cost synergies & cross-selling

- Repeatable add-on model

- Operational cash generation

Aftermarket and service potential

TerraVest's large installed base of tanks and pressure equipment drives steady inspection, repair and retrofit demand, supporting recurring service revenue with higher gross margins than project sales.

Close service touchpoints strengthen customer relationships and supply product-innovation feedback, helping stabilize cash flow against cyclical project revenues.

- Installed base fuels recurring, higher-margin services

- Services deepen customer relationships and R&D insights

- Aftermarket stabilizes cash flow vs project sales

Diversified fabricator leverages add-on M&A and recurring safety-critical aftermarket services

TerraVest (TSX: TVK) combines diversified end-markets and deep fabrication expertise to capture premium, safety-critical work and higher-margin aftermarket services. A repeatable acquisition-led model—executed via dozens of add-ons—drives scale, cross-selling and cash generation. Large installed base supports recurring inspection, repair and retrofit demand that stabilizes revenue through cycles.

| Metric | Value |

|---|---|

| Market context | $630B global industrial maintenance (2024) |

| M&A | Repeatable add-on model; dozens of deals |

What is included in the product

Provides a concise SWOT analysis of TerraVest, mapping its operational strengths and financial weaknesses while highlighting market opportunities and external threats shaping its growth trajectory.

Provides a concise, editable SWOT matrix tailored to TerraVest for rapid strategic alignment and decision-making, enabling executives to visualize strengths, weaknesses, opportunities and threats at a glance and quickly update priorities as market conditions change.

Weaknesses

End-market cyclicality

Exposure to oil and gas and industrial capital spending drives order volatility for TerraVest; energy-sector slowdowns historically lead customers to defer projects and compress pricing. Downturns cause working capital swings that can strain cash and credit lines, raising liquidity risk. Customer capex deferrals make forecasting sales and backlog unpredictable, complicating operational planning.

Scale versus global competitors

Lacking the scale of multinational fabricators lets larger rivals undercut TerraVest on price or outbid for mega-projects, especially in a market where world crude steel production reached about 1,910 million tonnes in 2024 (World Steel Association). Scale limits raise material and logistics cost per unit and weaker brand recognition in international tenders narrows addressable market segments.

Capital and labor intensity

Heavy fabrication forces TerraVest into ongoing capex for equipment, safety and regulatory compliance, pressuring free cash flow during downturns. Skilled welders and technicians are scarce and costly—the U.S. BLS reported median welder wages near $48k annually in 2023—raising labor spend and hiring difficulty. Utilization swings amplify margin variability by several hundred basis points in cyclical projects, while training and retention add recurring overhead and HR investment.

Regulatory compliance burden

Regulatory compliance for pressure vessels and hazardous storage demands ASME Section VIII certification and recurring inspections (commonly every 3–5 years), plus strict third-party audits. Non-compliance risks fines, costly rework, and reputational damage that can delay sales. Documentation, testing and recertification add cycle time and incremental cost and regulatory changes can force redesigns and retraining.

- ASME Section VIII requirement

- Inspections every 3–5 years

- Audits → rework/delays

- Design/retraining risk from rule changes

Geographic concentration risk

Concentration of operations in North America leaves TerraVest vulnerable to regional demand shocks and policy shifts that can disproportionately impact revenue and utilization; a single downturn or tariff change could compress margins rapidly. A limited global footprint constrains access to higher-growth markets in Asia and LatAm, while currency swings on any cross-border sales can erode net margins and unpredictable logistics costs rise for distant exports.

- Regional dependency risk

- Missed high-growth markets

- Currency exposure on exports

- Higher long-haul logistics costs

Energy capex swings, scale limits and welder shortage squeeze margins

Exposure to oil, gas and industrial capex drives order volatility and cash swings; customers defer projects in slowdowns. Lack of multinational scale raises per-unit costs vs larger fabricators while world crude steel output was about 1,910 Mt in 2024. Skilled-welder scarcity (median US welder wage ~48k in 2023) pressures margins.

| Weakness | Key metric |

|---|---|

| Order volatility | Energy capex sensitivity |

| Scale | World steel 1,910 Mt (2024) |

| Labor costs | Welder median ~48k (2023) |

Same Document Delivered

TerraVest SWOT Analysis

This is a live preview of the TerraVest SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The excerpt below is taken directly from the full, editable report and reflects the exact structure and insights included in the downloadable file. Complete access to the entire, detailed document is unlocked immediately after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

TerraVest's SWOT snapshot highlights resilient operational strengths, cyclical commodity exposure, and opportunistic asset optimization—key for stakeholders tracking industrial consolidation. Want deeper strategic context and quantified risks? Purchase the full SWOT analysis for a professionally written, editable report with Excel tools to support investment, planning, and pitches.

Strengths

Diversified industrial portfolio

Operating across energy, storage and handling, and processing equipment spreads TerraVest's exposure across multiple demand cycles, smoothing revenue volatility when one end market softens. Diversification enables resource sharing and transfer of best practices among units and strengthens negotiating leverage with suppliers and customers.

Deep fabrication and engineering know-how

TerraVest (TSX: TVK) leverages deep fabrication know-how in storage tanks, pressure vessels and specialized equipment to create high barriers to entry and support customized solutions that raise switching costs. Proven quality and regulatory compliance in critical sectors build trust with industrial customers. This technical foundation enables premium pricing in safety-critical applications.

Exposure to essential end markets

TerraVest's exposure to oil & gas, chemical, transportation and agriculture ties it to essential infrastructure sectors that contributed to an estimated global industrial maintenance market of roughly $630 billion in 2024, supporting predictable replacement cycles. These baseline needs generate recurring orders beyond greenfield projects and helped stabilize revenues through 2023–24 downturns. This end-market mix aids resilience across economic cycles.

Acquisition and operating discipline

TerraVest’s disciplined focus on acquiring niche manufacturers compounds capabilities and scale, enabling integration to deliver cost synergies, cross-selling opportunities and margin uplift across platforms.

Its repeatable M&A playbook—executed through dozens of add-on deals—accelerates entry into adjacent niches, while post-acquisition operational improvements have consistently enhanced free cash flow and cash generation.

- Acquisition-led scale

- Cost synergies & cross-selling

- Repeatable add-on model

- Operational cash generation

Aftermarket and service potential

TerraVest's large installed base of tanks and pressure equipment drives steady inspection, repair and retrofit demand, supporting recurring service revenue with higher gross margins than project sales.

Close service touchpoints strengthen customer relationships and supply product-innovation feedback, helping stabilize cash flow against cyclical project revenues.

- Installed base fuels recurring, higher-margin services

- Services deepen customer relationships and R&D insights

- Aftermarket stabilizes cash flow vs project sales

Diversified fabricator leverages add-on M&A and recurring safety-critical aftermarket services

TerraVest (TSX: TVK) combines diversified end-markets and deep fabrication expertise to capture premium, safety-critical work and higher-margin aftermarket services. A repeatable acquisition-led model—executed via dozens of add-ons—drives scale, cross-selling and cash generation. Large installed base supports recurring inspection, repair and retrofit demand that stabilizes revenue through cycles.

| Metric | Value |

|---|---|

| Market context | $630B global industrial maintenance (2024) |

| M&A | Repeatable add-on model; dozens of deals |

What is included in the product

Provides a concise SWOT analysis of TerraVest, mapping its operational strengths and financial weaknesses while highlighting market opportunities and external threats shaping its growth trajectory.

Provides a concise, editable SWOT matrix tailored to TerraVest for rapid strategic alignment and decision-making, enabling executives to visualize strengths, weaknesses, opportunities and threats at a glance and quickly update priorities as market conditions change.

Weaknesses

End-market cyclicality

Exposure to oil and gas and industrial capital spending drives order volatility for TerraVest; energy-sector slowdowns historically lead customers to defer projects and compress pricing. Downturns cause working capital swings that can strain cash and credit lines, raising liquidity risk. Customer capex deferrals make forecasting sales and backlog unpredictable, complicating operational planning.

Scale versus global competitors

Lacking the scale of multinational fabricators lets larger rivals undercut TerraVest on price or outbid for mega-projects, especially in a market where world crude steel production reached about 1,910 million tonnes in 2024 (World Steel Association). Scale limits raise material and logistics cost per unit and weaker brand recognition in international tenders narrows addressable market segments.

Capital and labor intensity

Heavy fabrication forces TerraVest into ongoing capex for equipment, safety and regulatory compliance, pressuring free cash flow during downturns. Skilled welders and technicians are scarce and costly—the U.S. BLS reported median welder wages near $48k annually in 2023—raising labor spend and hiring difficulty. Utilization swings amplify margin variability by several hundred basis points in cyclical projects, while training and retention add recurring overhead and HR investment.

Regulatory compliance burden

Regulatory compliance for pressure vessels and hazardous storage demands ASME Section VIII certification and recurring inspections (commonly every 3–5 years), plus strict third-party audits. Non-compliance risks fines, costly rework, and reputational damage that can delay sales. Documentation, testing and recertification add cycle time and incremental cost and regulatory changes can force redesigns and retraining.

- ASME Section VIII requirement

- Inspections every 3–5 years

- Audits → rework/delays

- Design/retraining risk from rule changes

Geographic concentration risk

Concentration of operations in North America leaves TerraVest vulnerable to regional demand shocks and policy shifts that can disproportionately impact revenue and utilization; a single downturn or tariff change could compress margins rapidly. A limited global footprint constrains access to higher-growth markets in Asia and LatAm, while currency swings on any cross-border sales can erode net margins and unpredictable logistics costs rise for distant exports.

- Regional dependency risk

- Missed high-growth markets

- Currency exposure on exports

- Higher long-haul logistics costs

Energy capex swings, scale limits and welder shortage squeeze margins

Exposure to oil, gas and industrial capex drives order volatility and cash swings; customers defer projects in slowdowns. Lack of multinational scale raises per-unit costs vs larger fabricators while world crude steel output was about 1,910 Mt in 2024. Skilled-welder scarcity (median US welder wage ~48k in 2023) pressures margins.

| Weakness | Key metric |

|---|---|

| Order volatility | Energy capex sensitivity |

| Scale | World steel 1,910 Mt (2024) |

| Labor costs | Welder median ~48k (2023) |

Same Document Delivered

TerraVest SWOT Analysis

This is a live preview of the TerraVest SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The excerpt below is taken directly from the full, editable report and reflects the exact structure and insights included in the downloadable file. Complete access to the entire, detailed document is unlocked immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

TerraVest's SWOT snapshot highlights resilient operational strengths, cyclical commodity exposure, and opportunistic asset optimization—key for stakeholders tracking industrial consolidation. Want deeper strategic context and quantified risks? Purchase the full SWOT analysis for a professionally written, editable report with Excel tools to support investment, planning, and pitches.

Strengths

Diversified industrial portfolio

Operating across energy, storage and handling, and processing equipment spreads TerraVest's exposure across multiple demand cycles, smoothing revenue volatility when one end market softens. Diversification enables resource sharing and transfer of best practices among units and strengthens negotiating leverage with suppliers and customers.

Deep fabrication and engineering know-how

TerraVest (TSX: TVK) leverages deep fabrication know-how in storage tanks, pressure vessels and specialized equipment to create high barriers to entry and support customized solutions that raise switching costs. Proven quality and regulatory compliance in critical sectors build trust with industrial customers. This technical foundation enables premium pricing in safety-critical applications.

Exposure to essential end markets

TerraVest's exposure to oil & gas, chemical, transportation and agriculture ties it to essential infrastructure sectors that contributed to an estimated global industrial maintenance market of roughly $630 billion in 2024, supporting predictable replacement cycles. These baseline needs generate recurring orders beyond greenfield projects and helped stabilize revenues through 2023–24 downturns. This end-market mix aids resilience across economic cycles.

Acquisition and operating discipline

TerraVest’s disciplined focus on acquiring niche manufacturers compounds capabilities and scale, enabling integration to deliver cost synergies, cross-selling opportunities and margin uplift across platforms.

Its repeatable M&A playbook—executed through dozens of add-on deals—accelerates entry into adjacent niches, while post-acquisition operational improvements have consistently enhanced free cash flow and cash generation.

- Acquisition-led scale

- Cost synergies & cross-selling

- Repeatable add-on model

- Operational cash generation

Aftermarket and service potential

TerraVest's large installed base of tanks and pressure equipment drives steady inspection, repair and retrofit demand, supporting recurring service revenue with higher gross margins than project sales.

Close service touchpoints strengthen customer relationships and supply product-innovation feedback, helping stabilize cash flow against cyclical project revenues.

- Installed base fuels recurring, higher-margin services

- Services deepen customer relationships and R&D insights

- Aftermarket stabilizes cash flow vs project sales

Diversified fabricator leverages add-on M&A and recurring safety-critical aftermarket services

TerraVest (TSX: TVK) combines diversified end-markets and deep fabrication expertise to capture premium, safety-critical work and higher-margin aftermarket services. A repeatable acquisition-led model—executed via dozens of add-ons—drives scale, cross-selling and cash generation. Large installed base supports recurring inspection, repair and retrofit demand that stabilizes revenue through cycles.

| Metric | Value |

|---|---|

| Market context | $630B global industrial maintenance (2024) |

| M&A | Repeatable add-on model; dozens of deals |

What is included in the product

Provides a concise SWOT analysis of TerraVest, mapping its operational strengths and financial weaknesses while highlighting market opportunities and external threats shaping its growth trajectory.

Provides a concise, editable SWOT matrix tailored to TerraVest for rapid strategic alignment and decision-making, enabling executives to visualize strengths, weaknesses, opportunities and threats at a glance and quickly update priorities as market conditions change.

Weaknesses

End-market cyclicality

Exposure to oil and gas and industrial capital spending drives order volatility for TerraVest; energy-sector slowdowns historically lead customers to defer projects and compress pricing. Downturns cause working capital swings that can strain cash and credit lines, raising liquidity risk. Customer capex deferrals make forecasting sales and backlog unpredictable, complicating operational planning.

Scale versus global competitors

Lacking the scale of multinational fabricators lets larger rivals undercut TerraVest on price or outbid for mega-projects, especially in a market where world crude steel production reached about 1,910 million tonnes in 2024 (World Steel Association). Scale limits raise material and logistics cost per unit and weaker brand recognition in international tenders narrows addressable market segments.

Capital and labor intensity

Heavy fabrication forces TerraVest into ongoing capex for equipment, safety and regulatory compliance, pressuring free cash flow during downturns. Skilled welders and technicians are scarce and costly—the U.S. BLS reported median welder wages near $48k annually in 2023—raising labor spend and hiring difficulty. Utilization swings amplify margin variability by several hundred basis points in cyclical projects, while training and retention add recurring overhead and HR investment.

Regulatory compliance burden

Regulatory compliance for pressure vessels and hazardous storage demands ASME Section VIII certification and recurring inspections (commonly every 3–5 years), plus strict third-party audits. Non-compliance risks fines, costly rework, and reputational damage that can delay sales. Documentation, testing and recertification add cycle time and incremental cost and regulatory changes can force redesigns and retraining.

- ASME Section VIII requirement

- Inspections every 3–5 years

- Audits → rework/delays

- Design/retraining risk from rule changes

Geographic concentration risk

Concentration of operations in North America leaves TerraVest vulnerable to regional demand shocks and policy shifts that can disproportionately impact revenue and utilization; a single downturn or tariff change could compress margins rapidly. A limited global footprint constrains access to higher-growth markets in Asia and LatAm, while currency swings on any cross-border sales can erode net margins and unpredictable logistics costs rise for distant exports.

- Regional dependency risk

- Missed high-growth markets

- Currency exposure on exports

- Higher long-haul logistics costs

Energy capex swings, scale limits and welder shortage squeeze margins

Exposure to oil, gas and industrial capex drives order volatility and cash swings; customers defer projects in slowdowns. Lack of multinational scale raises per-unit costs vs larger fabricators while world crude steel output was about 1,910 Mt in 2024. Skilled-welder scarcity (median US welder wage ~48k in 2023) pressures margins.

| Weakness | Key metric |

|---|---|

| Order volatility | Energy capex sensitivity |

| Scale | World steel 1,910 Mt (2024) |

| Labor costs | Welder median ~48k (2023) |

Same Document Delivered

TerraVest SWOT Analysis

This is a live preview of the TerraVest SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The excerpt below is taken directly from the full, editable report and reflects the exact structure and insights included in the downloadable file. Complete access to the entire, detailed document is unlocked immediately after checkout.