R&S Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

R&S Group shows resilient market positioning with strong client relationships and diversified services, but faces margin pressure from rising costs and competitive digital challengers. Our full SWOT unpacks risks, growth levers, and strategic moves with evidence and financial context. Purchase the complete, editable report to plan, pitch, or invest with confidence.

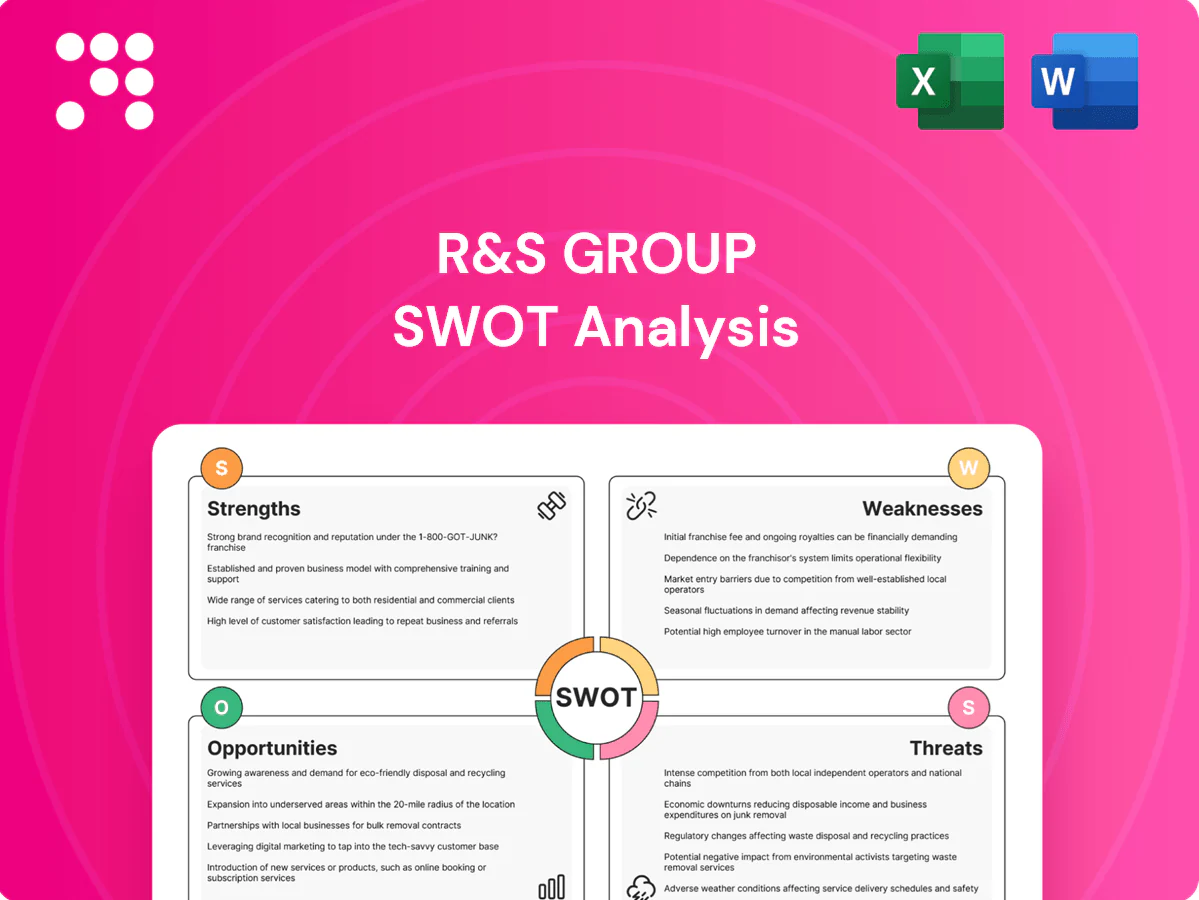

Strengths

Broad end-to-end electrical solutions

R&S Group delivers full-spectrum electrical services from design through installation and commissioning, minimizing vendor fragmentation and consolidating single-source responsibility. Integration of switchgear, automation and control measurably improves system performance and traceability, supporting uptime targets. Industry studies (2024) report integrated delivery shortens project timelines by ~20% and can reduce total cost of ownership 10–15%.

Deep expertise in switchgear and automation

Core technical strengths in power distribution, PLCs and advanced control systems enable R&S Group to deliver reliable, high-spec builds that meet IEC 62271 standards and industrial SCADA integration. This capability supports complex industrial and commercial projects with uptime targets commonly set at 99.9% to 99.999% for critical sites. It differentiates R&S from commodity installers by enabling higher-margin, specification-driven contracts and long-term service agreements.

Diversified sector exposure

Serving residential, commercial and industrial segments spreads demand risk across three end-markets, smoothing revenue swings when one vertical weakens. Cyclicality in commercial real estate in 2024 contrasted with steadier residential renovation demand, helping offset downturns. Cross-segment referenceability drives learning effects and operational improvements, supporting margin resilience and bid competitiveness.

Quality reputation and compliance focus

R&S Group's emphasis on standards, testing, and documentation builds trust with safety-critical clients and aligns with ISO 9001 practices (over 1 million certified organizations worldwide), driving lower failure rates that cut warranty exposure and encourage repeat business. Strong QA/QC directly improves tender competitiveness in highly regulated sectors.

- Standards-focused: ISO-aligned; global benchmark

- Lower failures: fewer warranty claims

- Tender wins: edge in regulated bids

Customer-centric customization

Bespoke engineering and flexible delivery models allow R&S Group to align solutions to client constraints, reducing deployment time and increasing fit-for-purpose adoption; tailored panels, controls and software integration raise switching costs and deepen platform dependency; close collaboration drives long-term accounts and service pull-through, supporting higher retention—a 5% retention lift can boost profits 25–95% (Bain).

- Client-fit solutions

- Higher switching costs

- Service-led revenue growth

Integrated electrical delivery: cut timelines ~20%, TCO 10–15%, uptime 99.9–99.999%

R&S Group offers integrated design-to-commission electrical delivery, cutting timelines ~20% and TCO 10–15% (2024 studies). Core strengths in power distribution, PLCs and SCADA support 99.9–99.999% uptime for critical sites and IEC 62271 compliance. Multi-segment exposure (res, comm, ind) smooths revenue; ISO-aligned QA reduces failures and warranty exposure. Bespoke engineering lifts retention and long-term service revenues.

| Metric | Value | Source/Year |

|---|---|---|

| Project timeline reduction | ~20% | Industry studies 2024 |

| TCO reduction | 10–15% | Industry studies 2024 |

| Uptime targets | 99.9–99.999% | Client SLAs 2024–25 |

| ISO 9001 base | 1M+ orgs globally | ISO data 2024 |

What is included in the product

Offers a strategic overview of R&S Group’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and the key risks shaping its future.

Provides a concise SWOT matrix tailored to R&S Group for quick strategic alignment and decision-making, enabling leaders to pinpoint priorities, mitigate risks, and streamline action planning at a glance.

Weaknesses

Project-driven revenue volatility

Backlog timing and milestone billing create lumpy cash flows, with milestone-dependent collections producing quarter-to-quarter revenue swings. Seasonal and tender-driven demand spikes strain capacity planning and raise overtime or subcontracting costs. Forecast accuracy is highly sensitive to a few large awards, which often exceed 20% of annual revenue.

Skilled labor dependency

Execution quality at R&S Group hinges on scarce electricians, panel builders and automation engineers; BLS reports 733,500 electricians employed in May 2024 with a median annual wage of $62,350, highlighting tight market demand. Industry hiring strains are acute—AGC’s 2023 survey found 89% of contractors struggled to recruit qualified craft workers—driving up labor costs and risking schedule slippage. High turnover amplifies knowledge loss, degrading delivery consistency and raising rework exposure.

Margin pressure from input costs

Switchgear components and semiconductors face volatile pricing and long lead times — industry lead times often range 12–40 weeks and spot price swings reached up to 30% during 2021–24 supply shocks. Fixed-price contracts therefore can compress gross margins when input costs rise, historically shaving several percentage points off project margins. Hedging and indexation are often infeasible in competitive tenders, leaving R&S exposed to raw-material and chip volatility.

Limited scale versus global OEMs

Smaller purchasing power often translates into 5–12% higher component costs versus global OEMs (industry procurement studies, 2023–24), and weaker payment/lead-time terms that compress margins. Lower brand visibility reduces success rates in major bids: multinationals captured the bulk of large frame agreements in 2023–24. This limits access to mega-projects >$250m where scale and balance-sheet are decisive.

- Higher procurement costs: +5–12% (2023–24)

- Weaker commercial terms and cash conversion

- Lower win rate on mega-projects and frame agreements

- Brand visibility gap versus global OEMs

Working capital intensity

Working capital intensity: inventory, WIP and retention payments tie up cash; long certification cycles delay billing and in 2024 often extend 6–12 months for regulated projects; negative cash-conversion cycles can constrain organic growth unless external financing is secured.

- Inventory/WIP lock-up

- Retention payments delayed

- 6–12 month certification lag (2024)

- Negative CCC limits growth

Backlog-driven lumpiness: top awards >20% revenue; supply shocks add +5-12% premium

Backlog timing and milestone billing produce lumpy cash flows, with top awards often >20% of annual revenue. Skilled-labor scarcity (BLS May 2024: 733,500 electricians; median wage $62,350) raises labor costs and turnover risk. Supply shocks (lead times 12–40 weeks) and +5–12% procurement premium compress margins and extend certification lags 6–12 months.

| Metric | Value |

|---|---|

| Large-awards concentration | >20% revenue |

| Electricians (May 2024) | 733,500 / $62,350 |

| Lead times | 12–40 weeks |

| Procurement premium | +5–12% |

| Certification lag | 6–12 months |

Full Version Awaits

R&S Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version, ready for immediate download.

Make Insightful Decisions Backed by Expert Research

R&S Group shows resilient market positioning with strong client relationships and diversified services, but faces margin pressure from rising costs and competitive digital challengers. Our full SWOT unpacks risks, growth levers, and strategic moves with evidence and financial context. Purchase the complete, editable report to plan, pitch, or invest with confidence.

Strengths

Broad end-to-end electrical solutions

R&S Group delivers full-spectrum electrical services from design through installation and commissioning, minimizing vendor fragmentation and consolidating single-source responsibility. Integration of switchgear, automation and control measurably improves system performance and traceability, supporting uptime targets. Industry studies (2024) report integrated delivery shortens project timelines by ~20% and can reduce total cost of ownership 10–15%.

Deep expertise in switchgear and automation

Core technical strengths in power distribution, PLCs and advanced control systems enable R&S Group to deliver reliable, high-spec builds that meet IEC 62271 standards and industrial SCADA integration. This capability supports complex industrial and commercial projects with uptime targets commonly set at 99.9% to 99.999% for critical sites. It differentiates R&S from commodity installers by enabling higher-margin, specification-driven contracts and long-term service agreements.

Diversified sector exposure

Serving residential, commercial and industrial segments spreads demand risk across three end-markets, smoothing revenue swings when one vertical weakens. Cyclicality in commercial real estate in 2024 contrasted with steadier residential renovation demand, helping offset downturns. Cross-segment referenceability drives learning effects and operational improvements, supporting margin resilience and bid competitiveness.

Quality reputation and compliance focus

R&S Group's emphasis on standards, testing, and documentation builds trust with safety-critical clients and aligns with ISO 9001 practices (over 1 million certified organizations worldwide), driving lower failure rates that cut warranty exposure and encourage repeat business. Strong QA/QC directly improves tender competitiveness in highly regulated sectors.

- Standards-focused: ISO-aligned; global benchmark

- Lower failures: fewer warranty claims

- Tender wins: edge in regulated bids

Customer-centric customization

Bespoke engineering and flexible delivery models allow R&S Group to align solutions to client constraints, reducing deployment time and increasing fit-for-purpose adoption; tailored panels, controls and software integration raise switching costs and deepen platform dependency; close collaboration drives long-term accounts and service pull-through, supporting higher retention—a 5% retention lift can boost profits 25–95% (Bain).

- Client-fit solutions

- Higher switching costs

- Service-led revenue growth

Integrated electrical delivery: cut timelines ~20%, TCO 10–15%, uptime 99.9–99.999%

R&S Group offers integrated design-to-commission electrical delivery, cutting timelines ~20% and TCO 10–15% (2024 studies). Core strengths in power distribution, PLCs and SCADA support 99.9–99.999% uptime for critical sites and IEC 62271 compliance. Multi-segment exposure (res, comm, ind) smooths revenue; ISO-aligned QA reduces failures and warranty exposure. Bespoke engineering lifts retention and long-term service revenues.

| Metric | Value | Source/Year |

|---|---|---|

| Project timeline reduction | ~20% | Industry studies 2024 |

| TCO reduction | 10–15% | Industry studies 2024 |

| Uptime targets | 99.9–99.999% | Client SLAs 2024–25 |

| ISO 9001 base | 1M+ orgs globally | ISO data 2024 |

What is included in the product

Offers a strategic overview of R&S Group’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and the key risks shaping its future.

Provides a concise SWOT matrix tailored to R&S Group for quick strategic alignment and decision-making, enabling leaders to pinpoint priorities, mitigate risks, and streamline action planning at a glance.

Weaknesses

Project-driven revenue volatility

Backlog timing and milestone billing create lumpy cash flows, with milestone-dependent collections producing quarter-to-quarter revenue swings. Seasonal and tender-driven demand spikes strain capacity planning and raise overtime or subcontracting costs. Forecast accuracy is highly sensitive to a few large awards, which often exceed 20% of annual revenue.

Skilled labor dependency

Execution quality at R&S Group hinges on scarce electricians, panel builders and automation engineers; BLS reports 733,500 electricians employed in May 2024 with a median annual wage of $62,350, highlighting tight market demand. Industry hiring strains are acute—AGC’s 2023 survey found 89% of contractors struggled to recruit qualified craft workers—driving up labor costs and risking schedule slippage. High turnover amplifies knowledge loss, degrading delivery consistency and raising rework exposure.

Margin pressure from input costs

Switchgear components and semiconductors face volatile pricing and long lead times — industry lead times often range 12–40 weeks and spot price swings reached up to 30% during 2021–24 supply shocks. Fixed-price contracts therefore can compress gross margins when input costs rise, historically shaving several percentage points off project margins. Hedging and indexation are often infeasible in competitive tenders, leaving R&S exposed to raw-material and chip volatility.

Limited scale versus global OEMs

Smaller purchasing power often translates into 5–12% higher component costs versus global OEMs (industry procurement studies, 2023–24), and weaker payment/lead-time terms that compress margins. Lower brand visibility reduces success rates in major bids: multinationals captured the bulk of large frame agreements in 2023–24. This limits access to mega-projects >$250m where scale and balance-sheet are decisive.

- Higher procurement costs: +5–12% (2023–24)

- Weaker commercial terms and cash conversion

- Lower win rate on mega-projects and frame agreements

- Brand visibility gap versus global OEMs

Working capital intensity

Working capital intensity: inventory, WIP and retention payments tie up cash; long certification cycles delay billing and in 2024 often extend 6–12 months for regulated projects; negative cash-conversion cycles can constrain organic growth unless external financing is secured.

- Inventory/WIP lock-up

- Retention payments delayed

- 6–12 month certification lag (2024)

- Negative CCC limits growth

Backlog-driven lumpiness: top awards >20% revenue; supply shocks add +5-12% premium

Backlog timing and milestone billing produce lumpy cash flows, with top awards often >20% of annual revenue. Skilled-labor scarcity (BLS May 2024: 733,500 electricians; median wage $62,350) raises labor costs and turnover risk. Supply shocks (lead times 12–40 weeks) and +5–12% procurement premium compress margins and extend certification lags 6–12 months.

| Metric | Value |

|---|---|

| Large-awards concentration | >20% revenue |

| Electricians (May 2024) | 733,500 / $62,350 |

| Lead times | 12–40 weeks |

| Procurement premium | +5–12% |

| Certification lag | 6–12 months |

Full Version Awaits

R&S Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version, ready for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

R&S Group shows resilient market positioning with strong client relationships and diversified services, but faces margin pressure from rising costs and competitive digital challengers. Our full SWOT unpacks risks, growth levers, and strategic moves with evidence and financial context. Purchase the complete, editable report to plan, pitch, or invest with confidence.

Strengths

Broad end-to-end electrical solutions

R&S Group delivers full-spectrum electrical services from design through installation and commissioning, minimizing vendor fragmentation and consolidating single-source responsibility. Integration of switchgear, automation and control measurably improves system performance and traceability, supporting uptime targets. Industry studies (2024) report integrated delivery shortens project timelines by ~20% and can reduce total cost of ownership 10–15%.

Deep expertise in switchgear and automation

Core technical strengths in power distribution, PLCs and advanced control systems enable R&S Group to deliver reliable, high-spec builds that meet IEC 62271 standards and industrial SCADA integration. This capability supports complex industrial and commercial projects with uptime targets commonly set at 99.9% to 99.999% for critical sites. It differentiates R&S from commodity installers by enabling higher-margin, specification-driven contracts and long-term service agreements.

Diversified sector exposure

Serving residential, commercial and industrial segments spreads demand risk across three end-markets, smoothing revenue swings when one vertical weakens. Cyclicality in commercial real estate in 2024 contrasted with steadier residential renovation demand, helping offset downturns. Cross-segment referenceability drives learning effects and operational improvements, supporting margin resilience and bid competitiveness.

Quality reputation and compliance focus

R&S Group's emphasis on standards, testing, and documentation builds trust with safety-critical clients and aligns with ISO 9001 practices (over 1 million certified organizations worldwide), driving lower failure rates that cut warranty exposure and encourage repeat business. Strong QA/QC directly improves tender competitiveness in highly regulated sectors.

- Standards-focused: ISO-aligned; global benchmark

- Lower failures: fewer warranty claims

- Tender wins: edge in regulated bids

Customer-centric customization

Bespoke engineering and flexible delivery models allow R&S Group to align solutions to client constraints, reducing deployment time and increasing fit-for-purpose adoption; tailored panels, controls and software integration raise switching costs and deepen platform dependency; close collaboration drives long-term accounts and service pull-through, supporting higher retention—a 5% retention lift can boost profits 25–95% (Bain).

- Client-fit solutions

- Higher switching costs

- Service-led revenue growth

Integrated electrical delivery: cut timelines ~20%, TCO 10–15%, uptime 99.9–99.999%

R&S Group offers integrated design-to-commission electrical delivery, cutting timelines ~20% and TCO 10–15% (2024 studies). Core strengths in power distribution, PLCs and SCADA support 99.9–99.999% uptime for critical sites and IEC 62271 compliance. Multi-segment exposure (res, comm, ind) smooths revenue; ISO-aligned QA reduces failures and warranty exposure. Bespoke engineering lifts retention and long-term service revenues.

| Metric | Value | Source/Year |

|---|---|---|

| Project timeline reduction | ~20% | Industry studies 2024 |

| TCO reduction | 10–15% | Industry studies 2024 |

| Uptime targets | 99.9–99.999% | Client SLAs 2024–25 |

| ISO 9001 base | 1M+ orgs globally | ISO data 2024 |

What is included in the product

Offers a strategic overview of R&S Group’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and the key risks shaping its future.

Provides a concise SWOT matrix tailored to R&S Group for quick strategic alignment and decision-making, enabling leaders to pinpoint priorities, mitigate risks, and streamline action planning at a glance.

Weaknesses

Project-driven revenue volatility

Backlog timing and milestone billing create lumpy cash flows, with milestone-dependent collections producing quarter-to-quarter revenue swings. Seasonal and tender-driven demand spikes strain capacity planning and raise overtime or subcontracting costs. Forecast accuracy is highly sensitive to a few large awards, which often exceed 20% of annual revenue.

Skilled labor dependency

Execution quality at R&S Group hinges on scarce electricians, panel builders and automation engineers; BLS reports 733,500 electricians employed in May 2024 with a median annual wage of $62,350, highlighting tight market demand. Industry hiring strains are acute—AGC’s 2023 survey found 89% of contractors struggled to recruit qualified craft workers—driving up labor costs and risking schedule slippage. High turnover amplifies knowledge loss, degrading delivery consistency and raising rework exposure.

Margin pressure from input costs

Switchgear components and semiconductors face volatile pricing and long lead times — industry lead times often range 12–40 weeks and spot price swings reached up to 30% during 2021–24 supply shocks. Fixed-price contracts therefore can compress gross margins when input costs rise, historically shaving several percentage points off project margins. Hedging and indexation are often infeasible in competitive tenders, leaving R&S exposed to raw-material and chip volatility.

Limited scale versus global OEMs

Smaller purchasing power often translates into 5–12% higher component costs versus global OEMs (industry procurement studies, 2023–24), and weaker payment/lead-time terms that compress margins. Lower brand visibility reduces success rates in major bids: multinationals captured the bulk of large frame agreements in 2023–24. This limits access to mega-projects >$250m where scale and balance-sheet are decisive.

- Higher procurement costs: +5–12% (2023–24)

- Weaker commercial terms and cash conversion

- Lower win rate on mega-projects and frame agreements

- Brand visibility gap versus global OEMs

Working capital intensity

Working capital intensity: inventory, WIP and retention payments tie up cash; long certification cycles delay billing and in 2024 often extend 6–12 months for regulated projects; negative cash-conversion cycles can constrain organic growth unless external financing is secured.

- Inventory/WIP lock-up

- Retention payments delayed

- 6–12 month certification lag (2024)

- Negative CCC limits growth

Backlog-driven lumpiness: top awards >20% revenue; supply shocks add +5-12% premium

Backlog timing and milestone billing produce lumpy cash flows, with top awards often >20% of annual revenue. Skilled-labor scarcity (BLS May 2024: 733,500 electricians; median wage $62,350) raises labor costs and turnover risk. Supply shocks (lead times 12–40 weeks) and +5–12% procurement premium compress margins and extend certification lags 6–12 months.

| Metric | Value |

|---|---|

| Large-awards concentration | >20% revenue |

| Electricians (May 2024) | 733,500 / $62,350 |

| Lead times | 12–40 weeks |

| Procurement premium | +5–12% |

| Certification lag | 6–12 months |

Full Version Awaits

R&S Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth, editable version, ready for immediate download.