The Arena Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

The Arena Group SWOT Analysis highlights content strengths, monetization opportunities, and competitive risks while identifying strategic growth drivers across digital media. Want the full story? Purchase the complete SWOT for a research-backed, editable Word report plus Excel matrix—ideal for investors, strategists, and advisors.

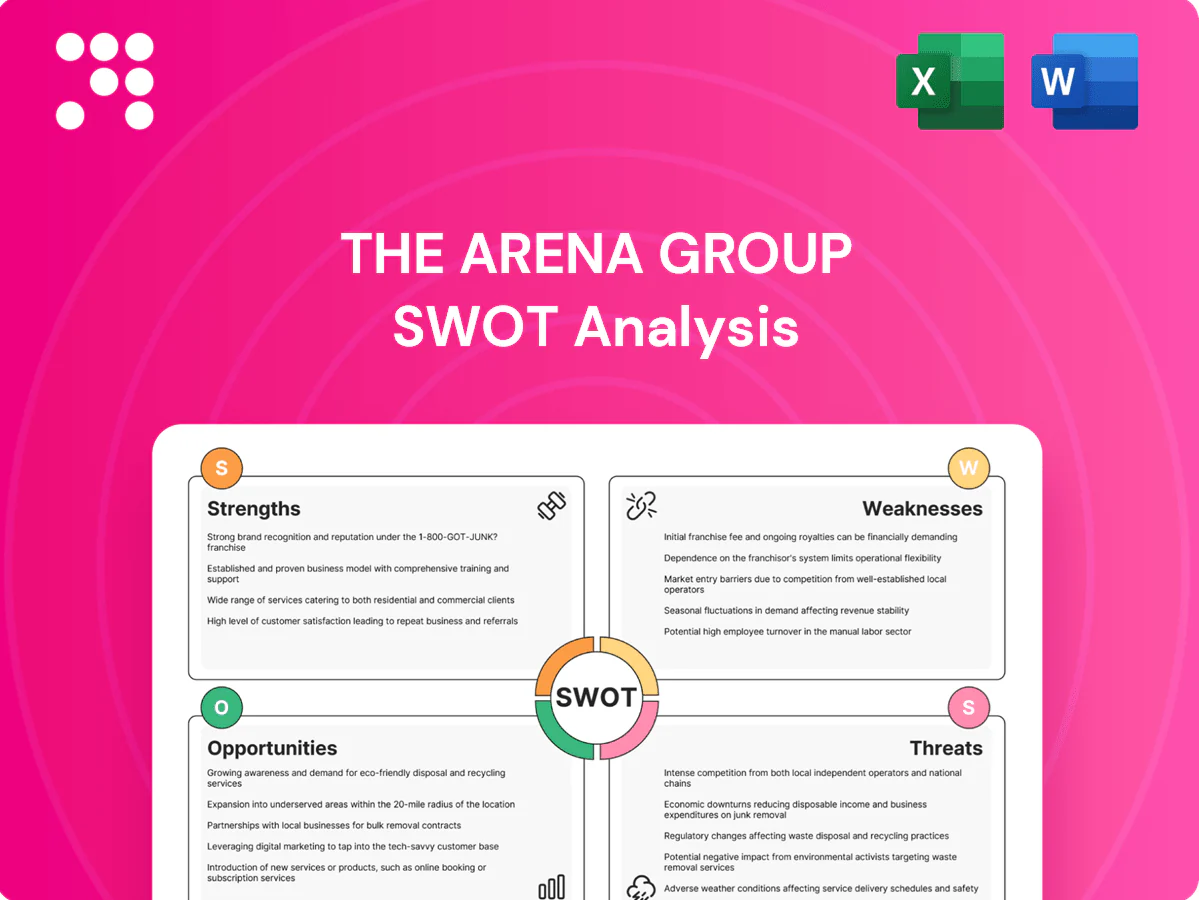

Strengths

Iconic brand portfolio

Ownership of Sports Illustrated (founded 1954), TheStreet (1996) and Parade (1941) gives The Arena Group strong brand equity and built-in audiences. These legacy titles enhance advertiser trust and support higher CPMs across sports, finance and lifestyle verticals. Cross-promotion among properties amplifies reach and customer lifetime value. Heritage credibility helps secure partnerships and premium content access.

Scalable tech platform

Centralized publishing, analytics, and monetization tools at The Arena Group streamline workflows to speed time-to-market and maintain consistent quality across brands; the company owns Sports Illustrated among its flagship properties. Shared technology lowers marginal content costs and standardizes best practices, while data-driven optimization has improved engagement and ad yield across its network. Platform scale enables rapid onboarding of new creators and properties, supporting portfolio expansion.

Diversified revenue mix

Digital advertising remains core but Arena Group supplements it with subscriptions and memberships across over 35 digital brands, reducing single-stream dependency. Multiple verticals such as sports, automotive and finance help offset cyclical ad softness with recurring subscription revenue. Branded content and sponsorships provide higher-margin revenue lines, while subscription data strengthens first-party audience profiles for improved monetization.

Creator-centric model

Audience scale and engagement

The Arena Group leverages flagship brands such as Sports Illustrated and TheStreet to span sports, finance and lifestyle, reaching diverse demographics with both evergreen and event-driven content tied to seasons, earnings cycles and awards calendars. Strong SEO from long-form journalism and branded franchises drives sustained organic discovery, while social distribution amplifies reach and lowers acquisition cost per user.

- Brand portfolio: Sports Illustrated, TheStreet, Parade

- Content mix: evergreen + event-driven

- Channels: SEO-led organic discovery + social amplification

Legacy titles and creator-driven scale: 35+ brands, $250B creator economy

The Arena Group owns flagship titles (Sports Illustrated 1954, TheStreet 1996, Parade 1941), delivering strong brand equity, higher CPMs and advertiser trust. Centralized platform and 35+ digital brands cut marginal costs and boost SEO-driven reach. Creator-centric model taps the $250B creator economy to scale content velocity and subscription diversification.

| Metric | Value |

|---|---|

| Flagship brands | Sports Illustrated, TheStreet, Parade |

| Brand count | 35+ digital brands |

| Creator economy | $250B (SignalFire 2021) |

What is included in the product

Provides a concise SWOT analysis of The Arena Group, highlighting internal capabilities and operational weaknesses, market opportunities in digital publishing and content monetization, and external threats from competition, platform changes, and advertising volatility.

Provides a focused SWOT matrix tailored to The Arena Group for rapid strategic alignment and stakeholder briefings; editable format enables quick updates to reflect evolving digital media priorities.

Weaknesses

Ad market sensitivity

Heavy reliance on digital advertising makes Arena Group revenue cyclical and volatile, with advertiser budget shifts translating quickly into quarterly swings. CPM compression and shifting demand have pressured margins, mirroring industry trends where programmatic now handles over 70% of display buying and drove mid-single-digit CPM declines in 2024. Dependence on programmatic reduces pricing control and magnifies the impact of advertiser pullbacks on results.

Brand stewardship risk

Managing legacy brands like Sports Illustrated and Parade requires continuous investment to maintain quality and relevance, with content and licensing spend driving operating costs. Missteps in editorial standards or licensing can rapidly erode trust, and with over 5 billion social media users in 2024, audience backlash spreads quickly. Rebuilding damaged brand equity is costly and often takes years and millions in remediation and marketing spend. Brand stewardship risk therefore represents a material operational vulnerability.

Platform dependence

The Arena Group’s reliance on search and social algorithms leaves site traffic vulnerable to exogenous shocks; Google controls ~92% of global search (StatCounter 2025) and Meta’s family reaches ~3.0B monthly users (Meta 2024), so algorithm or iOS privacy changes can sharply reduce reach. Limited bargaining power with these gatekeepers constrains growth, requiring sustained investment in direct channels and first-party data.

Subscription scale constraints

Converting large casual audiences into paying users is difficult—industry conversion for digital publishers was about 1–3% in 2024, constraining Arena Group’s subscription scale. Paywall strategy must balance reach with monetization, since aggressive metering can erode ad-driven reach. Media subscription churn averaged ~20–35% in 2024, requiring continual product upgrades and exclusive content to preserve LTV versus rising CAC.

- Conversion rate: 1–3% (2024 industry)

- Churn: ~20–35% (2024)

- CAC pressure vs LTV: high CAC dilutes unit economics

Operational complexity

Operational complexity: Multi-brand, multi-vertical operations raise coordination costs as creators, sales, and tech roadmaps demand intensive cross-functional alignment; fragmented content calendars hinder accurate inventory forecasting and slow monetization cycles; legal and licensing across properties increase compliance overhead and risk exposure.

- Coordination costs

- Roadmap integration strain

- Forecasting fragmentation

- Elevated legal/licensing burden

Programmatic >70%, paywall conversion 1-3% drive revenue volatility

Heavy ad reliance and programmatic pricing pressure (programmatic >70%; mid-single-digit CPM decline in 2024) create revenue volatility. Brand stewardship of legacy titles raises ongoing content and licensing costs and reputational risk. Platform dependence (Google ~92% search; Meta ~3.0B monthly) and low subscription conversion (1–3%) with churn (20–35%) constrain scalable monetization.

| Metric | Value |

|---|---|

| Programmatic share | >70% |

| CPM trend 2024 | mid-single-digit decline |

| Google search share | ~92% (2025) |

| Meta reach | ~3.0B monthly (2024) |

| Subscription conv | 1–3% (2024) |

| Churn | 20–35% (2024) |

Full Version Awaits

The Arena Group SWOT Analysis

This is the actual The Arena Group SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and insights. Purchase unlocks the complete, editable version immediately after checkout.

Make Insightful Decisions Backed by Expert Research

The Arena Group SWOT Analysis highlights content strengths, monetization opportunities, and competitive risks while identifying strategic growth drivers across digital media. Want the full story? Purchase the complete SWOT for a research-backed, editable Word report plus Excel matrix—ideal for investors, strategists, and advisors.

Strengths

Iconic brand portfolio

Ownership of Sports Illustrated (founded 1954), TheStreet (1996) and Parade (1941) gives The Arena Group strong brand equity and built-in audiences. These legacy titles enhance advertiser trust and support higher CPMs across sports, finance and lifestyle verticals. Cross-promotion among properties amplifies reach and customer lifetime value. Heritage credibility helps secure partnerships and premium content access.

Scalable tech platform

Centralized publishing, analytics, and monetization tools at The Arena Group streamline workflows to speed time-to-market and maintain consistent quality across brands; the company owns Sports Illustrated among its flagship properties. Shared technology lowers marginal content costs and standardizes best practices, while data-driven optimization has improved engagement and ad yield across its network. Platform scale enables rapid onboarding of new creators and properties, supporting portfolio expansion.

Diversified revenue mix

Digital advertising remains core but Arena Group supplements it with subscriptions and memberships across over 35 digital brands, reducing single-stream dependency. Multiple verticals such as sports, automotive and finance help offset cyclical ad softness with recurring subscription revenue. Branded content and sponsorships provide higher-margin revenue lines, while subscription data strengthens first-party audience profiles for improved monetization.

Creator-centric model

Audience scale and engagement

The Arena Group leverages flagship brands such as Sports Illustrated and TheStreet to span sports, finance and lifestyle, reaching diverse demographics with both evergreen and event-driven content tied to seasons, earnings cycles and awards calendars. Strong SEO from long-form journalism and branded franchises drives sustained organic discovery, while social distribution amplifies reach and lowers acquisition cost per user.

- Brand portfolio: Sports Illustrated, TheStreet, Parade

- Content mix: evergreen + event-driven

- Channels: SEO-led organic discovery + social amplification

Legacy titles and creator-driven scale: 35+ brands, $250B creator economy

The Arena Group owns flagship titles (Sports Illustrated 1954, TheStreet 1996, Parade 1941), delivering strong brand equity, higher CPMs and advertiser trust. Centralized platform and 35+ digital brands cut marginal costs and boost SEO-driven reach. Creator-centric model taps the $250B creator economy to scale content velocity and subscription diversification.

| Metric | Value |

|---|---|

| Flagship brands | Sports Illustrated, TheStreet, Parade |

| Brand count | 35+ digital brands |

| Creator economy | $250B (SignalFire 2021) |

What is included in the product

Provides a concise SWOT analysis of The Arena Group, highlighting internal capabilities and operational weaknesses, market opportunities in digital publishing and content monetization, and external threats from competition, platform changes, and advertising volatility.

Provides a focused SWOT matrix tailored to The Arena Group for rapid strategic alignment and stakeholder briefings; editable format enables quick updates to reflect evolving digital media priorities.

Weaknesses

Ad market sensitivity

Heavy reliance on digital advertising makes Arena Group revenue cyclical and volatile, with advertiser budget shifts translating quickly into quarterly swings. CPM compression and shifting demand have pressured margins, mirroring industry trends where programmatic now handles over 70% of display buying and drove mid-single-digit CPM declines in 2024. Dependence on programmatic reduces pricing control and magnifies the impact of advertiser pullbacks on results.

Brand stewardship risk

Managing legacy brands like Sports Illustrated and Parade requires continuous investment to maintain quality and relevance, with content and licensing spend driving operating costs. Missteps in editorial standards or licensing can rapidly erode trust, and with over 5 billion social media users in 2024, audience backlash spreads quickly. Rebuilding damaged brand equity is costly and often takes years and millions in remediation and marketing spend. Brand stewardship risk therefore represents a material operational vulnerability.

Platform dependence

The Arena Group’s reliance on search and social algorithms leaves site traffic vulnerable to exogenous shocks; Google controls ~92% of global search (StatCounter 2025) and Meta’s family reaches ~3.0B monthly users (Meta 2024), so algorithm or iOS privacy changes can sharply reduce reach. Limited bargaining power with these gatekeepers constrains growth, requiring sustained investment in direct channels and first-party data.

Subscription scale constraints

Converting large casual audiences into paying users is difficult—industry conversion for digital publishers was about 1–3% in 2024, constraining Arena Group’s subscription scale. Paywall strategy must balance reach with monetization, since aggressive metering can erode ad-driven reach. Media subscription churn averaged ~20–35% in 2024, requiring continual product upgrades and exclusive content to preserve LTV versus rising CAC.

- Conversion rate: 1–3% (2024 industry)

- Churn: ~20–35% (2024)

- CAC pressure vs LTV: high CAC dilutes unit economics

Operational complexity

Operational complexity: Multi-brand, multi-vertical operations raise coordination costs as creators, sales, and tech roadmaps demand intensive cross-functional alignment; fragmented content calendars hinder accurate inventory forecasting and slow monetization cycles; legal and licensing across properties increase compliance overhead and risk exposure.

- Coordination costs

- Roadmap integration strain

- Forecasting fragmentation

- Elevated legal/licensing burden

Programmatic >70%, paywall conversion 1-3% drive revenue volatility

Heavy ad reliance and programmatic pricing pressure (programmatic >70%; mid-single-digit CPM decline in 2024) create revenue volatility. Brand stewardship of legacy titles raises ongoing content and licensing costs and reputational risk. Platform dependence (Google ~92% search; Meta ~3.0B monthly) and low subscription conversion (1–3%) with churn (20–35%) constrain scalable monetization.

| Metric | Value |

|---|---|

| Programmatic share | >70% |

| CPM trend 2024 | mid-single-digit decline |

| Google search share | ~92% (2025) |

| Meta reach | ~3.0B monthly (2024) |

| Subscription conv | 1–3% (2024) |

| Churn | 20–35% (2024) |

Full Version Awaits

The Arena Group SWOT Analysis

This is the actual The Arena Group SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and insights. Purchase unlocks the complete, editable version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

The Arena Group SWOT Analysis highlights content strengths, monetization opportunities, and competitive risks while identifying strategic growth drivers across digital media. Want the full story? Purchase the complete SWOT for a research-backed, editable Word report plus Excel matrix—ideal for investors, strategists, and advisors.

Strengths

Iconic brand portfolio

Ownership of Sports Illustrated (founded 1954), TheStreet (1996) and Parade (1941) gives The Arena Group strong brand equity and built-in audiences. These legacy titles enhance advertiser trust and support higher CPMs across sports, finance and lifestyle verticals. Cross-promotion among properties amplifies reach and customer lifetime value. Heritage credibility helps secure partnerships and premium content access.

Scalable tech platform

Centralized publishing, analytics, and monetization tools at The Arena Group streamline workflows to speed time-to-market and maintain consistent quality across brands; the company owns Sports Illustrated among its flagship properties. Shared technology lowers marginal content costs and standardizes best practices, while data-driven optimization has improved engagement and ad yield across its network. Platform scale enables rapid onboarding of new creators and properties, supporting portfolio expansion.

Diversified revenue mix

Digital advertising remains core but Arena Group supplements it with subscriptions and memberships across over 35 digital brands, reducing single-stream dependency. Multiple verticals such as sports, automotive and finance help offset cyclical ad softness with recurring subscription revenue. Branded content and sponsorships provide higher-margin revenue lines, while subscription data strengthens first-party audience profiles for improved monetization.

Creator-centric model

Audience scale and engagement

The Arena Group leverages flagship brands such as Sports Illustrated and TheStreet to span sports, finance and lifestyle, reaching diverse demographics with both evergreen and event-driven content tied to seasons, earnings cycles and awards calendars. Strong SEO from long-form journalism and branded franchises drives sustained organic discovery, while social distribution amplifies reach and lowers acquisition cost per user.

- Brand portfolio: Sports Illustrated, TheStreet, Parade

- Content mix: evergreen + event-driven

- Channels: SEO-led organic discovery + social amplification

Legacy titles and creator-driven scale: 35+ brands, $250B creator economy

The Arena Group owns flagship titles (Sports Illustrated 1954, TheStreet 1996, Parade 1941), delivering strong brand equity, higher CPMs and advertiser trust. Centralized platform and 35+ digital brands cut marginal costs and boost SEO-driven reach. Creator-centric model taps the $250B creator economy to scale content velocity and subscription diversification.

| Metric | Value |

|---|---|

| Flagship brands | Sports Illustrated, TheStreet, Parade |

| Brand count | 35+ digital brands |

| Creator economy | $250B (SignalFire 2021) |

What is included in the product

Provides a concise SWOT analysis of The Arena Group, highlighting internal capabilities and operational weaknesses, market opportunities in digital publishing and content monetization, and external threats from competition, platform changes, and advertising volatility.

Provides a focused SWOT matrix tailored to The Arena Group for rapid strategic alignment and stakeholder briefings; editable format enables quick updates to reflect evolving digital media priorities.

Weaknesses

Ad market sensitivity

Heavy reliance on digital advertising makes Arena Group revenue cyclical and volatile, with advertiser budget shifts translating quickly into quarterly swings. CPM compression and shifting demand have pressured margins, mirroring industry trends where programmatic now handles over 70% of display buying and drove mid-single-digit CPM declines in 2024. Dependence on programmatic reduces pricing control and magnifies the impact of advertiser pullbacks on results.

Brand stewardship risk

Managing legacy brands like Sports Illustrated and Parade requires continuous investment to maintain quality and relevance, with content and licensing spend driving operating costs. Missteps in editorial standards or licensing can rapidly erode trust, and with over 5 billion social media users in 2024, audience backlash spreads quickly. Rebuilding damaged brand equity is costly and often takes years and millions in remediation and marketing spend. Brand stewardship risk therefore represents a material operational vulnerability.

Platform dependence

The Arena Group’s reliance on search and social algorithms leaves site traffic vulnerable to exogenous shocks; Google controls ~92% of global search (StatCounter 2025) and Meta’s family reaches ~3.0B monthly users (Meta 2024), so algorithm or iOS privacy changes can sharply reduce reach. Limited bargaining power with these gatekeepers constrains growth, requiring sustained investment in direct channels and first-party data.

Subscription scale constraints

Converting large casual audiences into paying users is difficult—industry conversion for digital publishers was about 1–3% in 2024, constraining Arena Group’s subscription scale. Paywall strategy must balance reach with monetization, since aggressive metering can erode ad-driven reach. Media subscription churn averaged ~20–35% in 2024, requiring continual product upgrades and exclusive content to preserve LTV versus rising CAC.

- Conversion rate: 1–3% (2024 industry)

- Churn: ~20–35% (2024)

- CAC pressure vs LTV: high CAC dilutes unit economics

Operational complexity

Operational complexity: Multi-brand, multi-vertical operations raise coordination costs as creators, sales, and tech roadmaps demand intensive cross-functional alignment; fragmented content calendars hinder accurate inventory forecasting and slow monetization cycles; legal and licensing across properties increase compliance overhead and risk exposure.

- Coordination costs

- Roadmap integration strain

- Forecasting fragmentation

- Elevated legal/licensing burden

Programmatic >70%, paywall conversion 1-3% drive revenue volatility

Heavy ad reliance and programmatic pricing pressure (programmatic >70%; mid-single-digit CPM decline in 2024) create revenue volatility. Brand stewardship of legacy titles raises ongoing content and licensing costs and reputational risk. Platform dependence (Google ~92% search; Meta ~3.0B monthly) and low subscription conversion (1–3%) with churn (20–35%) constrain scalable monetization.

| Metric | Value |

|---|---|

| Programmatic share | >70% |

| CPM trend 2024 | mid-single-digit decline |

| Google search share | ~92% (2025) |

| Meta reach | ~3.0B monthly (2024) |

| Subscription conv | 1–3% (2024) |

| Churn | 20–35% (2024) |

Full Version Awaits

The Arena Group SWOT Analysis

This is the actual The Arena Group SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and insights. Purchase unlocks the complete, editable version immediately after checkout.