Hackett Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

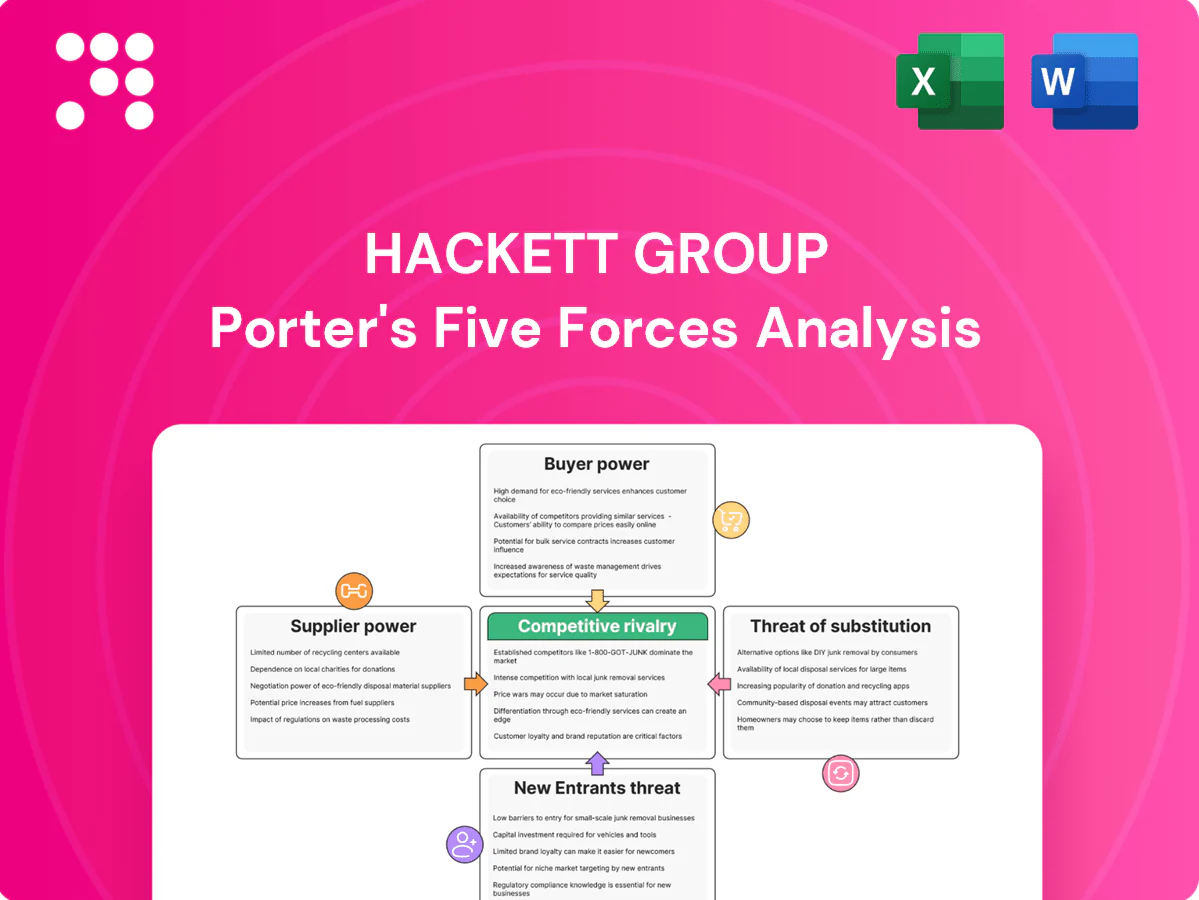

Hackett Group faces moderate buyer power and tech-driven substitution risks, while its niche advisory expertise and client relationships mitigate new-entrant threats; supplier influence and industry rivalry shape margin pressure. This snapshot highlights key dynamics but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore Hackett Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized data and benchmark providers

Benchmark datasets and industry taxonomies remain concentrated among a few specialized providers in 2024, giving those vendors notable negotiating leverage over clients like Hackett Group. Proprietary indices and longitudinal datasets are difficult to replace without degrading quality or comparability. Multi-year licenses and strict usage terms materially raise effective switching costs. Diversifying supplier sources and developing in-house benchmarks can partially offset that supplier power.

Cloud, analytics, and software platforms

Dependence on hyperscalers concentrates supplier power—AWS (32%), Azure (23%) and GCP (11%) hold roughly 66% of cloud market share in 2024, exposing Hackett Group margins to pricing and bundling shifts. Technical lock-in and integration complexity raise switching costs and migration risk. Volume commitments and partner tiers can secure discounts (up to ~60%) but add contractual obligations. Rising multi-cloud/open architecture adoption (87% of enterprises in 2024) is gradually eroding supplier leverage.

Expert human capital and niche contractors

Senior domain experts and scarce analytics talent act as critical suppliers to Hackett Group, commanding high wage bargaining power—US median data scientist pay rose to about $120,000 in 2024, tightening budgets. Certification and niche skills magnify pressure amid low unemployment in tech. Reliance on key individuals raises knowledge-transfer risk. Talent pipelines, internal academies and offshore delivery centers are used to balance cost and availability.

Research partners and academic alliances

Research partners and academic alliances lend methodological credibility and co-branded studies to Hackett Group, and a small set of reputable institutions often becomes the default source for validation, giving those partners leverage over project timelines and intellectual property terms.

- Limited substitutes increase supplier power

- Co-authorship and data-sharing can restrict commercialization

- IP and timeline influence raises operational risk

- Broadening partnerships mitigates concentration risk

Third-party data privacy, compliance, and tooling

Third-party privacy and regtech vendors dictate delivery feasibility in regulated sectors; the RegTech market was estimated at about $9B in 2024, increasing vendor leverage. Certification maintenance (SOC, ISO) aligns Hackett to vendors' annual audit cycles, so vendor price or scope hikes directly inflate project costs. Expanding internal compliance reduces this external dependency and cost volatility.

- Vendor leverage: regtech ~$9B (2024)

- Audit cycles: annual SOC/ISO tie-ins

- Mitigation: build internal compliance

Cloud concentration 32%/23%/11% and $9B regtech raise supplier leverage, boosting switching costs

Specialized data providers, hyperscalers and niche talent give suppliers high leverage, raising switching costs and margin risk. Cloud concentration (AWS 32%, Azure 23%, GCP 11%) and regtech market ~$9B (2024) amplify pricing exposure. Internal benchmarks, multi-cloud and talent development reduce dependency.

| Supplier | Metric |

|---|---|

| Cloud | AWS32%/Azure23%/GCP11% |

| RegTech | $9B (2024) |

| Talent | Data scientist median $120k (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Hackett Group that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, profitability and defensive positioning.

A concise, one-sheet Hackett Group Porter's Five Forces toolkit that instantly visualizes competitive pressure with a spider chart, lets you swap in your own data or scenarios without macros, and slots seamlessly into decks or Excel dashboards for faster, board-ready strategic decisions.

Customers Bargaining Power

Large enterprise and Fortune 1000 clients

Large enterprise and Fortune 1000 clients, numbering 1000 firms, are concentrated, sophisticated buyers with sizable budgets who exert strong price pressure. They routinely demand customized scope, outcome guarantees, and executive access while using referenceability and brand benefits to extract discounts. Multi-year programs reduce churn but extend negotiation cycles and procurement timelines.

RFP-driven procurement and benchmarking comparability

Formal RFPs standardize evaluation criteria, enabling apples-to-apples price comparison and driving reported price compression of roughly 8–14% in benchmarked deals in 2024. Benchmarking outputs are treated as comparable across vendors, heightening buyer leverage and accelerating award-to-negotiation cycles. Procurement frequently mandates rate cards, fee caps, and IP terms—present in about two-thirds of enterprise RFPs. Differentiated insights and speed-to-value remain the primary defenses against pure price competition.

Multi-sourcing and vendor consolidation cycles

Clients commonly split work among global firms, boutiques and internal teams—2024 Hackett Group benchmarking shows most buyers use three provider types, using competition to extract concessions. In downturns consolidation intensifies fee pressure, with benchmarked fee compression around 12% in 2024. Preferred vendor lists gate access and compress margins, while strong account management and cross-sell broaden wallet share and reduce dependency.

Switching costs tied to embedded taxonomies

Embedded Hackett taxonomies raise change costs as governance, KPIs and historical comparatives create inertia; buyers often phase transitions by parallel-running alternate frameworks, while data portability and API access become pivotal negotiation points—Postman 2024 reports 78% of enterprises prioritize API access in vendor deals.

- Embedded governance increases lock-in

- Historical KPIs deter full switch

- Parallel runs enable phased exit

- API/data portability = primary leverage

Outcome-based and risk-sharing contracts

Buyers increasingly demand value-linked fees and SLAs that shift downside to providers, raising pricing pressure while rewarding Hackett for differentiated IP that delivers measurable impact; Hackett reported in 2024 that outcome-linked engagements comprised about 28% of advisory contracts, lifting average contract value by 12% for measurable-win deals.

- Clear baselines and attribution models are decisive

- Robust measurement analytics can tilt power back to Hackett

- Outcome deals increase vendor risk but raise premium for proven impact

8–14% cuts; 78% API; 28% outcome deals

Large, sophisticated enterprise buyers drive strong price pressure, using RFPs and benchmarking to extract 8–14% price compression in 2024 and mandate rate cards/IP terms. Buyers split work across providers and in downturns push ~12% fee compression; preferred-vendor lists and procurement elongate cycles. API/data portability (78% priority) and outcome-linked fees (28% of deals) shift risk to providers but raise CV by ~12% for measurable wins.

| Metric | 2024 | Implication |

|---|---|---|

| Price compression | 8–14% | Higher buyer leverage |

| Fee compression (downturns) | ~12% | Margin pressure |

| Outcome-linked deals | 28% | Risk shift to vendor |

| API priority | 78% | Negotiation focus |

| Avg CV uplift (wins) | +12% | Premium for measurable impact |

Preview Before You Purchase

Hackett Group Porter's Five Forces Analysis

This preview shows the exact Hackett Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re previewing the final deliverable; once your purchase is complete you’ll get instant access to this same file.

Don't Miss the Bigger Picture

Hackett Group faces moderate buyer power and tech-driven substitution risks, while its niche advisory expertise and client relationships mitigate new-entrant threats; supplier influence and industry rivalry shape margin pressure. This snapshot highlights key dynamics but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore Hackett Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized data and benchmark providers

Benchmark datasets and industry taxonomies remain concentrated among a few specialized providers in 2024, giving those vendors notable negotiating leverage over clients like Hackett Group. Proprietary indices and longitudinal datasets are difficult to replace without degrading quality or comparability. Multi-year licenses and strict usage terms materially raise effective switching costs. Diversifying supplier sources and developing in-house benchmarks can partially offset that supplier power.

Cloud, analytics, and software platforms

Dependence on hyperscalers concentrates supplier power—AWS (32%), Azure (23%) and GCP (11%) hold roughly 66% of cloud market share in 2024, exposing Hackett Group margins to pricing and bundling shifts. Technical lock-in and integration complexity raise switching costs and migration risk. Volume commitments and partner tiers can secure discounts (up to ~60%) but add contractual obligations. Rising multi-cloud/open architecture adoption (87% of enterprises in 2024) is gradually eroding supplier leverage.

Expert human capital and niche contractors

Senior domain experts and scarce analytics talent act as critical suppliers to Hackett Group, commanding high wage bargaining power—US median data scientist pay rose to about $120,000 in 2024, tightening budgets. Certification and niche skills magnify pressure amid low unemployment in tech. Reliance on key individuals raises knowledge-transfer risk. Talent pipelines, internal academies and offshore delivery centers are used to balance cost and availability.

Research partners and academic alliances

Research partners and academic alliances lend methodological credibility and co-branded studies to Hackett Group, and a small set of reputable institutions often becomes the default source for validation, giving those partners leverage over project timelines and intellectual property terms.

- Limited substitutes increase supplier power

- Co-authorship and data-sharing can restrict commercialization

- IP and timeline influence raises operational risk

- Broadening partnerships mitigates concentration risk

Third-party data privacy, compliance, and tooling

Third-party privacy and regtech vendors dictate delivery feasibility in regulated sectors; the RegTech market was estimated at about $9B in 2024, increasing vendor leverage. Certification maintenance (SOC, ISO) aligns Hackett to vendors' annual audit cycles, so vendor price or scope hikes directly inflate project costs. Expanding internal compliance reduces this external dependency and cost volatility.

- Vendor leverage: regtech ~$9B (2024)

- Audit cycles: annual SOC/ISO tie-ins

- Mitigation: build internal compliance

Cloud concentration 32%/23%/11% and $9B regtech raise supplier leverage, boosting switching costs

Specialized data providers, hyperscalers and niche talent give suppliers high leverage, raising switching costs and margin risk. Cloud concentration (AWS 32%, Azure 23%, GCP 11%) and regtech market ~$9B (2024) amplify pricing exposure. Internal benchmarks, multi-cloud and talent development reduce dependency.

| Supplier | Metric |

|---|---|

| Cloud | AWS32%/Azure23%/GCP11% |

| RegTech | $9B (2024) |

| Talent | Data scientist median $120k (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Hackett Group that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, profitability and defensive positioning.

A concise, one-sheet Hackett Group Porter's Five Forces toolkit that instantly visualizes competitive pressure with a spider chart, lets you swap in your own data or scenarios without macros, and slots seamlessly into decks or Excel dashboards for faster, board-ready strategic decisions.

Customers Bargaining Power

Large enterprise and Fortune 1000 clients

Large enterprise and Fortune 1000 clients, numbering 1000 firms, are concentrated, sophisticated buyers with sizable budgets who exert strong price pressure. They routinely demand customized scope, outcome guarantees, and executive access while using referenceability and brand benefits to extract discounts. Multi-year programs reduce churn but extend negotiation cycles and procurement timelines.

RFP-driven procurement and benchmarking comparability

Formal RFPs standardize evaluation criteria, enabling apples-to-apples price comparison and driving reported price compression of roughly 8–14% in benchmarked deals in 2024. Benchmarking outputs are treated as comparable across vendors, heightening buyer leverage and accelerating award-to-negotiation cycles. Procurement frequently mandates rate cards, fee caps, and IP terms—present in about two-thirds of enterprise RFPs. Differentiated insights and speed-to-value remain the primary defenses against pure price competition.

Multi-sourcing and vendor consolidation cycles

Clients commonly split work among global firms, boutiques and internal teams—2024 Hackett Group benchmarking shows most buyers use three provider types, using competition to extract concessions. In downturns consolidation intensifies fee pressure, with benchmarked fee compression around 12% in 2024. Preferred vendor lists gate access and compress margins, while strong account management and cross-sell broaden wallet share and reduce dependency.

Switching costs tied to embedded taxonomies

Embedded Hackett taxonomies raise change costs as governance, KPIs and historical comparatives create inertia; buyers often phase transitions by parallel-running alternate frameworks, while data portability and API access become pivotal negotiation points—Postman 2024 reports 78% of enterprises prioritize API access in vendor deals.

- Embedded governance increases lock-in

- Historical KPIs deter full switch

- Parallel runs enable phased exit

- API/data portability = primary leverage

Outcome-based and risk-sharing contracts

Buyers increasingly demand value-linked fees and SLAs that shift downside to providers, raising pricing pressure while rewarding Hackett for differentiated IP that delivers measurable impact; Hackett reported in 2024 that outcome-linked engagements comprised about 28% of advisory contracts, lifting average contract value by 12% for measurable-win deals.

- Clear baselines and attribution models are decisive

- Robust measurement analytics can tilt power back to Hackett

- Outcome deals increase vendor risk but raise premium for proven impact

8–14% cuts; 78% API; 28% outcome deals

Large, sophisticated enterprise buyers drive strong price pressure, using RFPs and benchmarking to extract 8–14% price compression in 2024 and mandate rate cards/IP terms. Buyers split work across providers and in downturns push ~12% fee compression; preferred-vendor lists and procurement elongate cycles. API/data portability (78% priority) and outcome-linked fees (28% of deals) shift risk to providers but raise CV by ~12% for measurable wins.

| Metric | 2024 | Implication |

|---|---|---|

| Price compression | 8–14% | Higher buyer leverage |

| Fee compression (downturns) | ~12% | Margin pressure |

| Outcome-linked deals | 28% | Risk shift to vendor |

| API priority | 78% | Negotiation focus |

| Avg CV uplift (wins) | +12% | Premium for measurable impact |

Preview Before You Purchase

Hackett Group Porter's Five Forces Analysis

This preview shows the exact Hackett Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re previewing the final deliverable; once your purchase is complete you’ll get instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Hackett Group faces moderate buyer power and tech-driven substitution risks, while its niche advisory expertise and client relationships mitigate new-entrant threats; supplier influence and industry rivalry shape margin pressure. This snapshot highlights key dynamics but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore Hackett Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized data and benchmark providers

Benchmark datasets and industry taxonomies remain concentrated among a few specialized providers in 2024, giving those vendors notable negotiating leverage over clients like Hackett Group. Proprietary indices and longitudinal datasets are difficult to replace without degrading quality or comparability. Multi-year licenses and strict usage terms materially raise effective switching costs. Diversifying supplier sources and developing in-house benchmarks can partially offset that supplier power.

Cloud, analytics, and software platforms

Dependence on hyperscalers concentrates supplier power—AWS (32%), Azure (23%) and GCP (11%) hold roughly 66% of cloud market share in 2024, exposing Hackett Group margins to pricing and bundling shifts. Technical lock-in and integration complexity raise switching costs and migration risk. Volume commitments and partner tiers can secure discounts (up to ~60%) but add contractual obligations. Rising multi-cloud/open architecture adoption (87% of enterprises in 2024) is gradually eroding supplier leverage.

Expert human capital and niche contractors

Senior domain experts and scarce analytics talent act as critical suppliers to Hackett Group, commanding high wage bargaining power—US median data scientist pay rose to about $120,000 in 2024, tightening budgets. Certification and niche skills magnify pressure amid low unemployment in tech. Reliance on key individuals raises knowledge-transfer risk. Talent pipelines, internal academies and offshore delivery centers are used to balance cost and availability.

Research partners and academic alliances

Research partners and academic alliances lend methodological credibility and co-branded studies to Hackett Group, and a small set of reputable institutions often becomes the default source for validation, giving those partners leverage over project timelines and intellectual property terms.

- Limited substitutes increase supplier power

- Co-authorship and data-sharing can restrict commercialization

- IP and timeline influence raises operational risk

- Broadening partnerships mitigates concentration risk

Third-party data privacy, compliance, and tooling

Third-party privacy and regtech vendors dictate delivery feasibility in regulated sectors; the RegTech market was estimated at about $9B in 2024, increasing vendor leverage. Certification maintenance (SOC, ISO) aligns Hackett to vendors' annual audit cycles, so vendor price or scope hikes directly inflate project costs. Expanding internal compliance reduces this external dependency and cost volatility.

- Vendor leverage: regtech ~$9B (2024)

- Audit cycles: annual SOC/ISO tie-ins

- Mitigation: build internal compliance

Cloud concentration 32%/23%/11% and $9B regtech raise supplier leverage, boosting switching costs

Specialized data providers, hyperscalers and niche talent give suppliers high leverage, raising switching costs and margin risk. Cloud concentration (AWS 32%, Azure 23%, GCP 11%) and regtech market ~$9B (2024) amplify pricing exposure. Internal benchmarks, multi-cloud and talent development reduce dependency.

| Supplier | Metric |

|---|---|

| Cloud | AWS32%/Azure23%/GCP11% |

| RegTech | $9B (2024) |

| Talent | Data scientist median $120k (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Hackett Group that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, profitability and defensive positioning.

A concise, one-sheet Hackett Group Porter's Five Forces toolkit that instantly visualizes competitive pressure with a spider chart, lets you swap in your own data or scenarios without macros, and slots seamlessly into decks or Excel dashboards for faster, board-ready strategic decisions.

Customers Bargaining Power

Large enterprise and Fortune 1000 clients

Large enterprise and Fortune 1000 clients, numbering 1000 firms, are concentrated, sophisticated buyers with sizable budgets who exert strong price pressure. They routinely demand customized scope, outcome guarantees, and executive access while using referenceability and brand benefits to extract discounts. Multi-year programs reduce churn but extend negotiation cycles and procurement timelines.

RFP-driven procurement and benchmarking comparability

Formal RFPs standardize evaluation criteria, enabling apples-to-apples price comparison and driving reported price compression of roughly 8–14% in benchmarked deals in 2024. Benchmarking outputs are treated as comparable across vendors, heightening buyer leverage and accelerating award-to-negotiation cycles. Procurement frequently mandates rate cards, fee caps, and IP terms—present in about two-thirds of enterprise RFPs. Differentiated insights and speed-to-value remain the primary defenses against pure price competition.

Multi-sourcing and vendor consolidation cycles

Clients commonly split work among global firms, boutiques and internal teams—2024 Hackett Group benchmarking shows most buyers use three provider types, using competition to extract concessions. In downturns consolidation intensifies fee pressure, with benchmarked fee compression around 12% in 2024. Preferred vendor lists gate access and compress margins, while strong account management and cross-sell broaden wallet share and reduce dependency.

Switching costs tied to embedded taxonomies

Embedded Hackett taxonomies raise change costs as governance, KPIs and historical comparatives create inertia; buyers often phase transitions by parallel-running alternate frameworks, while data portability and API access become pivotal negotiation points—Postman 2024 reports 78% of enterprises prioritize API access in vendor deals.

- Embedded governance increases lock-in

- Historical KPIs deter full switch

- Parallel runs enable phased exit

- API/data portability = primary leverage

Outcome-based and risk-sharing contracts

Buyers increasingly demand value-linked fees and SLAs that shift downside to providers, raising pricing pressure while rewarding Hackett for differentiated IP that delivers measurable impact; Hackett reported in 2024 that outcome-linked engagements comprised about 28% of advisory contracts, lifting average contract value by 12% for measurable-win deals.

- Clear baselines and attribution models are decisive

- Robust measurement analytics can tilt power back to Hackett

- Outcome deals increase vendor risk but raise premium for proven impact

8–14% cuts; 78% API; 28% outcome deals

Large, sophisticated enterprise buyers drive strong price pressure, using RFPs and benchmarking to extract 8–14% price compression in 2024 and mandate rate cards/IP terms. Buyers split work across providers and in downturns push ~12% fee compression; preferred-vendor lists and procurement elongate cycles. API/data portability (78% priority) and outcome-linked fees (28% of deals) shift risk to providers but raise CV by ~12% for measurable wins.

| Metric | 2024 | Implication |

|---|---|---|

| Price compression | 8–14% | Higher buyer leverage |

| Fee compression (downturns) | ~12% | Margin pressure |

| Outcome-linked deals | 28% | Risk shift to vendor |

| API priority | 78% | Negotiation focus |

| Avg CV uplift (wins) | +12% | Premium for measurable impact |

Preview Before You Purchase

Hackett Group Porter's Five Forces Analysis

This preview shows the exact Hackett Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re previewing the final deliverable; once your purchase is complete you’ll get instant access to this same file.