The Learning Network Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

The Learning Network’s Porter's Five Forces snapshot highlights competitive intensity across buyers, suppliers, substitutes and entry threats, revealing where strategic pressure is greatest. This brief overview surfaces key risks and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to The Learning Network.

Suppliers Bargaining Power

Reliance on NYT newsroom

Journalists, photographers and editors at The New York Times—represented by a newsroom union of over 2,000 staff as of 2024—supply The Learning Network’s core content pipeline. Union rules, shift schedules and editorial priorities can constrain timing and classroom-ready formats, and NYT’s daily production of hundreds of articles sets the cadence for curriculum updates. Any disruption or policy shift at NYT would ripple into The Learning Network’s output, giving suppliers disproportionate leverage despite internal affiliation.

Licensing and media rights

Use of articles, images, videos and graphics requires clear rights management; specialty visuals and archival assets often carry premium licensing terms, and in 2024 these licensing constraints continued to drive higher content procurement costs for edu-tech platforms. Tight rights windows or reuse restrictions limit curricular reuse and derivative lesson design. Suppliers of third-party media can hold negotiating power on price and scope, forcing The Learning Network to allocate significant budget and legal resources to licensing.

Technology infrastructure vendors

Hosting, CMS, analytics and classroom integrations depend on external platforms, and the top three cloud providers held over 60% of the global cloud market in 2024, concentrating supplier influence. Changes in APIs, pricing or data policies can raise costs or degrade UX. Vendor switching is feasible but migration of integrations and data is resource-intensive, giving key tech suppliers moderate leverage.

Assessment and standards mappings

Curriculum alignment to frameworks like Common Core (adopted originally by 41 states plus DC) often relies on external consultants and mapping tools, creating supplier dependence. Frequent updates to standards force costly rework and re-tagging of content, increasing maintenance overhead for The Learning Network. A small pool of specialist suppliers concentrates expertise and can drive up prices, while perceived alignment credibility directly affects educator adoption and sales.

- Curriculum reliance: external consultants

- Standards updates: rework/tagging costs

- Supplier concentration: higher pricing risk

- Credibility: crucial for educator adoption

Freelancers and educational designers

Freelancers and pedagogy experts convert journalism into classroom-ready lessons, providing structure, learning objectives and assessment alignment. High-quality specialists are scarce and often command premium fees (commonly cited ranges in 2024: 60–150 USD/hr), and turnover disrupts cadence and consistency. Their bargaining power spikes during major news cycles when demand can double.

- Role: lesson writers, pedagogy experts

- Cost 2024: 60–150 USD/hr

- Risk: turnover → inconsistent releases

- Power: rises sharply during demand spikes

Unionized newsroom (2,000+) and top clouds (60%+) drive supplier leverage

NYT newsroom union (over 2,000 staff in 2024) and editorial schedules constrain The Learning Network’s cadence and give suppliers leverage. Licensing and archival fees rose in 2024, limiting reuse and raising procurement costs. Top three cloud providers held >60% market share in 2024, concentrating tech supplier power; freelancers charged 60–150 USD/hr, spiking during major news cycles.

| Supplier | 2024 stat | Impact |

|---|---|---|

| NYT newsroom | >2,000 union staff | Scheduling/editorial constraints |

| Licensing | Rising fees 2024 | Higher procurement costs |

| Cloud providers | Top3 >60% market share | Concentrated tech leverage |

| Freelancers | 60–150 USD/hr | Cost spikes, turnover risk |

What is included in the product

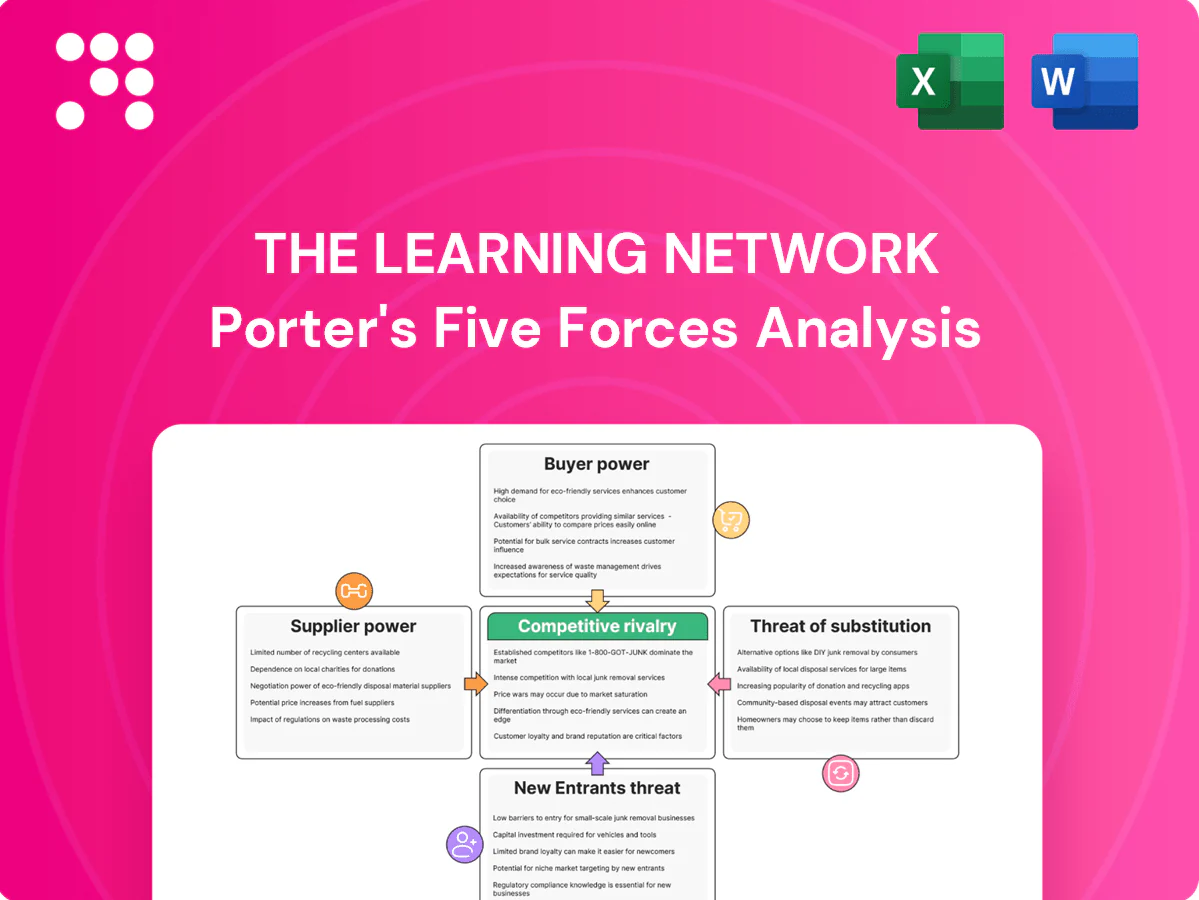

Analyzes competitive intensity, buyer and supplier power, threat of new entrants and substitutes for The Learning Network, highlighting disruptive technologies, content substitutes, and market entry barriers while outlining strategic implications for pricing, content differentiation, and scale to protect and grow market share.

A concise, one-sheet Porter's Five Forces for The Learning Network that visualizes competitive pressure with an interactive spider chart, lets you customize force intensities and notes without macros, and slips directly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Educators have low switching costs

Teachers can switch to OER, district-provided materials, or competitors with minimal friction, and in 2024 about 88% of US teachers reported using an LMS or digital platform facilitating quick substitution. Bookmarking and LMS links make replacing resources a single-click action, raising price sensitivity and feature expectations. Retention therefore depends on delivering consistent measurable time savings and recurring classroom value.

Districts and admins control budgets

Districts and admins, controlling roughly $824 billion in U.S. K–12 annual spending and serving about 50 million students, negotiate volume access, data safeguards, and integrations to meet scale needs. Centralized procurement consortia routinely extract discounts and pilot terms from vendors. FERPA, COPPA and accessibility obligations become explicit contractual negotiation points. This concentrates buyer power in larger deals.

Global and subject diversity

Needs vary across grade, literacy and subject lines, fragmenting demand and forcing The Learning Network to support differentiated paths; in 2024 the global edtech market was estimated at about $252 billion, amplifying buyer leverage. Gaps in ESL, SPED and assessment features enable districts and large buyers to demand roadmap changes and custom SLAs. Fragmentation raises the effective bargaining power of niche segments that command specialized procurement budgets.

Outcomes and accountability focus

- Outcome-driven buying: ~72% 2024

- Assessment efficiency required

- Impact data = pricing leverage

- Proven gains = stronger negotiation

Community influence and virality

Teacher communities and social channels quickly amplify preferences; positive word-of-mouth lowers acquisition costs while negative feedback forces concessions. Contests and prompts must stay engaging to maintain advocacy, since community sentiment directly translates into buyer leverage. In 2024 global social media users reached 5.07 billion (DataReportal), expanding reach for teacher-led influence.

- Community amplification: rapid spread of preferences

- Cost impact: earned advocacy cuts CAC

- Risk: negative feedback increases concessions

- Engagement: contests must evolve to sustain advocacy

Customers wield power: 88% LMS, $824B K-12, 72% outcome buyers, 5.07B social

Customers hold strong leverage: teachers can switch easily (88% use LMS in 2024), districts centralize purchasing (US K–12 spend ~$824B) and prioritize outcomes (~72% outcome-driven buyers), while community sentiment and 5.07B global social users amplify demands for proof and price concessions.

| Tag | Metric | Value |

|---|---|---|

| Teachers LMS | Adoption (2024) | 88% |

| District Spend | US K–12 annual | $824B |

| Outcome-driven | Buyers (2024) | 72% |

| Social Reach | Global users (2024) | 5.07B |

Full Version Awaits

The Learning Network Porter's Five Forces Analysis

This preview shows the exact The Learning Network Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders or mockups; the file here is the final deliverable. Use it instantly for strategic insights and competitive assessment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

The Learning Network’s Porter's Five Forces snapshot highlights competitive intensity across buyers, suppliers, substitutes and entry threats, revealing where strategic pressure is greatest. This brief overview surfaces key risks and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to The Learning Network.

Suppliers Bargaining Power

Reliance on NYT newsroom

Journalists, photographers and editors at The New York Times—represented by a newsroom union of over 2,000 staff as of 2024—supply The Learning Network’s core content pipeline. Union rules, shift schedules and editorial priorities can constrain timing and classroom-ready formats, and NYT’s daily production of hundreds of articles sets the cadence for curriculum updates. Any disruption or policy shift at NYT would ripple into The Learning Network’s output, giving suppliers disproportionate leverage despite internal affiliation.

Licensing and media rights

Use of articles, images, videos and graphics requires clear rights management; specialty visuals and archival assets often carry premium licensing terms, and in 2024 these licensing constraints continued to drive higher content procurement costs for edu-tech platforms. Tight rights windows or reuse restrictions limit curricular reuse and derivative lesson design. Suppliers of third-party media can hold negotiating power on price and scope, forcing The Learning Network to allocate significant budget and legal resources to licensing.

Technology infrastructure vendors

Hosting, CMS, analytics and classroom integrations depend on external platforms, and the top three cloud providers held over 60% of the global cloud market in 2024, concentrating supplier influence. Changes in APIs, pricing or data policies can raise costs or degrade UX. Vendor switching is feasible but migration of integrations and data is resource-intensive, giving key tech suppliers moderate leverage.

Assessment and standards mappings

Curriculum alignment to frameworks like Common Core (adopted originally by 41 states plus DC) often relies on external consultants and mapping tools, creating supplier dependence. Frequent updates to standards force costly rework and re-tagging of content, increasing maintenance overhead for The Learning Network. A small pool of specialist suppliers concentrates expertise and can drive up prices, while perceived alignment credibility directly affects educator adoption and sales.

- Curriculum reliance: external consultants

- Standards updates: rework/tagging costs

- Supplier concentration: higher pricing risk

- Credibility: crucial for educator adoption

Freelancers and educational designers

Freelancers and pedagogy experts convert journalism into classroom-ready lessons, providing structure, learning objectives and assessment alignment. High-quality specialists are scarce and often command premium fees (commonly cited ranges in 2024: 60–150 USD/hr), and turnover disrupts cadence and consistency. Their bargaining power spikes during major news cycles when demand can double.

- Role: lesson writers, pedagogy experts

- Cost 2024: 60–150 USD/hr

- Risk: turnover → inconsistent releases

- Power: rises sharply during demand spikes

Unionized newsroom (2,000+) and top clouds (60%+) drive supplier leverage

NYT newsroom union (over 2,000 staff in 2024) and editorial schedules constrain The Learning Network’s cadence and give suppliers leverage. Licensing and archival fees rose in 2024, limiting reuse and raising procurement costs. Top three cloud providers held >60% market share in 2024, concentrating tech supplier power; freelancers charged 60–150 USD/hr, spiking during major news cycles.

| Supplier | 2024 stat | Impact |

|---|---|---|

| NYT newsroom | >2,000 union staff | Scheduling/editorial constraints |

| Licensing | Rising fees 2024 | Higher procurement costs |

| Cloud providers | Top3 >60% market share | Concentrated tech leverage |

| Freelancers | 60–150 USD/hr | Cost spikes, turnover risk |

What is included in the product

Analyzes competitive intensity, buyer and supplier power, threat of new entrants and substitutes for The Learning Network, highlighting disruptive technologies, content substitutes, and market entry barriers while outlining strategic implications for pricing, content differentiation, and scale to protect and grow market share.

A concise, one-sheet Porter's Five Forces for The Learning Network that visualizes competitive pressure with an interactive spider chart, lets you customize force intensities and notes without macros, and slips directly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Educators have low switching costs

Teachers can switch to OER, district-provided materials, or competitors with minimal friction, and in 2024 about 88% of US teachers reported using an LMS or digital platform facilitating quick substitution. Bookmarking and LMS links make replacing resources a single-click action, raising price sensitivity and feature expectations. Retention therefore depends on delivering consistent measurable time savings and recurring classroom value.

Districts and admins control budgets

Districts and admins, controlling roughly $824 billion in U.S. K–12 annual spending and serving about 50 million students, negotiate volume access, data safeguards, and integrations to meet scale needs. Centralized procurement consortia routinely extract discounts and pilot terms from vendors. FERPA, COPPA and accessibility obligations become explicit contractual negotiation points. This concentrates buyer power in larger deals.

Global and subject diversity

Needs vary across grade, literacy and subject lines, fragmenting demand and forcing The Learning Network to support differentiated paths; in 2024 the global edtech market was estimated at about $252 billion, amplifying buyer leverage. Gaps in ESL, SPED and assessment features enable districts and large buyers to demand roadmap changes and custom SLAs. Fragmentation raises the effective bargaining power of niche segments that command specialized procurement budgets.

Outcomes and accountability focus

- Outcome-driven buying: ~72% 2024

- Assessment efficiency required

- Impact data = pricing leverage

- Proven gains = stronger negotiation

Community influence and virality

Teacher communities and social channels quickly amplify preferences; positive word-of-mouth lowers acquisition costs while negative feedback forces concessions. Contests and prompts must stay engaging to maintain advocacy, since community sentiment directly translates into buyer leverage. In 2024 global social media users reached 5.07 billion (DataReportal), expanding reach for teacher-led influence.

- Community amplification: rapid spread of preferences

- Cost impact: earned advocacy cuts CAC

- Risk: negative feedback increases concessions

- Engagement: contests must evolve to sustain advocacy

Customers wield power: 88% LMS, $824B K-12, 72% outcome buyers, 5.07B social

Customers hold strong leverage: teachers can switch easily (88% use LMS in 2024), districts centralize purchasing (US K–12 spend ~$824B) and prioritize outcomes (~72% outcome-driven buyers), while community sentiment and 5.07B global social users amplify demands for proof and price concessions.

| Tag | Metric | Value |

|---|---|---|

| Teachers LMS | Adoption (2024) | 88% |

| District Spend | US K–12 annual | $824B |

| Outcome-driven | Buyers (2024) | 72% |

| Social Reach | Global users (2024) | 5.07B |

Full Version Awaits

The Learning Network Porter's Five Forces Analysis

This preview shows the exact The Learning Network Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders or mockups; the file here is the final deliverable. Use it instantly for strategic insights and competitive assessment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

The Learning Network’s Porter's Five Forces snapshot highlights competitive intensity across buyers, suppliers, substitutes and entry threats, revealing where strategic pressure is greatest. This brief overview surfaces key risks and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to The Learning Network.

Suppliers Bargaining Power

Reliance on NYT newsroom

Journalists, photographers and editors at The New York Times—represented by a newsroom union of over 2,000 staff as of 2024—supply The Learning Network’s core content pipeline. Union rules, shift schedules and editorial priorities can constrain timing and classroom-ready formats, and NYT’s daily production of hundreds of articles sets the cadence for curriculum updates. Any disruption or policy shift at NYT would ripple into The Learning Network’s output, giving suppliers disproportionate leverage despite internal affiliation.

Licensing and media rights

Use of articles, images, videos and graphics requires clear rights management; specialty visuals and archival assets often carry premium licensing terms, and in 2024 these licensing constraints continued to drive higher content procurement costs for edu-tech platforms. Tight rights windows or reuse restrictions limit curricular reuse and derivative lesson design. Suppliers of third-party media can hold negotiating power on price and scope, forcing The Learning Network to allocate significant budget and legal resources to licensing.

Technology infrastructure vendors

Hosting, CMS, analytics and classroom integrations depend on external platforms, and the top three cloud providers held over 60% of the global cloud market in 2024, concentrating supplier influence. Changes in APIs, pricing or data policies can raise costs or degrade UX. Vendor switching is feasible but migration of integrations and data is resource-intensive, giving key tech suppliers moderate leverage.

Assessment and standards mappings

Curriculum alignment to frameworks like Common Core (adopted originally by 41 states plus DC) often relies on external consultants and mapping tools, creating supplier dependence. Frequent updates to standards force costly rework and re-tagging of content, increasing maintenance overhead for The Learning Network. A small pool of specialist suppliers concentrates expertise and can drive up prices, while perceived alignment credibility directly affects educator adoption and sales.

- Curriculum reliance: external consultants

- Standards updates: rework/tagging costs

- Supplier concentration: higher pricing risk

- Credibility: crucial for educator adoption

Freelancers and educational designers

Freelancers and pedagogy experts convert journalism into classroom-ready lessons, providing structure, learning objectives and assessment alignment. High-quality specialists are scarce and often command premium fees (commonly cited ranges in 2024: 60–150 USD/hr), and turnover disrupts cadence and consistency. Their bargaining power spikes during major news cycles when demand can double.

- Role: lesson writers, pedagogy experts

- Cost 2024: 60–150 USD/hr

- Risk: turnover → inconsistent releases

- Power: rises sharply during demand spikes

Unionized newsroom (2,000+) and top clouds (60%+) drive supplier leverage

NYT newsroom union (over 2,000 staff in 2024) and editorial schedules constrain The Learning Network’s cadence and give suppliers leverage. Licensing and archival fees rose in 2024, limiting reuse and raising procurement costs. Top three cloud providers held >60% market share in 2024, concentrating tech supplier power; freelancers charged 60–150 USD/hr, spiking during major news cycles.

| Supplier | 2024 stat | Impact |

|---|---|---|

| NYT newsroom | >2,000 union staff | Scheduling/editorial constraints |

| Licensing | Rising fees 2024 | Higher procurement costs |

| Cloud providers | Top3 >60% market share | Concentrated tech leverage |

| Freelancers | 60–150 USD/hr | Cost spikes, turnover risk |

What is included in the product

Analyzes competitive intensity, buyer and supplier power, threat of new entrants and substitutes for The Learning Network, highlighting disruptive technologies, content substitutes, and market entry barriers while outlining strategic implications for pricing, content differentiation, and scale to protect and grow market share.

A concise, one-sheet Porter's Five Forces for The Learning Network that visualizes competitive pressure with an interactive spider chart, lets you customize force intensities and notes without macros, and slips directly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Educators have low switching costs

Teachers can switch to OER, district-provided materials, or competitors with minimal friction, and in 2024 about 88% of US teachers reported using an LMS or digital platform facilitating quick substitution. Bookmarking and LMS links make replacing resources a single-click action, raising price sensitivity and feature expectations. Retention therefore depends on delivering consistent measurable time savings and recurring classroom value.

Districts and admins control budgets

Districts and admins, controlling roughly $824 billion in U.S. K–12 annual spending and serving about 50 million students, negotiate volume access, data safeguards, and integrations to meet scale needs. Centralized procurement consortia routinely extract discounts and pilot terms from vendors. FERPA, COPPA and accessibility obligations become explicit contractual negotiation points. This concentrates buyer power in larger deals.

Global and subject diversity

Needs vary across grade, literacy and subject lines, fragmenting demand and forcing The Learning Network to support differentiated paths; in 2024 the global edtech market was estimated at about $252 billion, amplifying buyer leverage. Gaps in ESL, SPED and assessment features enable districts and large buyers to demand roadmap changes and custom SLAs. Fragmentation raises the effective bargaining power of niche segments that command specialized procurement budgets.

Outcomes and accountability focus

- Outcome-driven buying: ~72% 2024

- Assessment efficiency required

- Impact data = pricing leverage

- Proven gains = stronger negotiation

Community influence and virality

Teacher communities and social channels quickly amplify preferences; positive word-of-mouth lowers acquisition costs while negative feedback forces concessions. Contests and prompts must stay engaging to maintain advocacy, since community sentiment directly translates into buyer leverage. In 2024 global social media users reached 5.07 billion (DataReportal), expanding reach for teacher-led influence.

- Community amplification: rapid spread of preferences

- Cost impact: earned advocacy cuts CAC

- Risk: negative feedback increases concessions

- Engagement: contests must evolve to sustain advocacy

Customers wield power: 88% LMS, $824B K-12, 72% outcome buyers, 5.07B social

Customers hold strong leverage: teachers can switch easily (88% use LMS in 2024), districts centralize purchasing (US K–12 spend ~$824B) and prioritize outcomes (~72% outcome-driven buyers), while community sentiment and 5.07B global social users amplify demands for proof and price concessions.

| Tag | Metric | Value |

|---|---|---|

| Teachers LMS | Adoption (2024) | 88% |

| District Spend | US K–12 annual | $824B |

| Outcome-driven | Buyers (2024) | 72% |

| Social Reach | Global users (2024) | 5.07B |

Full Version Awaits

The Learning Network Porter's Five Forces Analysis

This preview shows the exact The Learning Network Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders or mockups; the file here is the final deliverable. Use it instantly for strategic insights and competitive assessment.