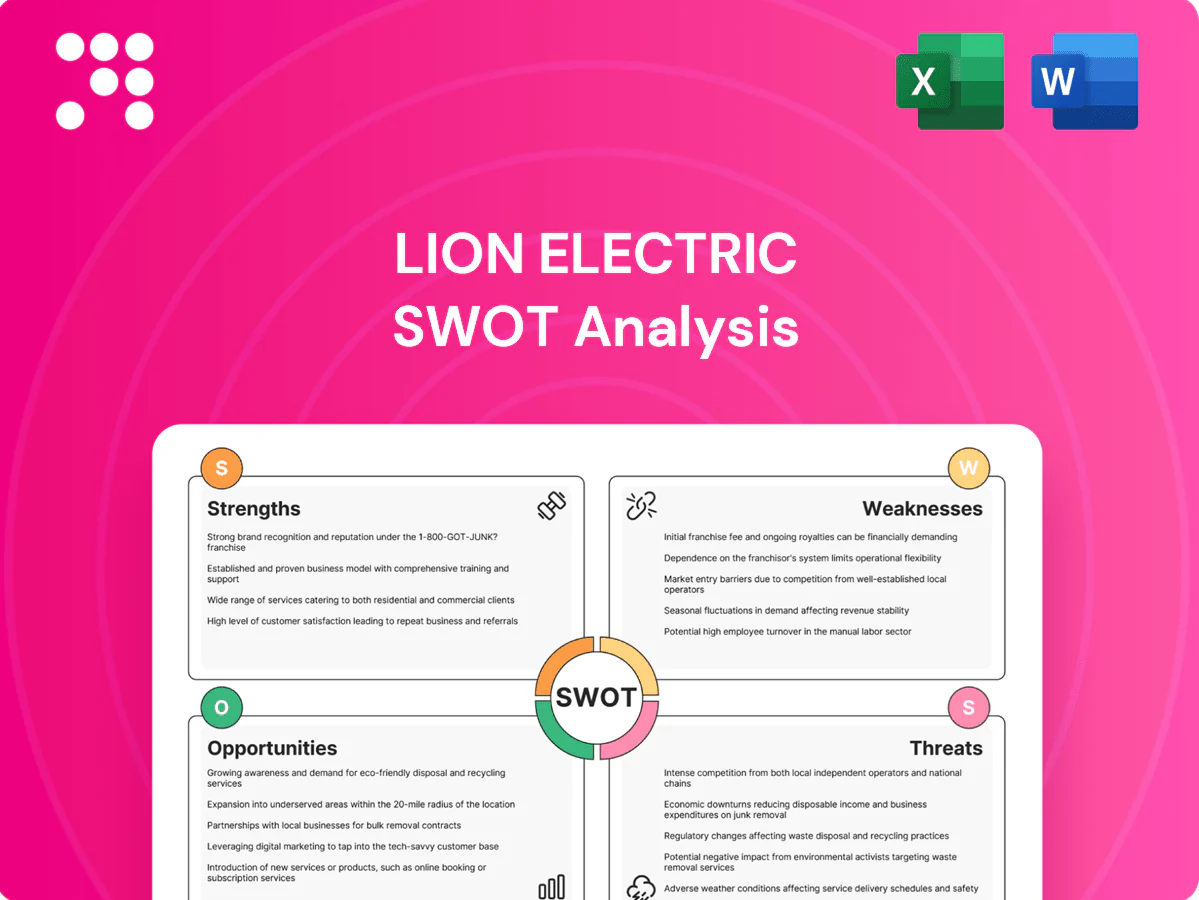

Lion Electric SWOT Analysis

Your Strategic Toolkit Starts Here

Lion Electric shows strong EV leadership in commercial vehicles, cost advantages from vertical integration, and expanding North American contracts, but faces supply-chain pressure, margin risks, and competitive and regulatory headwinds. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT analysis—deliverables include a polished Word report and editable Excel matrix for planning and pitches.

Strengths

Leader in electric school buses

Lion Electric is an early mover and is widely recognized as a North American leader in purpose-built all-electric school buses, with over 1,000 electric buses reported in service by 2024, strengthening brand trust among school districts and municipalities.

Focused product-market fit for school transport drives faster adoption and repeat orders, reflected in multi-year municipal contracts and fleet expansions reported across U.S. and Canadian districts.

High public visibility of school buses has helped Lion secure public-sector support, including state and federal incentives and grant-funded fleet purchases that accelerate procurement cycles.

Integrated vehicles, charging, and services

Lion Electric (NYSE: LEV, TSX: LEV), founded 2011 and publicly listed in 2021, bundles vehicles with charging and support to offer a one-stop solution that cuts customer friction in planning, installation, and operations. Bundling enables multi-year service agreements that boost customer stickiness and margin stability, while integrated telematics create data feedback loops for continuous product improvement.

Purpose-built, zero-emission platforms

Lion designs platforms specifically for electric drivetrains rather than retrofitting ICE chassis, enabling optimized battery placement, weight distribution and thermal management. Purpose-built architecture yields better range and reliability in urban duty cycles, improving total cost of ownership and uptime for fleets. This technical differentiation supports premium pricing and performance branding; Lion reported CAD 436M revenue in 2023, reflecting growing commercial traction.

Public-sector alignment and funding fit

Lion Electric’s electric school and transit vehicles map directly to clean-air mandates and fleet decarbonization, tapping a US school-bus fleet of about 480,000 vehicles and programs like the EPA Clean School Bus Program (roughly $5 billion) that shorten payback and speed procurement, improving pipeline visibility and supporting long-term demand.

- Policy tailwind: EPA $5B Clean School Bus

- Market fit: ~480,000 US school buses

- Financial impact: grants/rebates shorten payback, accelerate orders

North American manufacturing and support

North American manufacturing (Saint-Jérôme, QC and the Joliet, IL facility announced in 2022) allows Lion Electric to meet Buy America-type rules from the IIJA, shorten lead times to US/Canadian fleets, and reduce supply-chain and geopolitical exposure. Local plants improve after-sales support and operator training, and proximity to customers aids collaboration on custom specs and duty-cycle validation.

- Regional production: compliance with Buy America/IIJA

- Faster delivery: reduced lead times to North American fleets

- Enhanced service: stronger after-sales, training, and customization

- Risk mitigation: lower geopolitical and logistics exposure

Electric school-bus leader - 1,000+ in service; CAD 436M revenue

Lion Electric is a North American leader in purpose-built electric school buses with over 1,000 buses in service by 2024, boosting brand trust.

The company reported CAD 436M revenue in 2023 and leverages bundled vehicles, charging and telematics to increase stickiness and margins.

Policy tailwinds (EPA $5B Clean School Bus) and a ~480,000 US school-bus market support strong demand visibility.

North American plants (Saint-Jérôme, QC; Joliet, IL) ensure Buy America compliance, shorter lead times and better after-sales.

| Metric | Value |

|---|---|

| Buses in service (2024) | ~1,000 |

| Revenue (2023) | CAD 436M |

| EPA Clean School Bus | ~$5B |

| US school-bus fleet | ~480,000 |

What is included in the product

Delivers a strategic overview of Lion Electric’s internal strengths and weaknesses while outlining external opportunities and threats shaping its competitive position and future growth.

Provides a concise, Lion Electric–focused SWOT matrix for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting market or regulatory priorities.

Weaknesses

High capital needs and cash burn

Commercial EV manufacturing requires substantial investment in plants, tooling, and working capital, and Lion Electric has reported consistent operating losses as it scales production.

Scaling volumes to reach breakeven is time-sensitive and prolonged cash burn has pressured Lion’s liquidity, forcing reliance on equity and debt raises.

Dependence on external financing increases execution risk and can dilute shareholders if additional capital is needed before sustainable margins are achieved.

Battery and component dependencies

Lion Electric's core value proposition is tightly tied to battery pack availability and cost, with global average pack prices around $127/kWh in 2024 (BNEF), making input-price swings material to margins. Supplier constraints have delayed deliveries and compressed gross margins in recent quarters. With limited scale versus tier-1 cell and power-electronics suppliers, bargaining power is weak, and any battery quality or recall can cascade across multiple models and programs.

Scaling and quality management risks

Lion Electric (NYSE: LEV, TSX: LEV) flagged in its 2024 MD&A that ramping production while holding quality is complex for a growing OEM; low-to-mid volume variability raises unit costs and field reliability problems drive warranty expense and reputational risk; process maturity and stricter supplier PPAP discipline remain active priorities into 2025.

Customer concentration in public fleets

Customer concentration in public fleets leaves Lion Electric heavily reliant on school districts and municipal buyers; budget cycles and grant timing produce lumpy demand, while procurement delays or policy shifts can stall orders and amplify exposure to single large bid outcomes.

- Revenue reliance on public fleets

- Demand lumpiness from grant timing

- Procurement delays risk order timing

- High exposure to bid/program changes

Price pressure versus larger OEMs

Global truck and bus OEMs (Volvo, Daimler, Paccar, BYD, others) are rapidly entering the electric segment with scale, extensive dealer networks and captive finance arms, enabling aggressive pricing and bundled services that can compress Lion Electric’s margins. Fleet buyers often prefer established brands for perceived lower residual-value and operational risk, complicating Lion’s customer acquisition and pricing power.

- Competitive scale: large OEMs with global dealer and finance networks

- Margin pressure: aggressive pricing and bundled offerings

- Brand risk: fleets favor established OEMs for residual-value certainty

High capital intensity and cash burn amid $127/kWh battery cost pressure

High capital intensity and persistent operating losses hamper scale-up and drove continued cash burn per Lion’s 2024 MD&A.

Battery pack cost risk is material: global average pack price ~ $127/kWh in 2024 (BNEF), squeezing margins and exposing supplier dependency.

Customer concentration in public fleets creates lumpy demand and procurement timing risk versus large OEMs with scale advantages.

| Metric | 2024 |

|---|---|

| Avg pack $/kWh | $127 |

Full Version Awaits

Lion Electric SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate use after checkout.

Your Strategic Toolkit Starts Here

Lion Electric shows strong EV leadership in commercial vehicles, cost advantages from vertical integration, and expanding North American contracts, but faces supply-chain pressure, margin risks, and competitive and regulatory headwinds. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT analysis—deliverables include a polished Word report and editable Excel matrix for planning and pitches.

Strengths

Leader in electric school buses

Lion Electric is an early mover and is widely recognized as a North American leader in purpose-built all-electric school buses, with over 1,000 electric buses reported in service by 2024, strengthening brand trust among school districts and municipalities.

Focused product-market fit for school transport drives faster adoption and repeat orders, reflected in multi-year municipal contracts and fleet expansions reported across U.S. and Canadian districts.

High public visibility of school buses has helped Lion secure public-sector support, including state and federal incentives and grant-funded fleet purchases that accelerate procurement cycles.

Integrated vehicles, charging, and services

Lion Electric (NYSE: LEV, TSX: LEV), founded 2011 and publicly listed in 2021, bundles vehicles with charging and support to offer a one-stop solution that cuts customer friction in planning, installation, and operations. Bundling enables multi-year service agreements that boost customer stickiness and margin stability, while integrated telematics create data feedback loops for continuous product improvement.

Purpose-built, zero-emission platforms

Lion designs platforms specifically for electric drivetrains rather than retrofitting ICE chassis, enabling optimized battery placement, weight distribution and thermal management. Purpose-built architecture yields better range and reliability in urban duty cycles, improving total cost of ownership and uptime for fleets. This technical differentiation supports premium pricing and performance branding; Lion reported CAD 436M revenue in 2023, reflecting growing commercial traction.

Public-sector alignment and funding fit

Lion Electric’s electric school and transit vehicles map directly to clean-air mandates and fleet decarbonization, tapping a US school-bus fleet of about 480,000 vehicles and programs like the EPA Clean School Bus Program (roughly $5 billion) that shorten payback and speed procurement, improving pipeline visibility and supporting long-term demand.

- Policy tailwind: EPA $5B Clean School Bus

- Market fit: ~480,000 US school buses

- Financial impact: grants/rebates shorten payback, accelerate orders

North American manufacturing and support

North American manufacturing (Saint-Jérôme, QC and the Joliet, IL facility announced in 2022) allows Lion Electric to meet Buy America-type rules from the IIJA, shorten lead times to US/Canadian fleets, and reduce supply-chain and geopolitical exposure. Local plants improve after-sales support and operator training, and proximity to customers aids collaboration on custom specs and duty-cycle validation.

- Regional production: compliance with Buy America/IIJA

- Faster delivery: reduced lead times to North American fleets

- Enhanced service: stronger after-sales, training, and customization

- Risk mitigation: lower geopolitical and logistics exposure

Electric school-bus leader - 1,000+ in service; CAD 436M revenue

Lion Electric is a North American leader in purpose-built electric school buses with over 1,000 buses in service by 2024, boosting brand trust.

The company reported CAD 436M revenue in 2023 and leverages bundled vehicles, charging and telematics to increase stickiness and margins.

Policy tailwinds (EPA $5B Clean School Bus) and a ~480,000 US school-bus market support strong demand visibility.

North American plants (Saint-Jérôme, QC; Joliet, IL) ensure Buy America compliance, shorter lead times and better after-sales.

| Metric | Value |

|---|---|

| Buses in service (2024) | ~1,000 |

| Revenue (2023) | CAD 436M |

| EPA Clean School Bus | ~$5B |

| US school-bus fleet | ~480,000 |

What is included in the product

Delivers a strategic overview of Lion Electric’s internal strengths and weaknesses while outlining external opportunities and threats shaping its competitive position and future growth.

Provides a concise, Lion Electric–focused SWOT matrix for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting market or regulatory priorities.

Weaknesses

High capital needs and cash burn

Commercial EV manufacturing requires substantial investment in plants, tooling, and working capital, and Lion Electric has reported consistent operating losses as it scales production.

Scaling volumes to reach breakeven is time-sensitive and prolonged cash burn has pressured Lion’s liquidity, forcing reliance on equity and debt raises.

Dependence on external financing increases execution risk and can dilute shareholders if additional capital is needed before sustainable margins are achieved.

Battery and component dependencies

Lion Electric's core value proposition is tightly tied to battery pack availability and cost, with global average pack prices around $127/kWh in 2024 (BNEF), making input-price swings material to margins. Supplier constraints have delayed deliveries and compressed gross margins in recent quarters. With limited scale versus tier-1 cell and power-electronics suppliers, bargaining power is weak, and any battery quality or recall can cascade across multiple models and programs.

Scaling and quality management risks

Lion Electric (NYSE: LEV, TSX: LEV) flagged in its 2024 MD&A that ramping production while holding quality is complex for a growing OEM; low-to-mid volume variability raises unit costs and field reliability problems drive warranty expense and reputational risk; process maturity and stricter supplier PPAP discipline remain active priorities into 2025.

Customer concentration in public fleets

Customer concentration in public fleets leaves Lion Electric heavily reliant on school districts and municipal buyers; budget cycles and grant timing produce lumpy demand, while procurement delays or policy shifts can stall orders and amplify exposure to single large bid outcomes.

- Revenue reliance on public fleets

- Demand lumpiness from grant timing

- Procurement delays risk order timing

- High exposure to bid/program changes

Price pressure versus larger OEMs

Global truck and bus OEMs (Volvo, Daimler, Paccar, BYD, others) are rapidly entering the electric segment with scale, extensive dealer networks and captive finance arms, enabling aggressive pricing and bundled services that can compress Lion Electric’s margins. Fleet buyers often prefer established brands for perceived lower residual-value and operational risk, complicating Lion’s customer acquisition and pricing power.

- Competitive scale: large OEMs with global dealer and finance networks

- Margin pressure: aggressive pricing and bundled offerings

- Brand risk: fleets favor established OEMs for residual-value certainty

High capital intensity and cash burn amid $127/kWh battery cost pressure

High capital intensity and persistent operating losses hamper scale-up and drove continued cash burn per Lion’s 2024 MD&A.

Battery pack cost risk is material: global average pack price ~ $127/kWh in 2024 (BNEF), squeezing margins and exposing supplier dependency.

Customer concentration in public fleets creates lumpy demand and procurement timing risk versus large OEMs with scale advantages.

| Metric | 2024 |

|---|---|

| Avg pack $/kWh | $127 |

Full Version Awaits

Lion Electric SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate use after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Lion Electric shows strong EV leadership in commercial vehicles, cost advantages from vertical integration, and expanding North American contracts, but faces supply-chain pressure, margin risks, and competitive and regulatory headwinds. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT analysis—deliverables include a polished Word report and editable Excel matrix for planning and pitches.

Strengths

Leader in electric school buses

Lion Electric is an early mover and is widely recognized as a North American leader in purpose-built all-electric school buses, with over 1,000 electric buses reported in service by 2024, strengthening brand trust among school districts and municipalities.

Focused product-market fit for school transport drives faster adoption and repeat orders, reflected in multi-year municipal contracts and fleet expansions reported across U.S. and Canadian districts.

High public visibility of school buses has helped Lion secure public-sector support, including state and federal incentives and grant-funded fleet purchases that accelerate procurement cycles.

Integrated vehicles, charging, and services

Lion Electric (NYSE: LEV, TSX: LEV), founded 2011 and publicly listed in 2021, bundles vehicles with charging and support to offer a one-stop solution that cuts customer friction in planning, installation, and operations. Bundling enables multi-year service agreements that boost customer stickiness and margin stability, while integrated telematics create data feedback loops for continuous product improvement.

Purpose-built, zero-emission platforms

Lion designs platforms specifically for electric drivetrains rather than retrofitting ICE chassis, enabling optimized battery placement, weight distribution and thermal management. Purpose-built architecture yields better range and reliability in urban duty cycles, improving total cost of ownership and uptime for fleets. This technical differentiation supports premium pricing and performance branding; Lion reported CAD 436M revenue in 2023, reflecting growing commercial traction.

Public-sector alignment and funding fit

Lion Electric’s electric school and transit vehicles map directly to clean-air mandates and fleet decarbonization, tapping a US school-bus fleet of about 480,000 vehicles and programs like the EPA Clean School Bus Program (roughly $5 billion) that shorten payback and speed procurement, improving pipeline visibility and supporting long-term demand.

- Policy tailwind: EPA $5B Clean School Bus

- Market fit: ~480,000 US school buses

- Financial impact: grants/rebates shorten payback, accelerate orders

North American manufacturing and support

North American manufacturing (Saint-Jérôme, QC and the Joliet, IL facility announced in 2022) allows Lion Electric to meet Buy America-type rules from the IIJA, shorten lead times to US/Canadian fleets, and reduce supply-chain and geopolitical exposure. Local plants improve after-sales support and operator training, and proximity to customers aids collaboration on custom specs and duty-cycle validation.

- Regional production: compliance with Buy America/IIJA

- Faster delivery: reduced lead times to North American fleets

- Enhanced service: stronger after-sales, training, and customization

- Risk mitigation: lower geopolitical and logistics exposure

Electric school-bus leader - 1,000+ in service; CAD 436M revenue

Lion Electric is a North American leader in purpose-built electric school buses with over 1,000 buses in service by 2024, boosting brand trust.

The company reported CAD 436M revenue in 2023 and leverages bundled vehicles, charging and telematics to increase stickiness and margins.

Policy tailwinds (EPA $5B Clean School Bus) and a ~480,000 US school-bus market support strong demand visibility.

North American plants (Saint-Jérôme, QC; Joliet, IL) ensure Buy America compliance, shorter lead times and better after-sales.

| Metric | Value |

|---|---|

| Buses in service (2024) | ~1,000 |

| Revenue (2023) | CAD 436M |

| EPA Clean School Bus | ~$5B |

| US school-bus fleet | ~480,000 |

What is included in the product

Delivers a strategic overview of Lion Electric’s internal strengths and weaknesses while outlining external opportunities and threats shaping its competitive position and future growth.

Provides a concise, Lion Electric–focused SWOT matrix for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting market or regulatory priorities.

Weaknesses

High capital needs and cash burn

Commercial EV manufacturing requires substantial investment in plants, tooling, and working capital, and Lion Electric has reported consistent operating losses as it scales production.

Scaling volumes to reach breakeven is time-sensitive and prolonged cash burn has pressured Lion’s liquidity, forcing reliance on equity and debt raises.

Dependence on external financing increases execution risk and can dilute shareholders if additional capital is needed before sustainable margins are achieved.

Battery and component dependencies

Lion Electric's core value proposition is tightly tied to battery pack availability and cost, with global average pack prices around $127/kWh in 2024 (BNEF), making input-price swings material to margins. Supplier constraints have delayed deliveries and compressed gross margins in recent quarters. With limited scale versus tier-1 cell and power-electronics suppliers, bargaining power is weak, and any battery quality or recall can cascade across multiple models and programs.

Scaling and quality management risks

Lion Electric (NYSE: LEV, TSX: LEV) flagged in its 2024 MD&A that ramping production while holding quality is complex for a growing OEM; low-to-mid volume variability raises unit costs and field reliability problems drive warranty expense and reputational risk; process maturity and stricter supplier PPAP discipline remain active priorities into 2025.

Customer concentration in public fleets

Customer concentration in public fleets leaves Lion Electric heavily reliant on school districts and municipal buyers; budget cycles and grant timing produce lumpy demand, while procurement delays or policy shifts can stall orders and amplify exposure to single large bid outcomes.

- Revenue reliance on public fleets

- Demand lumpiness from grant timing

- Procurement delays risk order timing

- High exposure to bid/program changes

Price pressure versus larger OEMs

Global truck and bus OEMs (Volvo, Daimler, Paccar, BYD, others) are rapidly entering the electric segment with scale, extensive dealer networks and captive finance arms, enabling aggressive pricing and bundled services that can compress Lion Electric’s margins. Fleet buyers often prefer established brands for perceived lower residual-value and operational risk, complicating Lion’s customer acquisition and pricing power.

- Competitive scale: large OEMs with global dealer and finance networks

- Margin pressure: aggressive pricing and bundled offerings

- Brand risk: fleets favor established OEMs for residual-value certainty

High capital intensity and cash burn amid $127/kWh battery cost pressure

High capital intensity and persistent operating losses hamper scale-up and drove continued cash burn per Lion’s 2024 MD&A.

Battery pack cost risk is material: global average pack price ~ $127/kWh in 2024 (BNEF), squeezing margins and exposing supplier dependency.

Customer concentration in public fleets creates lumpy demand and procurement timing risk versus large OEMs with scale advantages.

| Metric | 2024 |

|---|---|

| Avg pack $/kWh | $127 |

Full Version Awaits

Lion Electric SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate use after checkout.