Navigator Company Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company faces moderate supplier power but intense rivalry driven by commodity pulp and paper markets. Buyer price sensitivity and digital substitutes pressure margins, while high capital requirements restrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Navigator Company’s competitive dynamics in detail.

Suppliers Bargaining Power

High self-supply of fiber

Navigator’s certified forest base, exceeding 320,000 hectares in 2024, internalizes a large share of wood fiber and reduces exposure to third‑party timber suppliers. Vertical integration lowers input price volatility and supplier leverage, contributing to stable pulp margins. Full certification ensures traceability and alignment with sustainability standards. Residual dependence remains for specific fiber grades and regional sourcing gaps.

Chemicals and additives concentration

Key inputs like chemicals, starch, fillers and bleaching agents are sourced from a concentrated set of global suppliers (major players include BASF, Dow, INEOS, Solvay), with the global pulp and paper chemicals market ~USD 12 billion in 2024. Standardization keeps switching costs moderate, but strict qualification and quality needs limit substitution. Long-term contracts and dual-sourcing mitigate supplier power; price pass-through was often partial during commodity spikes.

Energy and logistics dependencies

Despite significant bioenergy generation, Navigator still purchases external electricity, natural gas and transport fuel, leaving it exposed to volatile energy markets and freight pricing that spiked globally in 2022–23; logistics disruptions can rapidly raise input costs. Onsite cogeneration and biomass boilers now supply roughly half of heat and cut carbon intensity materially. Proximity to Leixões and Setúbal ports and optimized transport contracts help rebalance supplier leverage.

Capital equipment and maintenance

Paper machines, recovery boilers and automation systems for Navigator come from a small set of OEMs (Valmet, Andritz, Voith) with proprietary technology, creating high switching costs and supplier leverage; specialised maintenance and OEM spare parts reinforce that power. Long-life assets and preventive maintenance programmes reduce purchase frequency, while multi-year framework agreements and competitive tenders keep price pressure in check.

- Key OEMs: Valmet, Andritz, Voith

- High switching costs due to proprietary tech and spares

- Preventive maintenance dilutes bargaining frequency

- Framework agreements and tenders limit price premiums

Labor and specialized skills

Skilled operators, engineers and forestry experts at The Navigator Company are critical and hard to substitute; the firm reported about 3,324 employees in 2023 (annual report), concentrating operational expertise in mills and forest management. Tight Iberian labor markets and strict safety rules push wage pressure and OPEX up, while training pipelines and employer branding lower external dependency; union rules and local regs materially shape negotiation leverage.

- Workforce: ~3,324 (2023 annual report)

- Wage pressure: tight regional labor markets

- Mitigation: internal training & employer branding

- Driver: unions and local regulations

320,000+ ha curbs suppliers; chemicals (~USD 12bn)

Navigator’s supplier power is limited by 320,000+ ha certified forest (2024), vertical integration and long-term contracts, but concentrated chemical suppliers (~USD12bn market in 2024), OEM dependence (Valmet, Andritz, Voith) and energy/fuel exposure keep supplier leverage moderate to elevated in pockets.

| Metric | Value (2024) |

|---|---|

| Forest area | 320,000+ ha |

| Chemicals market | ~USD 12bn |

| Workforce | ~3,324 (2023) |

What is included in the product

Concise Porter's Five Forces review for Navigator Company, assessing rivalry, supplier and buyer power, substitution and entry threats, plus strategic levers to protect margins and guide competitive positioning.

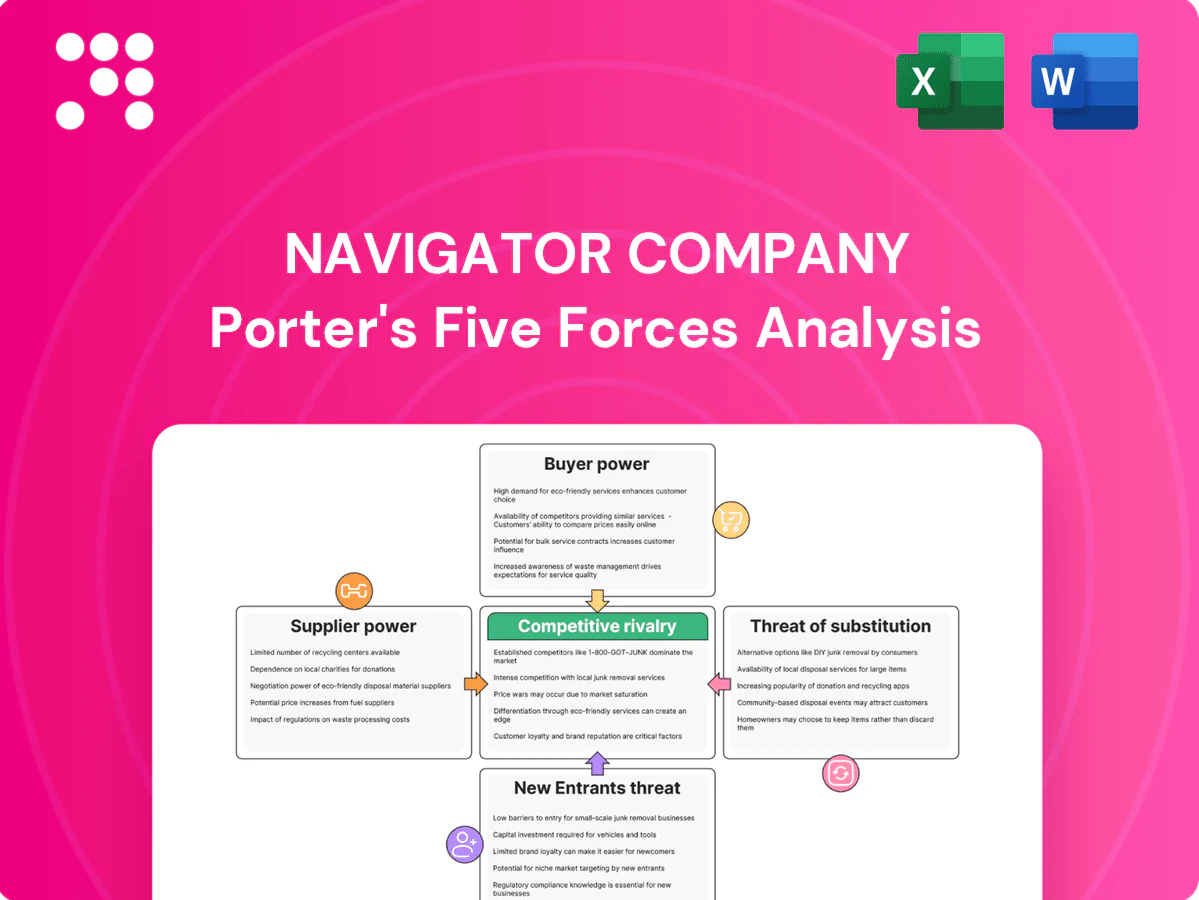

A concise, one-sheet Porter's Five Forces for The Navigator Company—visual spider chart and editable pressure sliders to instantly pinpoint strategic pain points, customize scenarios, and drop straight into decks or dashboards.

Customers Bargaining Power

Large B2B buyers concentrated

Large B2B buyers—publishers, printers, office distributors, tissue retailers and converters—buy in bulk (contracts often 1,000+ tonnes), giving them strong negotiating leverage on price and payment terms; framework contracts and public tenders further compress margins. For Navigator Company, where paper and pulp sales drove roughly €1.6bn revenue in 2023–24, service reliability and FSC/PEFC sustainability credentials can command premiums of 5–10% in key contracts.

Commoditization in UWF

Uncoated woodfree (UWF) paper is heavily price-referenced, boosting buyer bargaining power as standardized specs enable easy comparison across suppliers. Value-adds such as higher brightness, superior runnability and FSC/PEFC certifications can mitigate price pressure by creating differentiation. Navigator’s strong brand and on-time delivery performance support retention, aided by its c.1.7 million tonne paper/pulp capacity in 2024.

Switching costs are modest

Buyers can qualify multiple mills and routinely switch based on price or availability, limiting Navigator's pricing power despite the group reporting c.€2.2bn sales in 2023 and ~1.6 Mt paper/pulp capacity. Printing and converting lines accept equivalent grades, reducing hard barriers, while Navigator's technical service and consistent quality create soft switching frictions. Multi-year contracts and rebate schemes further lock in share with key customers.

Retail private label in tissue

Retailers aggressively expand private label in tissue, squeezing supplier margins as 2024 private-label penetration in European tissue reached about 45%, with promotional cycles and high shelf power amplifying buyer influence. Differentiation in softness, recycled content and innovation improves product mix and margin recovery. Geographic and channel diversification lowers concentration risk for Navigator Company.

- Private-label share ~45% (2024)

- Promotions/shelf power = higher buyer leverage

- Differentiation: softness, sustainability, innovation

- Diversify geographies/channels to reduce concentration

Sustainability and compliance demands

Customers increasingly demand FSC/PEFC certification, low-carbon footprints and full supply-chain traceability; compliance-driven costs lift supplier barriers to entry and can become a durable competitive moat. Buyers prefer partners with verified ESG metrics, and Navigator’s stated forestry stewardship and certified landholdings align closely with these procurement filters in 2024.

- Tags: FSC, PEFC, traceability

- 2024: certified stewardship aligns with buyer ESG filters

- Compliance raises supplier costs → moat

Large B2B buyers cut leverage; sales €1.6bn, capacity 1.7 Mt

Large B2B buyers (contracts 1,000+ t) exert strong price/payment leverage; Navigator’s paper/pulp sales ~€1.6bn (2023–24) and 1.7 Mt capacity limit pricing power. UWF commoditization and multi-mill qualification increase buyer power, while FSC/PEFC and on-time delivery can secure 5–10% premiums. European tissue private-label ~45% (2024) intensifies retailer bargaining, offset by product differentiation and geographic diversification.

| Metric | Value |

|---|---|

| Paper/pulp sales (2023–24) | €1.6bn |

| Capacity (2024) | 1.7 Mt |

| FSC/PEFC premium | 5–10% |

| EU tissue private-label (2024) | 45% |

Same Document Delivered

Navigator Company Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for The Navigator Company you'll receive after purchase—no surprises, no placeholders. The document is the full, professionally formatted assessment of competitive rivalry, buyer and supplier power, and threats of entry and substitution. It includes actionable insights and is ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company faces moderate supplier power but intense rivalry driven by commodity pulp and paper markets. Buyer price sensitivity and digital substitutes pressure margins, while high capital requirements restrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Navigator Company’s competitive dynamics in detail.

Suppliers Bargaining Power

High self-supply of fiber

Navigator’s certified forest base, exceeding 320,000 hectares in 2024, internalizes a large share of wood fiber and reduces exposure to third‑party timber suppliers. Vertical integration lowers input price volatility and supplier leverage, contributing to stable pulp margins. Full certification ensures traceability and alignment with sustainability standards. Residual dependence remains for specific fiber grades and regional sourcing gaps.

Chemicals and additives concentration

Key inputs like chemicals, starch, fillers and bleaching agents are sourced from a concentrated set of global suppliers (major players include BASF, Dow, INEOS, Solvay), with the global pulp and paper chemicals market ~USD 12 billion in 2024. Standardization keeps switching costs moderate, but strict qualification and quality needs limit substitution. Long-term contracts and dual-sourcing mitigate supplier power; price pass-through was often partial during commodity spikes.

Energy and logistics dependencies

Despite significant bioenergy generation, Navigator still purchases external electricity, natural gas and transport fuel, leaving it exposed to volatile energy markets and freight pricing that spiked globally in 2022–23; logistics disruptions can rapidly raise input costs. Onsite cogeneration and biomass boilers now supply roughly half of heat and cut carbon intensity materially. Proximity to Leixões and Setúbal ports and optimized transport contracts help rebalance supplier leverage.

Capital equipment and maintenance

Paper machines, recovery boilers and automation systems for Navigator come from a small set of OEMs (Valmet, Andritz, Voith) with proprietary technology, creating high switching costs and supplier leverage; specialised maintenance and OEM spare parts reinforce that power. Long-life assets and preventive maintenance programmes reduce purchase frequency, while multi-year framework agreements and competitive tenders keep price pressure in check.

- Key OEMs: Valmet, Andritz, Voith

- High switching costs due to proprietary tech and spares

- Preventive maintenance dilutes bargaining frequency

- Framework agreements and tenders limit price premiums

Labor and specialized skills

Skilled operators, engineers and forestry experts at The Navigator Company are critical and hard to substitute; the firm reported about 3,324 employees in 2023 (annual report), concentrating operational expertise in mills and forest management. Tight Iberian labor markets and strict safety rules push wage pressure and OPEX up, while training pipelines and employer branding lower external dependency; union rules and local regs materially shape negotiation leverage.

- Workforce: ~3,324 (2023 annual report)

- Wage pressure: tight regional labor markets

- Mitigation: internal training & employer branding

- Driver: unions and local regulations

320,000+ ha curbs suppliers; chemicals (~USD 12bn)

Navigator’s supplier power is limited by 320,000+ ha certified forest (2024), vertical integration and long-term contracts, but concentrated chemical suppliers (~USD12bn market in 2024), OEM dependence (Valmet, Andritz, Voith) and energy/fuel exposure keep supplier leverage moderate to elevated in pockets.

| Metric | Value (2024) |

|---|---|

| Forest area | 320,000+ ha |

| Chemicals market | ~USD 12bn |

| Workforce | ~3,324 (2023) |

What is included in the product

Concise Porter's Five Forces review for Navigator Company, assessing rivalry, supplier and buyer power, substitution and entry threats, plus strategic levers to protect margins and guide competitive positioning.

A concise, one-sheet Porter's Five Forces for The Navigator Company—visual spider chart and editable pressure sliders to instantly pinpoint strategic pain points, customize scenarios, and drop straight into decks or dashboards.

Customers Bargaining Power

Large B2B buyers concentrated

Large B2B buyers—publishers, printers, office distributors, tissue retailers and converters—buy in bulk (contracts often 1,000+ tonnes), giving them strong negotiating leverage on price and payment terms; framework contracts and public tenders further compress margins. For Navigator Company, where paper and pulp sales drove roughly €1.6bn revenue in 2023–24, service reliability and FSC/PEFC sustainability credentials can command premiums of 5–10% in key contracts.

Commoditization in UWF

Uncoated woodfree (UWF) paper is heavily price-referenced, boosting buyer bargaining power as standardized specs enable easy comparison across suppliers. Value-adds such as higher brightness, superior runnability and FSC/PEFC certifications can mitigate price pressure by creating differentiation. Navigator’s strong brand and on-time delivery performance support retention, aided by its c.1.7 million tonne paper/pulp capacity in 2024.

Switching costs are modest

Buyers can qualify multiple mills and routinely switch based on price or availability, limiting Navigator's pricing power despite the group reporting c.€2.2bn sales in 2023 and ~1.6 Mt paper/pulp capacity. Printing and converting lines accept equivalent grades, reducing hard barriers, while Navigator's technical service and consistent quality create soft switching frictions. Multi-year contracts and rebate schemes further lock in share with key customers.

Retail private label in tissue

Retailers aggressively expand private label in tissue, squeezing supplier margins as 2024 private-label penetration in European tissue reached about 45%, with promotional cycles and high shelf power amplifying buyer influence. Differentiation in softness, recycled content and innovation improves product mix and margin recovery. Geographic and channel diversification lowers concentration risk for Navigator Company.

- Private-label share ~45% (2024)

- Promotions/shelf power = higher buyer leverage

- Differentiation: softness, sustainability, innovation

- Diversify geographies/channels to reduce concentration

Sustainability and compliance demands

Customers increasingly demand FSC/PEFC certification, low-carbon footprints and full supply-chain traceability; compliance-driven costs lift supplier barriers to entry and can become a durable competitive moat. Buyers prefer partners with verified ESG metrics, and Navigator’s stated forestry stewardship and certified landholdings align closely with these procurement filters in 2024.

- Tags: FSC, PEFC, traceability

- 2024: certified stewardship aligns with buyer ESG filters

- Compliance raises supplier costs → moat

Large B2B buyers cut leverage; sales €1.6bn, capacity 1.7 Mt

Large B2B buyers (contracts 1,000+ t) exert strong price/payment leverage; Navigator’s paper/pulp sales ~€1.6bn (2023–24) and 1.7 Mt capacity limit pricing power. UWF commoditization and multi-mill qualification increase buyer power, while FSC/PEFC and on-time delivery can secure 5–10% premiums. European tissue private-label ~45% (2024) intensifies retailer bargaining, offset by product differentiation and geographic diversification.

| Metric | Value |

|---|---|

| Paper/pulp sales (2023–24) | €1.6bn |

| Capacity (2024) | 1.7 Mt |

| FSC/PEFC premium | 5–10% |

| EU tissue private-label (2024) | 45% |

Same Document Delivered

Navigator Company Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for The Navigator Company you'll receive after purchase—no surprises, no placeholders. The document is the full, professionally formatted assessment of competitive rivalry, buyer and supplier power, and threats of entry and substitution. It includes actionable insights and is ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company faces moderate supplier power but intense rivalry driven by commodity pulp and paper markets. Buyer price sensitivity and digital substitutes pressure margins, while high capital requirements restrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Navigator Company’s competitive dynamics in detail.

Suppliers Bargaining Power

High self-supply of fiber

Navigator’s certified forest base, exceeding 320,000 hectares in 2024, internalizes a large share of wood fiber and reduces exposure to third‑party timber suppliers. Vertical integration lowers input price volatility and supplier leverage, contributing to stable pulp margins. Full certification ensures traceability and alignment with sustainability standards. Residual dependence remains for specific fiber grades and regional sourcing gaps.

Chemicals and additives concentration

Key inputs like chemicals, starch, fillers and bleaching agents are sourced from a concentrated set of global suppliers (major players include BASF, Dow, INEOS, Solvay), with the global pulp and paper chemicals market ~USD 12 billion in 2024. Standardization keeps switching costs moderate, but strict qualification and quality needs limit substitution. Long-term contracts and dual-sourcing mitigate supplier power; price pass-through was often partial during commodity spikes.

Energy and logistics dependencies

Despite significant bioenergy generation, Navigator still purchases external electricity, natural gas and transport fuel, leaving it exposed to volatile energy markets and freight pricing that spiked globally in 2022–23; logistics disruptions can rapidly raise input costs. Onsite cogeneration and biomass boilers now supply roughly half of heat and cut carbon intensity materially. Proximity to Leixões and Setúbal ports and optimized transport contracts help rebalance supplier leverage.

Capital equipment and maintenance

Paper machines, recovery boilers and automation systems for Navigator come from a small set of OEMs (Valmet, Andritz, Voith) with proprietary technology, creating high switching costs and supplier leverage; specialised maintenance and OEM spare parts reinforce that power. Long-life assets and preventive maintenance programmes reduce purchase frequency, while multi-year framework agreements and competitive tenders keep price pressure in check.

- Key OEMs: Valmet, Andritz, Voith

- High switching costs due to proprietary tech and spares

- Preventive maintenance dilutes bargaining frequency

- Framework agreements and tenders limit price premiums

Labor and specialized skills

Skilled operators, engineers and forestry experts at The Navigator Company are critical and hard to substitute; the firm reported about 3,324 employees in 2023 (annual report), concentrating operational expertise in mills and forest management. Tight Iberian labor markets and strict safety rules push wage pressure and OPEX up, while training pipelines and employer branding lower external dependency; union rules and local regs materially shape negotiation leverage.

- Workforce: ~3,324 (2023 annual report)

- Wage pressure: tight regional labor markets

- Mitigation: internal training & employer branding

- Driver: unions and local regulations

320,000+ ha curbs suppliers; chemicals (~USD 12bn)

Navigator’s supplier power is limited by 320,000+ ha certified forest (2024), vertical integration and long-term contracts, but concentrated chemical suppliers (~USD12bn market in 2024), OEM dependence (Valmet, Andritz, Voith) and energy/fuel exposure keep supplier leverage moderate to elevated in pockets.

| Metric | Value (2024) |

|---|---|

| Forest area | 320,000+ ha |

| Chemicals market | ~USD 12bn |

| Workforce | ~3,324 (2023) |

What is included in the product

Concise Porter's Five Forces review for Navigator Company, assessing rivalry, supplier and buyer power, substitution and entry threats, plus strategic levers to protect margins and guide competitive positioning.

A concise, one-sheet Porter's Five Forces for The Navigator Company—visual spider chart and editable pressure sliders to instantly pinpoint strategic pain points, customize scenarios, and drop straight into decks or dashboards.

Customers Bargaining Power

Large B2B buyers concentrated

Large B2B buyers—publishers, printers, office distributors, tissue retailers and converters—buy in bulk (contracts often 1,000+ tonnes), giving them strong negotiating leverage on price and payment terms; framework contracts and public tenders further compress margins. For Navigator Company, where paper and pulp sales drove roughly €1.6bn revenue in 2023–24, service reliability and FSC/PEFC sustainability credentials can command premiums of 5–10% in key contracts.

Commoditization in UWF

Uncoated woodfree (UWF) paper is heavily price-referenced, boosting buyer bargaining power as standardized specs enable easy comparison across suppliers. Value-adds such as higher brightness, superior runnability and FSC/PEFC certifications can mitigate price pressure by creating differentiation. Navigator’s strong brand and on-time delivery performance support retention, aided by its c.1.7 million tonne paper/pulp capacity in 2024.

Switching costs are modest

Buyers can qualify multiple mills and routinely switch based on price or availability, limiting Navigator's pricing power despite the group reporting c.€2.2bn sales in 2023 and ~1.6 Mt paper/pulp capacity. Printing and converting lines accept equivalent grades, reducing hard barriers, while Navigator's technical service and consistent quality create soft switching frictions. Multi-year contracts and rebate schemes further lock in share with key customers.

Retail private label in tissue

Retailers aggressively expand private label in tissue, squeezing supplier margins as 2024 private-label penetration in European tissue reached about 45%, with promotional cycles and high shelf power amplifying buyer influence. Differentiation in softness, recycled content and innovation improves product mix and margin recovery. Geographic and channel diversification lowers concentration risk for Navigator Company.

- Private-label share ~45% (2024)

- Promotions/shelf power = higher buyer leverage

- Differentiation: softness, sustainability, innovation

- Diversify geographies/channels to reduce concentration

Sustainability and compliance demands

Customers increasingly demand FSC/PEFC certification, low-carbon footprints and full supply-chain traceability; compliance-driven costs lift supplier barriers to entry and can become a durable competitive moat. Buyers prefer partners with verified ESG metrics, and Navigator’s stated forestry stewardship and certified landholdings align closely with these procurement filters in 2024.

- Tags: FSC, PEFC, traceability

- 2024: certified stewardship aligns with buyer ESG filters

- Compliance raises supplier costs → moat

Large B2B buyers cut leverage; sales €1.6bn, capacity 1.7 Mt

Large B2B buyers (contracts 1,000+ t) exert strong price/payment leverage; Navigator’s paper/pulp sales ~€1.6bn (2023–24) and 1.7 Mt capacity limit pricing power. UWF commoditization and multi-mill qualification increase buyer power, while FSC/PEFC and on-time delivery can secure 5–10% premiums. European tissue private-label ~45% (2024) intensifies retailer bargaining, offset by product differentiation and geographic diversification.

| Metric | Value |

|---|---|

| Paper/pulp sales (2023–24) | €1.6bn |

| Capacity (2024) | 1.7 Mt |

| FSC/PEFC premium | 5–10% |

| EU tissue private-label (2024) | 45% |

Same Document Delivered

Navigator Company Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for The Navigator Company you'll receive after purchase—no surprises, no placeholders. The document is the full, professionally formatted assessment of competitive rivalry, buyer and supplier power, and threats of entry and substitution. It includes actionable insights and is ready for immediate download and use.