Navigator Company SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company combines scale in pulp and paper production, strong export markets and sustainability credentials, but faces commodity cyclicality, input-cost pressures and regulatory risks. Want deeper, editable insights and strategic recommendations? Purchase the full SWOT (Word + Excel) to plan with confidence.

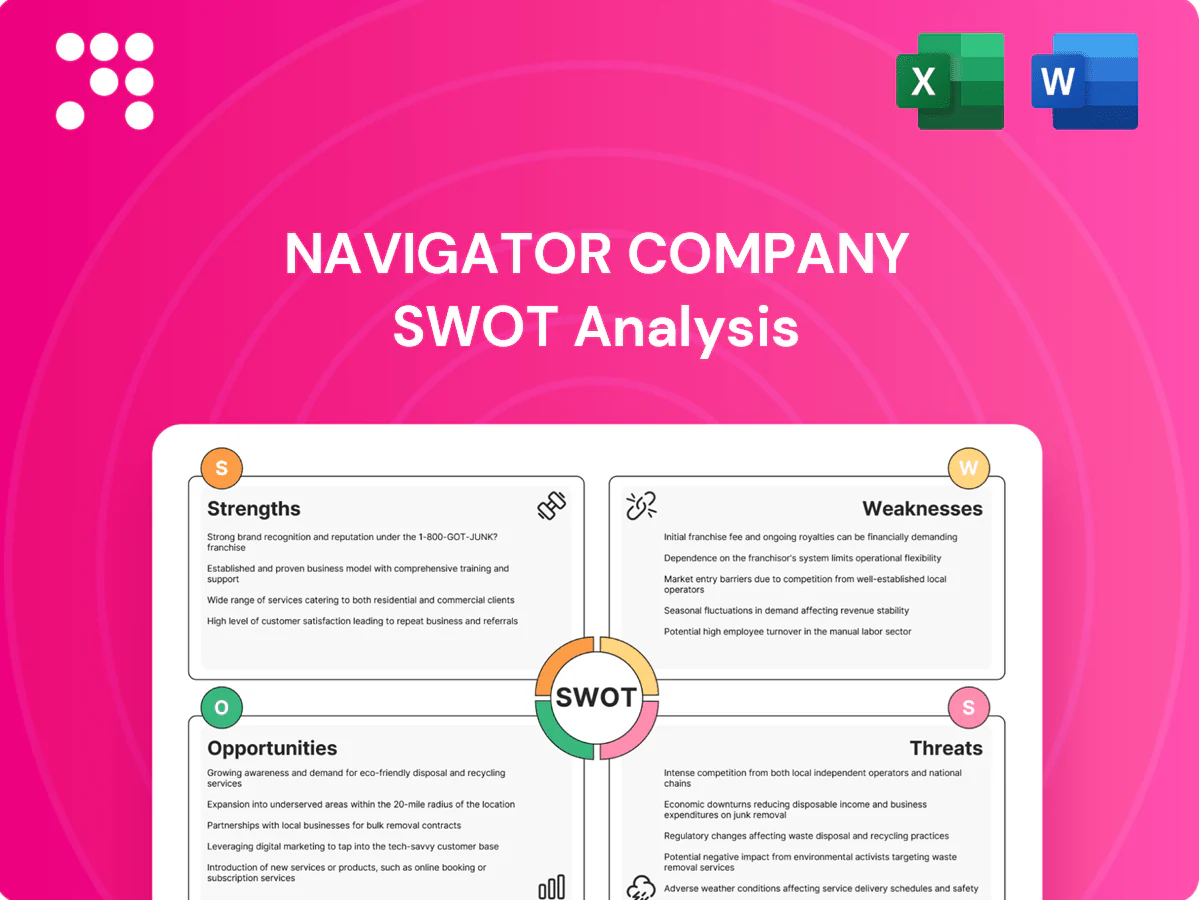

Strengths

Vertically integrated model

Navigator’s vertically integrated model controls ~114,000 hectares of forest and the full pulp, paper, tissue and energy chain, boosting cost visibility and supply security. Internal fiber sourcing cuts dependence on external pulp markets and supports consistent product quality and scheduling. Integration captures margin across the value chain, contributing to group revenues around €2.0bn (2024).

Certified sustainable forestry

Navigator Company holds FSC and PEFC certifications across its forest base, underpinning ESG credibility and long-term raw-material reliability.

These certifications facilitate access to premium customers and regulated EU markets, supporting higher-margin sales and supply-chain acceptance.

Sustainable forest practices reduce reputational and regulatory risk and enable participation in green finance instruments such as green bonds and sustainability-linked facilities.

Leadership in uncoated woodfree

Navigator’s leadership in uncoated woodfree paper—backed by ~1.2 Mtpa UWF capacity and 2023 revenue near €1.7bn—supports pricing power through a premium brand and quality. Scale efficiencies drive lower unit costs versus smaller rivals; a diversified customer split across office, home and professional channels stabilizes volumes. Ongoing product innovation preserves differentiation amid commoditization.

Renewable energy and bioenergy

Navigator's in-house biomass cogeneration supplies the bulk of heat and electricity needs, offsetting grid volatility and enabling surplus energy sales; in 2024 EU carbon prices averaged around €80/t, so lower carbon intensity directly protects margins under carbon pricing.

Self-generation and bioenergy exports created material ancillary revenue and improved resilience during recent European energy shocks (2022–24), reducing exposure to wholesale price spikes.

- captive cogeneration reduces grid dependence

- lower carbon intensity shields margins at ~€80/t EU ETS

- energy sales = additional revenue stream

- increases resilience in energy crises

Innovation and product breadth

R&D drives process efficiency, higher fiber yield and development of specialty grades, enabling Navigator to expand margins and product mix. Presence in tissue and value-added papers widens addressable markets and reduces exposure to commodity paper cycles. Continuous product upgrades and innovation support circularity and waste reduction across operations, reinforcing pricing power and market share defense.

- R&D-led yield and grade diversification

- Expansion into tissue/value-added papers

- Product upgrades defend price and share

- Innovation advances circularity, lowers waste

Vertically integrated pulp-paper-energy: 114k ha, €2.0bn

Navigator’s vertical integration controls ~114,000 ha and the full pulp‑paper‑energy chain, supporting 2024 group revenue ~€2.0bn and secure supply. FSC/PEFC certification underpins ESG credibility and access to premium EU markets. ~1.2 Mtpa UWF capacity, in‑house biomass cogeneration and R&D-driven grade diversification boost margins and resilience versus energy and pulp market swings (~€80/t EU ETS 2024).

| Metric | Value |

|---|---|

| Forest area | ~114,000 ha |

| Group revenue (2024) | ~€2.0bn |

| UWF capacity | ~1.2 Mtpa |

| EU ETS avg price (2024) | ~€80/t |

What is included in the product

Provides a concise SWOT analysis of Navigator Company, highlighting its market-leading pulp & paper production, strong sustainability credentials and integrated supply chain, alongside operational costs, revenue concentration and exposure to commodity cycles, and identifies growth opportunities in packaging, tissue and circular solutions plus threats from raw‑material volatility, regulatory shifts and global competition.

Provides a concise Navigator Company SWOT matrix for rapid strategic clarity, streamlining stakeholder presentations and enabling quick edits to reflect shifting market priorities.

Weaknesses

Exposure to print decline

Core uncoated woodfree (UWF) demand has been structurally pressured by digitization, with global graphic paper demand down c.30% since 2007, squeezing volumes and long‑run sales. Volume swings quickly compress mill utilization and margins given fixed-capacity mills and high conversion costs. Pricing cycles remain volatile and seasonal, tying cash flow to pulp and paper market swings. Heavy dependence on mature European markets constrains growth velocity.

Capital intensive operations

Forestry, pulping and papermaking at Navigator are highly capital intensive, requiring large upfront investment and continuous mill maintenance. High fixed costs mean margins swing sharply in downturns, amplifying earnings volatility. Major upgrade projects typically have multi-year payback horizons, tying up cash. During weak cycles balance-sheet flexibility can be constrained by sustained capex and working capital needs.

Geographic concentration

Navigator’s production and most mills are concentrated in Iberia, exposing the group to regional shocks; over 80% of its paper and pulp is exported, making local labor, regulatory or environmental disruptions highly impactful. Port congestion or logistics bottlenecks in Lisbon/Setúbal corridors can curtail shipments. Limited proximity to high‑growth APAC markets increases ocean freight costs and transit times compared with competitors with APAC hubs.

Input cost sensitivity

Despite strong bioenergy integration, Navigator remains exposed to chemical, logistics and residual energy costs that have shown volatility; in 2024 group revenue near EUR 2.5bn faced input cost spikes that at times outpaced contractual pass-throughs, compressing margins. Water-treatment and availability pressures during Iberian droughts have raised operating costs and capex needs, while EUR exchange volatility affects export unit economics and imported chemical prices.

- Input concentration: chemicals, logistics, energy

- 2024 revenue reference: ~EUR 2.5bn (cost pressure impact)

- Drought risk: higher water-treatment and capex

- Currency sensitivity: exports vs imported inputs

Product mix skew

Navigator’s product mix remains concentrated in office and printing grades—segments with slower growth compared with packaging and specialty papers—while shifting machines to packaging grades involves high capital expenditure and operational complexity. Tissue margins are compressed by rising private-label share, and limited exposure to high-barrier specialty grades reduces pricing insulation and margin resilience.

- Portfolio bias: office/printing over packaging

- Conversion cost: high CAPEX and downtime

- Tissue: private-label margin pressure

- Low specialty exposure: weaker pricing power

Iberian paper producer hit by ~30% demand drop, drought-driven capex strain

Navigator is exposed to structural UWF demand decline (global graphic paper down c.30% since 2007) and concentrated Iberian production, amplifying regional risk and logistics costs. 2024 revenue ~EUR 2.5bn faced volatile input costs and drought-driven capex/water costs. Portfolio bias to office/printing and high conversion CAPEX limits fast pivot to packaging/specialty.

| Metric | Value |

|---|---|

| 2024 revenue | ~EUR 2.5bn |

| Graphic paper decline | ~30% since 2007 |

Full Version Awaits

Navigator Company SWOT Analysis

This is the actual SWOT analysis document for Navigator Company you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report; buying unlocks the complete, editable version. You’re viewing a live preview of the exact file included in your download.

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company combines scale in pulp and paper production, strong export markets and sustainability credentials, but faces commodity cyclicality, input-cost pressures and regulatory risks. Want deeper, editable insights and strategic recommendations? Purchase the full SWOT (Word + Excel) to plan with confidence.

Strengths

Vertically integrated model

Navigator’s vertically integrated model controls ~114,000 hectares of forest and the full pulp, paper, tissue and energy chain, boosting cost visibility and supply security. Internal fiber sourcing cuts dependence on external pulp markets and supports consistent product quality and scheduling. Integration captures margin across the value chain, contributing to group revenues around €2.0bn (2024).

Certified sustainable forestry

Navigator Company holds FSC and PEFC certifications across its forest base, underpinning ESG credibility and long-term raw-material reliability.

These certifications facilitate access to premium customers and regulated EU markets, supporting higher-margin sales and supply-chain acceptance.

Sustainable forest practices reduce reputational and regulatory risk and enable participation in green finance instruments such as green bonds and sustainability-linked facilities.

Leadership in uncoated woodfree

Navigator’s leadership in uncoated woodfree paper—backed by ~1.2 Mtpa UWF capacity and 2023 revenue near €1.7bn—supports pricing power through a premium brand and quality. Scale efficiencies drive lower unit costs versus smaller rivals; a diversified customer split across office, home and professional channels stabilizes volumes. Ongoing product innovation preserves differentiation amid commoditization.

Renewable energy and bioenergy

Navigator's in-house biomass cogeneration supplies the bulk of heat and electricity needs, offsetting grid volatility and enabling surplus energy sales; in 2024 EU carbon prices averaged around €80/t, so lower carbon intensity directly protects margins under carbon pricing.

Self-generation and bioenergy exports created material ancillary revenue and improved resilience during recent European energy shocks (2022–24), reducing exposure to wholesale price spikes.

- captive cogeneration reduces grid dependence

- lower carbon intensity shields margins at ~€80/t EU ETS

- energy sales = additional revenue stream

- increases resilience in energy crises

Innovation and product breadth

R&D drives process efficiency, higher fiber yield and development of specialty grades, enabling Navigator to expand margins and product mix. Presence in tissue and value-added papers widens addressable markets and reduces exposure to commodity paper cycles. Continuous product upgrades and innovation support circularity and waste reduction across operations, reinforcing pricing power and market share defense.

- R&D-led yield and grade diversification

- Expansion into tissue/value-added papers

- Product upgrades defend price and share

- Innovation advances circularity, lowers waste

Vertically integrated pulp-paper-energy: 114k ha, €2.0bn

Navigator’s vertical integration controls ~114,000 ha and the full pulp‑paper‑energy chain, supporting 2024 group revenue ~€2.0bn and secure supply. FSC/PEFC certification underpins ESG credibility and access to premium EU markets. ~1.2 Mtpa UWF capacity, in‑house biomass cogeneration and R&D-driven grade diversification boost margins and resilience versus energy and pulp market swings (~€80/t EU ETS 2024).

| Metric | Value |

|---|---|

| Forest area | ~114,000 ha |

| Group revenue (2024) | ~€2.0bn |

| UWF capacity | ~1.2 Mtpa |

| EU ETS avg price (2024) | ~€80/t |

What is included in the product

Provides a concise SWOT analysis of Navigator Company, highlighting its market-leading pulp & paper production, strong sustainability credentials and integrated supply chain, alongside operational costs, revenue concentration and exposure to commodity cycles, and identifies growth opportunities in packaging, tissue and circular solutions plus threats from raw‑material volatility, regulatory shifts and global competition.

Provides a concise Navigator Company SWOT matrix for rapid strategic clarity, streamlining stakeholder presentations and enabling quick edits to reflect shifting market priorities.

Weaknesses

Exposure to print decline

Core uncoated woodfree (UWF) demand has been structurally pressured by digitization, with global graphic paper demand down c.30% since 2007, squeezing volumes and long‑run sales. Volume swings quickly compress mill utilization and margins given fixed-capacity mills and high conversion costs. Pricing cycles remain volatile and seasonal, tying cash flow to pulp and paper market swings. Heavy dependence on mature European markets constrains growth velocity.

Capital intensive operations

Forestry, pulping and papermaking at Navigator are highly capital intensive, requiring large upfront investment and continuous mill maintenance. High fixed costs mean margins swing sharply in downturns, amplifying earnings volatility. Major upgrade projects typically have multi-year payback horizons, tying up cash. During weak cycles balance-sheet flexibility can be constrained by sustained capex and working capital needs.

Geographic concentration

Navigator’s production and most mills are concentrated in Iberia, exposing the group to regional shocks; over 80% of its paper and pulp is exported, making local labor, regulatory or environmental disruptions highly impactful. Port congestion or logistics bottlenecks in Lisbon/Setúbal corridors can curtail shipments. Limited proximity to high‑growth APAC markets increases ocean freight costs and transit times compared with competitors with APAC hubs.

Input cost sensitivity

Despite strong bioenergy integration, Navigator remains exposed to chemical, logistics and residual energy costs that have shown volatility; in 2024 group revenue near EUR 2.5bn faced input cost spikes that at times outpaced contractual pass-throughs, compressing margins. Water-treatment and availability pressures during Iberian droughts have raised operating costs and capex needs, while EUR exchange volatility affects export unit economics and imported chemical prices.

- Input concentration: chemicals, logistics, energy

- 2024 revenue reference: ~EUR 2.5bn (cost pressure impact)

- Drought risk: higher water-treatment and capex

- Currency sensitivity: exports vs imported inputs

Product mix skew

Navigator’s product mix remains concentrated in office and printing grades—segments with slower growth compared with packaging and specialty papers—while shifting machines to packaging grades involves high capital expenditure and operational complexity. Tissue margins are compressed by rising private-label share, and limited exposure to high-barrier specialty grades reduces pricing insulation and margin resilience.

- Portfolio bias: office/printing over packaging

- Conversion cost: high CAPEX and downtime

- Tissue: private-label margin pressure

- Low specialty exposure: weaker pricing power

Iberian paper producer hit by ~30% demand drop, drought-driven capex strain

Navigator is exposed to structural UWF demand decline (global graphic paper down c.30% since 2007) and concentrated Iberian production, amplifying regional risk and logistics costs. 2024 revenue ~EUR 2.5bn faced volatile input costs and drought-driven capex/water costs. Portfolio bias to office/printing and high conversion CAPEX limits fast pivot to packaging/specialty.

| Metric | Value |

|---|---|

| 2024 revenue | ~EUR 2.5bn |

| Graphic paper decline | ~30% since 2007 |

Full Version Awaits

Navigator Company SWOT Analysis

This is the actual SWOT analysis document for Navigator Company you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report; buying unlocks the complete, editable version. You’re viewing a live preview of the exact file included in your download.

Description

Go Beyond the Preview—Access the Full Strategic Report

Navigator Company combines scale in pulp and paper production, strong export markets and sustainability credentials, but faces commodity cyclicality, input-cost pressures and regulatory risks. Want deeper, editable insights and strategic recommendations? Purchase the full SWOT (Word + Excel) to plan with confidence.

Strengths

Vertically integrated model

Navigator’s vertically integrated model controls ~114,000 hectares of forest and the full pulp, paper, tissue and energy chain, boosting cost visibility and supply security. Internal fiber sourcing cuts dependence on external pulp markets and supports consistent product quality and scheduling. Integration captures margin across the value chain, contributing to group revenues around €2.0bn (2024).

Certified sustainable forestry

Navigator Company holds FSC and PEFC certifications across its forest base, underpinning ESG credibility and long-term raw-material reliability.

These certifications facilitate access to premium customers and regulated EU markets, supporting higher-margin sales and supply-chain acceptance.

Sustainable forest practices reduce reputational and regulatory risk and enable participation in green finance instruments such as green bonds and sustainability-linked facilities.

Leadership in uncoated woodfree

Navigator’s leadership in uncoated woodfree paper—backed by ~1.2 Mtpa UWF capacity and 2023 revenue near €1.7bn—supports pricing power through a premium brand and quality. Scale efficiencies drive lower unit costs versus smaller rivals; a diversified customer split across office, home and professional channels stabilizes volumes. Ongoing product innovation preserves differentiation amid commoditization.

Renewable energy and bioenergy

Navigator's in-house biomass cogeneration supplies the bulk of heat and electricity needs, offsetting grid volatility and enabling surplus energy sales; in 2024 EU carbon prices averaged around €80/t, so lower carbon intensity directly protects margins under carbon pricing.

Self-generation and bioenergy exports created material ancillary revenue and improved resilience during recent European energy shocks (2022–24), reducing exposure to wholesale price spikes.

- captive cogeneration reduces grid dependence

- lower carbon intensity shields margins at ~€80/t EU ETS

- energy sales = additional revenue stream

- increases resilience in energy crises

Innovation and product breadth

R&D drives process efficiency, higher fiber yield and development of specialty grades, enabling Navigator to expand margins and product mix. Presence in tissue and value-added papers widens addressable markets and reduces exposure to commodity paper cycles. Continuous product upgrades and innovation support circularity and waste reduction across operations, reinforcing pricing power and market share defense.

- R&D-led yield and grade diversification

- Expansion into tissue/value-added papers

- Product upgrades defend price and share

- Innovation advances circularity, lowers waste

Vertically integrated pulp-paper-energy: 114k ha, €2.0bn

Navigator’s vertical integration controls ~114,000 ha and the full pulp‑paper‑energy chain, supporting 2024 group revenue ~€2.0bn and secure supply. FSC/PEFC certification underpins ESG credibility and access to premium EU markets. ~1.2 Mtpa UWF capacity, in‑house biomass cogeneration and R&D-driven grade diversification boost margins and resilience versus energy and pulp market swings (~€80/t EU ETS 2024).

| Metric | Value |

|---|---|

| Forest area | ~114,000 ha |

| Group revenue (2024) | ~€2.0bn |

| UWF capacity | ~1.2 Mtpa |

| EU ETS avg price (2024) | ~€80/t |

What is included in the product

Provides a concise SWOT analysis of Navigator Company, highlighting its market-leading pulp & paper production, strong sustainability credentials and integrated supply chain, alongside operational costs, revenue concentration and exposure to commodity cycles, and identifies growth opportunities in packaging, tissue and circular solutions plus threats from raw‑material volatility, regulatory shifts and global competition.

Provides a concise Navigator Company SWOT matrix for rapid strategic clarity, streamlining stakeholder presentations and enabling quick edits to reflect shifting market priorities.

Weaknesses

Exposure to print decline

Core uncoated woodfree (UWF) demand has been structurally pressured by digitization, with global graphic paper demand down c.30% since 2007, squeezing volumes and long‑run sales. Volume swings quickly compress mill utilization and margins given fixed-capacity mills and high conversion costs. Pricing cycles remain volatile and seasonal, tying cash flow to pulp and paper market swings. Heavy dependence on mature European markets constrains growth velocity.

Capital intensive operations

Forestry, pulping and papermaking at Navigator are highly capital intensive, requiring large upfront investment and continuous mill maintenance. High fixed costs mean margins swing sharply in downturns, amplifying earnings volatility. Major upgrade projects typically have multi-year payback horizons, tying up cash. During weak cycles balance-sheet flexibility can be constrained by sustained capex and working capital needs.

Geographic concentration

Navigator’s production and most mills are concentrated in Iberia, exposing the group to regional shocks; over 80% of its paper and pulp is exported, making local labor, regulatory or environmental disruptions highly impactful. Port congestion or logistics bottlenecks in Lisbon/Setúbal corridors can curtail shipments. Limited proximity to high‑growth APAC markets increases ocean freight costs and transit times compared with competitors with APAC hubs.

Input cost sensitivity

Despite strong bioenergy integration, Navigator remains exposed to chemical, logistics and residual energy costs that have shown volatility; in 2024 group revenue near EUR 2.5bn faced input cost spikes that at times outpaced contractual pass-throughs, compressing margins. Water-treatment and availability pressures during Iberian droughts have raised operating costs and capex needs, while EUR exchange volatility affects export unit economics and imported chemical prices.

- Input concentration: chemicals, logistics, energy

- 2024 revenue reference: ~EUR 2.5bn (cost pressure impact)

- Drought risk: higher water-treatment and capex

- Currency sensitivity: exports vs imported inputs

Product mix skew

Navigator’s product mix remains concentrated in office and printing grades—segments with slower growth compared with packaging and specialty papers—while shifting machines to packaging grades involves high capital expenditure and operational complexity. Tissue margins are compressed by rising private-label share, and limited exposure to high-barrier specialty grades reduces pricing insulation and margin resilience.

- Portfolio bias: office/printing over packaging

- Conversion cost: high CAPEX and downtime

- Tissue: private-label margin pressure

- Low specialty exposure: weaker pricing power

Iberian paper producer hit by ~30% demand drop, drought-driven capex strain

Navigator is exposed to structural UWF demand decline (global graphic paper down c.30% since 2007) and concentrated Iberian production, amplifying regional risk and logistics costs. 2024 revenue ~EUR 2.5bn faced volatile input costs and drought-driven capex/water costs. Portfolio bias to office/printing and high conversion CAPEX limits fast pivot to packaging/specialty.

| Metric | Value |

|---|---|

| 2024 revenue | ~EUR 2.5bn |

| Graphic paper decline | ~30% since 2007 |

Full Version Awaits

Navigator Company SWOT Analysis

This is the actual SWOT analysis document for Navigator Company you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report; buying unlocks the complete, editable version. You’re viewing a live preview of the exact file included in your download.