Phoenix Group Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

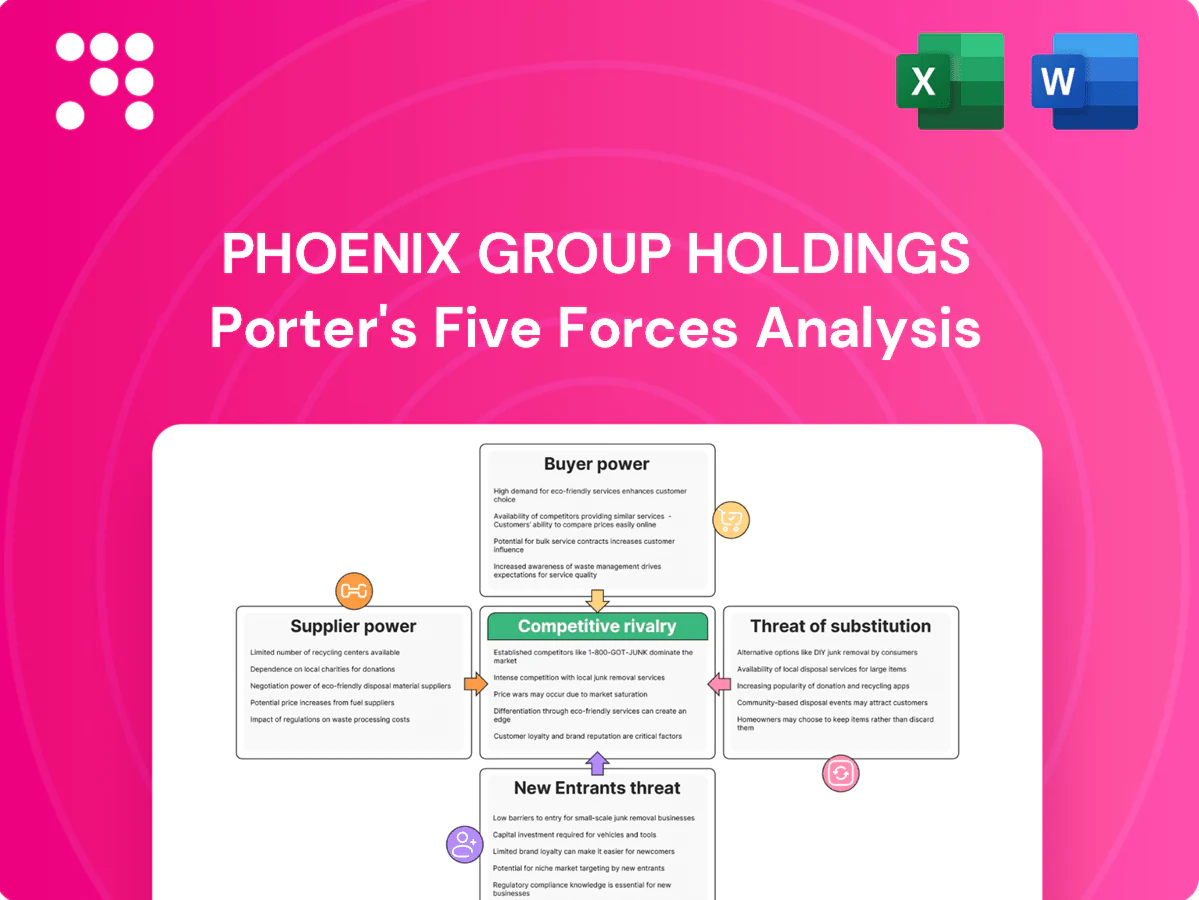

Phoenix Group Holdings faces moderate buyer power, regulatory-driven barriers to entry, and evolving substitute threats from digital insurers, while supplier influence remains limited and competitive rivalry centers on scale and distribution. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated reinsurers set terms

Longevity and mortality reinsurance is concentrated among Munich Re, Swiss Re, SCOR, Hannover Re and PartnerRe, giving these players pricing leverage. Phoenix relies on reinsurance to de-risk bulk purchase annuities and legacy liabilities. The reinsurance market hardened in 2023–24, compressing margins and tightening capacity for longevity deals. Phoenix’s scale and long-term relationships improve its negotiating position with these reinsurers.

Scarce actuarial and tech talent

Specialist actuarial, risk and data-migration skills are scarce in 2024, forcing wage inflation and extended timelines as vendor day rates rose about 15% during large projects; Phoenix, which manages c.£315bn of assets and ~10.6m policies, faces acute exposure on complex legacy integrations that heighten reliance on niche expertise. Supplier power spikes during major migrations and BPA surges; Phoenix mitigates with in-house academies and long-term vendor frameworks.

Admin and platform vendors’ switching costs

Core policy admin and investment platforms such as wrap/master trust carry high switching costs for Phoenix, with industry estimates in 2024 putting typical migration projects at £1–5m and 12–24 months due to data conversion and regulatory testing.

Vendors can leverage this lock-in to influence pricing and change windows, compressing Phoenix’s negotiating power.

Phoenix mitigates pressure by standardizing architectures and adopting multi-vendor strategies to reduce single-supplier dependency.

Capital market funding conditions

Debt investors and banks set capital costs for acquisitions and BPA collateral, and in 2024 higher interest rate backdrops (Bank of England base rate 5.25%, UK 10y gilt ~4.5%) pushed spreads and tighter covenant demands, while illiquid asset origination depends heavily on arrangers’ terms; Phoenix tempers exposure via diversified funding and internal cash generation.

Illiquid asset origination bottlenecks

Bargaining power of suppliers is heightened by illiquid asset origination bottlenecks: infrastructure debt, private credit and mortgages underpin Phoenix’s matching‑adjustment returns, while tighter supply or stricter underwriting increases arranger/manager leverage; competition from peers can bid yields higher. Phoenix reported c.£219bn assets under management at 31 Dec 2024 and uses in‑house origination plus partnerships to secure pipeline.

Supplier power squeezes longevity reinsurance pricing; vendor rates 15%

Supplier power is high in longevity reinsurance (Munich Re, Swiss Re, SCOR et al.) and illiquid origination, constraining pricing and capacity; Phoenix (AUM c.£219bn at 31 Dec 2024) mitigates with scale and in‑house origination. Specialist tech/actuarial skills pushed vendor day rates ~15% in 2024, raising switching costs. Debt markets tightened (BoE 5.25%, UK 10y ~4.5%), increasing covenant pressure.

| Supplier | Impact | 2024 datapoint |

|---|---|---|

| Reinsurers | Pricing leverage | Concentrated market |

| Specialist vendors | Cost/time inflation | ~15% day‑rate rise |

| Banks/arrangers | Tighter terms | BoE 5.25%, 10y ~4.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Phoenix Group Holdings that uncovers key competitive drivers, customer and supplier power, and barriers deterring new entrants. Identifies substitutes, emerging threats, and implications for pricing, profitability, and strategic positioning.

One-sheet Porter's Five Forces for Phoenix Group Holdings—quickly visualize insurer-specific competitive pressures with an editable radar chart and clear pressure levels for boardroom decisions.

Customers Bargaining Power

Workplace trustees and employers

Workplace trustees and large employers exert strong bargaining power, negotiating fees and service levels for master trusts and GPPs and often retendering mandates every 3–5 years, pressuring pricing.

Scheme consolidation concentrates buying power into fewer large sponsors; Phoenix, serving c.16 million customers with around £350bn of assets under administration, leverages brand, administration quality and retirement propositions to defend and retain mandates.

Bulk annuity purchasers are sophisticated

Pension scheme trustees, advised by consultants, run highly competitive bulk purchase annuity auctions where price, illiquid-asset capability and execution speed dominate covenant selection. High transparency in bids and market pricing amplifies buyer leverage, especially among large schemes (>£1bn). Phoenix leans on balance-sheet scale (around £200bn AUM in 2024), asset origination and visible pipeline to win mandates.

Advised retail customers via IFAs

IFAs and platforms act as gatekeepers, comparing charges and performance across thousands of funds, raising customers' bargaining power. Switching for open products is relatively easy, increasing price and service sensitivity. Consumer Duty, effective 31 July 2023, heightens value-for-money scrutiny. Phoenix leverages Standard Life’s distribution, service and digital tools (acquired 2018) to reduce churn.

Legacy policyholder inertia vs. regulation

Closed-book policyholder inertia reduces buyer power for Phoenix, but FCA Consumer Duty implementation (deadline July 31, 2024) and improved transfer/disclosure provisions increase mobility and complaint-driven leverage; Phoenix’s ongoing fair value reviews and heritage policyholder engagement seek to mitigate regulatory and complaint pressures.

- Inertia: closed-book dampens churn

- Regulation: Consumer Duty effective July 31, 2024

- Complaints: process increases settlement pressure

- Phoenix action: fair value reviews, heritage engagement

Price sensitivity in a high-rate environment

Higher Bank Rate (5.25% in 2024) and cash yields above 4% make cash and simple trackers attractive substitutes, elevating customer price sensitivity and fee scrutiny. Fee compression risk rises for platforms and drawdown as customers compare charges to low‑cost passive options. Customers demand clearer decumulation pathways; Phoenix refines pricing, nudges guided retirement uptake and strengthens outcomes communication.

- Bank Rate 5.25% (2024); cash yields >4%

- Elevated fee compression risk in platforms and drawdown

- Phoenix measures: pricing refinement, guided retirement nudges, clearer outcomes messaging

Trustees and big employers wield bargaining power as 5.25% Bank Rate heightens fee sensitivity

Trustees, large employers and IFAs exert strong bargaining power through retendering, fee negotiation and platform switching; Phoenix serves c.16m customers and defends mandates via brand and service. Bulk annuity auctions favour price and execution; Phoenix cites ~£200bn AUM and ~£350bn AUA (2024). Higher Bank Rate 5.25% raises fee sensitivity.

| Metric | 2024 |

|---|---|

| Customers | c.16m |

| AUM | £200bn |

| AUA | £350bn |

| Bank Rate | 5.25% |

Same Document Delivered

Phoenix Group Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Phoenix Group Holdings Porter's Five Forces analysis assesses industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressure with evidence-based scoring and implications. It is fully formatted, ready to download and use.

A Must-Have Tool for Decision-Makers

Phoenix Group Holdings faces moderate buyer power, regulatory-driven barriers to entry, and evolving substitute threats from digital insurers, while supplier influence remains limited and competitive rivalry centers on scale and distribution. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated reinsurers set terms

Longevity and mortality reinsurance is concentrated among Munich Re, Swiss Re, SCOR, Hannover Re and PartnerRe, giving these players pricing leverage. Phoenix relies on reinsurance to de-risk bulk purchase annuities and legacy liabilities. The reinsurance market hardened in 2023–24, compressing margins and tightening capacity for longevity deals. Phoenix’s scale and long-term relationships improve its negotiating position with these reinsurers.

Scarce actuarial and tech talent

Specialist actuarial, risk and data-migration skills are scarce in 2024, forcing wage inflation and extended timelines as vendor day rates rose about 15% during large projects; Phoenix, which manages c.£315bn of assets and ~10.6m policies, faces acute exposure on complex legacy integrations that heighten reliance on niche expertise. Supplier power spikes during major migrations and BPA surges; Phoenix mitigates with in-house academies and long-term vendor frameworks.

Admin and platform vendors’ switching costs

Core policy admin and investment platforms such as wrap/master trust carry high switching costs for Phoenix, with industry estimates in 2024 putting typical migration projects at £1–5m and 12–24 months due to data conversion and regulatory testing.

Vendors can leverage this lock-in to influence pricing and change windows, compressing Phoenix’s negotiating power.

Phoenix mitigates pressure by standardizing architectures and adopting multi-vendor strategies to reduce single-supplier dependency.

Capital market funding conditions

Debt investors and banks set capital costs for acquisitions and BPA collateral, and in 2024 higher interest rate backdrops (Bank of England base rate 5.25%, UK 10y gilt ~4.5%) pushed spreads and tighter covenant demands, while illiquid asset origination depends heavily on arrangers’ terms; Phoenix tempers exposure via diversified funding and internal cash generation.

Illiquid asset origination bottlenecks

Bargaining power of suppliers is heightened by illiquid asset origination bottlenecks: infrastructure debt, private credit and mortgages underpin Phoenix’s matching‑adjustment returns, while tighter supply or stricter underwriting increases arranger/manager leverage; competition from peers can bid yields higher. Phoenix reported c.£219bn assets under management at 31 Dec 2024 and uses in‑house origination plus partnerships to secure pipeline.

Supplier power squeezes longevity reinsurance pricing; vendor rates 15%

Supplier power is high in longevity reinsurance (Munich Re, Swiss Re, SCOR et al.) and illiquid origination, constraining pricing and capacity; Phoenix (AUM c.£219bn at 31 Dec 2024) mitigates with scale and in‑house origination. Specialist tech/actuarial skills pushed vendor day rates ~15% in 2024, raising switching costs. Debt markets tightened (BoE 5.25%, UK 10y ~4.5%), increasing covenant pressure.

| Supplier | Impact | 2024 datapoint |

|---|---|---|

| Reinsurers | Pricing leverage | Concentrated market |

| Specialist vendors | Cost/time inflation | ~15% day‑rate rise |

| Banks/arrangers | Tighter terms | BoE 5.25%, 10y ~4.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Phoenix Group Holdings that uncovers key competitive drivers, customer and supplier power, and barriers deterring new entrants. Identifies substitutes, emerging threats, and implications for pricing, profitability, and strategic positioning.

One-sheet Porter's Five Forces for Phoenix Group Holdings—quickly visualize insurer-specific competitive pressures with an editable radar chart and clear pressure levels for boardroom decisions.

Customers Bargaining Power

Workplace trustees and employers

Workplace trustees and large employers exert strong bargaining power, negotiating fees and service levels for master trusts and GPPs and often retendering mandates every 3–5 years, pressuring pricing.

Scheme consolidation concentrates buying power into fewer large sponsors; Phoenix, serving c.16 million customers with around £350bn of assets under administration, leverages brand, administration quality and retirement propositions to defend and retain mandates.

Bulk annuity purchasers are sophisticated

Pension scheme trustees, advised by consultants, run highly competitive bulk purchase annuity auctions where price, illiquid-asset capability and execution speed dominate covenant selection. High transparency in bids and market pricing amplifies buyer leverage, especially among large schemes (>£1bn). Phoenix leans on balance-sheet scale (around £200bn AUM in 2024), asset origination and visible pipeline to win mandates.

Advised retail customers via IFAs

IFAs and platforms act as gatekeepers, comparing charges and performance across thousands of funds, raising customers' bargaining power. Switching for open products is relatively easy, increasing price and service sensitivity. Consumer Duty, effective 31 July 2023, heightens value-for-money scrutiny. Phoenix leverages Standard Life’s distribution, service and digital tools (acquired 2018) to reduce churn.

Legacy policyholder inertia vs. regulation

Closed-book policyholder inertia reduces buyer power for Phoenix, but FCA Consumer Duty implementation (deadline July 31, 2024) and improved transfer/disclosure provisions increase mobility and complaint-driven leverage; Phoenix’s ongoing fair value reviews and heritage policyholder engagement seek to mitigate regulatory and complaint pressures.

- Inertia: closed-book dampens churn

- Regulation: Consumer Duty effective July 31, 2024

- Complaints: process increases settlement pressure

- Phoenix action: fair value reviews, heritage engagement

Price sensitivity in a high-rate environment

Higher Bank Rate (5.25% in 2024) and cash yields above 4% make cash and simple trackers attractive substitutes, elevating customer price sensitivity and fee scrutiny. Fee compression risk rises for platforms and drawdown as customers compare charges to low‑cost passive options. Customers demand clearer decumulation pathways; Phoenix refines pricing, nudges guided retirement uptake and strengthens outcomes communication.

- Bank Rate 5.25% (2024); cash yields >4%

- Elevated fee compression risk in platforms and drawdown

- Phoenix measures: pricing refinement, guided retirement nudges, clearer outcomes messaging

Trustees and big employers wield bargaining power as 5.25% Bank Rate heightens fee sensitivity

Trustees, large employers and IFAs exert strong bargaining power through retendering, fee negotiation and platform switching; Phoenix serves c.16m customers and defends mandates via brand and service. Bulk annuity auctions favour price and execution; Phoenix cites ~£200bn AUM and ~£350bn AUA (2024). Higher Bank Rate 5.25% raises fee sensitivity.

| Metric | 2024 |

|---|---|

| Customers | c.16m |

| AUM | £200bn |

| AUA | £350bn |

| Bank Rate | 5.25% |

Same Document Delivered

Phoenix Group Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Phoenix Group Holdings Porter's Five Forces analysis assesses industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressure with evidence-based scoring and implications. It is fully formatted, ready to download and use.

Description

A Must-Have Tool for Decision-Makers

Phoenix Group Holdings faces moderate buyer power, regulatory-driven barriers to entry, and evolving substitute threats from digital insurers, while supplier influence remains limited and competitive rivalry centers on scale and distribution. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated reinsurers set terms

Longevity and mortality reinsurance is concentrated among Munich Re, Swiss Re, SCOR, Hannover Re and PartnerRe, giving these players pricing leverage. Phoenix relies on reinsurance to de-risk bulk purchase annuities and legacy liabilities. The reinsurance market hardened in 2023–24, compressing margins and tightening capacity for longevity deals. Phoenix’s scale and long-term relationships improve its negotiating position with these reinsurers.

Scarce actuarial and tech talent

Specialist actuarial, risk and data-migration skills are scarce in 2024, forcing wage inflation and extended timelines as vendor day rates rose about 15% during large projects; Phoenix, which manages c.£315bn of assets and ~10.6m policies, faces acute exposure on complex legacy integrations that heighten reliance on niche expertise. Supplier power spikes during major migrations and BPA surges; Phoenix mitigates with in-house academies and long-term vendor frameworks.

Admin and platform vendors’ switching costs

Core policy admin and investment platforms such as wrap/master trust carry high switching costs for Phoenix, with industry estimates in 2024 putting typical migration projects at £1–5m and 12–24 months due to data conversion and regulatory testing.

Vendors can leverage this lock-in to influence pricing and change windows, compressing Phoenix’s negotiating power.

Phoenix mitigates pressure by standardizing architectures and adopting multi-vendor strategies to reduce single-supplier dependency.

Capital market funding conditions

Debt investors and banks set capital costs for acquisitions and BPA collateral, and in 2024 higher interest rate backdrops (Bank of England base rate 5.25%, UK 10y gilt ~4.5%) pushed spreads and tighter covenant demands, while illiquid asset origination depends heavily on arrangers’ terms; Phoenix tempers exposure via diversified funding and internal cash generation.

Illiquid asset origination bottlenecks

Bargaining power of suppliers is heightened by illiquid asset origination bottlenecks: infrastructure debt, private credit and mortgages underpin Phoenix’s matching‑adjustment returns, while tighter supply or stricter underwriting increases arranger/manager leverage; competition from peers can bid yields higher. Phoenix reported c.£219bn assets under management at 31 Dec 2024 and uses in‑house origination plus partnerships to secure pipeline.

Supplier power squeezes longevity reinsurance pricing; vendor rates 15%

Supplier power is high in longevity reinsurance (Munich Re, Swiss Re, SCOR et al.) and illiquid origination, constraining pricing and capacity; Phoenix (AUM c.£219bn at 31 Dec 2024) mitigates with scale and in‑house origination. Specialist tech/actuarial skills pushed vendor day rates ~15% in 2024, raising switching costs. Debt markets tightened (BoE 5.25%, UK 10y ~4.5%), increasing covenant pressure.

| Supplier | Impact | 2024 datapoint |

|---|---|---|

| Reinsurers | Pricing leverage | Concentrated market |

| Specialist vendors | Cost/time inflation | ~15% day‑rate rise |

| Banks/arrangers | Tighter terms | BoE 5.25%, 10y ~4.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Phoenix Group Holdings that uncovers key competitive drivers, customer and supplier power, and barriers deterring new entrants. Identifies substitutes, emerging threats, and implications for pricing, profitability, and strategic positioning.

One-sheet Porter's Five Forces for Phoenix Group Holdings—quickly visualize insurer-specific competitive pressures with an editable radar chart and clear pressure levels for boardroom decisions.

Customers Bargaining Power

Workplace trustees and employers

Workplace trustees and large employers exert strong bargaining power, negotiating fees and service levels for master trusts and GPPs and often retendering mandates every 3–5 years, pressuring pricing.

Scheme consolidation concentrates buying power into fewer large sponsors; Phoenix, serving c.16 million customers with around £350bn of assets under administration, leverages brand, administration quality and retirement propositions to defend and retain mandates.

Bulk annuity purchasers are sophisticated

Pension scheme trustees, advised by consultants, run highly competitive bulk purchase annuity auctions where price, illiquid-asset capability and execution speed dominate covenant selection. High transparency in bids and market pricing amplifies buyer leverage, especially among large schemes (>£1bn). Phoenix leans on balance-sheet scale (around £200bn AUM in 2024), asset origination and visible pipeline to win mandates.

Advised retail customers via IFAs

IFAs and platforms act as gatekeepers, comparing charges and performance across thousands of funds, raising customers' bargaining power. Switching for open products is relatively easy, increasing price and service sensitivity. Consumer Duty, effective 31 July 2023, heightens value-for-money scrutiny. Phoenix leverages Standard Life’s distribution, service and digital tools (acquired 2018) to reduce churn.

Legacy policyholder inertia vs. regulation

Closed-book policyholder inertia reduces buyer power for Phoenix, but FCA Consumer Duty implementation (deadline July 31, 2024) and improved transfer/disclosure provisions increase mobility and complaint-driven leverage; Phoenix’s ongoing fair value reviews and heritage policyholder engagement seek to mitigate regulatory and complaint pressures.

- Inertia: closed-book dampens churn

- Regulation: Consumer Duty effective July 31, 2024

- Complaints: process increases settlement pressure

- Phoenix action: fair value reviews, heritage engagement

Price sensitivity in a high-rate environment

Higher Bank Rate (5.25% in 2024) and cash yields above 4% make cash and simple trackers attractive substitutes, elevating customer price sensitivity and fee scrutiny. Fee compression risk rises for platforms and drawdown as customers compare charges to low‑cost passive options. Customers demand clearer decumulation pathways; Phoenix refines pricing, nudges guided retirement uptake and strengthens outcomes communication.

- Bank Rate 5.25% (2024); cash yields >4%

- Elevated fee compression risk in platforms and drawdown

- Phoenix measures: pricing refinement, guided retirement nudges, clearer outcomes messaging

Trustees and big employers wield bargaining power as 5.25% Bank Rate heightens fee sensitivity

Trustees, large employers and IFAs exert strong bargaining power through retendering, fee negotiation and platform switching; Phoenix serves c.16m customers and defends mandates via brand and service. Bulk annuity auctions favour price and execution; Phoenix cites ~£200bn AUM and ~£350bn AUA (2024). Higher Bank Rate 5.25% raises fee sensitivity.

| Metric | 2024 |

|---|---|

| Customers | c.16m |

| AUM | £200bn |

| AUA | £350bn |

| Bank Rate | 5.25% |

Same Document Delivered

Phoenix Group Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Phoenix Group Holdings Porter's Five Forces analysis assesses industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressure with evidence-based scoring and implications. It is fully formatted, ready to download and use.