RealReal Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

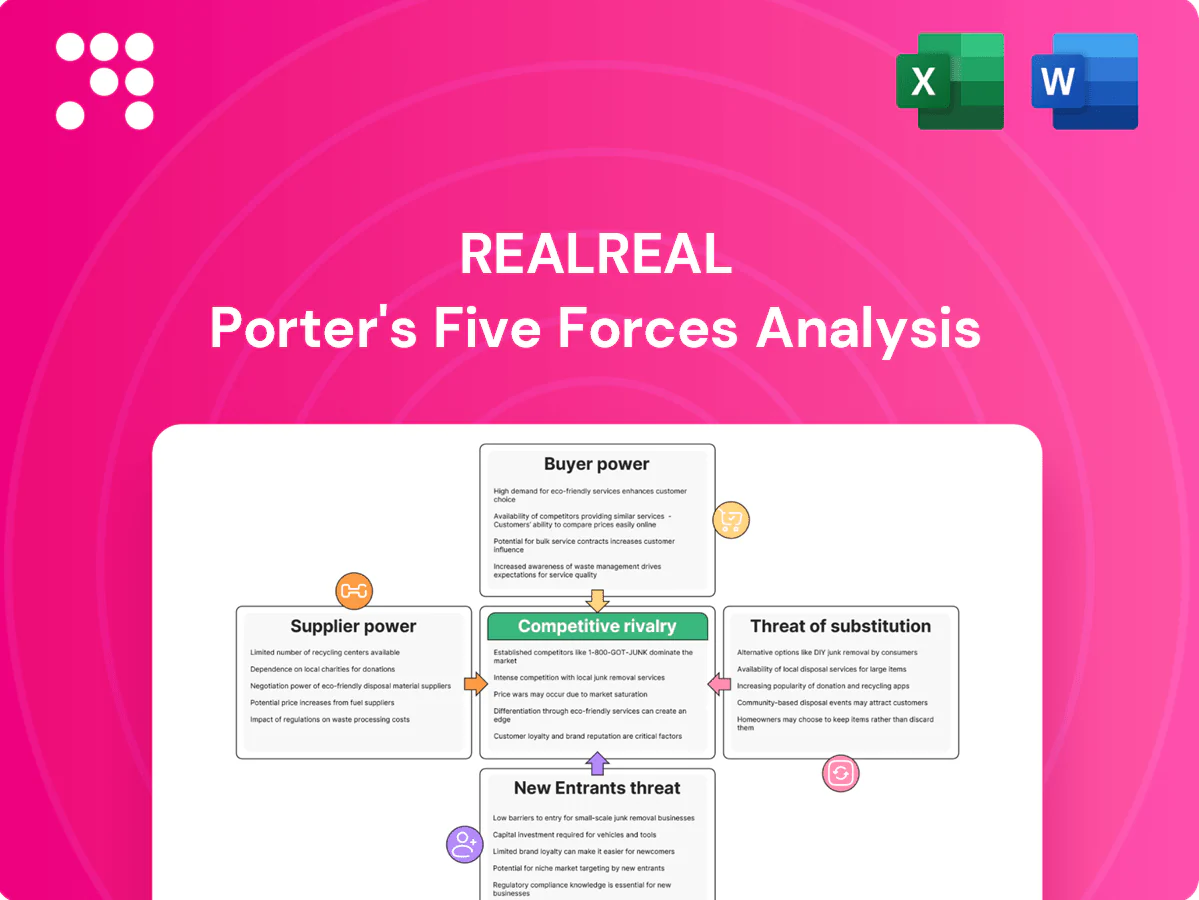

The RealReal faces moderate buyer power, growing substitute threats from peer-to-peer resale and rental platforms, supplier constraints in sourcing authenticated luxury, and intensifying rivalry with digital consignment rivals. Regulatory and platform risks add external pressure. Strategic differentiation hinges on authentication and brand partnerships. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights.

Suppliers Bargaining Power

Concentration of top consignors

High-value consignors control scarce, in-demand SKUs, giving them leverage on commission splits and service levels. A small cohort drives outsized GMV—RealReal reported $375.4 million revenue in 2023, highlighting dependence on top sellers and concentrated flows. Losing them would dent category depth and sell-through; retention programs and white-glove service aim to mitigate this concentration risk.

Limited supply of iconic luxury

True scarcity of marquee items like Hermès, Chanel and Rolex amplifies supplier clout as consignors know these goods command outsized resale value. Consignors frequently multi-home across platforms to chase better net proceeds, forcing The RealReal to offer tighter commission splits and faster payouts. The RealReal’s authentication credibility (hundreds of specialists and branded guarantees) mitigates but does not remove supplier leverage. Limited supply keeps bargaining power tilted toward consignors of marquee pieces.

Low switching costs for consignors

Consignors can list identical items on competing marketplaces with minimal friction, and rivals like Poshmark, Depop and ThredUp commonly ease onboarding with free shipping kits or instant quotes, pushing platforms to offer higher seller splits; RealReal consignor payouts typically range by service level (roughly 50–85% depending on item and seller tier). This ease of exit compresses commissions and forces faster turnaround times, while loyalty perks and concierge pickup aim to raise switching costs.

Brand-owner policies and litigation risk

Luxury brands' anti-counterfeit enforcement forces RealReal to tighten sourcing and authentication workflows, raising verification and legal-review costs and increasing supply friction. Tighter brand restrictions and litigation risk discourage some consignors and sensitive categories, shrinking available inventory and margin on disputed items. Strong authentication protocols reduce brand conflicts but add ongoing compliance burden and operational expense.

- Brand enforcement → higher verification costs

- Litigation risk → consignor deterrence

- Authentication lowers disputes but increases compliance

Alternative resale channels

Suppliers can bypass The RealReal by selling to boutiques, auction houses, peer-to-peer apps or buyout services; auction houses and specialty resellers increasingly court high-value items with seller-friendly terms, raising outside options and pressuring consignor acquisition. The RealReal must outcompete on trust, speed and net proceeds to win supply amid a resale market exceeding $120 billion globally.

- Outside options: boutiques, auctions, P2P apps, buyouts

- High-value focus: auction houses offer premium terms

- Competitive levers: trust, speed, net proceeds

Marquee consignors concentrate GMV, forcing tighter seller splits and higher verification costs

High-value consignors of marquee brands hold outsized leverage, concentrating GMV and pressuring commissions; RealReal reported $375.4M revenue in 2023, underscoring dependence on top sellers. Multi-homing and low switching costs force tighter seller splits (typical payouts ~50–85% by service level) while authentication and brand enforcement raise verification costs and constrain supply.

| Metric | Value |

|---|---|

| RealReal revenue (2023) | $375.4M |

| Global resale market | >$120B |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to The RealReal, detailing bargaining power of suppliers/buyers, threat of substitutes and entrants, and rivalry intensity with strategic implications.

A clear one-sheet Porter's Five Forces for The RealReal—instantly visualize competitive pressure with a customizable spider chart and editable pressure levels, ready to drop into pitch decks, boardroom slides or Excel dashboards.

Customers Bargaining Power

High price transparency

High price transparency lets buyers compare RealReal listings with competitors instantly, and with RealReal reporting roughly $1.0B GMV in 2024 buyers' sensitivity to commissions and fees intensifies. Visible comps force expected discounting and frequent promotions, compressing seller and platform margins. Accurate pricing algorithms and curated assortments are key defenses to preserve realized value.

Abundant multi-homing

Shoppers routinely multi-home, browsing resale and retail platforms before buying, which raises buyer bargaining power as low switching costs make price and convenience primary drivers. When listings are duplicated across sites buyers chase the best deal, pressuring margins. The RealReal's exclusive consignments and investments in faster fulfillment limit this effect by offering inventory and speed not easily matched by aggregators.

Quality and authenticity expectations

Buyers demand stringent authentication and consistent condition grading; industry reports peg the global resale market at about $82 billion in 2024, intensifying scrutiny. Any lapse weakens trust and elevates returns or disputes, pressuring platforms to bolster checks. High standards raise operating costs but help anchor pricing power. The resulting trust premium can partially offset buyer leverage.

Demand elasticity by category

Core luxury staples (Hermes, Chanel classics) show steadier demand and smaller price elasticity than trend items, which often require 20–40% markdowns to clear; RealReal mix shifts therefore drive customer bargaining power and margin pressure. Dynamic pricing must balance sell-through with margin, while bundles and point-of-sale financing reduce perceived price pain and boost conversion.

- staples: low elasticity, smaller markdowns

- trend items: high elasticity, 20–40% discounts

- dynamic pricing: sell-through vs margin trade-off

- bundles/financing: lower price sensitivity

Access to substitutes

Access to substitutes is high as consumers shift between new luxury, rentals and alternative brands, with the resale market growing about 20% YoY in 2024, pressuring take rates and seller pricing. RealReal offsets this through styling, repair and authenticity guarantees that increase seller conversion. Loyalty programs blunt pure price competition by raising repeat-purchase rates.

- Substitutes: rentals/new/alt brands

- 2024 growth: ~20% YoY

- Value-adds: styling/repair/guarantees

- Loyalty: reduces price-only churn

Transparent market: ~$1.0B GMV, $82B resale, buyers push 20-40% trend markdowns

High price transparency and ~$1.0B GMV (2024) raise buyer sensitivity to fees; visible comps force discounts. Resale market ~$82B (2024) and ~20% YoY growth increase substitutes and switching. Staples show low elasticity; trend items need 20–40% markdowns, boosting buyer bargaining power while authentication and services partly restore pricing power.

| Metric | 2024 |

|---|---|

| GMV | $1.0B |

| Market size | $82B |

| YoY growth | ~20% |

| Markdowns (trend) | 20–40% |

What You See Is What You Get

RealReal Porter's Five Forces Analysis

This preview shows the exact RealReal Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It provides a full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Purchase grants instant access to this same professionally formatted file.

Go Beyond the Preview—Access the Full Strategic Report

The RealReal faces moderate buyer power, growing substitute threats from peer-to-peer resale and rental platforms, supplier constraints in sourcing authenticated luxury, and intensifying rivalry with digital consignment rivals. Regulatory and platform risks add external pressure. Strategic differentiation hinges on authentication and brand partnerships. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights.

Suppliers Bargaining Power

Concentration of top consignors

High-value consignors control scarce, in-demand SKUs, giving them leverage on commission splits and service levels. A small cohort drives outsized GMV—RealReal reported $375.4 million revenue in 2023, highlighting dependence on top sellers and concentrated flows. Losing them would dent category depth and sell-through; retention programs and white-glove service aim to mitigate this concentration risk.

Limited supply of iconic luxury

True scarcity of marquee items like Hermès, Chanel and Rolex amplifies supplier clout as consignors know these goods command outsized resale value. Consignors frequently multi-home across platforms to chase better net proceeds, forcing The RealReal to offer tighter commission splits and faster payouts. The RealReal’s authentication credibility (hundreds of specialists and branded guarantees) mitigates but does not remove supplier leverage. Limited supply keeps bargaining power tilted toward consignors of marquee pieces.

Low switching costs for consignors

Consignors can list identical items on competing marketplaces with minimal friction, and rivals like Poshmark, Depop and ThredUp commonly ease onboarding with free shipping kits or instant quotes, pushing platforms to offer higher seller splits; RealReal consignor payouts typically range by service level (roughly 50–85% depending on item and seller tier). This ease of exit compresses commissions and forces faster turnaround times, while loyalty perks and concierge pickup aim to raise switching costs.

Brand-owner policies and litigation risk

Luxury brands' anti-counterfeit enforcement forces RealReal to tighten sourcing and authentication workflows, raising verification and legal-review costs and increasing supply friction. Tighter brand restrictions and litigation risk discourage some consignors and sensitive categories, shrinking available inventory and margin on disputed items. Strong authentication protocols reduce brand conflicts but add ongoing compliance burden and operational expense.

- Brand enforcement → higher verification costs

- Litigation risk → consignor deterrence

- Authentication lowers disputes but increases compliance

Alternative resale channels

Suppliers can bypass The RealReal by selling to boutiques, auction houses, peer-to-peer apps or buyout services; auction houses and specialty resellers increasingly court high-value items with seller-friendly terms, raising outside options and pressuring consignor acquisition. The RealReal must outcompete on trust, speed and net proceeds to win supply amid a resale market exceeding $120 billion globally.

- Outside options: boutiques, auctions, P2P apps, buyouts

- High-value focus: auction houses offer premium terms

- Competitive levers: trust, speed, net proceeds

Marquee consignors concentrate GMV, forcing tighter seller splits and higher verification costs

High-value consignors of marquee brands hold outsized leverage, concentrating GMV and pressuring commissions; RealReal reported $375.4M revenue in 2023, underscoring dependence on top sellers. Multi-homing and low switching costs force tighter seller splits (typical payouts ~50–85% by service level) while authentication and brand enforcement raise verification costs and constrain supply.

| Metric | Value |

|---|---|

| RealReal revenue (2023) | $375.4M |

| Global resale market | >$120B |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to The RealReal, detailing bargaining power of suppliers/buyers, threat of substitutes and entrants, and rivalry intensity with strategic implications.

A clear one-sheet Porter's Five Forces for The RealReal—instantly visualize competitive pressure with a customizable spider chart and editable pressure levels, ready to drop into pitch decks, boardroom slides or Excel dashboards.

Customers Bargaining Power

High price transparency

High price transparency lets buyers compare RealReal listings with competitors instantly, and with RealReal reporting roughly $1.0B GMV in 2024 buyers' sensitivity to commissions and fees intensifies. Visible comps force expected discounting and frequent promotions, compressing seller and platform margins. Accurate pricing algorithms and curated assortments are key defenses to preserve realized value.

Abundant multi-homing

Shoppers routinely multi-home, browsing resale and retail platforms before buying, which raises buyer bargaining power as low switching costs make price and convenience primary drivers. When listings are duplicated across sites buyers chase the best deal, pressuring margins. The RealReal's exclusive consignments and investments in faster fulfillment limit this effect by offering inventory and speed not easily matched by aggregators.

Quality and authenticity expectations

Buyers demand stringent authentication and consistent condition grading; industry reports peg the global resale market at about $82 billion in 2024, intensifying scrutiny. Any lapse weakens trust and elevates returns or disputes, pressuring platforms to bolster checks. High standards raise operating costs but help anchor pricing power. The resulting trust premium can partially offset buyer leverage.

Demand elasticity by category

Core luxury staples (Hermes, Chanel classics) show steadier demand and smaller price elasticity than trend items, which often require 20–40% markdowns to clear; RealReal mix shifts therefore drive customer bargaining power and margin pressure. Dynamic pricing must balance sell-through with margin, while bundles and point-of-sale financing reduce perceived price pain and boost conversion.

- staples: low elasticity, smaller markdowns

- trend items: high elasticity, 20–40% discounts

- dynamic pricing: sell-through vs margin trade-off

- bundles/financing: lower price sensitivity

Access to substitutes

Access to substitutes is high as consumers shift between new luxury, rentals and alternative brands, with the resale market growing about 20% YoY in 2024, pressuring take rates and seller pricing. RealReal offsets this through styling, repair and authenticity guarantees that increase seller conversion. Loyalty programs blunt pure price competition by raising repeat-purchase rates.

- Substitutes: rentals/new/alt brands

- 2024 growth: ~20% YoY

- Value-adds: styling/repair/guarantees

- Loyalty: reduces price-only churn

Transparent market: ~$1.0B GMV, $82B resale, buyers push 20-40% trend markdowns

High price transparency and ~$1.0B GMV (2024) raise buyer sensitivity to fees; visible comps force discounts. Resale market ~$82B (2024) and ~20% YoY growth increase substitutes and switching. Staples show low elasticity; trend items need 20–40% markdowns, boosting buyer bargaining power while authentication and services partly restore pricing power.

| Metric | 2024 |

|---|---|

| GMV | $1.0B |

| Market size | $82B |

| YoY growth | ~20% |

| Markdowns (trend) | 20–40% |

What You See Is What You Get

RealReal Porter's Five Forces Analysis

This preview shows the exact RealReal Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It provides a full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Purchase grants instant access to this same professionally formatted file.

Description

Go Beyond the Preview—Access the Full Strategic Report

The RealReal faces moderate buyer power, growing substitute threats from peer-to-peer resale and rental platforms, supplier constraints in sourcing authenticated luxury, and intensifying rivalry with digital consignment rivals. Regulatory and platform risks add external pressure. Strategic differentiation hinges on authentication and brand partnerships. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights.

Suppliers Bargaining Power

Concentration of top consignors

High-value consignors control scarce, in-demand SKUs, giving them leverage on commission splits and service levels. A small cohort drives outsized GMV—RealReal reported $375.4 million revenue in 2023, highlighting dependence on top sellers and concentrated flows. Losing them would dent category depth and sell-through; retention programs and white-glove service aim to mitigate this concentration risk.

Limited supply of iconic luxury

True scarcity of marquee items like Hermès, Chanel and Rolex amplifies supplier clout as consignors know these goods command outsized resale value. Consignors frequently multi-home across platforms to chase better net proceeds, forcing The RealReal to offer tighter commission splits and faster payouts. The RealReal’s authentication credibility (hundreds of specialists and branded guarantees) mitigates but does not remove supplier leverage. Limited supply keeps bargaining power tilted toward consignors of marquee pieces.

Low switching costs for consignors

Consignors can list identical items on competing marketplaces with minimal friction, and rivals like Poshmark, Depop and ThredUp commonly ease onboarding with free shipping kits or instant quotes, pushing platforms to offer higher seller splits; RealReal consignor payouts typically range by service level (roughly 50–85% depending on item and seller tier). This ease of exit compresses commissions and forces faster turnaround times, while loyalty perks and concierge pickup aim to raise switching costs.

Brand-owner policies and litigation risk

Luxury brands' anti-counterfeit enforcement forces RealReal to tighten sourcing and authentication workflows, raising verification and legal-review costs and increasing supply friction. Tighter brand restrictions and litigation risk discourage some consignors and sensitive categories, shrinking available inventory and margin on disputed items. Strong authentication protocols reduce brand conflicts but add ongoing compliance burden and operational expense.

- Brand enforcement → higher verification costs

- Litigation risk → consignor deterrence

- Authentication lowers disputes but increases compliance

Alternative resale channels

Suppliers can bypass The RealReal by selling to boutiques, auction houses, peer-to-peer apps or buyout services; auction houses and specialty resellers increasingly court high-value items with seller-friendly terms, raising outside options and pressuring consignor acquisition. The RealReal must outcompete on trust, speed and net proceeds to win supply amid a resale market exceeding $120 billion globally.

- Outside options: boutiques, auctions, P2P apps, buyouts

- High-value focus: auction houses offer premium terms

- Competitive levers: trust, speed, net proceeds

Marquee consignors concentrate GMV, forcing tighter seller splits and higher verification costs

High-value consignors of marquee brands hold outsized leverage, concentrating GMV and pressuring commissions; RealReal reported $375.4M revenue in 2023, underscoring dependence on top sellers. Multi-homing and low switching costs force tighter seller splits (typical payouts ~50–85% by service level) while authentication and brand enforcement raise verification costs and constrain supply.

| Metric | Value |

|---|---|

| RealReal revenue (2023) | $375.4M |

| Global resale market | >$120B |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to The RealReal, detailing bargaining power of suppliers/buyers, threat of substitutes and entrants, and rivalry intensity with strategic implications.

A clear one-sheet Porter's Five Forces for The RealReal—instantly visualize competitive pressure with a customizable spider chart and editable pressure levels, ready to drop into pitch decks, boardroom slides or Excel dashboards.

Customers Bargaining Power

High price transparency

High price transparency lets buyers compare RealReal listings with competitors instantly, and with RealReal reporting roughly $1.0B GMV in 2024 buyers' sensitivity to commissions and fees intensifies. Visible comps force expected discounting and frequent promotions, compressing seller and platform margins. Accurate pricing algorithms and curated assortments are key defenses to preserve realized value.

Abundant multi-homing

Shoppers routinely multi-home, browsing resale and retail platforms before buying, which raises buyer bargaining power as low switching costs make price and convenience primary drivers. When listings are duplicated across sites buyers chase the best deal, pressuring margins. The RealReal's exclusive consignments and investments in faster fulfillment limit this effect by offering inventory and speed not easily matched by aggregators.

Quality and authenticity expectations

Buyers demand stringent authentication and consistent condition grading; industry reports peg the global resale market at about $82 billion in 2024, intensifying scrutiny. Any lapse weakens trust and elevates returns or disputes, pressuring platforms to bolster checks. High standards raise operating costs but help anchor pricing power. The resulting trust premium can partially offset buyer leverage.

Demand elasticity by category

Core luxury staples (Hermes, Chanel classics) show steadier demand and smaller price elasticity than trend items, which often require 20–40% markdowns to clear; RealReal mix shifts therefore drive customer bargaining power and margin pressure. Dynamic pricing must balance sell-through with margin, while bundles and point-of-sale financing reduce perceived price pain and boost conversion.

- staples: low elasticity, smaller markdowns

- trend items: high elasticity, 20–40% discounts

- dynamic pricing: sell-through vs margin trade-off

- bundles/financing: lower price sensitivity

Access to substitutes

Access to substitutes is high as consumers shift between new luxury, rentals and alternative brands, with the resale market growing about 20% YoY in 2024, pressuring take rates and seller pricing. RealReal offsets this through styling, repair and authenticity guarantees that increase seller conversion. Loyalty programs blunt pure price competition by raising repeat-purchase rates.

- Substitutes: rentals/new/alt brands

- 2024 growth: ~20% YoY

- Value-adds: styling/repair/guarantees

- Loyalty: reduces price-only churn

Transparent market: ~$1.0B GMV, $82B resale, buyers push 20-40% trend markdowns

High price transparency and ~$1.0B GMV (2024) raise buyer sensitivity to fees; visible comps force discounts. Resale market ~$82B (2024) and ~20% YoY growth increase substitutes and switching. Staples show low elasticity; trend items need 20–40% markdowns, boosting buyer bargaining power while authentication and services partly restore pricing power.

| Metric | 2024 |

|---|---|

| GMV | $1.0B |

| Market size | $82B |

| YoY growth | ~20% |

| Markdowns (trend) | 20–40% |

What You See Is What You Get

RealReal Porter's Five Forces Analysis

This preview shows the exact RealReal Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It provides a full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Purchase grants instant access to this same professionally formatted file.