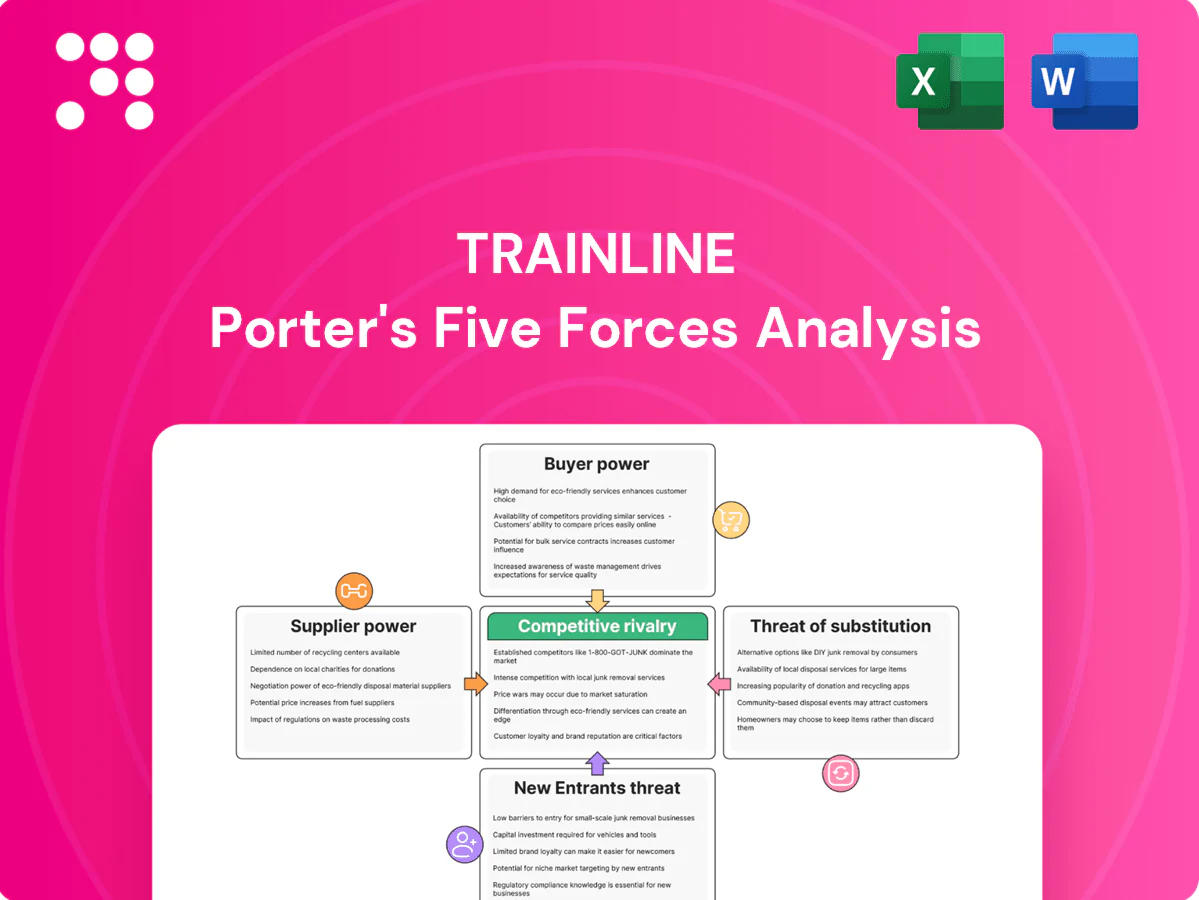

Trainline Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Trainline faces intense rivalry from integrated rail operators and OTAs, moderate buyer power from price-sensitive travelers, limited supplier leverage but rising platform integration risks, and growing substitute/threats from mobility apps and regional services. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rail and coach operators

National rail incumbents such as Govia, FirstGroup and Avanti West Coast and major coaches like FlixBus (operating in 35 countries in 2024) control essential inventory on key corridors, letting them set commercial terms and data access. This concentration raises dependency risk for an aggregator like Trainline. Trainline must balance partner relationships across markets to avoid overreliance on any single supplier.

Direct-to-consumer channels by operators

Operators' direct-to-consumer channels and loyalty apps have grown, with operator D2C share rising sharply into 2024 and reducing platform exclusivity; they can withhold promotions, limit API features or enforce parity clauses to raise leverage in fee and data talks. This strengthens supplier bargaining power versus aggregators. Trainline reported c.233m journeys in 2023 and offsets pressure by delivering incremental demand and superior UX that preserves fee and data negotiations.

Data access and technical integration power

Real-time timetables, fares and disruption feeds for Trainline are controlled by operators and infrastructure managers, with Trainline aggregating data from over 270 rail and coach operators; API standards vary and differing SLAs can limit product performance. Suppliers can prioritize their own platforms during disruptions, affecting availability for hundreds of millions of journeys annually. Robust integrations, caching and redundancy materially reduce this supplier leverage.

Commission and fee pressure

Suppliers can squeeze aggregator commissions or shift to fixed fees, while changes in fare rules, refunds and chargeback policies in 2024 moved cost and risk onto platforms, intensifying margin pressure on commoditized routes; volume commitments and value-added merchandising (ancillaries, dynamic offers) protect economics.

- Commission squeeze → fixed fees

- Fare/refund rules shift risk to platform

- Commoditized routes = margin pressure

- Volume commitments & merchandising protect margins

Regulatory and public policy influence

State-owned operators often follow public policy over pure commercial logic, and as of 2024 regulatory mandates on open data and ticketing can both limit and increase supplier leverage; compliance costs frequently pass through suppliers, slowing technical integration, while active policy engagement by Trainline can shift commercial terms toward greater interoperability.

- as of 2024: policy-led operators raise switching costs

- open-data mandates can reduce gatekeeping but add supplier compliance burden

- compliance routed via suppliers slows integrations

- engagement with regulators rebalances terms toward interoperability

Platform faces supplier leverage, margin squeeze; ancillaries and volume commitments mitigate risk

National rail incumbents and major coaches (FlixBus in 35 countries in 2024) control inventory and data, raising dependency for Trainline. Operators' D2C growth and parity clauses increased supplier leverage, despite Trainline delivering c.233m journeys in 2023 and aggregating feeds from >270 operators. Fare/refund shifts and commission→fixed-fee moves pressure margins; volume commitments and ancillaries mitigate risk.

| Metric | Value | Note |

|---|---|---|

| Journeys | c.233m | 2023 |

| Operators aggregated | >270 | 2024 |

| FlixBus footprint | 35 countries | 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Trainline uncovering key competitive drivers, buyer and supplier influence, substitutes and disruptive threats, barriers protecting incumbents, and actionable insights for pricing and profitability—fully editable for investor decks, strategy reports, or academic use.

Clear, one-sheet Porter's Five Forces for Trainline—instantly spot where competitive pressure hurts margins and where to defend pricing or expand partnerships. Duplicate scenarios for regulatory shifts or new rail entrants to guide quick, board-ready decisions.

Customers Bargaining Power

High price transparency and comparison

High price transparency lets customers compare fares, routes and schedules across apps in seconds, lowering switching costs and raising expectations for best-price guarantees. Any visible price or fee disadvantage can erode share rapidly; Trainline, which reported handling over 50 million bookings annually in 2024, must keep comprehensive coverage and clear, comparable pricing. Maintaining parity on fees is critical to retain market position.

Multi-homing and low switching costs

Multi-homing is common: users keep multiple travel apps and often book via operator-direct channels, with Trainline reporting about 10.9 million active customers in 2024; quick account setup and portable payment methods magnify buyer power over convenience and fees. Stickiness is primarily from saved preferences, stored tickets and after-sales support, which partly offsets switching but does not eliminate price sensitivity.

Sensitivity to fees and service quality

Travelers react strongly to booking fees (commonly £1–3) and ancillary costs such as seat selection (£2–10) and restrictive refund rules, which increase churn. Service during disruptions, real-time updates and responsive customer support drive repeat usage and can offset price sensitivity. Poor incident handling pushes users to alternatives, while superior post‑booking care reduces fee-driven switching.

Corporate and frequent traveler leverage

Corporate and frequent-traveler segments deliver high lifetime value for Trainline; in 2024 the company highlighted business accounts and subscriptions as strategic growth drivers, with these customers able to negotiate rates, features, and service levels, and their loss disproportionately harming unit economics.

- High-LTV segments drive revenue stability

- Negotiate rates, service tiers, SLAs

- Churn hits margins disproportionately

- Dashboards, invoicing, policy tools cut churn

Ratings, reviews, and social proof

Public ratings and reviews sharply amplify buyer influence on Trainline: BrightLocal 2024 found 79% of consumers trust online reviews as much as personal recommendations, so service failures propagate rapidly across platforms and depress bookings; conversely positive advocacy reduces acquisition cost while negative sentiment raises it. Proactive communication and clear refund/exchange policies have been shown to temper buyer power by limiting review escalation.

- Ratings affect trust: 79% trust reviews (BrightLocal 2024)

- Service failures spread fast across social channels

- Positive advocacy lowers CAC; negative raises it

- Transparent policies and proactive comms reduce churn

Low fees boost buyer power — 50M+ bookings, 79% trust

High fare transparency and low switching costs amplify buyer power; Trainline handled over 50 million bookings and ~10.9 million active customers in 2024, so visible price/fee gaps quickly erode share. Small booking fees (£1–3) and ancillaries (£2–10) drive churn, while strong disruption handling and B2B accounts (higher LTV) reduce sensitivity. Online reviews (79% trust) magnify effects.

| Metric | 2024 |

|---|---|

| Bookings | 50M+ |

| Active customers | 10.9M |

| Booking fee | £1–3 |

| Seat/ancillary | £2–10 |

| Trust in reviews | 79% |

Preview Before You Purchase

Trainline Porter's Five Forces Analysis

This preview shows the exact Trainline Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file displayed is fully formatted, professionally written, and ready to download and use the moment you complete payment. What you see is what you get.

From Overview to Strategy Blueprint

Trainline faces intense rivalry from integrated rail operators and OTAs, moderate buyer power from price-sensitive travelers, limited supplier leverage but rising platform integration risks, and growing substitute/threats from mobility apps and regional services. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rail and coach operators

National rail incumbents such as Govia, FirstGroup and Avanti West Coast and major coaches like FlixBus (operating in 35 countries in 2024) control essential inventory on key corridors, letting them set commercial terms and data access. This concentration raises dependency risk for an aggregator like Trainline. Trainline must balance partner relationships across markets to avoid overreliance on any single supplier.

Direct-to-consumer channels by operators

Operators' direct-to-consumer channels and loyalty apps have grown, with operator D2C share rising sharply into 2024 and reducing platform exclusivity; they can withhold promotions, limit API features or enforce parity clauses to raise leverage in fee and data talks. This strengthens supplier bargaining power versus aggregators. Trainline reported c.233m journeys in 2023 and offsets pressure by delivering incremental demand and superior UX that preserves fee and data negotiations.

Data access and technical integration power

Real-time timetables, fares and disruption feeds for Trainline are controlled by operators and infrastructure managers, with Trainline aggregating data from over 270 rail and coach operators; API standards vary and differing SLAs can limit product performance. Suppliers can prioritize their own platforms during disruptions, affecting availability for hundreds of millions of journeys annually. Robust integrations, caching and redundancy materially reduce this supplier leverage.

Commission and fee pressure

Suppliers can squeeze aggregator commissions or shift to fixed fees, while changes in fare rules, refunds and chargeback policies in 2024 moved cost and risk onto platforms, intensifying margin pressure on commoditized routes; volume commitments and value-added merchandising (ancillaries, dynamic offers) protect economics.

- Commission squeeze → fixed fees

- Fare/refund rules shift risk to platform

- Commoditized routes = margin pressure

- Volume commitments & merchandising protect margins

Regulatory and public policy influence

State-owned operators often follow public policy over pure commercial logic, and as of 2024 regulatory mandates on open data and ticketing can both limit and increase supplier leverage; compliance costs frequently pass through suppliers, slowing technical integration, while active policy engagement by Trainline can shift commercial terms toward greater interoperability.

- as of 2024: policy-led operators raise switching costs

- open-data mandates can reduce gatekeeping but add supplier compliance burden

- compliance routed via suppliers slows integrations

- engagement with regulators rebalances terms toward interoperability

Platform faces supplier leverage, margin squeeze; ancillaries and volume commitments mitigate risk

National rail incumbents and major coaches (FlixBus in 35 countries in 2024) control inventory and data, raising dependency for Trainline. Operators' D2C growth and parity clauses increased supplier leverage, despite Trainline delivering c.233m journeys in 2023 and aggregating feeds from >270 operators. Fare/refund shifts and commission→fixed-fee moves pressure margins; volume commitments and ancillaries mitigate risk.

| Metric | Value | Note |

|---|---|---|

| Journeys | c.233m | 2023 |

| Operators aggregated | >270 | 2024 |

| FlixBus footprint | 35 countries | 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Trainline uncovering key competitive drivers, buyer and supplier influence, substitutes and disruptive threats, barriers protecting incumbents, and actionable insights for pricing and profitability—fully editable for investor decks, strategy reports, or academic use.

Clear, one-sheet Porter's Five Forces for Trainline—instantly spot where competitive pressure hurts margins and where to defend pricing or expand partnerships. Duplicate scenarios for regulatory shifts or new rail entrants to guide quick, board-ready decisions.

Customers Bargaining Power

High price transparency and comparison

High price transparency lets customers compare fares, routes and schedules across apps in seconds, lowering switching costs and raising expectations for best-price guarantees. Any visible price or fee disadvantage can erode share rapidly; Trainline, which reported handling over 50 million bookings annually in 2024, must keep comprehensive coverage and clear, comparable pricing. Maintaining parity on fees is critical to retain market position.

Multi-homing and low switching costs

Multi-homing is common: users keep multiple travel apps and often book via operator-direct channels, with Trainline reporting about 10.9 million active customers in 2024; quick account setup and portable payment methods magnify buyer power over convenience and fees. Stickiness is primarily from saved preferences, stored tickets and after-sales support, which partly offsets switching but does not eliminate price sensitivity.

Sensitivity to fees and service quality

Travelers react strongly to booking fees (commonly £1–3) and ancillary costs such as seat selection (£2–10) and restrictive refund rules, which increase churn. Service during disruptions, real-time updates and responsive customer support drive repeat usage and can offset price sensitivity. Poor incident handling pushes users to alternatives, while superior post‑booking care reduces fee-driven switching.

Corporate and frequent traveler leverage

Corporate and frequent-traveler segments deliver high lifetime value for Trainline; in 2024 the company highlighted business accounts and subscriptions as strategic growth drivers, with these customers able to negotiate rates, features, and service levels, and their loss disproportionately harming unit economics.

- High-LTV segments drive revenue stability

- Negotiate rates, service tiers, SLAs

- Churn hits margins disproportionately

- Dashboards, invoicing, policy tools cut churn

Ratings, reviews, and social proof

Public ratings and reviews sharply amplify buyer influence on Trainline: BrightLocal 2024 found 79% of consumers trust online reviews as much as personal recommendations, so service failures propagate rapidly across platforms and depress bookings; conversely positive advocacy reduces acquisition cost while negative sentiment raises it. Proactive communication and clear refund/exchange policies have been shown to temper buyer power by limiting review escalation.

- Ratings affect trust: 79% trust reviews (BrightLocal 2024)

- Service failures spread fast across social channels

- Positive advocacy lowers CAC; negative raises it

- Transparent policies and proactive comms reduce churn

Low fees boost buyer power — 50M+ bookings, 79% trust

High fare transparency and low switching costs amplify buyer power; Trainline handled over 50 million bookings and ~10.9 million active customers in 2024, so visible price/fee gaps quickly erode share. Small booking fees (£1–3) and ancillaries (£2–10) drive churn, while strong disruption handling and B2B accounts (higher LTV) reduce sensitivity. Online reviews (79% trust) magnify effects.

| Metric | 2024 |

|---|---|

| Bookings | 50M+ |

| Active customers | 10.9M |

| Booking fee | £1–3 |

| Seat/ancillary | £2–10 |

| Trust in reviews | 79% |

Preview Before You Purchase

Trainline Porter's Five Forces Analysis

This preview shows the exact Trainline Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file displayed is fully formatted, professionally written, and ready to download and use the moment you complete payment. What you see is what you get.

Description

From Overview to Strategy Blueprint

Trainline faces intense rivalry from integrated rail operators and OTAs, moderate buyer power from price-sensitive travelers, limited supplier leverage but rising platform integration risks, and growing substitute/threats from mobility apps and regional services. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rail and coach operators

National rail incumbents such as Govia, FirstGroup and Avanti West Coast and major coaches like FlixBus (operating in 35 countries in 2024) control essential inventory on key corridors, letting them set commercial terms and data access. This concentration raises dependency risk for an aggregator like Trainline. Trainline must balance partner relationships across markets to avoid overreliance on any single supplier.

Direct-to-consumer channels by operators

Operators' direct-to-consumer channels and loyalty apps have grown, with operator D2C share rising sharply into 2024 and reducing platform exclusivity; they can withhold promotions, limit API features or enforce parity clauses to raise leverage in fee and data talks. This strengthens supplier bargaining power versus aggregators. Trainline reported c.233m journeys in 2023 and offsets pressure by delivering incremental demand and superior UX that preserves fee and data negotiations.

Data access and technical integration power

Real-time timetables, fares and disruption feeds for Trainline are controlled by operators and infrastructure managers, with Trainline aggregating data from over 270 rail and coach operators; API standards vary and differing SLAs can limit product performance. Suppliers can prioritize their own platforms during disruptions, affecting availability for hundreds of millions of journeys annually. Robust integrations, caching and redundancy materially reduce this supplier leverage.

Commission and fee pressure

Suppliers can squeeze aggregator commissions or shift to fixed fees, while changes in fare rules, refunds and chargeback policies in 2024 moved cost and risk onto platforms, intensifying margin pressure on commoditized routes; volume commitments and value-added merchandising (ancillaries, dynamic offers) protect economics.

- Commission squeeze → fixed fees

- Fare/refund rules shift risk to platform

- Commoditized routes = margin pressure

- Volume commitments & merchandising protect margins

Regulatory and public policy influence

State-owned operators often follow public policy over pure commercial logic, and as of 2024 regulatory mandates on open data and ticketing can both limit and increase supplier leverage; compliance costs frequently pass through suppliers, slowing technical integration, while active policy engagement by Trainline can shift commercial terms toward greater interoperability.

- as of 2024: policy-led operators raise switching costs

- open-data mandates can reduce gatekeeping but add supplier compliance burden

- compliance routed via suppliers slows integrations

- engagement with regulators rebalances terms toward interoperability

Platform faces supplier leverage, margin squeeze; ancillaries and volume commitments mitigate risk

National rail incumbents and major coaches (FlixBus in 35 countries in 2024) control inventory and data, raising dependency for Trainline. Operators' D2C growth and parity clauses increased supplier leverage, despite Trainline delivering c.233m journeys in 2023 and aggregating feeds from >270 operators. Fare/refund shifts and commission→fixed-fee moves pressure margins; volume commitments and ancillaries mitigate risk.

| Metric | Value | Note |

|---|---|---|

| Journeys | c.233m | 2023 |

| Operators aggregated | >270 | 2024 |

| FlixBus footprint | 35 countries | 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Trainline uncovering key competitive drivers, buyer and supplier influence, substitutes and disruptive threats, barriers protecting incumbents, and actionable insights for pricing and profitability—fully editable for investor decks, strategy reports, or academic use.

Clear, one-sheet Porter's Five Forces for Trainline—instantly spot where competitive pressure hurts margins and where to defend pricing or expand partnerships. Duplicate scenarios for regulatory shifts or new rail entrants to guide quick, board-ready decisions.

Customers Bargaining Power

High price transparency and comparison

High price transparency lets customers compare fares, routes and schedules across apps in seconds, lowering switching costs and raising expectations for best-price guarantees. Any visible price or fee disadvantage can erode share rapidly; Trainline, which reported handling over 50 million bookings annually in 2024, must keep comprehensive coverage and clear, comparable pricing. Maintaining parity on fees is critical to retain market position.

Multi-homing and low switching costs

Multi-homing is common: users keep multiple travel apps and often book via operator-direct channels, with Trainline reporting about 10.9 million active customers in 2024; quick account setup and portable payment methods magnify buyer power over convenience and fees. Stickiness is primarily from saved preferences, stored tickets and after-sales support, which partly offsets switching but does not eliminate price sensitivity.

Sensitivity to fees and service quality

Travelers react strongly to booking fees (commonly £1–3) and ancillary costs such as seat selection (£2–10) and restrictive refund rules, which increase churn. Service during disruptions, real-time updates and responsive customer support drive repeat usage and can offset price sensitivity. Poor incident handling pushes users to alternatives, while superior post‑booking care reduces fee-driven switching.

Corporate and frequent traveler leverage

Corporate and frequent-traveler segments deliver high lifetime value for Trainline; in 2024 the company highlighted business accounts and subscriptions as strategic growth drivers, with these customers able to negotiate rates, features, and service levels, and their loss disproportionately harming unit economics.

- High-LTV segments drive revenue stability

- Negotiate rates, service tiers, SLAs

- Churn hits margins disproportionately

- Dashboards, invoicing, policy tools cut churn

Ratings, reviews, and social proof

Public ratings and reviews sharply amplify buyer influence on Trainline: BrightLocal 2024 found 79% of consumers trust online reviews as much as personal recommendations, so service failures propagate rapidly across platforms and depress bookings; conversely positive advocacy reduces acquisition cost while negative sentiment raises it. Proactive communication and clear refund/exchange policies have been shown to temper buyer power by limiting review escalation.

- Ratings affect trust: 79% trust reviews (BrightLocal 2024)

- Service failures spread fast across social channels

- Positive advocacy lowers CAC; negative raises it

- Transparent policies and proactive comms reduce churn

Low fees boost buyer power — 50M+ bookings, 79% trust

High fare transparency and low switching costs amplify buyer power; Trainline handled over 50 million bookings and ~10.9 million active customers in 2024, so visible price/fee gaps quickly erode share. Small booking fees (£1–3) and ancillaries (£2–10) drive churn, while strong disruption handling and B2B accounts (higher LTV) reduce sensitivity. Online reviews (79% trust) magnify effects.

| Metric | 2024 |

|---|---|

| Bookings | 50M+ |

| Active customers | 10.9M |

| Booking fee | £1–3 |

| Seat/ancillary | £2–10 |

| Trust in reviews | 79% |

Preview Before You Purchase

Trainline Porter's Five Forces Analysis

This preview shows the exact Trainline Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file displayed is fully formatted, professionally written, and ready to download and use the moment you complete payment. What you see is what you get.