Vita Coco Porter's Five Forces Analysis

From Overview to Strategy Blueprint

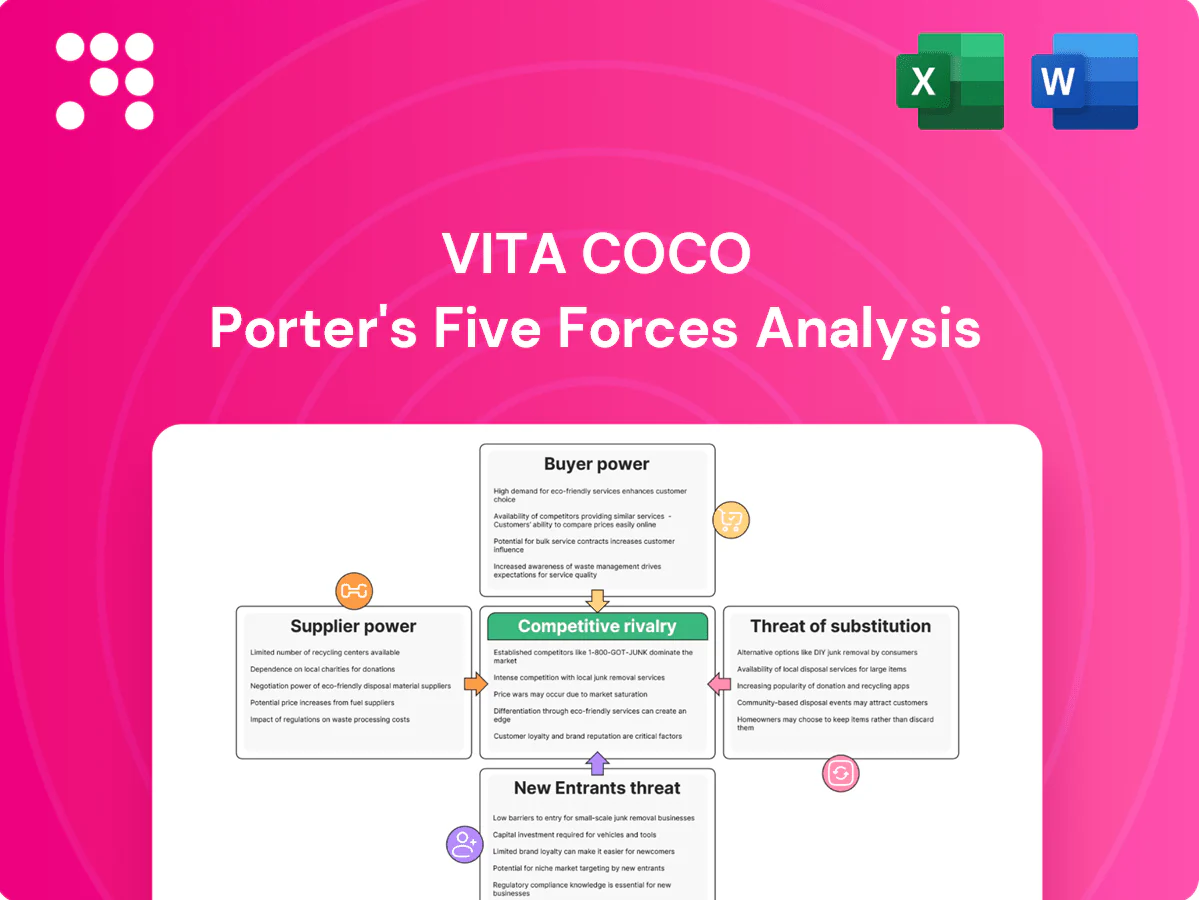

Vita Coco faces moderate supplier power, intense rivalry from established beverage brands, growing buyer sophistication, low but rising threat of substitutes, and barriers that deter some entrants but not innovators. This snapshot highlights key dynamics shaping margins and growth potential. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated coconut sourcing regions

Coconut water sourcing is highly concentrated in tropical hubs—Indonesia and the Philippines together account for over 50% of global coconut production (FAO 2022), with Brazil and Sri Lanka important regional suppliers. Weather shocks and El Niño episodes (eg 2015–16) and plant disease have historically tightened supply and raised input pressure. When harvests swing, growers gain leverage over volumes and contract terms. Diversifying origins and multi‑year contracts mitigate but do not eliminate these constraints.

Quality and specification dependency

Vita Coco’s premium taste, sweetness profile, and strict microbiological specs narrow acceptable coconut sources, making suppliers less interchangeable and elevating bargaining power for qualified processors; the global coconut water market was valued at about $5.4 billion in 2024, intensifying demand for certified supply. Certification requirements like organic and fair trade further shrink the supplier pool, empowering certified co-packers. Tight QA and yearly audits reduce risk but increase switching costs for Vita Coco due to limited qualified partners.

Packaging and input volatility

Dependence on cartons, cans, caps and resins ties Vita Coco to a small set of global packaging firms, increasing supplier bargaining power; commodity swings and container freight volatility during 2021–2023 highlighted how quickly input costs can shift supplier leverage. Long-term supply agreements and multi-sourcing have reduced but not eliminated disruption risk. Sustainability targets for recyclable packaging narrow qualified vendors and can raise costs.

Logistics and port dependencies

Ocean shipping concentration—major alliances controlling roughly 80% of container capacity—gives carriers and forwarders outsized leverage in tight 2024 capacity cycles; port congestion and regulatory delays materially raise landed costs and extend lead times, while suppliers with integrated logistics or port proximity secure better terms; Vita Coco and peers use 60–90 day inventory buffers to partly offset timing risks.

- Alliances control ~80% of container capacity (2024)

- Port congestion increases landed cost and lead times

- Integrated logistics/proximity = stronger commercial terms

- Typical strategic buffers: 60–90 days inventory

Countervailing brand scale

Vita Coco’s category leadership and predictable, year-round demand give suppliers stable multi-million-case volume commitments in 2024, enabling priority allocations and negotiated price concessions.

Co-investments in processing capacity and farmer programs in key sourcing regions align incentives, lowering input cost volatility and gradually reducing supplier power versus arrangements with smaller brands.

- 2024: category leadership drives volume stability

- Priority allocations and price concessions

- Co-investment in capacity and farmer programs

- Supplier power erosion vis-à-vis smaller brands

Coconut supply (50%+) and carriers (~80%) amplify input-cost risk

Suppliers hold elevated leverage: concentrated coconut supply (Indonesia+Philippines >50% production) and strict quality/certification needs make qualified sources scarce, raising switching costs and prices. Packaging and shipping concentration (carriers ~80% capacity) amplify input cost volatility; Vita Coco offsets with 60–90 day buffers and long-term contracts. Co-investments and volume commitments partly dilute supplier power versus smaller brands.

| Metric | 2024 |

|---|---|

| Coconut supply concentration | Indonesia+Philippines >50% |

| Global coconut water market | $5.4B |

| Container capacity control | ~80% |

| Inventory buffer | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis of Vita Coco uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to defend market share and profitability.

A concise, one-sheet Porter's Five Forces for Vita Coco that instantly highlights supplier, buyer, and competitive pressures—ideal for quick strategic decisions and pitch decks. Customize ratings, swap data, and view a spider chart to relieve analysis bottlenecks without any complex setup.

Customers Bargaining Power

Large retail consolidators

Mass retailers, club stores and national grocers control shelf access and wield outsized leverage—Walmart accounted for roughly 25% of US grocery sales in 2024 and Kroger about 10%—so they press suppliers for lower prices, promo funding and extended payment terms (often 60–120 days). Slotting fees and resets can cost tens to hundreds of thousands per SKU, heightening dependence on key accounts; Vita Coco’s high velocity mitigates risk but buyer power stays strong.

Low switching costs for consumers

Coconut water and functional beverages are easily substituted at point of sale, so shoppers switch brands on price, flavor or promotion with minimal friction, pressuring margins and forcing sustained marketing; the global coconut water market is forecast to grow at roughly 8% CAGR through 2030, increasing competitive intensity. Brand equity and Vita Coco’s leading U.S. position partially blunt this power via taste consistency and distribution advantages.

Private label and owned brands

Retailers introducing private-label coconut water anchor price points and increase price sensitivity, with private-label penetration exceeding 40% in the UK and around 20% in the US, compressing category premiums. Such options erode Vita Coco’s brand power and raise trade-down risk during macro slowdowns. Vita Coco must reinforce quality, sourcing transparency, and product innovation to defend margins and share.

Omnichannel transparency

Omnichannel transparency lets shoppers compare Vita Coco prices and reviews across e-commerce, marketplaces and delivery apps, boosting buyer leverage; U.S. e-commerce was about 18% of retail sales in 2024 (eMarketer), increasing price visibility. Dynamic pricing and frequent promotions set consumer expectations for deals, while DTC channels improve margins and first-party data even though retail still holds scale. Assortment curation online alters product visibility and conversion rates.

- Omnichannel price visibility: raises bargaining power

- DTC: higher margins + data but smaller scale vs retail

- Promotions/dynamic pricing: normalize deal expectations

- Assortment curation: controls search visibility and sales

Foodservice and convenience mix

Distributors and chain operators press for consistent supply, margin cushions and rebate programs, giving buyers leverage; package-size mix and cold-chain shelf placement materially affect SKU throughput and shrink. Vita Coco’s presence across grocery, convenience and foodservice—sold in 30+ countries—diversifies exposure, yet volume concentration in top accounts still amplifies buyer influence.

- Buyers: seek supply, margins, rebates

- Throughput: package size + cold-chain crucial

- Channel breadth: grocery, convenience, foodservice

- Risk: top-account volume concentration

Retail giants squeeze coconut-water margins as private label and promos heighten price pressure

Mass retailers (Walmart ~25% US grocery sales 2024; Kroger ~10%) exert strong leverage on Vita Coco, forcing price, promo and payment concessions. Easy substitution, private-label (UK >40%, US ~20%) and promotions (e‑commerce ~18% of retail 2024) increase price sensitivity despite Vita Coco's scale. Diversified channels help but top-account concentration keeps buyer power elevated.

| Metric | 2024 figure |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| E‑commerce retail | ~18% |

| Private‑label penetration | UK >40% / US ~20% |

| Coconut water market CAGR | ~8% to 2030 |

Full Version Awaits

Vita Coco Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Vita Coco Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, with industry-specific data, implications and strategic recommendations. It's the final, fully formatted deliverable ready for immediate download and use.

From Overview to Strategy Blueprint

Vita Coco faces moderate supplier power, intense rivalry from established beverage brands, growing buyer sophistication, low but rising threat of substitutes, and barriers that deter some entrants but not innovators. This snapshot highlights key dynamics shaping margins and growth potential. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated coconut sourcing regions

Coconut water sourcing is highly concentrated in tropical hubs—Indonesia and the Philippines together account for over 50% of global coconut production (FAO 2022), with Brazil and Sri Lanka important regional suppliers. Weather shocks and El Niño episodes (eg 2015–16) and plant disease have historically tightened supply and raised input pressure. When harvests swing, growers gain leverage over volumes and contract terms. Diversifying origins and multi‑year contracts mitigate but do not eliminate these constraints.

Quality and specification dependency

Vita Coco’s premium taste, sweetness profile, and strict microbiological specs narrow acceptable coconut sources, making suppliers less interchangeable and elevating bargaining power for qualified processors; the global coconut water market was valued at about $5.4 billion in 2024, intensifying demand for certified supply. Certification requirements like organic and fair trade further shrink the supplier pool, empowering certified co-packers. Tight QA and yearly audits reduce risk but increase switching costs for Vita Coco due to limited qualified partners.

Packaging and input volatility

Dependence on cartons, cans, caps and resins ties Vita Coco to a small set of global packaging firms, increasing supplier bargaining power; commodity swings and container freight volatility during 2021–2023 highlighted how quickly input costs can shift supplier leverage. Long-term supply agreements and multi-sourcing have reduced but not eliminated disruption risk. Sustainability targets for recyclable packaging narrow qualified vendors and can raise costs.

Logistics and port dependencies

Ocean shipping concentration—major alliances controlling roughly 80% of container capacity—gives carriers and forwarders outsized leverage in tight 2024 capacity cycles; port congestion and regulatory delays materially raise landed costs and extend lead times, while suppliers with integrated logistics or port proximity secure better terms; Vita Coco and peers use 60–90 day inventory buffers to partly offset timing risks.

- Alliances control ~80% of container capacity (2024)

- Port congestion increases landed cost and lead times

- Integrated logistics/proximity = stronger commercial terms

- Typical strategic buffers: 60–90 days inventory

Countervailing brand scale

Vita Coco’s category leadership and predictable, year-round demand give suppliers stable multi-million-case volume commitments in 2024, enabling priority allocations and negotiated price concessions.

Co-investments in processing capacity and farmer programs in key sourcing regions align incentives, lowering input cost volatility and gradually reducing supplier power versus arrangements with smaller brands.

- 2024: category leadership drives volume stability

- Priority allocations and price concessions

- Co-investment in capacity and farmer programs

- Supplier power erosion vis-à-vis smaller brands

Coconut supply (50%+) and carriers (~80%) amplify input-cost risk

Suppliers hold elevated leverage: concentrated coconut supply (Indonesia+Philippines >50% production) and strict quality/certification needs make qualified sources scarce, raising switching costs and prices. Packaging and shipping concentration (carriers ~80% capacity) amplify input cost volatility; Vita Coco offsets with 60–90 day buffers and long-term contracts. Co-investments and volume commitments partly dilute supplier power versus smaller brands.

| Metric | 2024 |

|---|---|

| Coconut supply concentration | Indonesia+Philippines >50% |

| Global coconut water market | $5.4B |

| Container capacity control | ~80% |

| Inventory buffer | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis of Vita Coco uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to defend market share and profitability.

A concise, one-sheet Porter's Five Forces for Vita Coco that instantly highlights supplier, buyer, and competitive pressures—ideal for quick strategic decisions and pitch decks. Customize ratings, swap data, and view a spider chart to relieve analysis bottlenecks without any complex setup.

Customers Bargaining Power

Large retail consolidators

Mass retailers, club stores and national grocers control shelf access and wield outsized leverage—Walmart accounted for roughly 25% of US grocery sales in 2024 and Kroger about 10%—so they press suppliers for lower prices, promo funding and extended payment terms (often 60–120 days). Slotting fees and resets can cost tens to hundreds of thousands per SKU, heightening dependence on key accounts; Vita Coco’s high velocity mitigates risk but buyer power stays strong.

Low switching costs for consumers

Coconut water and functional beverages are easily substituted at point of sale, so shoppers switch brands on price, flavor or promotion with minimal friction, pressuring margins and forcing sustained marketing; the global coconut water market is forecast to grow at roughly 8% CAGR through 2030, increasing competitive intensity. Brand equity and Vita Coco’s leading U.S. position partially blunt this power via taste consistency and distribution advantages.

Private label and owned brands

Retailers introducing private-label coconut water anchor price points and increase price sensitivity, with private-label penetration exceeding 40% in the UK and around 20% in the US, compressing category premiums. Such options erode Vita Coco’s brand power and raise trade-down risk during macro slowdowns. Vita Coco must reinforce quality, sourcing transparency, and product innovation to defend margins and share.

Omnichannel transparency

Omnichannel transparency lets shoppers compare Vita Coco prices and reviews across e-commerce, marketplaces and delivery apps, boosting buyer leverage; U.S. e-commerce was about 18% of retail sales in 2024 (eMarketer), increasing price visibility. Dynamic pricing and frequent promotions set consumer expectations for deals, while DTC channels improve margins and first-party data even though retail still holds scale. Assortment curation online alters product visibility and conversion rates.

- Omnichannel price visibility: raises bargaining power

- DTC: higher margins + data but smaller scale vs retail

- Promotions/dynamic pricing: normalize deal expectations

- Assortment curation: controls search visibility and sales

Foodservice and convenience mix

Distributors and chain operators press for consistent supply, margin cushions and rebate programs, giving buyers leverage; package-size mix and cold-chain shelf placement materially affect SKU throughput and shrink. Vita Coco’s presence across grocery, convenience and foodservice—sold in 30+ countries—diversifies exposure, yet volume concentration in top accounts still amplifies buyer influence.

- Buyers: seek supply, margins, rebates

- Throughput: package size + cold-chain crucial

- Channel breadth: grocery, convenience, foodservice

- Risk: top-account volume concentration

Retail giants squeeze coconut-water margins as private label and promos heighten price pressure

Mass retailers (Walmart ~25% US grocery sales 2024; Kroger ~10%) exert strong leverage on Vita Coco, forcing price, promo and payment concessions. Easy substitution, private-label (UK >40%, US ~20%) and promotions (e‑commerce ~18% of retail 2024) increase price sensitivity despite Vita Coco's scale. Diversified channels help but top-account concentration keeps buyer power elevated.

| Metric | 2024 figure |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| E‑commerce retail | ~18% |

| Private‑label penetration | UK >40% / US ~20% |

| Coconut water market CAGR | ~8% to 2030 |

Full Version Awaits

Vita Coco Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Vita Coco Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, with industry-specific data, implications and strategic recommendations. It's the final, fully formatted deliverable ready for immediate download and use.

Description

From Overview to Strategy Blueprint

Vita Coco faces moderate supplier power, intense rivalry from established beverage brands, growing buyer sophistication, low but rising threat of substitutes, and barriers that deter some entrants but not innovators. This snapshot highlights key dynamics shaping margins and growth potential. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated coconut sourcing regions

Coconut water sourcing is highly concentrated in tropical hubs—Indonesia and the Philippines together account for over 50% of global coconut production (FAO 2022), with Brazil and Sri Lanka important regional suppliers. Weather shocks and El Niño episodes (eg 2015–16) and plant disease have historically tightened supply and raised input pressure. When harvests swing, growers gain leverage over volumes and contract terms. Diversifying origins and multi‑year contracts mitigate but do not eliminate these constraints.

Quality and specification dependency

Vita Coco’s premium taste, sweetness profile, and strict microbiological specs narrow acceptable coconut sources, making suppliers less interchangeable and elevating bargaining power for qualified processors; the global coconut water market was valued at about $5.4 billion in 2024, intensifying demand for certified supply. Certification requirements like organic and fair trade further shrink the supplier pool, empowering certified co-packers. Tight QA and yearly audits reduce risk but increase switching costs for Vita Coco due to limited qualified partners.

Packaging and input volatility

Dependence on cartons, cans, caps and resins ties Vita Coco to a small set of global packaging firms, increasing supplier bargaining power; commodity swings and container freight volatility during 2021–2023 highlighted how quickly input costs can shift supplier leverage. Long-term supply agreements and multi-sourcing have reduced but not eliminated disruption risk. Sustainability targets for recyclable packaging narrow qualified vendors and can raise costs.

Logistics and port dependencies

Ocean shipping concentration—major alliances controlling roughly 80% of container capacity—gives carriers and forwarders outsized leverage in tight 2024 capacity cycles; port congestion and regulatory delays materially raise landed costs and extend lead times, while suppliers with integrated logistics or port proximity secure better terms; Vita Coco and peers use 60–90 day inventory buffers to partly offset timing risks.

- Alliances control ~80% of container capacity (2024)

- Port congestion increases landed cost and lead times

- Integrated logistics/proximity = stronger commercial terms

- Typical strategic buffers: 60–90 days inventory

Countervailing brand scale

Vita Coco’s category leadership and predictable, year-round demand give suppliers stable multi-million-case volume commitments in 2024, enabling priority allocations and negotiated price concessions.

Co-investments in processing capacity and farmer programs in key sourcing regions align incentives, lowering input cost volatility and gradually reducing supplier power versus arrangements with smaller brands.

- 2024: category leadership drives volume stability

- Priority allocations and price concessions

- Co-investment in capacity and farmer programs

- Supplier power erosion vis-à-vis smaller brands

Coconut supply (50%+) and carriers (~80%) amplify input-cost risk

Suppliers hold elevated leverage: concentrated coconut supply (Indonesia+Philippines >50% production) and strict quality/certification needs make qualified sources scarce, raising switching costs and prices. Packaging and shipping concentration (carriers ~80% capacity) amplify input cost volatility; Vita Coco offsets with 60–90 day buffers and long-term contracts. Co-investments and volume commitments partly dilute supplier power versus smaller brands.

| Metric | 2024 |

|---|---|

| Coconut supply concentration | Indonesia+Philippines >50% |

| Global coconut water market | $5.4B |

| Container capacity control | ~80% |

| Inventory buffer | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis of Vita Coco uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to defend market share and profitability.

A concise, one-sheet Porter's Five Forces for Vita Coco that instantly highlights supplier, buyer, and competitive pressures—ideal for quick strategic decisions and pitch decks. Customize ratings, swap data, and view a spider chart to relieve analysis bottlenecks without any complex setup.

Customers Bargaining Power

Large retail consolidators

Mass retailers, club stores and national grocers control shelf access and wield outsized leverage—Walmart accounted for roughly 25% of US grocery sales in 2024 and Kroger about 10%—so they press suppliers for lower prices, promo funding and extended payment terms (often 60–120 days). Slotting fees and resets can cost tens to hundreds of thousands per SKU, heightening dependence on key accounts; Vita Coco’s high velocity mitigates risk but buyer power stays strong.

Low switching costs for consumers

Coconut water and functional beverages are easily substituted at point of sale, so shoppers switch brands on price, flavor or promotion with minimal friction, pressuring margins and forcing sustained marketing; the global coconut water market is forecast to grow at roughly 8% CAGR through 2030, increasing competitive intensity. Brand equity and Vita Coco’s leading U.S. position partially blunt this power via taste consistency and distribution advantages.

Private label and owned brands

Retailers introducing private-label coconut water anchor price points and increase price sensitivity, with private-label penetration exceeding 40% in the UK and around 20% in the US, compressing category premiums. Such options erode Vita Coco’s brand power and raise trade-down risk during macro slowdowns. Vita Coco must reinforce quality, sourcing transparency, and product innovation to defend margins and share.

Omnichannel transparency

Omnichannel transparency lets shoppers compare Vita Coco prices and reviews across e-commerce, marketplaces and delivery apps, boosting buyer leverage; U.S. e-commerce was about 18% of retail sales in 2024 (eMarketer), increasing price visibility. Dynamic pricing and frequent promotions set consumer expectations for deals, while DTC channels improve margins and first-party data even though retail still holds scale. Assortment curation online alters product visibility and conversion rates.

- Omnichannel price visibility: raises bargaining power

- DTC: higher margins + data but smaller scale vs retail

- Promotions/dynamic pricing: normalize deal expectations

- Assortment curation: controls search visibility and sales

Foodservice and convenience mix

Distributors and chain operators press for consistent supply, margin cushions and rebate programs, giving buyers leverage; package-size mix and cold-chain shelf placement materially affect SKU throughput and shrink. Vita Coco’s presence across grocery, convenience and foodservice—sold in 30+ countries—diversifies exposure, yet volume concentration in top accounts still amplifies buyer influence.

- Buyers: seek supply, margins, rebates

- Throughput: package size + cold-chain crucial

- Channel breadth: grocery, convenience, foodservice

- Risk: top-account volume concentration

Retail giants squeeze coconut-water margins as private label and promos heighten price pressure

Mass retailers (Walmart ~25% US grocery sales 2024; Kroger ~10%) exert strong leverage on Vita Coco, forcing price, promo and payment concessions. Easy substitution, private-label (UK >40%, US ~20%) and promotions (e‑commerce ~18% of retail 2024) increase price sensitivity despite Vita Coco's scale. Diversified channels help but top-account concentration keeps buyer power elevated.

| Metric | 2024 figure |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| E‑commerce retail | ~18% |

| Private‑label penetration | UK >40% / US ~20% |

| Coconut water market CAGR | ~8% to 2030 |

Full Version Awaits

Vita Coco Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Vita Coco Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, with industry-specific data, implications and strategic recommendations. It's the final, fully formatted deliverable ready for immediate download and use.