Thomson Reuters SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Thomson Reuters stands as a global information powerhouse with deep content assets, strong client relationships, and resilient recurring revenue, yet faces digital disruption and regulatory risks. Our full SWOT unpacks competitive edges, vulnerabilities, and strategic options with data-driven insight. Purchase the complete, editable report to inform investment, strategy, or due diligence.

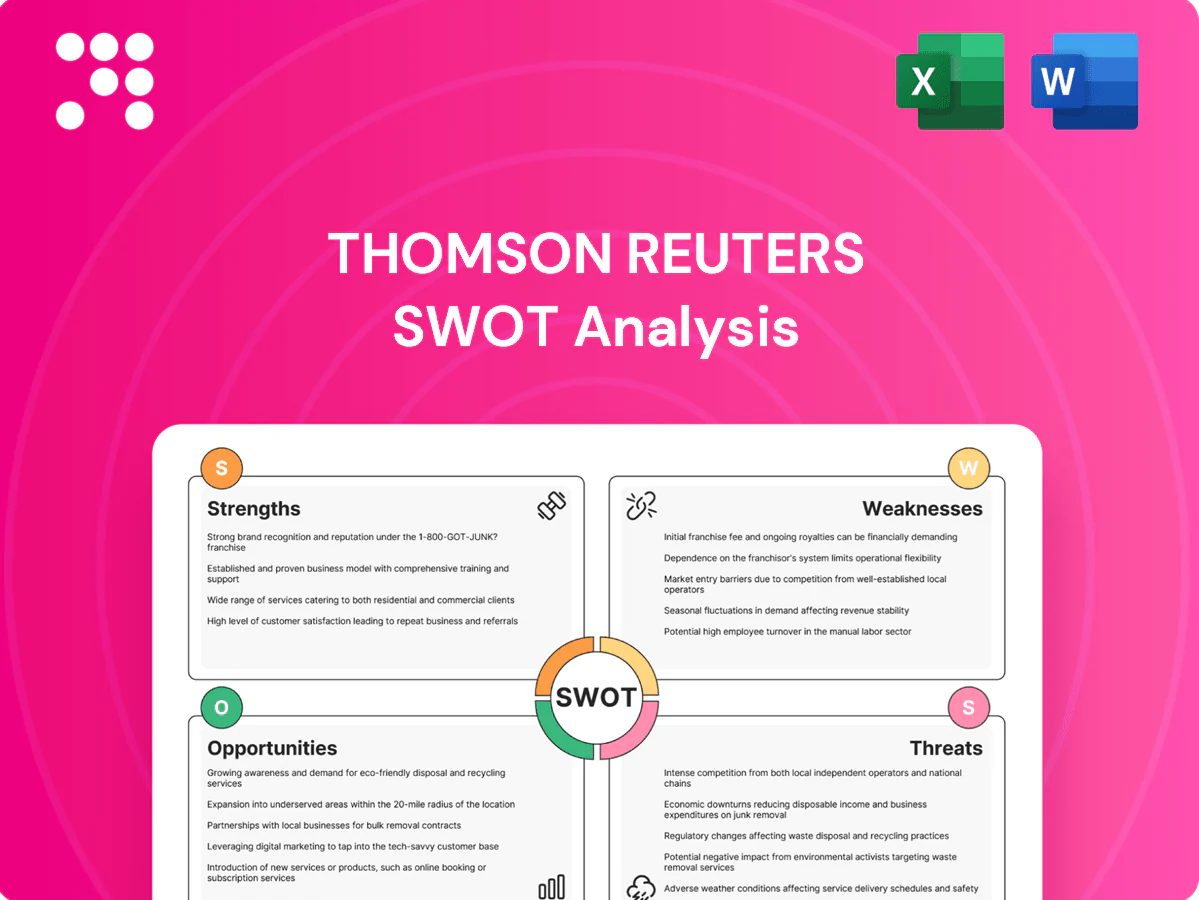

Strengths

Trusted global brand

Thomson Reuters is widely recognized as a premium, mission‑critical provider to legal, tax, risk, and government professionals, leveraging decades of accuracy, timeliness, and reliability to build strong customer trust. That brand equity supports pricing power and renewal rates above 90% and underpinned 2024 revenue of $7.2 billion, differentiating it from lower‑cost or point‑solution rivals.

Deep proprietary content

Flagship assets such as Westlaw, Practical Law, Checkpoint and Reuters News deliver differentiated primary and secondary content, backed by over 170 years of Reuters editorial expertise. Proprietary editorial standards and taxonomy boost search relevance and user productivity across legal and tax workflows. Exclusive datasets and expert annotations create a defensible moat that supports premium subscription pricing. These assets are difficult to replicate, sustaining high retention among professional users.

Integrated workflow platforms

Thomson Reuters bundles content with software like Westlaw Precision, ONESOURCE and HighQ to embed into client workflows, increasing switching costs and driving multi-product adoption. This integrated approach delivers measurable efficiency, auditability and compliance outcomes, supporting client retention. In FY2024 Thomson Reuters reported about $7.7bn revenue with roughly 80% recurring revenue, underscoring stable, end-to-end revenue streams.

AI and analytics capabilities

- 2024 product AI rollouts

- Workflow upsell / higher usage

- Improved precision & speed

- Robust governance & model validation

Diversified, recurring revenue base

Thomson Reuters benefits from a diversified, largely subscription-based revenue mix across Legal, Tax, Risk and News, with subscriptions representing roughly three-quarters of sales and driving high retention and steady seat expansion that produce predictable cash flows; geographic and sector spread reduces volatility and supports continued R&D and bolt-on M&A.

- Subscription mix ~75% of revenue

- High retention and seat expansion

- Geographic and sector diversity

- Cashflow funds R&D and acquisitions

Premium legal-tax intelligence platform: $7.7bn revenue, >90% renewals, ~80% recurring

Thomson Reuters commands premium trust in legal, tax, risk and government markets, supporting >90% renewal rates and FY2024 revenue of $7.7bn. Flagship assets (Westlaw, Checkpoint, Reuters) and proprietary datasets create a high-moat subscription base (~80% recurring). Integrated software bundles and 2024 AI rollouts increased upsell, usage and switching costs, funding steady R&D and bolt-on M&A.

| Metric | 2024 |

|---|---|

| Revenue | $7.7bn |

| Recurring mix | ~80% |

| Renewal rate | >90% |

What is included in the product

Provides a concise SWOT assessment of Thomson Reuters, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Provides a concise, standardized SWOT matrix that simplifies competitive assessment and speeds cross-team alignment, making it easy to integrate findings into reports and executive presentations.

Weaknesses

Premium pricing perception

Premium pricing perception constrains SMB penetration, as Thomson Reuters reported FY2023 revenue of about $6.0 billion, reflecting strong enterprise focus but limited small-business share. High-price tiers see slower uptake in price-sensitive regions, prompting budget scrutiny that slows expansions and seat negotiations. This opens space for lower-cost or AI-native entrants, and discounting pressure can compress margins in competitive deals.

Product complexity

Thomson Reuters product complexity, driven by broad functionality across 100+ countries, raises onboarding and training needs, often extending implementation timelines; the company reported roughly $6.9B revenue in 2024 while serving 50,000+ customers. Complex deployments can lengthen sales cycles and time-to-value, and feature underutilization reduces perceived ROI. High complexity also limits rapid experimentation compared with nimble startups.

Legacy integration burden

Merging legacy systems, content models and acquired tools slows roadmap velocity at Thomson Reuters, where a global footprint across 100+ countries and roughly 25,000 employees raises coordination complexity. Technical debt increases maintenance costs and complicates scaled AI deployment, risking slower time-to-market for analytics and generative features. Inconsistent UX across modules frustrates users and integration risk can delay cross-sell synergies and revenue realization.

Lower-margin news exposure

Reuters News is strategic but operates at lower margins than Thomson Reuters software and data businesses; it accounted for roughly 10% of group revenue in FY2024, constraining consolidated margin expansion. Cyclical media and advertising trends introduce earnings volatility, while strict editorial independence limits cross-monetization and pricing leverage.

- Lower-margin news vs software/data

- ~10% of group revenue FY2024

- Media/advertising cyclicality = earnings variability

- Editorial independence reduces cross-monetization

Dependence on professional budgets

Dependence on professional budgets leaves Thomson Reuters vulnerable when law firms, corporates and governments tighten spending in downturns; legal and tax solutions represent roughly one-third of group revenue, amplifying exposure. Hiring freezes and staffing cuts reduce seat counts and usage, while procurement centralization squeezes pricing and long approval cycles delay large deals.

- Spending volatility: professional clients

- Seat risk: hiring freezes cut usage

- Pricing pressure: centralized procurement

- Sales lag: long approval cycles

Premium pricing curbs SMB uptake; $6.9B FY24; news ~10%, legal/tax ~33%

Premium pricing limits SMB penetration despite FY2024 revenue of about $6.9B, slowing expansion in price-sensitive markets.

Product complexity and legacy integration extend onboarding and sales cycles across 100+ countries and ~50,000 customers.

Reuters news (~10% of group revenue) and reliance on legal/tax (~33% of revenue) constrain margins and increase cyclicality.

| Metric | Value |

|---|---|

| Group revenue FY2024 | $6.9B |

| Reuters share | ~10% |

| Legal/Tax share | ~33% |

| Customers / Employees | ~50,000 / ~25,000 |

Preview Before You Purchase

Thomson Reuters SWOT Analysis

This is a live preview of the Thomson Reuters SWOT Analysis document you’ll receive upon purchase—no sample, no surprises. The content below is pulled directly from the full report and is professional, structured, and ready to use. Complete, editable version is unlocked immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Thomson Reuters stands as a global information powerhouse with deep content assets, strong client relationships, and resilient recurring revenue, yet faces digital disruption and regulatory risks. Our full SWOT unpacks competitive edges, vulnerabilities, and strategic options with data-driven insight. Purchase the complete, editable report to inform investment, strategy, or due diligence.

Strengths

Trusted global brand

Thomson Reuters is widely recognized as a premium, mission‑critical provider to legal, tax, risk, and government professionals, leveraging decades of accuracy, timeliness, and reliability to build strong customer trust. That brand equity supports pricing power and renewal rates above 90% and underpinned 2024 revenue of $7.2 billion, differentiating it from lower‑cost or point‑solution rivals.

Deep proprietary content

Flagship assets such as Westlaw, Practical Law, Checkpoint and Reuters News deliver differentiated primary and secondary content, backed by over 170 years of Reuters editorial expertise. Proprietary editorial standards and taxonomy boost search relevance and user productivity across legal and tax workflows. Exclusive datasets and expert annotations create a defensible moat that supports premium subscription pricing. These assets are difficult to replicate, sustaining high retention among professional users.

Integrated workflow platforms

Thomson Reuters bundles content with software like Westlaw Precision, ONESOURCE and HighQ to embed into client workflows, increasing switching costs and driving multi-product adoption. This integrated approach delivers measurable efficiency, auditability and compliance outcomes, supporting client retention. In FY2024 Thomson Reuters reported about $7.7bn revenue with roughly 80% recurring revenue, underscoring stable, end-to-end revenue streams.

AI and analytics capabilities

- 2024 product AI rollouts

- Workflow upsell / higher usage

- Improved precision & speed

- Robust governance & model validation

Diversified, recurring revenue base

Thomson Reuters benefits from a diversified, largely subscription-based revenue mix across Legal, Tax, Risk and News, with subscriptions representing roughly three-quarters of sales and driving high retention and steady seat expansion that produce predictable cash flows; geographic and sector spread reduces volatility and supports continued R&D and bolt-on M&A.

- Subscription mix ~75% of revenue

- High retention and seat expansion

- Geographic and sector diversity

- Cashflow funds R&D and acquisitions

Premium legal-tax intelligence platform: $7.7bn revenue, >90% renewals, ~80% recurring

Thomson Reuters commands premium trust in legal, tax, risk and government markets, supporting >90% renewal rates and FY2024 revenue of $7.7bn. Flagship assets (Westlaw, Checkpoint, Reuters) and proprietary datasets create a high-moat subscription base (~80% recurring). Integrated software bundles and 2024 AI rollouts increased upsell, usage and switching costs, funding steady R&D and bolt-on M&A.

| Metric | 2024 |

|---|---|

| Revenue | $7.7bn |

| Recurring mix | ~80% |

| Renewal rate | >90% |

What is included in the product

Provides a concise SWOT assessment of Thomson Reuters, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Provides a concise, standardized SWOT matrix that simplifies competitive assessment and speeds cross-team alignment, making it easy to integrate findings into reports and executive presentations.

Weaknesses

Premium pricing perception

Premium pricing perception constrains SMB penetration, as Thomson Reuters reported FY2023 revenue of about $6.0 billion, reflecting strong enterprise focus but limited small-business share. High-price tiers see slower uptake in price-sensitive regions, prompting budget scrutiny that slows expansions and seat negotiations. This opens space for lower-cost or AI-native entrants, and discounting pressure can compress margins in competitive deals.

Product complexity

Thomson Reuters product complexity, driven by broad functionality across 100+ countries, raises onboarding and training needs, often extending implementation timelines; the company reported roughly $6.9B revenue in 2024 while serving 50,000+ customers. Complex deployments can lengthen sales cycles and time-to-value, and feature underutilization reduces perceived ROI. High complexity also limits rapid experimentation compared with nimble startups.

Legacy integration burden

Merging legacy systems, content models and acquired tools slows roadmap velocity at Thomson Reuters, where a global footprint across 100+ countries and roughly 25,000 employees raises coordination complexity. Technical debt increases maintenance costs and complicates scaled AI deployment, risking slower time-to-market for analytics and generative features. Inconsistent UX across modules frustrates users and integration risk can delay cross-sell synergies and revenue realization.

Lower-margin news exposure

Reuters News is strategic but operates at lower margins than Thomson Reuters software and data businesses; it accounted for roughly 10% of group revenue in FY2024, constraining consolidated margin expansion. Cyclical media and advertising trends introduce earnings volatility, while strict editorial independence limits cross-monetization and pricing leverage.

- Lower-margin news vs software/data

- ~10% of group revenue FY2024

- Media/advertising cyclicality = earnings variability

- Editorial independence reduces cross-monetization

Dependence on professional budgets

Dependence on professional budgets leaves Thomson Reuters vulnerable when law firms, corporates and governments tighten spending in downturns; legal and tax solutions represent roughly one-third of group revenue, amplifying exposure. Hiring freezes and staffing cuts reduce seat counts and usage, while procurement centralization squeezes pricing and long approval cycles delay large deals.

- Spending volatility: professional clients

- Seat risk: hiring freezes cut usage

- Pricing pressure: centralized procurement

- Sales lag: long approval cycles

Premium pricing curbs SMB uptake; $6.9B FY24; news ~10%, legal/tax ~33%

Premium pricing limits SMB penetration despite FY2024 revenue of about $6.9B, slowing expansion in price-sensitive markets.

Product complexity and legacy integration extend onboarding and sales cycles across 100+ countries and ~50,000 customers.

Reuters news (~10% of group revenue) and reliance on legal/tax (~33% of revenue) constrain margins and increase cyclicality.

| Metric | Value |

|---|---|

| Group revenue FY2024 | $6.9B |

| Reuters share | ~10% |

| Legal/Tax share | ~33% |

| Customers / Employees | ~50,000 / ~25,000 |

Preview Before You Purchase

Thomson Reuters SWOT Analysis

This is a live preview of the Thomson Reuters SWOT Analysis document you’ll receive upon purchase—no sample, no surprises. The content below is pulled directly from the full report and is professional, structured, and ready to use. Complete, editable version is unlocked immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Thomson Reuters stands as a global information powerhouse with deep content assets, strong client relationships, and resilient recurring revenue, yet faces digital disruption and regulatory risks. Our full SWOT unpacks competitive edges, vulnerabilities, and strategic options with data-driven insight. Purchase the complete, editable report to inform investment, strategy, or due diligence.

Strengths

Trusted global brand

Thomson Reuters is widely recognized as a premium, mission‑critical provider to legal, tax, risk, and government professionals, leveraging decades of accuracy, timeliness, and reliability to build strong customer trust. That brand equity supports pricing power and renewal rates above 90% and underpinned 2024 revenue of $7.2 billion, differentiating it from lower‑cost or point‑solution rivals.

Deep proprietary content

Flagship assets such as Westlaw, Practical Law, Checkpoint and Reuters News deliver differentiated primary and secondary content, backed by over 170 years of Reuters editorial expertise. Proprietary editorial standards and taxonomy boost search relevance and user productivity across legal and tax workflows. Exclusive datasets and expert annotations create a defensible moat that supports premium subscription pricing. These assets are difficult to replicate, sustaining high retention among professional users.

Integrated workflow platforms

Thomson Reuters bundles content with software like Westlaw Precision, ONESOURCE and HighQ to embed into client workflows, increasing switching costs and driving multi-product adoption. This integrated approach delivers measurable efficiency, auditability and compliance outcomes, supporting client retention. In FY2024 Thomson Reuters reported about $7.7bn revenue with roughly 80% recurring revenue, underscoring stable, end-to-end revenue streams.

AI and analytics capabilities

- 2024 product AI rollouts

- Workflow upsell / higher usage

- Improved precision & speed

- Robust governance & model validation

Diversified, recurring revenue base

Thomson Reuters benefits from a diversified, largely subscription-based revenue mix across Legal, Tax, Risk and News, with subscriptions representing roughly three-quarters of sales and driving high retention and steady seat expansion that produce predictable cash flows; geographic and sector spread reduces volatility and supports continued R&D and bolt-on M&A.

- Subscription mix ~75% of revenue

- High retention and seat expansion

- Geographic and sector diversity

- Cashflow funds R&D and acquisitions

Premium legal-tax intelligence platform: $7.7bn revenue, >90% renewals, ~80% recurring

Thomson Reuters commands premium trust in legal, tax, risk and government markets, supporting >90% renewal rates and FY2024 revenue of $7.7bn. Flagship assets (Westlaw, Checkpoint, Reuters) and proprietary datasets create a high-moat subscription base (~80% recurring). Integrated software bundles and 2024 AI rollouts increased upsell, usage and switching costs, funding steady R&D and bolt-on M&A.

| Metric | 2024 |

|---|---|

| Revenue | $7.7bn |

| Recurring mix | ~80% |

| Renewal rate | >90% |

What is included in the product

Provides a concise SWOT assessment of Thomson Reuters, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Provides a concise, standardized SWOT matrix that simplifies competitive assessment and speeds cross-team alignment, making it easy to integrate findings into reports and executive presentations.

Weaknesses

Premium pricing perception

Premium pricing perception constrains SMB penetration, as Thomson Reuters reported FY2023 revenue of about $6.0 billion, reflecting strong enterprise focus but limited small-business share. High-price tiers see slower uptake in price-sensitive regions, prompting budget scrutiny that slows expansions and seat negotiations. This opens space for lower-cost or AI-native entrants, and discounting pressure can compress margins in competitive deals.

Product complexity

Thomson Reuters product complexity, driven by broad functionality across 100+ countries, raises onboarding and training needs, often extending implementation timelines; the company reported roughly $6.9B revenue in 2024 while serving 50,000+ customers. Complex deployments can lengthen sales cycles and time-to-value, and feature underutilization reduces perceived ROI. High complexity also limits rapid experimentation compared with nimble startups.

Legacy integration burden

Merging legacy systems, content models and acquired tools slows roadmap velocity at Thomson Reuters, where a global footprint across 100+ countries and roughly 25,000 employees raises coordination complexity. Technical debt increases maintenance costs and complicates scaled AI deployment, risking slower time-to-market for analytics and generative features. Inconsistent UX across modules frustrates users and integration risk can delay cross-sell synergies and revenue realization.

Lower-margin news exposure

Reuters News is strategic but operates at lower margins than Thomson Reuters software and data businesses; it accounted for roughly 10% of group revenue in FY2024, constraining consolidated margin expansion. Cyclical media and advertising trends introduce earnings volatility, while strict editorial independence limits cross-monetization and pricing leverage.

- Lower-margin news vs software/data

- ~10% of group revenue FY2024

- Media/advertising cyclicality = earnings variability

- Editorial independence reduces cross-monetization

Dependence on professional budgets

Dependence on professional budgets leaves Thomson Reuters vulnerable when law firms, corporates and governments tighten spending in downturns; legal and tax solutions represent roughly one-third of group revenue, amplifying exposure. Hiring freezes and staffing cuts reduce seat counts and usage, while procurement centralization squeezes pricing and long approval cycles delay large deals.

- Spending volatility: professional clients

- Seat risk: hiring freezes cut usage

- Pricing pressure: centralized procurement

- Sales lag: long approval cycles

Premium pricing curbs SMB uptake; $6.9B FY24; news ~10%, legal/tax ~33%

Premium pricing limits SMB penetration despite FY2024 revenue of about $6.9B, slowing expansion in price-sensitive markets.

Product complexity and legacy integration extend onboarding and sales cycles across 100+ countries and ~50,000 customers.

Reuters news (~10% of group revenue) and reliance on legal/tax (~33% of revenue) constrain margins and increase cyclicality.

| Metric | Value |

|---|---|

| Group revenue FY2024 | $6.9B |

| Reuters share | ~10% |

| Legal/Tax share | ~33% |

| Customers / Employees | ~50,000 / ~25,000 |

Preview Before You Purchase

Thomson Reuters SWOT Analysis

This is a live preview of the Thomson Reuters SWOT Analysis document you’ll receive upon purchase—no sample, no surprises. The content below is pulled directly from the full report and is professional, structured, and ready to use. Complete, editable version is unlocked immediately after checkout.