THOR Industries SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

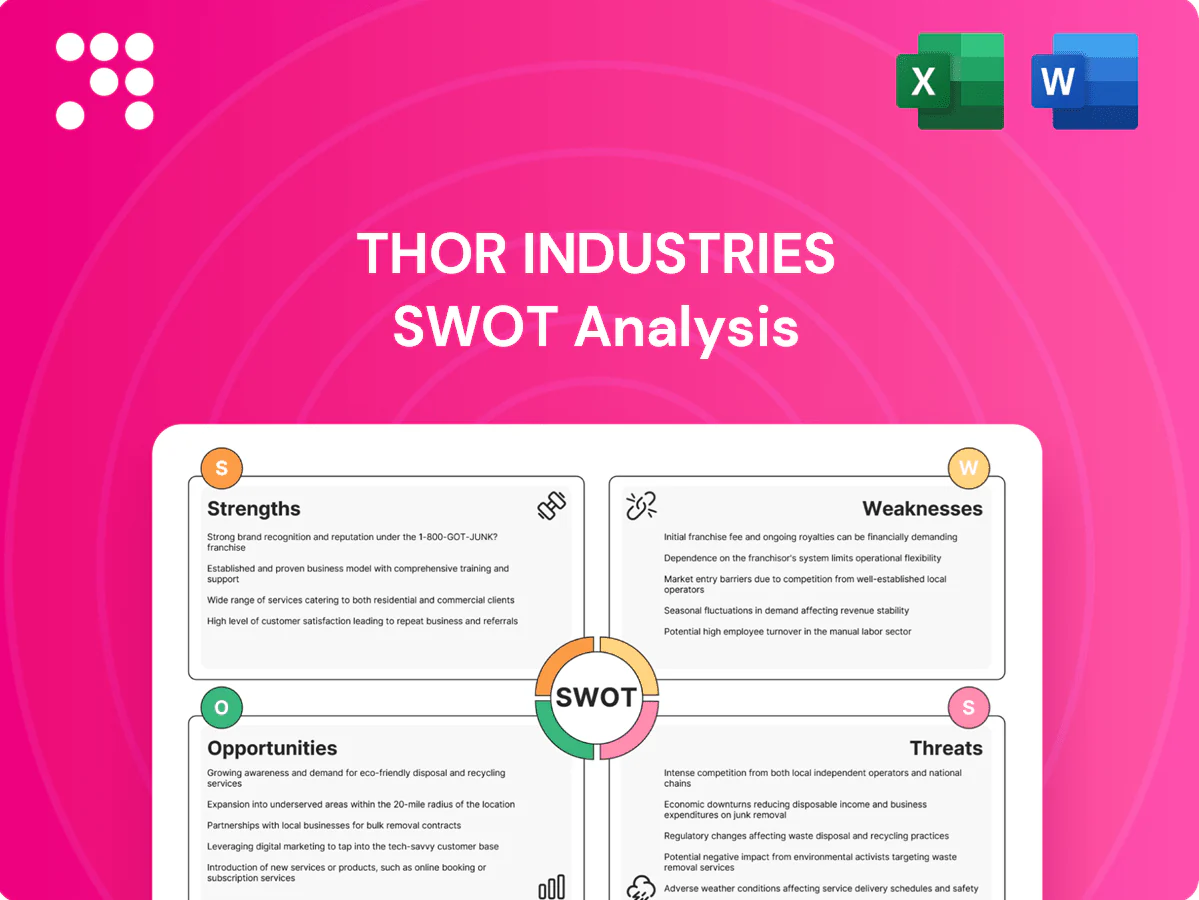

THOR Industries' SWOT highlights dominant market share, strong dealer network, and product diversity, balanced by supply-chain pressures and cyclical RV demand. Our full SWOT dives into actionable strengths, quantified risks, and strategic opportunities for investors and strategists. Purchase the complete, editable report (Word + Excel) to leverage research-backed insights for planning, pitching, or investing.

Strengths

Global RV market leadership

THOR is the largest global RV manufacturer, leveraging scale to secure procurement discounts, consolidated branding and stronger dealer leverage; the company reported over $11 billion in revenue in FY2024. Market leadership boosts negotiating power with suppliers and distributors, lowering input costs and improving margins. Broader product and price coverage gives resilience across cycles, while strong brand visibility attracts consumers and dealers seeking reliability and after-sales support.

Broad, multi-brand product portfolio

Thor Industries, the largest RV manufacturer in North America with marquee brands such as Airstream, Jayco and Keystone, spans travel trailers, fifth wheels and motorhomes across entry, mid and premium tiers. This breadth reduces dependence on any single product segment or price point and supports cross-selling as customers trade up or down. A wide lineup helps match evolving consumer preferences and budget constraints.

Extensive dealer network in North America and Europe

THOR distributes primarily through more than 3,000 independent dealers across North America and Europe, leveraging deep local relationships and service capabilities to accelerate inventory turns and shorten market feedback loops. The dealer network underpins after-sales service, parts and warranty delivery that strengthen loyalty, while Europe contributes roughly 12% of revenue, diversifying exposure beyond North America.

Operational scale and supply chain reach

Scale supports cost efficiencies in materials sourcing, logistics, and shared components, helping THOR contain costs as LTM revenue exceeded $10 billion in 2024. Standardization and platforming improve manufacturing throughput and quality across facilities. Greater bargaining power helps mitigate input-price volatility. Scale also funds investments in technology, safety, and sustainability initiatives.

- Cost leverage: lower unit materials/logistics

- Platforming: higher throughput & quality

- Bargaining power: cushions input swings

- Capital: funds tech, safety, sustainability

Strong parts, accessories, and service ecosystem

Thor Industries leverages a robust parts, accessories, and service ecosystem that drives recurring revenue and deeper customer engagement; accessories and attachments lift margin per unit and help convert one-time buyers into lifetime customers. Thor reported fiscal 2024 revenue of about $11.6 billion, with aftermarket and service channels improving dealer economics and retention. The ecosystem strengthens dealer value through maintenance, upgrades, and higher lifetime value, increasing brand stickiness.

- Recurring revenue from parts/services

- Higher margin via accessories

- Stronger dealer value proposition

- Improved customer lifetime value

Global RV leader: $11.6B, >3,000 dealers

THOR is the largest global RV manufacturer with FY2024 revenue $11.6B, >3,000 dealers and ~12% revenue from Europe; scale secures procurement discounts and stronger dealer leverage. Platforming and standardization boost throughput and quality, lowering unit costs. A broad brand lineup plus parts/services drive recurring revenue and higher customer lifetime value.

| Metric | Value |

|---|---|

| FY2024 Revenue | $11.6B |

| Dealer Network | >3,000 |

| Europe Revenue | ~12% |

| Market Position | Largest global RV manufacturer |

What is included in the product

Delivers a strategic overview of THOR Industries’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, key growth drivers, operational gaps, and market risks shaping future performance.

Provides a concise SWOT matrix for THOR Industries that highlights strategic gaps and growth opportunities at a glance, enabling fast alignment and decision-making for executives and investors.

Weaknesses

High cyclicality and discretionary demand exposure

RV purchases are big-ticket, rate-sensitive buys tied to consumer confidence; Thor's FY2024 revenue of about $11.5 billion reflects sensitivity to demand swings. The RV Industry Association reported wholesale shipments down roughly 34% from the 2021 peak by 2024, showing downturns rapidly cut orders and dealer inventories. Such volatility complicates capacity planning, labor utilization and can pressure pricing and margins in slow periods.

Dealer-channel dependence

Reliance on approximately 1,400 independent dealers limits THOR’s direct control over retail pricing, customer experience and inventory mix. Dealer financial health and inventory turns drive THOR’s sell-in dynamics and warranty outcomes, raising exposure during demand slowdowns. Any direct-to-consumer experiments risk channel conflict and strained dealer relations. Geographic gaps in dealer coverage, especially outside North America, can constrain market expansion.

Manufacturing complexity and fixed-cost base

Multiple brands and platforms increase scheduling, quality-control and supply-chain complexity across THOR’s operations, straining coordination and ramp times. High fixed factory and labor costs create pronounced operating leverage that depresses margins in downturns. Ongoing component shortages have intermittently halted production lines and delayed deliveries. This complexity also raises warranty and rework expenses, eroding profitability.

Exposure to input cost inflation

Exposure to input cost inflation: steel, aluminum, lumber, resins, electronics and chassis components are major cost drivers that create margin volatility for THOR Industries; rapid commodity swings and higher freight rates can quickly compress gross margins. Price increases to dealers and consumers often lag raw‑material spikes because of fixed dealer contracts and demand sensitivity; hedging and supplier diversification only partially mitigate this risk.

- Key drivers: steel, aluminum, lumber, resins, electronics, chassis

- Margin pressure from commodity and freight volatility

- Pricing lag vs. cost spikes due to dealer contracts

- Hedging/diversification provide limited protection

Limited diversification beyond RVs

THOR Industries remains heavily concentrated in RVs, leaving the company exposed to sector-specific cycles, regulatory shifts and supply-chain disruptions tied to camping and leisure travel. Adjacent markets such as marine and powersports are relatively small or indirect contributors, limiting revenue diversification. Seasonal sales patterns strain working capital and inventory management, while dependence on travel and outdoor recreation trends increases demand volatility.

- Revenue concentration: majority from RVs

- Adjacencies: limited contribution from marine/powersports

- Seasonality: spring/summer sales peak

- Demand risk: tied to travel/outdoor trends

FY2024 $11.5B; shipments down 34% vs 2021; dealer dependence, margin squeeze

THOR’s FY2024 revenue ~11.5B shows exposure to demand swings; wholesale RV shipments were down ~34% vs 2021 by 2024, amplifying margin and capacity risk. Dependence on ~1,400 independent dealers limits pricing control and slows pass-through of commodity cost hikes. High fixed costs, multi-brand complexity and input inflation (steel, lumber, chassis) compress margins in downturns.

| Metric | 2024 |

|---|---|

| Revenue | $11.5B |

| Shipments vs 2021 | -34% |

| Dealers | ~1,400 |

Same Document Delivered

THOR Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the THOR Industries analysis file, and the complete, editable report becomes available after checkout.

Go Beyond the Preview—Access the Full Strategic Report

THOR Industries' SWOT highlights dominant market share, strong dealer network, and product diversity, balanced by supply-chain pressures and cyclical RV demand. Our full SWOT dives into actionable strengths, quantified risks, and strategic opportunities for investors and strategists. Purchase the complete, editable report (Word + Excel) to leverage research-backed insights for planning, pitching, or investing.

Strengths

Global RV market leadership

THOR is the largest global RV manufacturer, leveraging scale to secure procurement discounts, consolidated branding and stronger dealer leverage; the company reported over $11 billion in revenue in FY2024. Market leadership boosts negotiating power with suppliers and distributors, lowering input costs and improving margins. Broader product and price coverage gives resilience across cycles, while strong brand visibility attracts consumers and dealers seeking reliability and after-sales support.

Broad, multi-brand product portfolio

Thor Industries, the largest RV manufacturer in North America with marquee brands such as Airstream, Jayco and Keystone, spans travel trailers, fifth wheels and motorhomes across entry, mid and premium tiers. This breadth reduces dependence on any single product segment or price point and supports cross-selling as customers trade up or down. A wide lineup helps match evolving consumer preferences and budget constraints.

Extensive dealer network in North America and Europe

THOR distributes primarily through more than 3,000 independent dealers across North America and Europe, leveraging deep local relationships and service capabilities to accelerate inventory turns and shorten market feedback loops. The dealer network underpins after-sales service, parts and warranty delivery that strengthen loyalty, while Europe contributes roughly 12% of revenue, diversifying exposure beyond North America.

Operational scale and supply chain reach

Scale supports cost efficiencies in materials sourcing, logistics, and shared components, helping THOR contain costs as LTM revenue exceeded $10 billion in 2024. Standardization and platforming improve manufacturing throughput and quality across facilities. Greater bargaining power helps mitigate input-price volatility. Scale also funds investments in technology, safety, and sustainability initiatives.

- Cost leverage: lower unit materials/logistics

- Platforming: higher throughput & quality

- Bargaining power: cushions input swings

- Capital: funds tech, safety, sustainability

Strong parts, accessories, and service ecosystem

Thor Industries leverages a robust parts, accessories, and service ecosystem that drives recurring revenue and deeper customer engagement; accessories and attachments lift margin per unit and help convert one-time buyers into lifetime customers. Thor reported fiscal 2024 revenue of about $11.6 billion, with aftermarket and service channels improving dealer economics and retention. The ecosystem strengthens dealer value through maintenance, upgrades, and higher lifetime value, increasing brand stickiness.

- Recurring revenue from parts/services

- Higher margin via accessories

- Stronger dealer value proposition

- Improved customer lifetime value

Global RV leader: $11.6B, >3,000 dealers

THOR is the largest global RV manufacturer with FY2024 revenue $11.6B, >3,000 dealers and ~12% revenue from Europe; scale secures procurement discounts and stronger dealer leverage. Platforming and standardization boost throughput and quality, lowering unit costs. A broad brand lineup plus parts/services drive recurring revenue and higher customer lifetime value.

| Metric | Value |

|---|---|

| FY2024 Revenue | $11.6B |

| Dealer Network | >3,000 |

| Europe Revenue | ~12% |

| Market Position | Largest global RV manufacturer |

What is included in the product

Delivers a strategic overview of THOR Industries’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, key growth drivers, operational gaps, and market risks shaping future performance.

Provides a concise SWOT matrix for THOR Industries that highlights strategic gaps and growth opportunities at a glance, enabling fast alignment and decision-making for executives and investors.

Weaknesses

High cyclicality and discretionary demand exposure

RV purchases are big-ticket, rate-sensitive buys tied to consumer confidence; Thor's FY2024 revenue of about $11.5 billion reflects sensitivity to demand swings. The RV Industry Association reported wholesale shipments down roughly 34% from the 2021 peak by 2024, showing downturns rapidly cut orders and dealer inventories. Such volatility complicates capacity planning, labor utilization and can pressure pricing and margins in slow periods.

Dealer-channel dependence

Reliance on approximately 1,400 independent dealers limits THOR’s direct control over retail pricing, customer experience and inventory mix. Dealer financial health and inventory turns drive THOR’s sell-in dynamics and warranty outcomes, raising exposure during demand slowdowns. Any direct-to-consumer experiments risk channel conflict and strained dealer relations. Geographic gaps in dealer coverage, especially outside North America, can constrain market expansion.

Manufacturing complexity and fixed-cost base

Multiple brands and platforms increase scheduling, quality-control and supply-chain complexity across THOR’s operations, straining coordination and ramp times. High fixed factory and labor costs create pronounced operating leverage that depresses margins in downturns. Ongoing component shortages have intermittently halted production lines and delayed deliveries. This complexity also raises warranty and rework expenses, eroding profitability.

Exposure to input cost inflation

Exposure to input cost inflation: steel, aluminum, lumber, resins, electronics and chassis components are major cost drivers that create margin volatility for THOR Industries; rapid commodity swings and higher freight rates can quickly compress gross margins. Price increases to dealers and consumers often lag raw‑material spikes because of fixed dealer contracts and demand sensitivity; hedging and supplier diversification only partially mitigate this risk.

- Key drivers: steel, aluminum, lumber, resins, electronics, chassis

- Margin pressure from commodity and freight volatility

- Pricing lag vs. cost spikes due to dealer contracts

- Hedging/diversification provide limited protection

Limited diversification beyond RVs

THOR Industries remains heavily concentrated in RVs, leaving the company exposed to sector-specific cycles, regulatory shifts and supply-chain disruptions tied to camping and leisure travel. Adjacent markets such as marine and powersports are relatively small or indirect contributors, limiting revenue diversification. Seasonal sales patterns strain working capital and inventory management, while dependence on travel and outdoor recreation trends increases demand volatility.

- Revenue concentration: majority from RVs

- Adjacencies: limited contribution from marine/powersports

- Seasonality: spring/summer sales peak

- Demand risk: tied to travel/outdoor trends

FY2024 $11.5B; shipments down 34% vs 2021; dealer dependence, margin squeeze

THOR’s FY2024 revenue ~11.5B shows exposure to demand swings; wholesale RV shipments were down ~34% vs 2021 by 2024, amplifying margin and capacity risk. Dependence on ~1,400 independent dealers limits pricing control and slows pass-through of commodity cost hikes. High fixed costs, multi-brand complexity and input inflation (steel, lumber, chassis) compress margins in downturns.

| Metric | 2024 |

|---|---|

| Revenue | $11.5B |

| Shipments vs 2021 | -34% |

| Dealers | ~1,400 |

Same Document Delivered

THOR Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the THOR Industries analysis file, and the complete, editable report becomes available after checkout.

Description

Go Beyond the Preview—Access the Full Strategic Report

THOR Industries' SWOT highlights dominant market share, strong dealer network, and product diversity, balanced by supply-chain pressures and cyclical RV demand. Our full SWOT dives into actionable strengths, quantified risks, and strategic opportunities for investors and strategists. Purchase the complete, editable report (Word + Excel) to leverage research-backed insights for planning, pitching, or investing.

Strengths

Global RV market leadership

THOR is the largest global RV manufacturer, leveraging scale to secure procurement discounts, consolidated branding and stronger dealer leverage; the company reported over $11 billion in revenue in FY2024. Market leadership boosts negotiating power with suppliers and distributors, lowering input costs and improving margins. Broader product and price coverage gives resilience across cycles, while strong brand visibility attracts consumers and dealers seeking reliability and after-sales support.

Broad, multi-brand product portfolio

Thor Industries, the largest RV manufacturer in North America with marquee brands such as Airstream, Jayco and Keystone, spans travel trailers, fifth wheels and motorhomes across entry, mid and premium tiers. This breadth reduces dependence on any single product segment or price point and supports cross-selling as customers trade up or down. A wide lineup helps match evolving consumer preferences and budget constraints.

Extensive dealer network in North America and Europe

THOR distributes primarily through more than 3,000 independent dealers across North America and Europe, leveraging deep local relationships and service capabilities to accelerate inventory turns and shorten market feedback loops. The dealer network underpins after-sales service, parts and warranty delivery that strengthen loyalty, while Europe contributes roughly 12% of revenue, diversifying exposure beyond North America.

Operational scale and supply chain reach

Scale supports cost efficiencies in materials sourcing, logistics, and shared components, helping THOR contain costs as LTM revenue exceeded $10 billion in 2024. Standardization and platforming improve manufacturing throughput and quality across facilities. Greater bargaining power helps mitigate input-price volatility. Scale also funds investments in technology, safety, and sustainability initiatives.

- Cost leverage: lower unit materials/logistics

- Platforming: higher throughput & quality

- Bargaining power: cushions input swings

- Capital: funds tech, safety, sustainability

Strong parts, accessories, and service ecosystem

Thor Industries leverages a robust parts, accessories, and service ecosystem that drives recurring revenue and deeper customer engagement; accessories and attachments lift margin per unit and help convert one-time buyers into lifetime customers. Thor reported fiscal 2024 revenue of about $11.6 billion, with aftermarket and service channels improving dealer economics and retention. The ecosystem strengthens dealer value through maintenance, upgrades, and higher lifetime value, increasing brand stickiness.

- Recurring revenue from parts/services

- Higher margin via accessories

- Stronger dealer value proposition

- Improved customer lifetime value

Global RV leader: $11.6B, >3,000 dealers

THOR is the largest global RV manufacturer with FY2024 revenue $11.6B, >3,000 dealers and ~12% revenue from Europe; scale secures procurement discounts and stronger dealer leverage. Platforming and standardization boost throughput and quality, lowering unit costs. A broad brand lineup plus parts/services drive recurring revenue and higher customer lifetime value.

| Metric | Value |

|---|---|

| FY2024 Revenue | $11.6B |

| Dealer Network | >3,000 |

| Europe Revenue | ~12% |

| Market Position | Largest global RV manufacturer |

What is included in the product

Delivers a strategic overview of THOR Industries’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, key growth drivers, operational gaps, and market risks shaping future performance.

Provides a concise SWOT matrix for THOR Industries that highlights strategic gaps and growth opportunities at a glance, enabling fast alignment and decision-making for executives and investors.

Weaknesses

High cyclicality and discretionary demand exposure

RV purchases are big-ticket, rate-sensitive buys tied to consumer confidence; Thor's FY2024 revenue of about $11.5 billion reflects sensitivity to demand swings. The RV Industry Association reported wholesale shipments down roughly 34% from the 2021 peak by 2024, showing downturns rapidly cut orders and dealer inventories. Such volatility complicates capacity planning, labor utilization and can pressure pricing and margins in slow periods.

Dealer-channel dependence

Reliance on approximately 1,400 independent dealers limits THOR’s direct control over retail pricing, customer experience and inventory mix. Dealer financial health and inventory turns drive THOR’s sell-in dynamics and warranty outcomes, raising exposure during demand slowdowns. Any direct-to-consumer experiments risk channel conflict and strained dealer relations. Geographic gaps in dealer coverage, especially outside North America, can constrain market expansion.

Manufacturing complexity and fixed-cost base

Multiple brands and platforms increase scheduling, quality-control and supply-chain complexity across THOR’s operations, straining coordination and ramp times. High fixed factory and labor costs create pronounced operating leverage that depresses margins in downturns. Ongoing component shortages have intermittently halted production lines and delayed deliveries. This complexity also raises warranty and rework expenses, eroding profitability.

Exposure to input cost inflation

Exposure to input cost inflation: steel, aluminum, lumber, resins, electronics and chassis components are major cost drivers that create margin volatility for THOR Industries; rapid commodity swings and higher freight rates can quickly compress gross margins. Price increases to dealers and consumers often lag raw‑material spikes because of fixed dealer contracts and demand sensitivity; hedging and supplier diversification only partially mitigate this risk.

- Key drivers: steel, aluminum, lumber, resins, electronics, chassis

- Margin pressure from commodity and freight volatility

- Pricing lag vs. cost spikes due to dealer contracts

- Hedging/diversification provide limited protection

Limited diversification beyond RVs

THOR Industries remains heavily concentrated in RVs, leaving the company exposed to sector-specific cycles, regulatory shifts and supply-chain disruptions tied to camping and leisure travel. Adjacent markets such as marine and powersports are relatively small or indirect contributors, limiting revenue diversification. Seasonal sales patterns strain working capital and inventory management, while dependence on travel and outdoor recreation trends increases demand volatility.

- Revenue concentration: majority from RVs

- Adjacencies: limited contribution from marine/powersports

- Seasonality: spring/summer sales peak

- Demand risk: tied to travel/outdoor trends

FY2024 $11.5B; shipments down 34% vs 2021; dealer dependence, margin squeeze

THOR’s FY2024 revenue ~11.5B shows exposure to demand swings; wholesale RV shipments were down ~34% vs 2021 by 2024, amplifying margin and capacity risk. Dependence on ~1,400 independent dealers limits pricing control and slows pass-through of commodity cost hikes. High fixed costs, multi-brand complexity and input inflation (steel, lumber, chassis) compress margins in downturns.

| Metric | 2024 |

|---|---|

| Revenue | $11.5B |

| Shipments vs 2021 | -34% |

| Dealers | ~1,400 |

Same Document Delivered

THOR Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the THOR Industries analysis file, and the complete, editable report becomes available after checkout.