Tianshan Material Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Tianshan Material faces moderate supplier bargaining due to specialized inputs, intense rivalry from regional producers, and a growing threat from low-cost substitutes as downstream demand shifts; buyer power is rising with larger distributors consolidating. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Captive limestone mitigates input leverage

Core limestone is largely secured through captive or long-term quarry rights—commonly 20–30 year leases—limiting supplier bargaining power over Tianshan Material’s key input. This lowers price volatility and switching risk across Xinjiang and adjacent markets. Permitting timelines and reserve quality, however, still drive mining cost variance and capex timing. Supply interruptions tend to stem from regulatory or geological issues rather than vendor pricing pressure.

Energy and fuel suppliers hold moderate power

Thermal coal, petcoke and electricity drive ~25–35% of operating costs for materials handling in 2024, and regional energy rules plus transport constraints raise supplier leverage. Xinjiang’s remoteness adds ~10–15% to inbound logistics and heightens reliance on steady fuel flows. Multi-sourcing and fuel-mix flexibility blunt but cannot fully offset price spikes; industrial tariffs (≈0.5–0.9 RMB/kWh) and seasonal curtailments (up to 10–20% in peak months) increase bargaining pressure.

Gypsum and additives are substitutable

Gypsum, slag and other additives come from multiple regional mines and recycling streams, making them readily substitutable and capping any single supplier’s clout. Quality is governed by national GB and international standards, enabling competitive bidding across vendors. Proximity and freight remain key differentiators for landed cost, while long‑term contracts and safety stocks typically reduce supplier leverage further.

Equipment OEMs and spare parts exert episodic leverage

Equipment OEMs for kilns, mills and environmental controls are concentrated (major global suppliers dominate aftermarket supply), granting episodic pricing power during capex surges; long lead times and proprietary components frequently create lock‑in for service contracts. Lifecycle procurement, local fabrication and third‑party maintenance dilute recurring leverage, while plant digital monitoring enables predictive maintenance to avoid OEM premium emergencies.

- OEM concentration: episodic capex pricing power

- Long lead times/proprietary parts → service lock‑in

- Lifecycle buys + local fabrication reduce recurring dependence

- Digital monitoring enables predictive maintenance, lowers emergency spend

Logistics providers influence delivered cost

Rail and truck capacity in and out of Xinjiang directly shapes delivered cement pricing; 2024 peak-season truck rates spiked about 25% versus off-peak, and fuel comprises roughly 30% of short-haul trucking cost, shifting margins toward carriers during bottlenecks. Long-term rail allocations and owners running captive fleets have reduced transporter leverage, while proximity to demand centers remains the strongest countermeasure.

- Rail vs truck cost gap ~30–50%

- Peak truck rate rise ~25% (2024)

- Fuel ~30% of trucking opex

- Own-fleet/rail contracts cut supplier power

- Proximity to demand = primary hedge

Leases 20–30y curb supplier power; energy ~30% opex

Captive limestone leases (20–30y) and long‑term contracts curb supplier pricing power for core feedstock. Energy (thermal coal/petcoke/electricity) drives ~30% of 2024 opex and Xinjiang remoteness adds ~10–15% logistics premium, increasing supplier leverage. OEM concentration and long lead times create episodic capex/service lock‑in; peak truck rates jumped ~25% in 2024.

| Metric | 2024 Value |

|---|---|

| Limestone lease length | 20–30 years |

| Energy share of opex | ~30% |

| Logistics premium (remoteness) | 10–15% |

| Peak truck rate spike | ~25% |

| Rail vs truck gap | 30–50% |

| OEM concentration | High (episodic power) |

What is included in the product

Tailored exclusively for Tianshan Material, this Porter’s Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies disruptive threats and market dynamics shaping pricing and profitability.

Clear one-sheet Tianshan Material Five Forces summary for fast, board-ready decisions—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart for rapid scenario comparison.

Customers Bargaining Power

Large projects and SOE contractors negotiate hard

Large infrastructure and SOE EPC buyers command volume-based discounts and strict technical specs, squeezing margins as they bundle multi-site contracts to drive procurement leverage. Vendors compete on delivered reliability and extended credit terms to win business amid price pressure. Deep relationships and consistently on-time delivery can sustain per-project margins despite negotiated discounts. Industry reports show major EPC tenders favor suppliers offering integrated logistics and payment flexibility.

Ready-mix plants face low switching costs

Cement is a highly standardized commodity (global production ~4.4 billion tonnes in 2024), so RMC buyers switch suppliers quickly on price and logistics, driving frequent re-bidding and typically short-tenor contracts often under 12 months. Consistent quality and technical support create soft switching frictions that raise retention. Proximity and reliable peak-season supply further sustain customer stickiness.

Demand cyclicality strengthens buyer timing power

Demand cyclicality — with seasonal construction peaks in spring-summer and policy-driven pauses in late-year 2024 — shifts buyer timing power as purchasers defer orders in soft months to extract typical price cuts of 3–5%. Producers respond with production discipline and coordinated maintenance outages to support spot prices. Back-to-back logistics commitments lock in volumes and mitigate mid-cycle volatility.

Payment terms and credit raise hidden leverage

Extended receivables in construction chains shift financing costs onto suppliers, increasing effective cost of goods sold and pressuring margins; industry data (Intrum Payment Report 2024) showed average days beyond terms around 40 days in many markets, highlighting the scale of delayed payments. Downstream creditworthiness commonly dictates price concessions and allocation; tightening terms risks losing volume to rivals who absorb financing, while credit insurance and factoring partially offset buyer leverage.

- Receivables transfer financing burden

- Buyer credit shapes pricing/allocation

- Tighter terms can cost volume to financing-ready rivals

- Credit insurance/factoring reduce but do not eliminate leverage

Specification and performance service add value

Technical support for blended cements, low-heat mixes and durability specifications lets Tianshan Material differentiate offers; in 2024 critical infrastructure buyers typically accept 3–7% price premiums for proven performance, narrowing headline-price sensitivity. Lab services, onsite trials and precise delivery lower performance risk and shift procurement toward value metrics, marginally weakening buyer bargaining power in high-stakes applications.

- Performance-led premiums: 3–7% accepted

- Risk reduction: lab trials and QA raise switching costs

- Delivery precision: reduces focus on headline price

SOE/EPC price pressure; reliable delivery and 3–7% premiums protect suppliers

Large SOE/EPC buyers extract volume discounts and extended terms, cutting margins; key tenders favor integrated logistics and payment flexibility. Cement commoditization (global 4.4b t in 2024) and short contracts raise switching; performance premiums (3–7%) and reliable delivery limit full price pressure. Late payments (~40 days beyond terms) shift financing costs to suppliers and shape allocation.

| Metric | 2024 |

|---|---|

| Global cement | 4.4b t |

| Accepted premium | 3–7% |

| Days beyond terms | ~40 |

Preview Before You Purchase

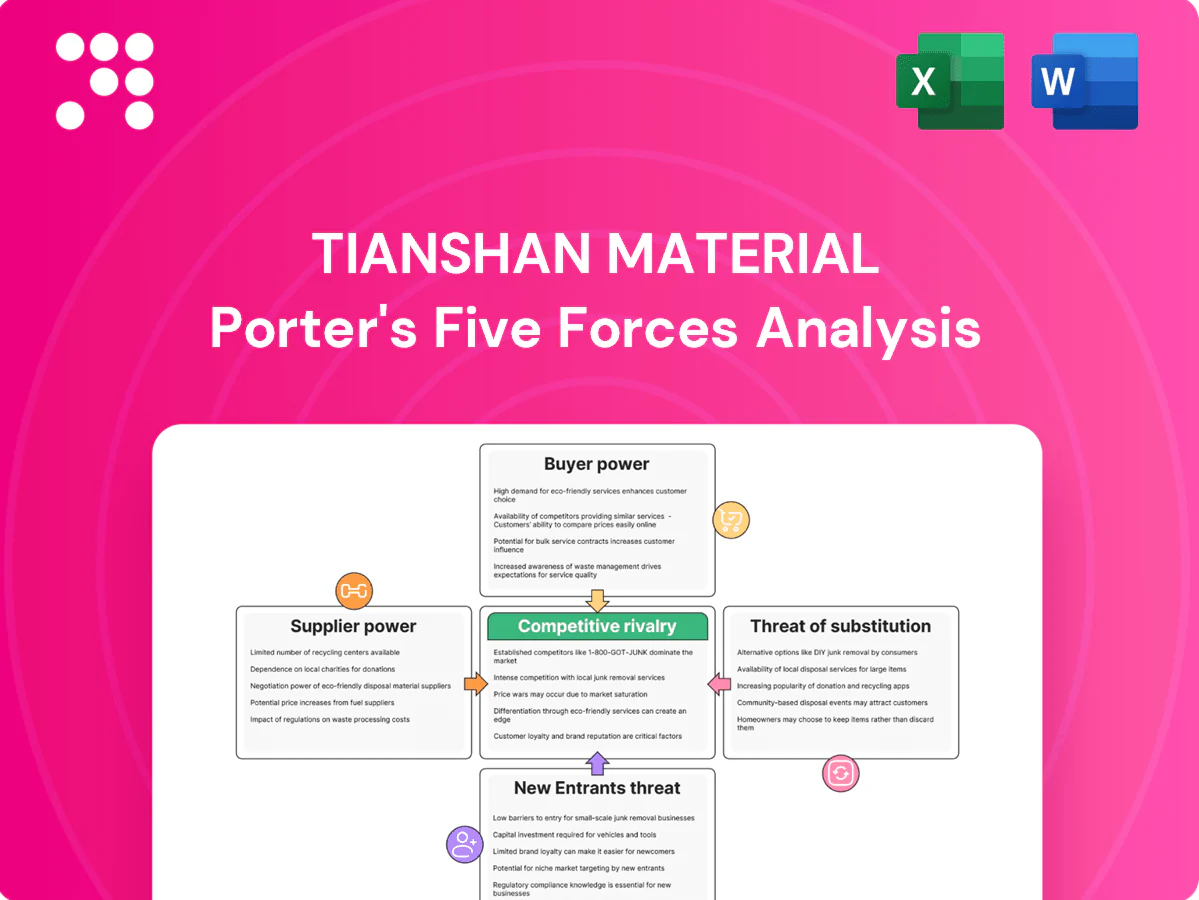

Tianshan Material Porter's Five Forces Analysis

This preview displays the exact Tianshan Material Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples. Instant download of this same document after payment.

A Must-Have Tool for Decision-Makers

Tianshan Material faces moderate supplier bargaining due to specialized inputs, intense rivalry from regional producers, and a growing threat from low-cost substitutes as downstream demand shifts; buyer power is rising with larger distributors consolidating. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Captive limestone mitigates input leverage

Core limestone is largely secured through captive or long-term quarry rights—commonly 20–30 year leases—limiting supplier bargaining power over Tianshan Material’s key input. This lowers price volatility and switching risk across Xinjiang and adjacent markets. Permitting timelines and reserve quality, however, still drive mining cost variance and capex timing. Supply interruptions tend to stem from regulatory or geological issues rather than vendor pricing pressure.

Energy and fuel suppliers hold moderate power

Thermal coal, petcoke and electricity drive ~25–35% of operating costs for materials handling in 2024, and regional energy rules plus transport constraints raise supplier leverage. Xinjiang’s remoteness adds ~10–15% to inbound logistics and heightens reliance on steady fuel flows. Multi-sourcing and fuel-mix flexibility blunt but cannot fully offset price spikes; industrial tariffs (≈0.5–0.9 RMB/kWh) and seasonal curtailments (up to 10–20% in peak months) increase bargaining pressure.

Gypsum and additives are substitutable

Gypsum, slag and other additives come from multiple regional mines and recycling streams, making them readily substitutable and capping any single supplier’s clout. Quality is governed by national GB and international standards, enabling competitive bidding across vendors. Proximity and freight remain key differentiators for landed cost, while long‑term contracts and safety stocks typically reduce supplier leverage further.

Equipment OEMs and spare parts exert episodic leverage

Equipment OEMs for kilns, mills and environmental controls are concentrated (major global suppliers dominate aftermarket supply), granting episodic pricing power during capex surges; long lead times and proprietary components frequently create lock‑in for service contracts. Lifecycle procurement, local fabrication and third‑party maintenance dilute recurring leverage, while plant digital monitoring enables predictive maintenance to avoid OEM premium emergencies.

- OEM concentration: episodic capex pricing power

- Long lead times/proprietary parts → service lock‑in

- Lifecycle buys + local fabrication reduce recurring dependence

- Digital monitoring enables predictive maintenance, lowers emergency spend

Logistics providers influence delivered cost

Rail and truck capacity in and out of Xinjiang directly shapes delivered cement pricing; 2024 peak-season truck rates spiked about 25% versus off-peak, and fuel comprises roughly 30% of short-haul trucking cost, shifting margins toward carriers during bottlenecks. Long-term rail allocations and owners running captive fleets have reduced transporter leverage, while proximity to demand centers remains the strongest countermeasure.

- Rail vs truck cost gap ~30–50%

- Peak truck rate rise ~25% (2024)

- Fuel ~30% of trucking opex

- Own-fleet/rail contracts cut supplier power

- Proximity to demand = primary hedge

Leases 20–30y curb supplier power; energy ~30% opex

Captive limestone leases (20–30y) and long‑term contracts curb supplier pricing power for core feedstock. Energy (thermal coal/petcoke/electricity) drives ~30% of 2024 opex and Xinjiang remoteness adds ~10–15% logistics premium, increasing supplier leverage. OEM concentration and long lead times create episodic capex/service lock‑in; peak truck rates jumped ~25% in 2024.

| Metric | 2024 Value |

|---|---|

| Limestone lease length | 20–30 years |

| Energy share of opex | ~30% |

| Logistics premium (remoteness) | 10–15% |

| Peak truck rate spike | ~25% |

| Rail vs truck gap | 30–50% |

| OEM concentration | High (episodic power) |

What is included in the product

Tailored exclusively for Tianshan Material, this Porter’s Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies disruptive threats and market dynamics shaping pricing and profitability.

Clear one-sheet Tianshan Material Five Forces summary for fast, board-ready decisions—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart for rapid scenario comparison.

Customers Bargaining Power

Large projects and SOE contractors negotiate hard

Large infrastructure and SOE EPC buyers command volume-based discounts and strict technical specs, squeezing margins as they bundle multi-site contracts to drive procurement leverage. Vendors compete on delivered reliability and extended credit terms to win business amid price pressure. Deep relationships and consistently on-time delivery can sustain per-project margins despite negotiated discounts. Industry reports show major EPC tenders favor suppliers offering integrated logistics and payment flexibility.

Ready-mix plants face low switching costs

Cement is a highly standardized commodity (global production ~4.4 billion tonnes in 2024), so RMC buyers switch suppliers quickly on price and logistics, driving frequent re-bidding and typically short-tenor contracts often under 12 months. Consistent quality and technical support create soft switching frictions that raise retention. Proximity and reliable peak-season supply further sustain customer stickiness.

Demand cyclicality strengthens buyer timing power

Demand cyclicality — with seasonal construction peaks in spring-summer and policy-driven pauses in late-year 2024 — shifts buyer timing power as purchasers defer orders in soft months to extract typical price cuts of 3–5%. Producers respond with production discipline and coordinated maintenance outages to support spot prices. Back-to-back logistics commitments lock in volumes and mitigate mid-cycle volatility.

Payment terms and credit raise hidden leverage

Extended receivables in construction chains shift financing costs onto suppliers, increasing effective cost of goods sold and pressuring margins; industry data (Intrum Payment Report 2024) showed average days beyond terms around 40 days in many markets, highlighting the scale of delayed payments. Downstream creditworthiness commonly dictates price concessions and allocation; tightening terms risks losing volume to rivals who absorb financing, while credit insurance and factoring partially offset buyer leverage.

- Receivables transfer financing burden

- Buyer credit shapes pricing/allocation

- Tighter terms can cost volume to financing-ready rivals

- Credit insurance/factoring reduce but do not eliminate leverage

Specification and performance service add value

Technical support for blended cements, low-heat mixes and durability specifications lets Tianshan Material differentiate offers; in 2024 critical infrastructure buyers typically accept 3–7% price premiums for proven performance, narrowing headline-price sensitivity. Lab services, onsite trials and precise delivery lower performance risk and shift procurement toward value metrics, marginally weakening buyer bargaining power in high-stakes applications.

- Performance-led premiums: 3–7% accepted

- Risk reduction: lab trials and QA raise switching costs

- Delivery precision: reduces focus on headline price

SOE/EPC price pressure; reliable delivery and 3–7% premiums protect suppliers

Large SOE/EPC buyers extract volume discounts and extended terms, cutting margins; key tenders favor integrated logistics and payment flexibility. Cement commoditization (global 4.4b t in 2024) and short contracts raise switching; performance premiums (3–7%) and reliable delivery limit full price pressure. Late payments (~40 days beyond terms) shift financing costs to suppliers and shape allocation.

| Metric | 2024 |

|---|---|

| Global cement | 4.4b t |

| Accepted premium | 3–7% |

| Days beyond terms | ~40 |

Preview Before You Purchase

Tianshan Material Porter's Five Forces Analysis

This preview displays the exact Tianshan Material Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples. Instant download of this same document after payment.

Description

A Must-Have Tool for Decision-Makers

Tianshan Material faces moderate supplier bargaining due to specialized inputs, intense rivalry from regional producers, and a growing threat from low-cost substitutes as downstream demand shifts; buyer power is rising with larger distributors consolidating. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Captive limestone mitigates input leverage

Core limestone is largely secured through captive or long-term quarry rights—commonly 20–30 year leases—limiting supplier bargaining power over Tianshan Material’s key input. This lowers price volatility and switching risk across Xinjiang and adjacent markets. Permitting timelines and reserve quality, however, still drive mining cost variance and capex timing. Supply interruptions tend to stem from regulatory or geological issues rather than vendor pricing pressure.

Energy and fuel suppliers hold moderate power

Thermal coal, petcoke and electricity drive ~25–35% of operating costs for materials handling in 2024, and regional energy rules plus transport constraints raise supplier leverage. Xinjiang’s remoteness adds ~10–15% to inbound logistics and heightens reliance on steady fuel flows. Multi-sourcing and fuel-mix flexibility blunt but cannot fully offset price spikes; industrial tariffs (≈0.5–0.9 RMB/kWh) and seasonal curtailments (up to 10–20% in peak months) increase bargaining pressure.

Gypsum and additives are substitutable

Gypsum, slag and other additives come from multiple regional mines and recycling streams, making them readily substitutable and capping any single supplier’s clout. Quality is governed by national GB and international standards, enabling competitive bidding across vendors. Proximity and freight remain key differentiators for landed cost, while long‑term contracts and safety stocks typically reduce supplier leverage further.

Equipment OEMs and spare parts exert episodic leverage

Equipment OEMs for kilns, mills and environmental controls are concentrated (major global suppliers dominate aftermarket supply), granting episodic pricing power during capex surges; long lead times and proprietary components frequently create lock‑in for service contracts. Lifecycle procurement, local fabrication and third‑party maintenance dilute recurring leverage, while plant digital monitoring enables predictive maintenance to avoid OEM premium emergencies.

- OEM concentration: episodic capex pricing power

- Long lead times/proprietary parts → service lock‑in

- Lifecycle buys + local fabrication reduce recurring dependence

- Digital monitoring enables predictive maintenance, lowers emergency spend

Logistics providers influence delivered cost

Rail and truck capacity in and out of Xinjiang directly shapes delivered cement pricing; 2024 peak-season truck rates spiked about 25% versus off-peak, and fuel comprises roughly 30% of short-haul trucking cost, shifting margins toward carriers during bottlenecks. Long-term rail allocations and owners running captive fleets have reduced transporter leverage, while proximity to demand centers remains the strongest countermeasure.

- Rail vs truck cost gap ~30–50%

- Peak truck rate rise ~25% (2024)

- Fuel ~30% of trucking opex

- Own-fleet/rail contracts cut supplier power

- Proximity to demand = primary hedge

Leases 20–30y curb supplier power; energy ~30% opex

Captive limestone leases (20–30y) and long‑term contracts curb supplier pricing power for core feedstock. Energy (thermal coal/petcoke/electricity) drives ~30% of 2024 opex and Xinjiang remoteness adds ~10–15% logistics premium, increasing supplier leverage. OEM concentration and long lead times create episodic capex/service lock‑in; peak truck rates jumped ~25% in 2024.

| Metric | 2024 Value |

|---|---|

| Limestone lease length | 20–30 years |

| Energy share of opex | ~30% |

| Logistics premium (remoteness) | 10–15% |

| Peak truck rate spike | ~25% |

| Rail vs truck gap | 30–50% |

| OEM concentration | High (episodic power) |

What is included in the product

Tailored exclusively for Tianshan Material, this Porter’s Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies disruptive threats and market dynamics shaping pricing and profitability.

Clear one-sheet Tianshan Material Five Forces summary for fast, board-ready decisions—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart for rapid scenario comparison.

Customers Bargaining Power

Large projects and SOE contractors negotiate hard

Large infrastructure and SOE EPC buyers command volume-based discounts and strict technical specs, squeezing margins as they bundle multi-site contracts to drive procurement leverage. Vendors compete on delivered reliability and extended credit terms to win business amid price pressure. Deep relationships and consistently on-time delivery can sustain per-project margins despite negotiated discounts. Industry reports show major EPC tenders favor suppliers offering integrated logistics and payment flexibility.

Ready-mix plants face low switching costs

Cement is a highly standardized commodity (global production ~4.4 billion tonnes in 2024), so RMC buyers switch suppliers quickly on price and logistics, driving frequent re-bidding and typically short-tenor contracts often under 12 months. Consistent quality and technical support create soft switching frictions that raise retention. Proximity and reliable peak-season supply further sustain customer stickiness.

Demand cyclicality strengthens buyer timing power

Demand cyclicality — with seasonal construction peaks in spring-summer and policy-driven pauses in late-year 2024 — shifts buyer timing power as purchasers defer orders in soft months to extract typical price cuts of 3–5%. Producers respond with production discipline and coordinated maintenance outages to support spot prices. Back-to-back logistics commitments lock in volumes and mitigate mid-cycle volatility.

Payment terms and credit raise hidden leverage

Extended receivables in construction chains shift financing costs onto suppliers, increasing effective cost of goods sold and pressuring margins; industry data (Intrum Payment Report 2024) showed average days beyond terms around 40 days in many markets, highlighting the scale of delayed payments. Downstream creditworthiness commonly dictates price concessions and allocation; tightening terms risks losing volume to rivals who absorb financing, while credit insurance and factoring partially offset buyer leverage.

- Receivables transfer financing burden

- Buyer credit shapes pricing/allocation

- Tighter terms can cost volume to financing-ready rivals

- Credit insurance/factoring reduce but do not eliminate leverage

Specification and performance service add value

Technical support for blended cements, low-heat mixes and durability specifications lets Tianshan Material differentiate offers; in 2024 critical infrastructure buyers typically accept 3–7% price premiums for proven performance, narrowing headline-price sensitivity. Lab services, onsite trials and precise delivery lower performance risk and shift procurement toward value metrics, marginally weakening buyer bargaining power in high-stakes applications.

- Performance-led premiums: 3–7% accepted

- Risk reduction: lab trials and QA raise switching costs

- Delivery precision: reduces focus on headline price

SOE/EPC price pressure; reliable delivery and 3–7% premiums protect suppliers

Large SOE/EPC buyers extract volume discounts and extended terms, cutting margins; key tenders favor integrated logistics and payment flexibility. Cement commoditization (global 4.4b t in 2024) and short contracts raise switching; performance premiums (3–7%) and reliable delivery limit full price pressure. Late payments (~40 days beyond terms) shift financing costs to suppliers and shape allocation.

| Metric | 2024 |

|---|---|

| Global cement | 4.4b t |

| Accepted premium | 3–7% |

| Days beyond terms | ~40 |

Preview Before You Purchase

Tianshan Material Porter's Five Forces Analysis

This preview displays the exact Tianshan Material Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples. Instant download of this same document after payment.