Tianshan Material PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

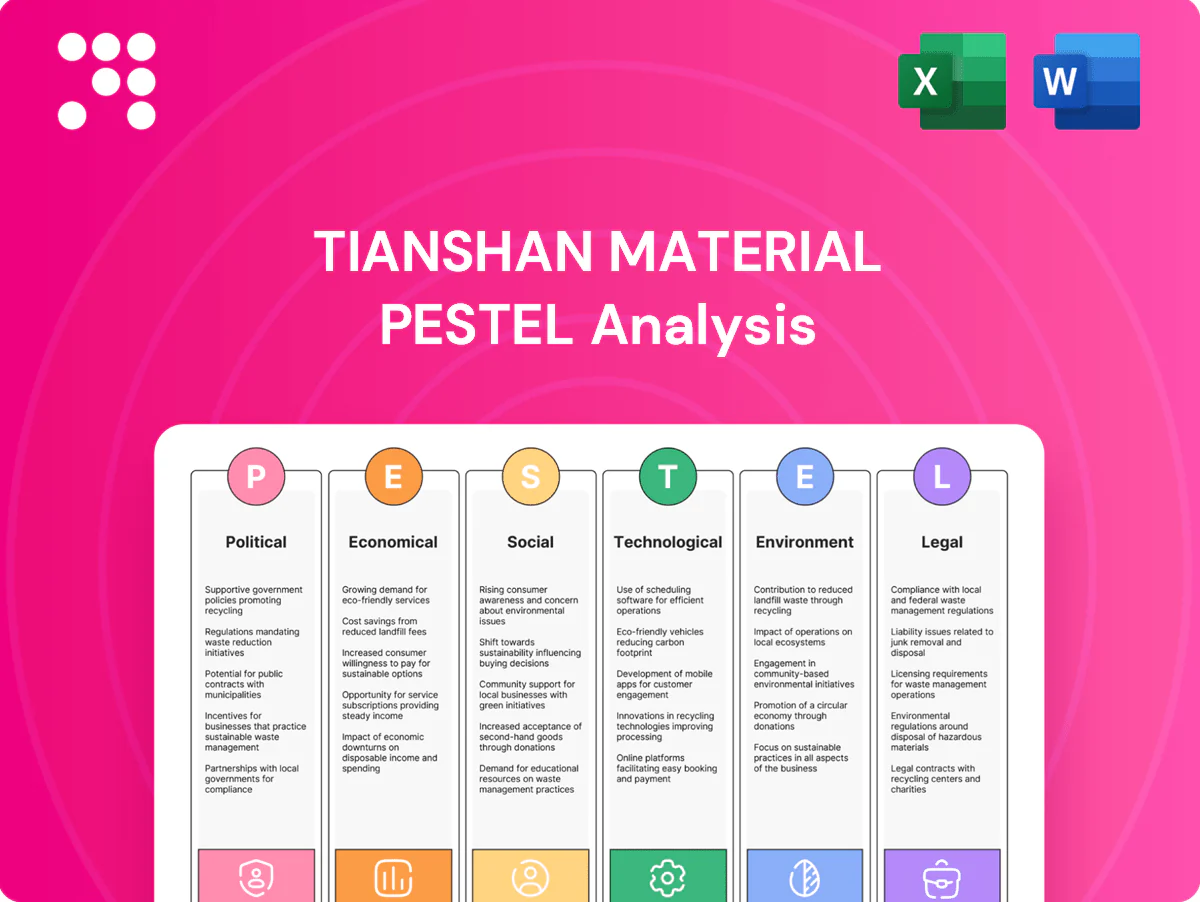

Gain strategic clarity with our PESTLE Analysis tailored to Tianshan Material—mapping political, economic, social, technological, legal, and environmental forces shaping its outlook. Perfect for investors and strategists seeking actionable intelligence. Purchase the full report now for the complete, editable breakdown and immediate insights.

Political factors

Infrastructure-led stimulus

China’s central and provincial governments periodically deploy infrastructure stimulus—2024 special local government bond quota of 3.65 trillion yuan underpins project pipelines—driving sharp upticks in cement demand in Xinjiang and neighbouring regions tied to transport, energy and urban projects. Pipeline visibility hinges on budget allocations and policy priority; execution speed and tender cadence directly determine plant utilization and short-term revenue for Tianshan Material.

Regional policy priorities

Xinjiang-focused development under the 14th Five-Year Plan (2021–25) steers Tianshan Material’s project mix, timelines, and access to central subsidies and regional financing. Preferential policies under this framework often ease logistics, land allocation, and energy access, lowering start-up barriers for industrial projects. Sudden shifts in regional emphasis can reallocate funding and permits within months, while policy continuity across the plan period is critical for multi-year capacity planning.

Government pricing and oversight

Authorities closely monitor construction input prices to curb inflation; China's CPI rose about 0.3% year-on-year in 2024, keeping oversight active and putting pressure on input costs. Guidance and scrutiny on cement pricing—after a roughly 5% year-on-year decline in the national cement price index in 2024—can compress Tianshan Material margins. Administrative peak-season production controls aim to balance supply and demand, and strict compliance avoids fines and sales disruptions.

Belt and Road linkages

Belt and Road corridors crossing Western China can catalyze cement demand for roads, rails and logistics hubs as BRI involved 150+ countries and 3,000+ projects by 2024, boosting regional infrastructure pipelines relevant to Tianshan Material. Cross-border projects may open sales and JV opportunities, but timelines are highly sensitive to geopolitical relations and sanctions risks. Closer coordination with SOEs and provincial authorities like Xinjiang investment arms improves project access and bidding success.

- BRI scale: 150+ countries, 3,000+ projects (2024)

- Opportunities: sales, JVs, logistics hub construction

- Risks: geopolitical delays, sanction exposure

- Mitigation: coordinate with SOEs and provincial partners

Stability and security conditions

Security protocols in Xinjiang materially affect labor mobility, logistics, and site access for Tianshan Material, with checkpoints and access controls adding administrative steps that can slow crew rotations and equipment movement. Additional compliance and vetting procedures often elongate procurement and delivery timelines, increasing lead-time variability. Stable security conditions support predictable operations, while disruptions raise transport costs and inventory risk.

- operational access: restricted sites increase scheduling risk

- procurement: extra vetting -> longer lead times

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

Central/provincial infrastructure stimulus (2024 special local government bond quota 3.65 trillion yuan) and 14th Five-Year Plan priorities drive Xinjiang cement demand and access to subsidies, but allocation shifts affect project timing. 2024 CPI ~0.3% and a ~5% y/y national cement price decline compress margins while production controls raise compliance risk. BRI scale (150+ countries, 3,000+ projects by 2024) expands export/JV prospects; Xinjiang security measures increase logistics and staffing costs.

| Indicator | 2024/data |

|---|---|

| Local govt bond quota | 3.65 trillion yuan |

| CPI | ~0.3% y/y |

| Cement price index | ~-5% y/y |

| BRI scale | 150+ countries; 3,000+ projects |

What is included in the product

Provides a concise PESTLE assessment of Tianshan Material across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current regional industry data and trends to reveal risks, opportunities and forward-looking implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Tianshan Material that simplifies external risk assessment, is easily edited for local context, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Property cycle exposure

China’s real estate slowdown has cut bagged cement demand sharply, with property-related activity accounting for roughly 25% of GDP and real estate investment down materially through 2023–24. Mix shifts toward infrastructure and public works—where government-led investment rose in 2024—are critical offsets for Tianshan Material. Pricing power weakens in down-cycles as finished goods inventories and regional overcapacity rise. Cash collection risk increases as stressed developers show higher default rates and delayed payments.

Energy and fuel volatility

Fuel (coal, petcoke, electricity) typically represents 40–60% of kiln cash costs, so spot price swings have rapidly shifted unit cash costs and margins in 2022–24. Long‑term fuel contracts, fuel‑switching (petcoke/biomass/waste) and kiln efficiency lower unit fuel use. Hedging programs and large procurement scale materially differentiate peer margins.

Overcapacity and consolidation

Regional overcapacity in China — total cement capacity around 2.2 billion tonnes in 2024 with utilization near 70% — fuels price competition and forces off-peak kiln shutdowns; industry consolidation and joint operations have risen, with top groups increasing market share to curb volatility. Clinker swaps and optimized kiln runs cut freight and improve load factors, while asset rationalization and plant closures have lifted peer ROCEs into the mid-teens in recent years.

Logistics and geography

- freight-to-value: elevated by ~3,500–4,000 km haul

- rail/bulk: primary determinants of delivered price

- seasonality: winter −30°C, spring thaw impacts

- proximity: Urumqi/regional hubs preserve margin

Credit and liquidity conditions

Infrastructure funding for Tianshan relies heavily on local government financing and bank appetite; China set a 2024 local government special bond quota of about 3.95 trillion CNY, while 1‑year and 5‑year LPRs stood at 3.45% and 4.30% respectively, impacting borrowing costs. Tighter credit and slower bank loan growth stretch receivables and delay project starts, whereas easing credit boosts new tenders and working capital, and cost of capital shapes timing of capacity upgrades.

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

China’s real estate slowdown cut bagged cement demand (property ≈25% of GDP; investment down through 2023–24), shifting mix to infrastructure as 2024 govt spending rose. Fuel = 40–60% of kiln cash costs, spot swings hit margins; hedging and scale differentiate peers. Industry capacity ≈2.2bn t, utilization ~70% (2024); long hauls 3,500–4,000 km raise freight; local bond quota 3.95T CNY, LPRs 3.45/4.30%.

| Metric | 2024 |

|---|---|

| Property share of GDP | ≈25% |

| Cement capacity | ≈2.2bn t |

| Utilization | ~70% |

| Fuel % of cash cost | 40–60% |

| Freight haul | 3,500–4,000 km |

| Local bond quota | 3.95T CNY |

| LPR (1y/5y) | 3.45% / 4.30% |

Full Version Awaits

Tianshan Material PESTLE Analysis

The Tianshan Material PESTLE Analysis provides a concise, professionally formatted assessment of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or edits required; download the finished file immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis tailored to Tianshan Material—mapping political, economic, social, technological, legal, and environmental forces shaping its outlook. Perfect for investors and strategists seeking actionable intelligence. Purchase the full report now for the complete, editable breakdown and immediate insights.

Political factors

Infrastructure-led stimulus

China’s central and provincial governments periodically deploy infrastructure stimulus—2024 special local government bond quota of 3.65 trillion yuan underpins project pipelines—driving sharp upticks in cement demand in Xinjiang and neighbouring regions tied to transport, energy and urban projects. Pipeline visibility hinges on budget allocations and policy priority; execution speed and tender cadence directly determine plant utilization and short-term revenue for Tianshan Material.

Regional policy priorities

Xinjiang-focused development under the 14th Five-Year Plan (2021–25) steers Tianshan Material’s project mix, timelines, and access to central subsidies and regional financing. Preferential policies under this framework often ease logistics, land allocation, and energy access, lowering start-up barriers for industrial projects. Sudden shifts in regional emphasis can reallocate funding and permits within months, while policy continuity across the plan period is critical for multi-year capacity planning.

Government pricing and oversight

Authorities closely monitor construction input prices to curb inflation; China's CPI rose about 0.3% year-on-year in 2024, keeping oversight active and putting pressure on input costs. Guidance and scrutiny on cement pricing—after a roughly 5% year-on-year decline in the national cement price index in 2024—can compress Tianshan Material margins. Administrative peak-season production controls aim to balance supply and demand, and strict compliance avoids fines and sales disruptions.

Belt and Road linkages

Belt and Road corridors crossing Western China can catalyze cement demand for roads, rails and logistics hubs as BRI involved 150+ countries and 3,000+ projects by 2024, boosting regional infrastructure pipelines relevant to Tianshan Material. Cross-border projects may open sales and JV opportunities, but timelines are highly sensitive to geopolitical relations and sanctions risks. Closer coordination with SOEs and provincial authorities like Xinjiang investment arms improves project access and bidding success.

- BRI scale: 150+ countries, 3,000+ projects (2024)

- Opportunities: sales, JVs, logistics hub construction

- Risks: geopolitical delays, sanction exposure

- Mitigation: coordinate with SOEs and provincial partners

Stability and security conditions

Security protocols in Xinjiang materially affect labor mobility, logistics, and site access for Tianshan Material, with checkpoints and access controls adding administrative steps that can slow crew rotations and equipment movement. Additional compliance and vetting procedures often elongate procurement and delivery timelines, increasing lead-time variability. Stable security conditions support predictable operations, while disruptions raise transport costs and inventory risk.

- operational access: restricted sites increase scheduling risk

- procurement: extra vetting -> longer lead times

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

Central/provincial infrastructure stimulus (2024 special local government bond quota 3.65 trillion yuan) and 14th Five-Year Plan priorities drive Xinjiang cement demand and access to subsidies, but allocation shifts affect project timing. 2024 CPI ~0.3% and a ~5% y/y national cement price decline compress margins while production controls raise compliance risk. BRI scale (150+ countries, 3,000+ projects by 2024) expands export/JV prospects; Xinjiang security measures increase logistics and staffing costs.

| Indicator | 2024/data |

|---|---|

| Local govt bond quota | 3.65 trillion yuan |

| CPI | ~0.3% y/y |

| Cement price index | ~-5% y/y |

| BRI scale | 150+ countries; 3,000+ projects |

What is included in the product

Provides a concise PESTLE assessment of Tianshan Material across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current regional industry data and trends to reveal risks, opportunities and forward-looking implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Tianshan Material that simplifies external risk assessment, is easily edited for local context, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Property cycle exposure

China’s real estate slowdown has cut bagged cement demand sharply, with property-related activity accounting for roughly 25% of GDP and real estate investment down materially through 2023–24. Mix shifts toward infrastructure and public works—where government-led investment rose in 2024—are critical offsets for Tianshan Material. Pricing power weakens in down-cycles as finished goods inventories and regional overcapacity rise. Cash collection risk increases as stressed developers show higher default rates and delayed payments.

Energy and fuel volatility

Fuel (coal, petcoke, electricity) typically represents 40–60% of kiln cash costs, so spot price swings have rapidly shifted unit cash costs and margins in 2022–24. Long‑term fuel contracts, fuel‑switching (petcoke/biomass/waste) and kiln efficiency lower unit fuel use. Hedging programs and large procurement scale materially differentiate peer margins.

Overcapacity and consolidation

Regional overcapacity in China — total cement capacity around 2.2 billion tonnes in 2024 with utilization near 70% — fuels price competition and forces off-peak kiln shutdowns; industry consolidation and joint operations have risen, with top groups increasing market share to curb volatility. Clinker swaps and optimized kiln runs cut freight and improve load factors, while asset rationalization and plant closures have lifted peer ROCEs into the mid-teens in recent years.

Logistics and geography

- freight-to-value: elevated by ~3,500–4,000 km haul

- rail/bulk: primary determinants of delivered price

- seasonality: winter −30°C, spring thaw impacts

- proximity: Urumqi/regional hubs preserve margin

Credit and liquidity conditions

Infrastructure funding for Tianshan relies heavily on local government financing and bank appetite; China set a 2024 local government special bond quota of about 3.95 trillion CNY, while 1‑year and 5‑year LPRs stood at 3.45% and 4.30% respectively, impacting borrowing costs. Tighter credit and slower bank loan growth stretch receivables and delay project starts, whereas easing credit boosts new tenders and working capital, and cost of capital shapes timing of capacity upgrades.

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

China’s real estate slowdown cut bagged cement demand (property ≈25% of GDP; investment down through 2023–24), shifting mix to infrastructure as 2024 govt spending rose. Fuel = 40–60% of kiln cash costs, spot swings hit margins; hedging and scale differentiate peers. Industry capacity ≈2.2bn t, utilization ~70% (2024); long hauls 3,500–4,000 km raise freight; local bond quota 3.95T CNY, LPRs 3.45/4.30%.

| Metric | 2024 |

|---|---|

| Property share of GDP | ≈25% |

| Cement capacity | ≈2.2bn t |

| Utilization | ~70% |

| Fuel % of cash cost | 40–60% |

| Freight haul | 3,500–4,000 km |

| Local bond quota | 3.95T CNY |

| LPR (1y/5y) | 3.45% / 4.30% |

Full Version Awaits

Tianshan Material PESTLE Analysis

The Tianshan Material PESTLE Analysis provides a concise, professionally formatted assessment of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or edits required; download the finished file immediately after checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis tailored to Tianshan Material—mapping political, economic, social, technological, legal, and environmental forces shaping its outlook. Perfect for investors and strategists seeking actionable intelligence. Purchase the full report now for the complete, editable breakdown and immediate insights.

Political factors

Infrastructure-led stimulus

China’s central and provincial governments periodically deploy infrastructure stimulus—2024 special local government bond quota of 3.65 trillion yuan underpins project pipelines—driving sharp upticks in cement demand in Xinjiang and neighbouring regions tied to transport, energy and urban projects. Pipeline visibility hinges on budget allocations and policy priority; execution speed and tender cadence directly determine plant utilization and short-term revenue for Tianshan Material.

Regional policy priorities

Xinjiang-focused development under the 14th Five-Year Plan (2021–25) steers Tianshan Material’s project mix, timelines, and access to central subsidies and regional financing. Preferential policies under this framework often ease logistics, land allocation, and energy access, lowering start-up barriers for industrial projects. Sudden shifts in regional emphasis can reallocate funding and permits within months, while policy continuity across the plan period is critical for multi-year capacity planning.

Government pricing and oversight

Authorities closely monitor construction input prices to curb inflation; China's CPI rose about 0.3% year-on-year in 2024, keeping oversight active and putting pressure on input costs. Guidance and scrutiny on cement pricing—after a roughly 5% year-on-year decline in the national cement price index in 2024—can compress Tianshan Material margins. Administrative peak-season production controls aim to balance supply and demand, and strict compliance avoids fines and sales disruptions.

Belt and Road linkages

Belt and Road corridors crossing Western China can catalyze cement demand for roads, rails and logistics hubs as BRI involved 150+ countries and 3,000+ projects by 2024, boosting regional infrastructure pipelines relevant to Tianshan Material. Cross-border projects may open sales and JV opportunities, but timelines are highly sensitive to geopolitical relations and sanctions risks. Closer coordination with SOEs and provincial authorities like Xinjiang investment arms improves project access and bidding success.

- BRI scale: 150+ countries, 3,000+ projects (2024)

- Opportunities: sales, JVs, logistics hub construction

- Risks: geopolitical delays, sanction exposure

- Mitigation: coordinate with SOEs and provincial partners

Stability and security conditions

Security protocols in Xinjiang materially affect labor mobility, logistics, and site access for Tianshan Material, with checkpoints and access controls adding administrative steps that can slow crew rotations and equipment movement. Additional compliance and vetting procedures often elongate procurement and delivery timelines, increasing lead-time variability. Stable security conditions support predictable operations, while disruptions raise transport costs and inventory risk.

- operational access: restricted sites increase scheduling risk

- procurement: extra vetting -> longer lead times

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

Central/provincial infrastructure stimulus (2024 special local government bond quota 3.65 trillion yuan) and 14th Five-Year Plan priorities drive Xinjiang cement demand and access to subsidies, but allocation shifts affect project timing. 2024 CPI ~0.3% and a ~5% y/y national cement price decline compress margins while production controls raise compliance risk. BRI scale (150+ countries, 3,000+ projects by 2024) expands export/JV prospects; Xinjiang security measures increase logistics and staffing costs.

| Indicator | 2024/data |

|---|---|

| Local govt bond quota | 3.65 trillion yuan |

| CPI | ~0.3% y/y |

| Cement price index | ~-5% y/y |

| BRI scale | 150+ countries; 3,000+ projects |

What is included in the product

Provides a concise PESTLE assessment of Tianshan Material across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current regional industry data and trends to reveal risks, opportunities and forward-looking implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Tianshan Material that simplifies external risk assessment, is easily edited for local context, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Property cycle exposure

China’s real estate slowdown has cut bagged cement demand sharply, with property-related activity accounting for roughly 25% of GDP and real estate investment down materially through 2023–24. Mix shifts toward infrastructure and public works—where government-led investment rose in 2024—are critical offsets for Tianshan Material. Pricing power weakens in down-cycles as finished goods inventories and regional overcapacity rise. Cash collection risk increases as stressed developers show higher default rates and delayed payments.

Energy and fuel volatility

Fuel (coal, petcoke, electricity) typically represents 40–60% of kiln cash costs, so spot price swings have rapidly shifted unit cash costs and margins in 2022–24. Long‑term fuel contracts, fuel‑switching (petcoke/biomass/waste) and kiln efficiency lower unit fuel use. Hedging programs and large procurement scale materially differentiate peer margins.

Overcapacity and consolidation

Regional overcapacity in China — total cement capacity around 2.2 billion tonnes in 2024 with utilization near 70% — fuels price competition and forces off-peak kiln shutdowns; industry consolidation and joint operations have risen, with top groups increasing market share to curb volatility. Clinker swaps and optimized kiln runs cut freight and improve load factors, while asset rationalization and plant closures have lifted peer ROCEs into the mid-teens in recent years.

Logistics and geography

- freight-to-value: elevated by ~3,500–4,000 km haul

- rail/bulk: primary determinants of delivered price

- seasonality: winter −30°C, spring thaw impacts

- proximity: Urumqi/regional hubs preserve margin

Credit and liquidity conditions

Infrastructure funding for Tianshan relies heavily on local government financing and bank appetite; China set a 2024 local government special bond quota of about 3.95 trillion CNY, while 1‑year and 5‑year LPRs stood at 3.45% and 4.30% respectively, impacting borrowing costs. Tighter credit and slower bank loan growth stretch receivables and delay project starts, whereas easing credit boosts new tenders and working capital, and cost of capital shapes timing of capacity upgrades.

Infrastructure, 14th Plan boost Xinjiang cement demand; bond quota 3.65T

China’s real estate slowdown cut bagged cement demand (property ≈25% of GDP; investment down through 2023–24), shifting mix to infrastructure as 2024 govt spending rose. Fuel = 40–60% of kiln cash costs, spot swings hit margins; hedging and scale differentiate peers. Industry capacity ≈2.2bn t, utilization ~70% (2024); long hauls 3,500–4,000 km raise freight; local bond quota 3.95T CNY, LPRs 3.45/4.30%.

| Metric | 2024 |

|---|---|

| Property share of GDP | ≈25% |

| Cement capacity | ≈2.2bn t |

| Utilization | ~70% |

| Fuel % of cash cost | 40–60% |

| Freight haul | 3,500–4,000 km |

| Local bond quota | 3.95T CNY |

| LPR (1y/5y) | 3.45% / 4.30% |

Full Version Awaits

Tianshan Material PESTLE Analysis

The Tianshan Material PESTLE Analysis provides a concise, professionally formatted assessment of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or edits required; download the finished file immediately after checkout.