Tile Shop Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

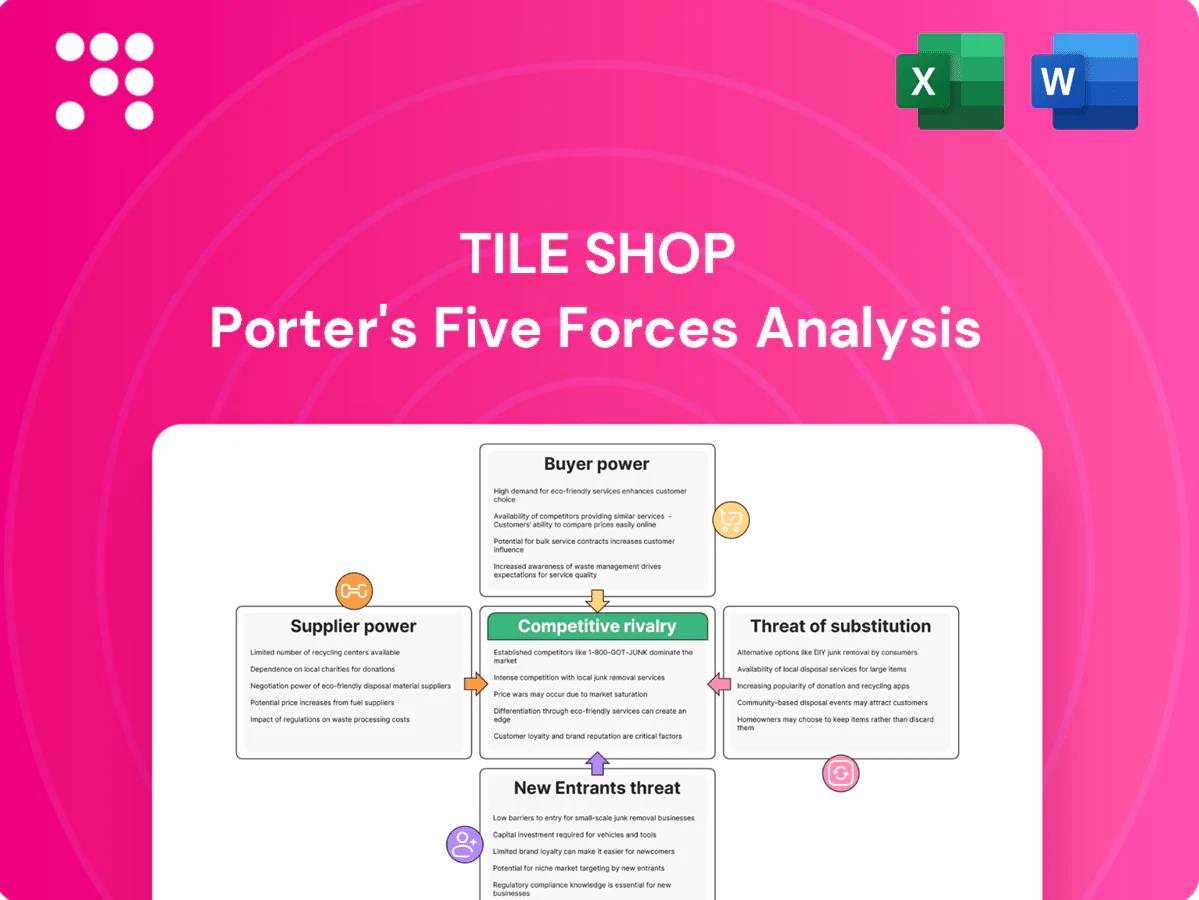

Tile Shop faces moderate buyer power, intense rivalry from big-box and online retailers, supplier leverage in specialty lines, and limited but present threats from substitutes and new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tile Shop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global quarry reliance

Many tiles and natural stone used by Tile Shop are sourced from concentrated overseas quarries and factories—suppliers in Italy, Spain, China and India dominate the upstream market—giving vendors leverage on pricing and allocation; U.S. ceramic tile imports totaled about $1.8 billion in 2024, and currency swings plus geopolitical risks (e.g., trade tensions) amplify supplier power and input-cost volatility.

Differentiated natural stone

Unique veining, finishes, and rare stones give suppliers strong leverage over Tile Shop, since differentiated slabs cannot be easily substituted; the global natural stone market was valued at about USD 54.9 billion in 2023, underscoring supplier market heft. Limited alternatives for specific aesthetics raise dependence, allowing suppliers to impose minimum order sizes and tighter payment and delivery terms. Suppliers' control over rare inventory can compress Tile Shop's margins and inventory flexibility.

High logistics costs

Tiles are heavy, fragile, and expensive to ship, pushing inbound freight to a material share of COGS and compressing gross margins for retailers like Tile Shop; in 2024 freight volatility continued to raise landed costs across building materials. Elevated handling and specialized packaging increase switching costs, reducing buyers’ leverage. Port delays and spot-rate swings in 2024 shifted short-term bargaining power toward suppliers and carriers.

Private-label leverage

Developing exclusive private-label lines reduces direct price comparability by differentiating Tile Shop’s assortment and supporting higher margin capture; committing volume to select vendors slightly rebalances supplier power by securing better pricing and terms. However, exclusivity can increase dependence on a few partners, raising supply risk if a vendor faces disruption or negotiates harder on other contract terms. In 2024 this strategy remains a key lever for retail margin management.

- Private-label reduces price transparency

- Volume commitments yield better terms

- Heightened vendor concentration risk

- 2024: continued focus on private assortments

Multi-sourcing and contracts

Multi-sourcing across regions and locking in volume contracts reduces exposure to raw-material and freight swings; firms that secured 60%–75% of annual tile volumes in firm contracts in 2024 reported more stable input costs. Long-term supplier relationships improved quality consistency and fill rates, supporting in-stock levels above 95% in leading specialty retailers. This approach partially mitigates supplier bargaining power but does not eliminate risks from concentrated raw-material suppliers.

- Coverage: 60%–75% of annual volumes contracted (2024)

- Fill rates: >95% for established supplier networks

- Effect: ~12% lower input-cost volatility vs spot purchasing

Concentrated overseas quarries raise supplier leverage, freight and allocation risks

Supplier power is high for Tile Shop due to concentrated overseas quarry/factory sources (U.S. ceramic tile imports ~$1.8B in 2024) and differentiated natural stone (global market ~$54.9B in 2023), raising price and allocation risk; multi-sourcing and 60%–75% volume contracts in 2024 cut input volatility ~12% but dependence on key vendors and freight pressure (affecting landed costs) keeps leverage elevated.

| Metric | Value |

|---|---|

| US tile imports (2024) | $1.8B |

| Global natural stone (2023) | $54.9B |

| Contracted volume (2024) | 60%–75% |

| Input-volatility reduction | ~12% |

| Fill rates (leading retailers) | >95% |

What is included in the product

Uncovers Tile Shop’s competitive pressures by analyzing rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory dynamics; highlights disruptive trends, entry barriers, and pricing levers that shape its market position and profitability.

A clear, one-sheet summary of Tile Shop's five forces—perfect for quick decision-making and slide-ready boardroom use.

Customers Bargaining Power

Fragmented customer base

Homeowners and small contractors drive the bulk of Tile Shop demand, with the chain operating roughly 120 stores in 2024, which concentrates sales in fragmented, retail-sized orders. Average ticket sizes vary widely by bathroom or kitchen project but remain dispersed across many small purchases. This dispersion limits individual negotiating clout and generally keeps buyer power moderate.

Price transparency online

E-commerce listings and comparison sites mean shoppers can check Tile Shop prices instantly; e-commerce accounted for about 17% of US retail sales in 2024, increasing visibility of SKUs. Buyers benchmark Tile Shop SKUs and alternatives across marketplaces in seconds, with surveys showing roughly 72% of home-improvement shoppers compare prices online in 2024. This transparency heightens discount pressure and elevates buyer bargaining power, compressing gross margin potential.

Low switching costs

Customers can switch to big-box chains (Home Depot, Lowe's), specialty rivals, or online marketplaces with minimal friction; 2024 data show online share of home improvement product purchases grew to roughly 20%, raising comparison shopping. If professional installation has not started, consumers frequently swap or return tile choices, keeping inventory turnover high for retailers. This flexibility amplifies buyer leverage on promotions, price matching, and return policies, pressuring Tile Shop margins.

Design and installation support

Showroom design help, samples, and project guidance raise perceived value and soften price resistance, enabling modest premiums and higher margin capture on projects. Advisory services and bundled setting materials create stickiness and higher lifetime value by simplifying purchase decisions. These service-led differentiators reduce buyer price sensitivity at the margin and support project-based upsells.

- Showroom design help

- Samples and project guidance

- Advisory services + bundled materials

- Lower marginal price sensitivity

Project-driven purchasing

Orders tied to contractor schedules make purchasing urgent and reduce buyer leverage; in 2024, 62% of renovations were reported as time-sensitive, limiting shopping around (Home Improvement Research Institute 2024). Urgency and stock/delivery speed often override small price differences, so availability and fast fulfillment strengthen seller position during projects.

- Project urgency: reduces buyer bargaining

- Stock & delivery: trump small price gaps

- Contractor schedules: drive purchase timing

Moderate buyer power as 72% compare prices and online channels rise

Buyers have moderate power: Tile Shop’s ~120 stores concentrate many small-ticket homeowners/contractor purchases that limit single-buyer leverage, but online price transparency raises pressure. In 2024 about 72% of shoppers compared prices and e-commerce represented ~17% of US retail; home-improvement online share ~20%, and 62% of renovations were time-sensitive, shifting leverage to sellers for urgent fulfillment.

| Metric | 2024 Value |

|---|---|

| Tile Shop stores | ~120 |

| Shoppers comparing prices | 72% |

| E-commerce share (US retail) | 17% |

| Home-improvement online share | 20% |

| Time-sensitive renovations | 62% |

Same Document Delivered

Tile Shop Porter's Five Forces Analysis

This Tile Shop Porter's Five Forces Analysis delivers a concise evaluation of competitive rivalry, buyer and supplier power, and threats of entry and substitution, with clear strategic implications. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted. It is ready for instant download and immediate use in decision-making or reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Tile Shop faces moderate buyer power, intense rivalry from big-box and online retailers, supplier leverage in specialty lines, and limited but present threats from substitutes and new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tile Shop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global quarry reliance

Many tiles and natural stone used by Tile Shop are sourced from concentrated overseas quarries and factories—suppliers in Italy, Spain, China and India dominate the upstream market—giving vendors leverage on pricing and allocation; U.S. ceramic tile imports totaled about $1.8 billion in 2024, and currency swings plus geopolitical risks (e.g., trade tensions) amplify supplier power and input-cost volatility.

Differentiated natural stone

Unique veining, finishes, and rare stones give suppliers strong leverage over Tile Shop, since differentiated slabs cannot be easily substituted; the global natural stone market was valued at about USD 54.9 billion in 2023, underscoring supplier market heft. Limited alternatives for specific aesthetics raise dependence, allowing suppliers to impose minimum order sizes and tighter payment and delivery terms. Suppliers' control over rare inventory can compress Tile Shop's margins and inventory flexibility.

High logistics costs

Tiles are heavy, fragile, and expensive to ship, pushing inbound freight to a material share of COGS and compressing gross margins for retailers like Tile Shop; in 2024 freight volatility continued to raise landed costs across building materials. Elevated handling and specialized packaging increase switching costs, reducing buyers’ leverage. Port delays and spot-rate swings in 2024 shifted short-term bargaining power toward suppliers and carriers.

Private-label leverage

Developing exclusive private-label lines reduces direct price comparability by differentiating Tile Shop’s assortment and supporting higher margin capture; committing volume to select vendors slightly rebalances supplier power by securing better pricing and terms. However, exclusivity can increase dependence on a few partners, raising supply risk if a vendor faces disruption or negotiates harder on other contract terms. In 2024 this strategy remains a key lever for retail margin management.

- Private-label reduces price transparency

- Volume commitments yield better terms

- Heightened vendor concentration risk

- 2024: continued focus on private assortments

Multi-sourcing and contracts

Multi-sourcing across regions and locking in volume contracts reduces exposure to raw-material and freight swings; firms that secured 60%–75% of annual tile volumes in firm contracts in 2024 reported more stable input costs. Long-term supplier relationships improved quality consistency and fill rates, supporting in-stock levels above 95% in leading specialty retailers. This approach partially mitigates supplier bargaining power but does not eliminate risks from concentrated raw-material suppliers.

- Coverage: 60%–75% of annual volumes contracted (2024)

- Fill rates: >95% for established supplier networks

- Effect: ~12% lower input-cost volatility vs spot purchasing

Concentrated overseas quarries raise supplier leverage, freight and allocation risks

Supplier power is high for Tile Shop due to concentrated overseas quarry/factory sources (U.S. ceramic tile imports ~$1.8B in 2024) and differentiated natural stone (global market ~$54.9B in 2023), raising price and allocation risk; multi-sourcing and 60%–75% volume contracts in 2024 cut input volatility ~12% but dependence on key vendors and freight pressure (affecting landed costs) keeps leverage elevated.

| Metric | Value |

|---|---|

| US tile imports (2024) | $1.8B |

| Global natural stone (2023) | $54.9B |

| Contracted volume (2024) | 60%–75% |

| Input-volatility reduction | ~12% |

| Fill rates (leading retailers) | >95% |

What is included in the product

Uncovers Tile Shop’s competitive pressures by analyzing rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory dynamics; highlights disruptive trends, entry barriers, and pricing levers that shape its market position and profitability.

A clear, one-sheet summary of Tile Shop's five forces—perfect for quick decision-making and slide-ready boardroom use.

Customers Bargaining Power

Fragmented customer base

Homeowners and small contractors drive the bulk of Tile Shop demand, with the chain operating roughly 120 stores in 2024, which concentrates sales in fragmented, retail-sized orders. Average ticket sizes vary widely by bathroom or kitchen project but remain dispersed across many small purchases. This dispersion limits individual negotiating clout and generally keeps buyer power moderate.

Price transparency online

E-commerce listings and comparison sites mean shoppers can check Tile Shop prices instantly; e-commerce accounted for about 17% of US retail sales in 2024, increasing visibility of SKUs. Buyers benchmark Tile Shop SKUs and alternatives across marketplaces in seconds, with surveys showing roughly 72% of home-improvement shoppers compare prices online in 2024. This transparency heightens discount pressure and elevates buyer bargaining power, compressing gross margin potential.

Low switching costs

Customers can switch to big-box chains (Home Depot, Lowe's), specialty rivals, or online marketplaces with minimal friction; 2024 data show online share of home improvement product purchases grew to roughly 20%, raising comparison shopping. If professional installation has not started, consumers frequently swap or return tile choices, keeping inventory turnover high for retailers. This flexibility amplifies buyer leverage on promotions, price matching, and return policies, pressuring Tile Shop margins.

Design and installation support

Showroom design help, samples, and project guidance raise perceived value and soften price resistance, enabling modest premiums and higher margin capture on projects. Advisory services and bundled setting materials create stickiness and higher lifetime value by simplifying purchase decisions. These service-led differentiators reduce buyer price sensitivity at the margin and support project-based upsells.

- Showroom design help

- Samples and project guidance

- Advisory services + bundled materials

- Lower marginal price sensitivity

Project-driven purchasing

Orders tied to contractor schedules make purchasing urgent and reduce buyer leverage; in 2024, 62% of renovations were reported as time-sensitive, limiting shopping around (Home Improvement Research Institute 2024). Urgency and stock/delivery speed often override small price differences, so availability and fast fulfillment strengthen seller position during projects.

- Project urgency: reduces buyer bargaining

- Stock & delivery: trump small price gaps

- Contractor schedules: drive purchase timing

Moderate buyer power as 72% compare prices and online channels rise

Buyers have moderate power: Tile Shop’s ~120 stores concentrate many small-ticket homeowners/contractor purchases that limit single-buyer leverage, but online price transparency raises pressure. In 2024 about 72% of shoppers compared prices and e-commerce represented ~17% of US retail; home-improvement online share ~20%, and 62% of renovations were time-sensitive, shifting leverage to sellers for urgent fulfillment.

| Metric | 2024 Value |

|---|---|

| Tile Shop stores | ~120 |

| Shoppers comparing prices | 72% |

| E-commerce share (US retail) | 17% |

| Home-improvement online share | 20% |

| Time-sensitive renovations | 62% |

Same Document Delivered

Tile Shop Porter's Five Forces Analysis

This Tile Shop Porter's Five Forces Analysis delivers a concise evaluation of competitive rivalry, buyer and supplier power, and threats of entry and substitution, with clear strategic implications. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted. It is ready for instant download and immediate use in decision-making or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Tile Shop faces moderate buyer power, intense rivalry from big-box and online retailers, supplier leverage in specialty lines, and limited but present threats from substitutes and new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tile Shop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global quarry reliance

Many tiles and natural stone used by Tile Shop are sourced from concentrated overseas quarries and factories—suppliers in Italy, Spain, China and India dominate the upstream market—giving vendors leverage on pricing and allocation; U.S. ceramic tile imports totaled about $1.8 billion in 2024, and currency swings plus geopolitical risks (e.g., trade tensions) amplify supplier power and input-cost volatility.

Differentiated natural stone

Unique veining, finishes, and rare stones give suppliers strong leverage over Tile Shop, since differentiated slabs cannot be easily substituted; the global natural stone market was valued at about USD 54.9 billion in 2023, underscoring supplier market heft. Limited alternatives for specific aesthetics raise dependence, allowing suppliers to impose minimum order sizes and tighter payment and delivery terms. Suppliers' control over rare inventory can compress Tile Shop's margins and inventory flexibility.

High logistics costs

Tiles are heavy, fragile, and expensive to ship, pushing inbound freight to a material share of COGS and compressing gross margins for retailers like Tile Shop; in 2024 freight volatility continued to raise landed costs across building materials. Elevated handling and specialized packaging increase switching costs, reducing buyers’ leverage. Port delays and spot-rate swings in 2024 shifted short-term bargaining power toward suppliers and carriers.

Private-label leverage

Developing exclusive private-label lines reduces direct price comparability by differentiating Tile Shop’s assortment and supporting higher margin capture; committing volume to select vendors slightly rebalances supplier power by securing better pricing and terms. However, exclusivity can increase dependence on a few partners, raising supply risk if a vendor faces disruption or negotiates harder on other contract terms. In 2024 this strategy remains a key lever for retail margin management.

- Private-label reduces price transparency

- Volume commitments yield better terms

- Heightened vendor concentration risk

- 2024: continued focus on private assortments

Multi-sourcing and contracts

Multi-sourcing across regions and locking in volume contracts reduces exposure to raw-material and freight swings; firms that secured 60%–75% of annual tile volumes in firm contracts in 2024 reported more stable input costs. Long-term supplier relationships improved quality consistency and fill rates, supporting in-stock levels above 95% in leading specialty retailers. This approach partially mitigates supplier bargaining power but does not eliminate risks from concentrated raw-material suppliers.

- Coverage: 60%–75% of annual volumes contracted (2024)

- Fill rates: >95% for established supplier networks

- Effect: ~12% lower input-cost volatility vs spot purchasing

Concentrated overseas quarries raise supplier leverage, freight and allocation risks

Supplier power is high for Tile Shop due to concentrated overseas quarry/factory sources (U.S. ceramic tile imports ~$1.8B in 2024) and differentiated natural stone (global market ~$54.9B in 2023), raising price and allocation risk; multi-sourcing and 60%–75% volume contracts in 2024 cut input volatility ~12% but dependence on key vendors and freight pressure (affecting landed costs) keeps leverage elevated.

| Metric | Value |

|---|---|

| US tile imports (2024) | $1.8B |

| Global natural stone (2023) | $54.9B |

| Contracted volume (2024) | 60%–75% |

| Input-volatility reduction | ~12% |

| Fill rates (leading retailers) | >95% |

What is included in the product

Uncovers Tile Shop’s competitive pressures by analyzing rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory dynamics; highlights disruptive trends, entry barriers, and pricing levers that shape its market position and profitability.

A clear, one-sheet summary of Tile Shop's five forces—perfect for quick decision-making and slide-ready boardroom use.

Customers Bargaining Power

Fragmented customer base

Homeowners and small contractors drive the bulk of Tile Shop demand, with the chain operating roughly 120 stores in 2024, which concentrates sales in fragmented, retail-sized orders. Average ticket sizes vary widely by bathroom or kitchen project but remain dispersed across many small purchases. This dispersion limits individual negotiating clout and generally keeps buyer power moderate.

Price transparency online

E-commerce listings and comparison sites mean shoppers can check Tile Shop prices instantly; e-commerce accounted for about 17% of US retail sales in 2024, increasing visibility of SKUs. Buyers benchmark Tile Shop SKUs and alternatives across marketplaces in seconds, with surveys showing roughly 72% of home-improvement shoppers compare prices online in 2024. This transparency heightens discount pressure and elevates buyer bargaining power, compressing gross margin potential.

Low switching costs

Customers can switch to big-box chains (Home Depot, Lowe's), specialty rivals, or online marketplaces with minimal friction; 2024 data show online share of home improvement product purchases grew to roughly 20%, raising comparison shopping. If professional installation has not started, consumers frequently swap or return tile choices, keeping inventory turnover high for retailers. This flexibility amplifies buyer leverage on promotions, price matching, and return policies, pressuring Tile Shop margins.

Design and installation support

Showroom design help, samples, and project guidance raise perceived value and soften price resistance, enabling modest premiums and higher margin capture on projects. Advisory services and bundled setting materials create stickiness and higher lifetime value by simplifying purchase decisions. These service-led differentiators reduce buyer price sensitivity at the margin and support project-based upsells.

- Showroom design help

- Samples and project guidance

- Advisory services + bundled materials

- Lower marginal price sensitivity

Project-driven purchasing

Orders tied to contractor schedules make purchasing urgent and reduce buyer leverage; in 2024, 62% of renovations were reported as time-sensitive, limiting shopping around (Home Improvement Research Institute 2024). Urgency and stock/delivery speed often override small price differences, so availability and fast fulfillment strengthen seller position during projects.

- Project urgency: reduces buyer bargaining

- Stock & delivery: trump small price gaps

- Contractor schedules: drive purchase timing

Moderate buyer power as 72% compare prices and online channels rise

Buyers have moderate power: Tile Shop’s ~120 stores concentrate many small-ticket homeowners/contractor purchases that limit single-buyer leverage, but online price transparency raises pressure. In 2024 about 72% of shoppers compared prices and e-commerce represented ~17% of US retail; home-improvement online share ~20%, and 62% of renovations were time-sensitive, shifting leverage to sellers for urgent fulfillment.

| Metric | 2024 Value |

|---|---|

| Tile Shop stores | ~120 |

| Shoppers comparing prices | 72% |

| E-commerce share (US retail) | 17% |

| Home-improvement online share | 20% |

| Time-sensitive renovations | 62% |

Same Document Delivered

Tile Shop Porter's Five Forces Analysis

This Tile Shop Porter's Five Forces Analysis delivers a concise evaluation of competitive rivalry, buyer and supplier power, and threats of entry and substitution, with clear strategic implications. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted. It is ready for instant download and immediate use in decision-making or reporting.