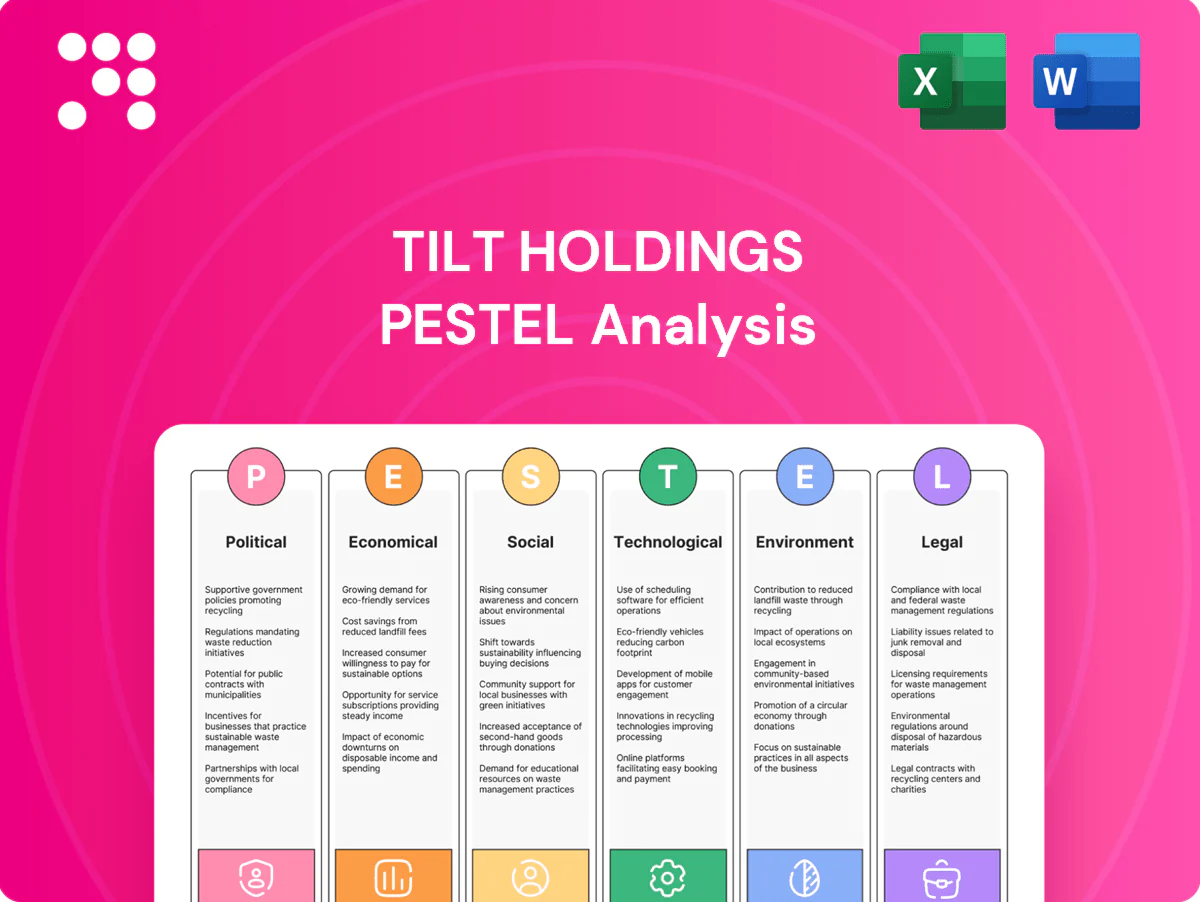

TILT Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regulatory trends, economic cycles, social sentiment, technological advances, and environmental pressures are reshaping TILT Holdings’ outlook in our concise PESTLE snapshot. Use these curated insights to anticipate risks and spot strategic opportunities. Purchase the full analysis for a complete, actionable briefing you can deploy today.

Political factors

Federal–state policy divergence

U.S. federal cannabis remains Schedule I while 38 states allow medical use and 24+ permit adult-use, creating misalignment that shapes TILT’s market access and compliance burden. Operating across jurisdictions forces tailored policies and fragmented reporting, slowing scale. Federal enforcement priorities shift with administrations—bills like SAFE Banking remain unresolved as of mid-2025—so focus on compliant, regulated states mitigates legal and financial uncertainty.

Rescheduling and reform momentum

Ongoing federal rescheduling debates and banking reform—including the SAFER Banking Act, which has passed the House multiple times but was not enacted into law as of July 2025—could unlock tax relief and broader capital access for operators. US legal cannabis sales were about $27 billion in 2024, so policy wins would materially ease 280E tax burdens and financing constraints. Timing and scope remain uncertain, so TILT must scenario-plan; early readiness would accelerate growth, while delays prolong cost and financing headwinds.

Local licensing and zoning controls

City and county votes, buffer rules and municipal license caps directly determine where clients can operate, shaping TILT’s service demand; 23 states plus DC had adult-use markets by 2024, but local controls often restrict storefront density. Political turnover can tighten or relax rules rapidly. Proactive stakeholder engagement and community benefits boost approval odds, while geographic diversification reduces concentration of municipal policy risk.

Social equity and public health priorities

States increasingly tie licenses and procurement to equity participation and public health safeguards; demonstrable community impact builds political goodwill and can sway procurement decisions. TILT can offer lower-cost infrastructure and compliance support to equity operators, aligning with program criteria and unlocking partnerships as the legal market—retail sales reached about $30 billion in 2023—continues to professionalize. Programs also shape brand and vendor selection, affecting go-to-market strategy.

- Equity-focused licensing

- Compliance-as-service

- Partnerships influence procurement

- Community impact = political capital

Trade and interstate commerce debates

As interstate commerce debates continue, supply chains may restructure, shifting cultivation and processing footprints; 23 states plus DC allowed adult-use cannabis and 37 allowed medical programs in 2024, creating fragmented markets that contest cross-border logistics. Political resistance from protectionist states can slow harmonization, while TILT’s modular services position the company to pivot if federal or interstate rules enable commerce. Advocacy coalitions such as NCIA and state chambers (lobby spend rising into tens of millions annually) will shape rulemaking and market access.

- fragmentation: 23+DC adult-use, 37 medical (2024)

- protectionism: state-level barriers risk slower harmonization

- TILT agility: modular services enable cross-border logistics

- advocacy: industry coalitions influencing federal/interstate policy

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

Federal Schedule I status and unresolved banking reform (SAFER/SAFE not enacted as of July 2025) keep 280E tax and financing risks high; US legal cannabis sales were about $27B in 2024. State/local patchwork (23 states+DC adult-use; 37 medical in 2024) drives fragmented compliance and municipal risk. TILT’s modular services and equity-focused offerings reduce policy exposure and enable municipal procurement wins.

| Metric | 2024/2025 | Implication |

|---|---|---|

| US legal sales | $27B (2024) | Market scale; eases unit economics if reform |

| Adult-use states | 23+DC (2024) | Fragmented market, localized policy risk |

| Banking reform | Not enacted (Jul 2025) | Continued financing & tax constraints |

What is included in the product

Explores how external macro-environmental factors uniquely affect TILT Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it includes detailed sub-points, forward-looking insights, and practical implications to support strategy, risk management, and fundraising.

Condensed, visually segmented PESTLE summary for TILT Holdings that simplifies external risk assessment and market positioning, ideal for quick insertion into presentations or strategy sessions. Editable notes and shareable format speed team alignment and client reporting, reducing prep time and decision friction.

Economic factors

Capital access and cost of funds

High financing costs and limited traditional banking push cannabis-sector WACC to roughly 14–20% as of 2024, constraining expansion and technology adoption and slowing TILT’s pipeline conversion. Any measurable improvement in credit availability historically unlocks capital-intensive infrastructure demand, boosting orders for service providers. Cash-efficient go-to-market models and vendor financing programs can bridge gaps and sustain rollout when bank credit remains tight.

Price compression and margin pressures

Wholesale oversupply in states such as Oregon and Michigan has driven volatility, with BDSA reporting U.S. wholesale cannabis prices down about 15% in 2024, squeezing operator margins. Clients increasingly seek efficiency solutions, and TILT’s tech and processes advertise up to 20% cost savings for operators. Service pricing must track client profitability cycles to remain viable. Diversification across markets and segments helps buffer revenue swings.

Consumer demand normalization

Post-pandemic consumer demand has largely normalized, with trade-down behaviors during inflationary periods—U.S. CPI eased to about 3.4% in 2024, driving share gains for value and mid-tier brands and pressuring mix and service requirements. Value/mid-tier growth shifts SKU mix and fulfillment needs, increasing demand for private-label and cost-efficient supply chains. TILT can focus on process efficiencies, SKU rationalization and private-label support to protect margins. Elasticity-aware pricing and bundled offerings help sustain volumes during downcycles.

M&A and consolidation cycles

M&A and consolidation cycles drive demand for integration services and brand rationalization as distressed assets and roll-ups proliferate; according to industry reports through 2024–H1 2025, deal volume remains below earlier peaks, creating opportunities for TILT to monetize via turnaround support and standardization, though elongated timelines delay revenue realization and require cash-flow management.

- Monetization: turnaround fees, integration retainers

- Risk: elongated deal timelines compress near-term cash

- Mitigation: flexible milestone-tied contracts

- Opportunity: brand rationalization on roll-ups

Input costs and supply chain resilience

Energy, packaging and labor costs remain volatile and region-specific, with U.S. industrial electricity and packaging resin markets still showing elevated price variability through 2024–2025; TILT offsets this by strengthening localized supplier networks and adding automation to cultivation and processing lines to lower unit labor costs.

Inventory discipline—targeting lower days on hand—reduces working capital drag for clients, while data-driven procurement across facilities has improved gross margins by optimizing batch sourcing and reducing spoilage.

- Region-specific energy and packaging volatility impacting COGS

- Localized suppliers + automation lower labor intensity

- Inventory discipline cuts working capital needs

- Data-driven procurement improves margins facility-wide

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

High financing costs (sector WACC ~14–20% in 2024) and tight credit limit capex, while wholesale prices fell ~15% in 2024 squeezing margins; CPI eased to ~3.4% in 2024 shifting buyers to value tiers. M&A deal volume remains below prior peaks through H1 2025, boosting demand for integration and turnaround services. Inventory and automation reduce working-capital drag and labor intensity.

| Metric | Value (2024–H1 2025) |

|---|---|

| Sector WACC | 14–20% |

| Wholesale price change | -15% (2024) |

| U.S. CPI | ~3.4% (2024) |

| M&A volume | Below peaks (H1 2025) |

Preview the Actual Deliverable

TILT Holdings PESTLE Analysis

The preview shown here is the exact TILT Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment with charts and citations. No placeholders, no surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regulatory trends, economic cycles, social sentiment, technological advances, and environmental pressures are reshaping TILT Holdings’ outlook in our concise PESTLE snapshot. Use these curated insights to anticipate risks and spot strategic opportunities. Purchase the full analysis for a complete, actionable briefing you can deploy today.

Political factors

Federal–state policy divergence

U.S. federal cannabis remains Schedule I while 38 states allow medical use and 24+ permit adult-use, creating misalignment that shapes TILT’s market access and compliance burden. Operating across jurisdictions forces tailored policies and fragmented reporting, slowing scale. Federal enforcement priorities shift with administrations—bills like SAFE Banking remain unresolved as of mid-2025—so focus on compliant, regulated states mitigates legal and financial uncertainty.

Rescheduling and reform momentum

Ongoing federal rescheduling debates and banking reform—including the SAFER Banking Act, which has passed the House multiple times but was not enacted into law as of July 2025—could unlock tax relief and broader capital access for operators. US legal cannabis sales were about $27 billion in 2024, so policy wins would materially ease 280E tax burdens and financing constraints. Timing and scope remain uncertain, so TILT must scenario-plan; early readiness would accelerate growth, while delays prolong cost and financing headwinds.

Local licensing and zoning controls

City and county votes, buffer rules and municipal license caps directly determine where clients can operate, shaping TILT’s service demand; 23 states plus DC had adult-use markets by 2024, but local controls often restrict storefront density. Political turnover can tighten or relax rules rapidly. Proactive stakeholder engagement and community benefits boost approval odds, while geographic diversification reduces concentration of municipal policy risk.

Social equity and public health priorities

States increasingly tie licenses and procurement to equity participation and public health safeguards; demonstrable community impact builds political goodwill and can sway procurement decisions. TILT can offer lower-cost infrastructure and compliance support to equity operators, aligning with program criteria and unlocking partnerships as the legal market—retail sales reached about $30 billion in 2023—continues to professionalize. Programs also shape brand and vendor selection, affecting go-to-market strategy.

- Equity-focused licensing

- Compliance-as-service

- Partnerships influence procurement

- Community impact = political capital

Trade and interstate commerce debates

As interstate commerce debates continue, supply chains may restructure, shifting cultivation and processing footprints; 23 states plus DC allowed adult-use cannabis and 37 allowed medical programs in 2024, creating fragmented markets that contest cross-border logistics. Political resistance from protectionist states can slow harmonization, while TILT’s modular services position the company to pivot if federal or interstate rules enable commerce. Advocacy coalitions such as NCIA and state chambers (lobby spend rising into tens of millions annually) will shape rulemaking and market access.

- fragmentation: 23+DC adult-use, 37 medical (2024)

- protectionism: state-level barriers risk slower harmonization

- TILT agility: modular services enable cross-border logistics

- advocacy: industry coalitions influencing federal/interstate policy

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

Federal Schedule I status and unresolved banking reform (SAFER/SAFE not enacted as of July 2025) keep 280E tax and financing risks high; US legal cannabis sales were about $27B in 2024. State/local patchwork (23 states+DC adult-use; 37 medical in 2024) drives fragmented compliance and municipal risk. TILT’s modular services and equity-focused offerings reduce policy exposure and enable municipal procurement wins.

| Metric | 2024/2025 | Implication |

|---|---|---|

| US legal sales | $27B (2024) | Market scale; eases unit economics if reform |

| Adult-use states | 23+DC (2024) | Fragmented market, localized policy risk |

| Banking reform | Not enacted (Jul 2025) | Continued financing & tax constraints |

What is included in the product

Explores how external macro-environmental factors uniquely affect TILT Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it includes detailed sub-points, forward-looking insights, and practical implications to support strategy, risk management, and fundraising.

Condensed, visually segmented PESTLE summary for TILT Holdings that simplifies external risk assessment and market positioning, ideal for quick insertion into presentations or strategy sessions. Editable notes and shareable format speed team alignment and client reporting, reducing prep time and decision friction.

Economic factors

Capital access and cost of funds

High financing costs and limited traditional banking push cannabis-sector WACC to roughly 14–20% as of 2024, constraining expansion and technology adoption and slowing TILT’s pipeline conversion. Any measurable improvement in credit availability historically unlocks capital-intensive infrastructure demand, boosting orders for service providers. Cash-efficient go-to-market models and vendor financing programs can bridge gaps and sustain rollout when bank credit remains tight.

Price compression and margin pressures

Wholesale oversupply in states such as Oregon and Michigan has driven volatility, with BDSA reporting U.S. wholesale cannabis prices down about 15% in 2024, squeezing operator margins. Clients increasingly seek efficiency solutions, and TILT’s tech and processes advertise up to 20% cost savings for operators. Service pricing must track client profitability cycles to remain viable. Diversification across markets and segments helps buffer revenue swings.

Consumer demand normalization

Post-pandemic consumer demand has largely normalized, with trade-down behaviors during inflationary periods—U.S. CPI eased to about 3.4% in 2024, driving share gains for value and mid-tier brands and pressuring mix and service requirements. Value/mid-tier growth shifts SKU mix and fulfillment needs, increasing demand for private-label and cost-efficient supply chains. TILT can focus on process efficiencies, SKU rationalization and private-label support to protect margins. Elasticity-aware pricing and bundled offerings help sustain volumes during downcycles.

M&A and consolidation cycles

M&A and consolidation cycles drive demand for integration services and brand rationalization as distressed assets and roll-ups proliferate; according to industry reports through 2024–H1 2025, deal volume remains below earlier peaks, creating opportunities for TILT to monetize via turnaround support and standardization, though elongated timelines delay revenue realization and require cash-flow management.

- Monetization: turnaround fees, integration retainers

- Risk: elongated deal timelines compress near-term cash

- Mitigation: flexible milestone-tied contracts

- Opportunity: brand rationalization on roll-ups

Input costs and supply chain resilience

Energy, packaging and labor costs remain volatile and region-specific, with U.S. industrial electricity and packaging resin markets still showing elevated price variability through 2024–2025; TILT offsets this by strengthening localized supplier networks and adding automation to cultivation and processing lines to lower unit labor costs.

Inventory discipline—targeting lower days on hand—reduces working capital drag for clients, while data-driven procurement across facilities has improved gross margins by optimizing batch sourcing and reducing spoilage.

- Region-specific energy and packaging volatility impacting COGS

- Localized suppliers + automation lower labor intensity

- Inventory discipline cuts working capital needs

- Data-driven procurement improves margins facility-wide

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

High financing costs (sector WACC ~14–20% in 2024) and tight credit limit capex, while wholesale prices fell ~15% in 2024 squeezing margins; CPI eased to ~3.4% in 2024 shifting buyers to value tiers. M&A deal volume remains below prior peaks through H1 2025, boosting demand for integration and turnaround services. Inventory and automation reduce working-capital drag and labor intensity.

| Metric | Value (2024–H1 2025) |

|---|---|

| Sector WACC | 14–20% |

| Wholesale price change | -15% (2024) |

| U.S. CPI | ~3.4% (2024) |

| M&A volume | Below peaks (H1 2025) |

Preview the Actual Deliverable

TILT Holdings PESTLE Analysis

The preview shown here is the exact TILT Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment with charts and citations. No placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regulatory trends, economic cycles, social sentiment, technological advances, and environmental pressures are reshaping TILT Holdings’ outlook in our concise PESTLE snapshot. Use these curated insights to anticipate risks and spot strategic opportunities. Purchase the full analysis for a complete, actionable briefing you can deploy today.

Political factors

Federal–state policy divergence

U.S. federal cannabis remains Schedule I while 38 states allow medical use and 24+ permit adult-use, creating misalignment that shapes TILT’s market access and compliance burden. Operating across jurisdictions forces tailored policies and fragmented reporting, slowing scale. Federal enforcement priorities shift with administrations—bills like SAFE Banking remain unresolved as of mid-2025—so focus on compliant, regulated states mitigates legal and financial uncertainty.

Rescheduling and reform momentum

Ongoing federal rescheduling debates and banking reform—including the SAFER Banking Act, which has passed the House multiple times but was not enacted into law as of July 2025—could unlock tax relief and broader capital access for operators. US legal cannabis sales were about $27 billion in 2024, so policy wins would materially ease 280E tax burdens and financing constraints. Timing and scope remain uncertain, so TILT must scenario-plan; early readiness would accelerate growth, while delays prolong cost and financing headwinds.

Local licensing and zoning controls

City and county votes, buffer rules and municipal license caps directly determine where clients can operate, shaping TILT’s service demand; 23 states plus DC had adult-use markets by 2024, but local controls often restrict storefront density. Political turnover can tighten or relax rules rapidly. Proactive stakeholder engagement and community benefits boost approval odds, while geographic diversification reduces concentration of municipal policy risk.

Social equity and public health priorities

States increasingly tie licenses and procurement to equity participation and public health safeguards; demonstrable community impact builds political goodwill and can sway procurement decisions. TILT can offer lower-cost infrastructure and compliance support to equity operators, aligning with program criteria and unlocking partnerships as the legal market—retail sales reached about $30 billion in 2023—continues to professionalize. Programs also shape brand and vendor selection, affecting go-to-market strategy.

- Equity-focused licensing

- Compliance-as-service

- Partnerships influence procurement

- Community impact = political capital

Trade and interstate commerce debates

As interstate commerce debates continue, supply chains may restructure, shifting cultivation and processing footprints; 23 states plus DC allowed adult-use cannabis and 37 allowed medical programs in 2024, creating fragmented markets that contest cross-border logistics. Political resistance from protectionist states can slow harmonization, while TILT’s modular services position the company to pivot if federal or interstate rules enable commerce. Advocacy coalitions such as NCIA and state chambers (lobby spend rising into tens of millions annually) will shape rulemaking and market access.

- fragmentation: 23+DC adult-use, 37 medical (2024)

- protectionism: state-level barriers risk slower harmonization

- TILT agility: modular services enable cross-border logistics

- advocacy: industry coalitions influencing federal/interstate policy

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

Federal Schedule I status and unresolved banking reform (SAFER/SAFE not enacted as of July 2025) keep 280E tax and financing risks high; US legal cannabis sales were about $27B in 2024. State/local patchwork (23 states+DC adult-use; 37 medical in 2024) drives fragmented compliance and municipal risk. TILT’s modular services and equity-focused offerings reduce policy exposure and enable municipal procurement wins.

| Metric | 2024/2025 | Implication |

|---|---|---|

| US legal sales | $27B (2024) | Market scale; eases unit economics if reform |

| Adult-use states | 23+DC (2024) | Fragmented market, localized policy risk |

| Banking reform | Not enacted (Jul 2025) | Continued financing & tax constraints |

What is included in the product

Explores how external macro-environmental factors uniquely affect TILT Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it includes detailed sub-points, forward-looking insights, and practical implications to support strategy, risk management, and fundraising.

Condensed, visually segmented PESTLE summary for TILT Holdings that simplifies external risk assessment and market positioning, ideal for quick insertion into presentations or strategy sessions. Editable notes and shareable format speed team alignment and client reporting, reducing prep time and decision friction.

Economic factors

Capital access and cost of funds

High financing costs and limited traditional banking push cannabis-sector WACC to roughly 14–20% as of 2024, constraining expansion and technology adoption and slowing TILT’s pipeline conversion. Any measurable improvement in credit availability historically unlocks capital-intensive infrastructure demand, boosting orders for service providers. Cash-efficient go-to-market models and vendor financing programs can bridge gaps and sustain rollout when bank credit remains tight.

Price compression and margin pressures

Wholesale oversupply in states such as Oregon and Michigan has driven volatility, with BDSA reporting U.S. wholesale cannabis prices down about 15% in 2024, squeezing operator margins. Clients increasingly seek efficiency solutions, and TILT’s tech and processes advertise up to 20% cost savings for operators. Service pricing must track client profitability cycles to remain viable. Diversification across markets and segments helps buffer revenue swings.

Consumer demand normalization

Post-pandemic consumer demand has largely normalized, with trade-down behaviors during inflationary periods—U.S. CPI eased to about 3.4% in 2024, driving share gains for value and mid-tier brands and pressuring mix and service requirements. Value/mid-tier growth shifts SKU mix and fulfillment needs, increasing demand for private-label and cost-efficient supply chains. TILT can focus on process efficiencies, SKU rationalization and private-label support to protect margins. Elasticity-aware pricing and bundled offerings help sustain volumes during downcycles.

M&A and consolidation cycles

M&A and consolidation cycles drive demand for integration services and brand rationalization as distressed assets and roll-ups proliferate; according to industry reports through 2024–H1 2025, deal volume remains below earlier peaks, creating opportunities for TILT to monetize via turnaround support and standardization, though elongated timelines delay revenue realization and require cash-flow management.

- Monetization: turnaround fees, integration retainers

- Risk: elongated deal timelines compress near-term cash

- Mitigation: flexible milestone-tied contracts

- Opportunity: brand rationalization on roll-ups

Input costs and supply chain resilience

Energy, packaging and labor costs remain volatile and region-specific, with U.S. industrial electricity and packaging resin markets still showing elevated price variability through 2024–2025; TILT offsets this by strengthening localized supplier networks and adding automation to cultivation and processing lines to lower unit labor costs.

Inventory discipline—targeting lower days on hand—reduces working capital drag for clients, while data-driven procurement across facilities has improved gross margins by optimizing batch sourcing and reducing spoilage.

- Region-specific energy and packaging volatility impacting COGS

- Localized suppliers + automation lower labor intensity

- Inventory discipline cuts working capital needs

- Data-driven procurement improves margins facility-wide

Schedule I, banking reform not enacted (Jul 2025): 280E risk high; US $27B

High financing costs (sector WACC ~14–20% in 2024) and tight credit limit capex, while wholesale prices fell ~15% in 2024 squeezing margins; CPI eased to ~3.4% in 2024 shifting buyers to value tiers. M&A deal volume remains below prior peaks through H1 2025, boosting demand for integration and turnaround services. Inventory and automation reduce working-capital drag and labor intensity.

| Metric | Value (2024–H1 2025) |

|---|---|

| Sector WACC | 14–20% |

| Wholesale price change | -15% (2024) |

| U.S. CPI | ~3.4% (2024) |

| M&A volume | Below peaks (H1 2025) |

Preview the Actual Deliverable

TILT Holdings PESTLE Analysis

The preview shown here is the exact TILT Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment with charts and citations. No placeholders, no surprises.