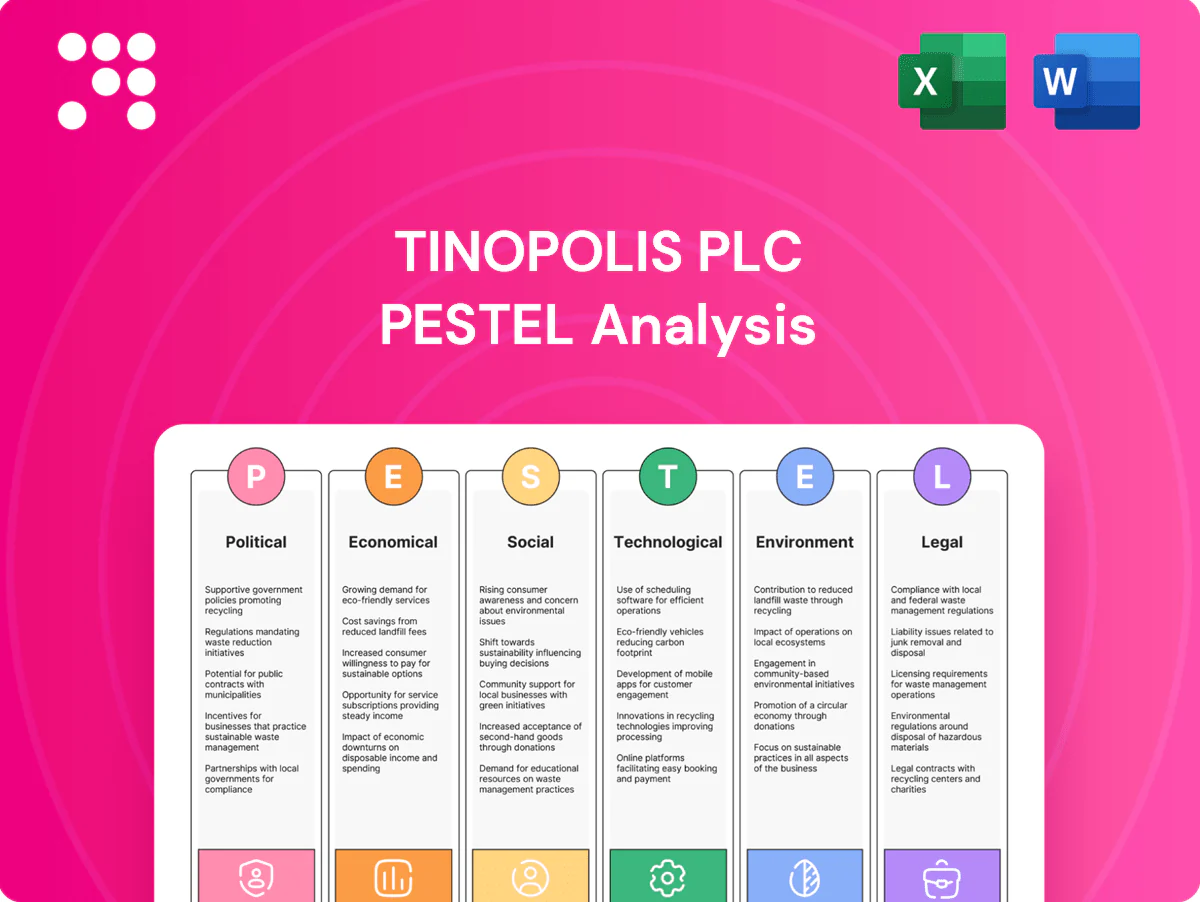

Tinopolis PLC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Tinopolis PLC reveals how political shifts, economic pressures, social trends, technological change, legal risks, and environmental factors converge on its strategy. Use these concise insights to assess risk and spot growth opportunities. Purchase the full report for the detailed, editable analysis you can action today.

Political factors

Public broadcasting policy shifts

Changes in UK and EU/US public service broadcasting mandates affect commissioning volumes and funding routes for factual and current affairs content. The AVMSD sets a minimum 30% share of European works for on‑demand services, and local content quotas can advantage domestic producers like Tinopolis in target markets. Conversely, austerity or reallocation of public funds to news can crowd out entertainment budgets; monitoring regulator consultations and lobbying via industry bodies mitigates risk.

Trade relations and market access

Post-Brexit UK-EU Trade and Cooperation Agreement (signed Dec 2020) removed tariff barriers for goods but left audiovisual co-production, mutual recognition and crew mobility constrained, adding visa, carnet and customs frictions that raise shoot costs and delays. International production expenses can rise materially while favourable co‑production treaties and tax incentives (often up to 30% rebates) in secondary markets help offset barriers. Strategic partnerships with EU subsidiaries preserve distribution access and mitigate market disruption.

Tax incentives and regional grants

Production tax credits—UK film tax relief up to 25%, Ireland’s Section 481 up to 32%, Canada federal/provincial combos often deliver 25–65% and US states (eg Georgia) offer up to ~30%—materially drive greenlighting and location choice. Policy stability dictates multi-year slate planning and studio utilization. Competitive regional grant bidding boosts budgets for high-end drama and factuals. Diversifying eligibility across geographies reduces concentration risk.

Geopolitical stability and event risk

Conflicts, strikes and election cycles can delay production schedules, restrict site access and rapidly shift audience preferences, with sports and live-event commissions the most exposed to cancellations and postponements. Higher perceived instability has pushed event and political-risk insurance costs higher—renewal rates rose roughly 10% in 2024 per market reports—squeezing margins. Tinopolis mitigates risk through contingency planning and distributed production hubs to maintain deliverability and protect revenues.

- Exposures: sports/live events vulnerable

- Drivers: conflicts, strikes, elections

- Costs: ~10% insurance rate rise in 2024

- Mitigation: contingency plans, distributed hubs

Regulatory oversight of content standards

Ofcom and comparable regulators set binding content standards that directly shape Tinopolis editorial choices across factual and entertainment genres; Ofcom logged c.180,000 broadcast complaints in 2023–24, keeping scrutiny high. Tighter rules on misinformation, fairness and harmful content have increased compliance workload, with many producers reporting compliance budgets rising c.3–6% year‑on‑year. Political pressure on public discourse further intensifies review of current affairs output, and robust compliance frameworks protect key broadcaster relationships and reduce regulatory risk.

- Regulator: Ofcom (UK) and national equivalents

- 2023–24 complaints: c.180,000 (Ofcom)

- Compliance cost rise: ≈3–6% YOY

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Policy shifts (AVMSD 30% EU quota), post‑Brexit frictions, and production tax credits (UK ~25%, Ireland ~32%, Canada 25–65%) drive commissioning, location and costs; Ofcom logged c.180,000 complaints (2023–24) raising compliance spend ~3–6% YOY. Insurance renewals rose ~10% in 2024; strikes/elections add scheduling risk. Tinopolis uses distributed hubs, co‑prods and lobbying to mitigate.

| Factor | Metric |

|---|---|

| AVMSD quota | 30% |

| Ofcom complaints (23–24) | c.180,000 |

| Compliance cost rise | 3–6% YOY |

| Insurance renewal rise (2024) | ~10% |

| Typical tax credits | UK 25%, IE 32%, CA 25–65% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Tinopolis PLC, with data-driven insights and trend analysis tailored to its media production and distribution footprint; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategies.

A concise, visually segmented PESTLE summary for Tinopolis PLC that can be dropped into presentations, shared across teams, and annotated for regional or business-line specifics to streamline strategy sessions and external risk discussions.

Economic factors

Advertising cycles and broadcaster budgets

Ad-market downturns compress broadcaster commissioning, shifting spend to lower‑risk formats; UK TV ad revenues fell notably in recessionary 2023–24, tightening commissioning pipelines. Streamers’ content budgets (global streaming content spend >$70bn in 2024) can support demand but are increasingly selective. Tinopolis’s diversification across 25+ genres buffers volatility, while flexible cost bases and co‑financing (covering ~30–40% of some projects) help sustain margins.

Currency volatility

Tinopolis faces FX exposure across GBP, USD and EUR; a stronger dollar (DXY ~103.5, GBP/USD ~1.27 July 2025) can boost USD-denominated distribution income while raising costs for overseas production. Active hedging and natural slate offsets have historically trimmed quarterly earnings volatility. Contracting key commissions in commissioning currencies further stabilises cash flows.

Cost inflation in production

Rising labor, set, travel and insurance costs—with studio hire and specialist crew day rates reported up to 25% higher in recent high-end unscripted and drama shoots—are squeezing Tinopolis PLC production margins.

Studio scarcity and equipment shortages have pushed some hire rates 20–40% above pre-pandemic levels, forcing tighter scheduling and higher contingency spend.

Efficiency gains from remote workflows and standardized production kits help protect gross margins, while negotiating escalators and cost-sharing with commissioners remains critical to pass through inflationary pressures.

Streaming platform procurement dynamics

Streamers increasingly favor global-rights, buyout models that limit back-end participation, pressuring producers; Netflix spent $17.3bn on content in 2023, underscoring scale and negotiating power. Greater budget discipline and ROI scrutiny have raised cancellation and renewal risk, while a balanced mix of domestic broadcaster commissions and international presales improves revenue visibility. Strong IP ownership preserves library value and long-term monetisation.

- Global buyouts concentrate negotiating power

- Netflix content spend: 17.3bn (2023)

- Mixed commissions + presales = better revenue visibility

- IP ownership sustains catalogue value

M&A and capital availability

Private capital interest, supported by roughly $2.5tn global private capital dry powder at end-2024 (Preqin), uplifts valuations and exit options for production assets, while Bank of England base rate around 5.25% in 2024 raises gap and deficit funding costs. Joint ventures enable capital-light entry into new genres and territories, and maintaining low leverage preserves resilience amid tighter credit.

- Private capital: $2.5tn dry powder (end-2024)

- Interest rates: BoE ~5.25% (2024)

- JV: capital-light expansion

- Low leverage: enhances credit resilience

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Tinopolis faces ad-revenue cyclicality after UK TV ad declines in 2023–24, while global streaming spend (~$70bn in 2024) offers selective demand; diversification and co‑financing (~30–40%) support margins. FX (DXY ~103.5; GBP/USD ~1.27 Jul 2025) and rising costs (crew/studio +20–40%, crew day rates up to 25%) squeeze margins; low leverage and JVs preserve resilience.

| Metric | Value |

|---|---|

| Streaming spend 2024 | $70bn |

| Netflix 2023 | $17.3bn |

| Dry powder end‑2024 | $2.5tn |

| BoE base rate 2024 | ~5.25% |

Preview the Actual Deliverable

Tinopolis PLC PESTLE Analysis

The preview shown here is the exact Tinopolis PLC PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This document presents political, economic, social, technological, legal and environmental factors with actionable insights. No placeholders or teasers—what you see is the final file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Tinopolis PLC reveals how political shifts, economic pressures, social trends, technological change, legal risks, and environmental factors converge on its strategy. Use these concise insights to assess risk and spot growth opportunities. Purchase the full report for the detailed, editable analysis you can action today.

Political factors

Public broadcasting policy shifts

Changes in UK and EU/US public service broadcasting mandates affect commissioning volumes and funding routes for factual and current affairs content. The AVMSD sets a minimum 30% share of European works for on‑demand services, and local content quotas can advantage domestic producers like Tinopolis in target markets. Conversely, austerity or reallocation of public funds to news can crowd out entertainment budgets; monitoring regulator consultations and lobbying via industry bodies mitigates risk.

Trade relations and market access

Post-Brexit UK-EU Trade and Cooperation Agreement (signed Dec 2020) removed tariff barriers for goods but left audiovisual co-production, mutual recognition and crew mobility constrained, adding visa, carnet and customs frictions that raise shoot costs and delays. International production expenses can rise materially while favourable co‑production treaties and tax incentives (often up to 30% rebates) in secondary markets help offset barriers. Strategic partnerships with EU subsidiaries preserve distribution access and mitigate market disruption.

Tax incentives and regional grants

Production tax credits—UK film tax relief up to 25%, Ireland’s Section 481 up to 32%, Canada federal/provincial combos often deliver 25–65% and US states (eg Georgia) offer up to ~30%—materially drive greenlighting and location choice. Policy stability dictates multi-year slate planning and studio utilization. Competitive regional grant bidding boosts budgets for high-end drama and factuals. Diversifying eligibility across geographies reduces concentration risk.

Geopolitical stability and event risk

Conflicts, strikes and election cycles can delay production schedules, restrict site access and rapidly shift audience preferences, with sports and live-event commissions the most exposed to cancellations and postponements. Higher perceived instability has pushed event and political-risk insurance costs higher—renewal rates rose roughly 10% in 2024 per market reports—squeezing margins. Tinopolis mitigates risk through contingency planning and distributed production hubs to maintain deliverability and protect revenues.

- Exposures: sports/live events vulnerable

- Drivers: conflicts, strikes, elections

- Costs: ~10% insurance rate rise in 2024

- Mitigation: contingency plans, distributed hubs

Regulatory oversight of content standards

Ofcom and comparable regulators set binding content standards that directly shape Tinopolis editorial choices across factual and entertainment genres; Ofcom logged c.180,000 broadcast complaints in 2023–24, keeping scrutiny high. Tighter rules on misinformation, fairness and harmful content have increased compliance workload, with many producers reporting compliance budgets rising c.3–6% year‑on‑year. Political pressure on public discourse further intensifies review of current affairs output, and robust compliance frameworks protect key broadcaster relationships and reduce regulatory risk.

- Regulator: Ofcom (UK) and national equivalents

- 2023–24 complaints: c.180,000 (Ofcom)

- Compliance cost rise: ≈3–6% YOY

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Policy shifts (AVMSD 30% EU quota), post‑Brexit frictions, and production tax credits (UK ~25%, Ireland ~32%, Canada 25–65%) drive commissioning, location and costs; Ofcom logged c.180,000 complaints (2023–24) raising compliance spend ~3–6% YOY. Insurance renewals rose ~10% in 2024; strikes/elections add scheduling risk. Tinopolis uses distributed hubs, co‑prods and lobbying to mitigate.

| Factor | Metric |

|---|---|

| AVMSD quota | 30% |

| Ofcom complaints (23–24) | c.180,000 |

| Compliance cost rise | 3–6% YOY |

| Insurance renewal rise (2024) | ~10% |

| Typical tax credits | UK 25%, IE 32%, CA 25–65% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Tinopolis PLC, with data-driven insights and trend analysis tailored to its media production and distribution footprint; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategies.

A concise, visually segmented PESTLE summary for Tinopolis PLC that can be dropped into presentations, shared across teams, and annotated for regional or business-line specifics to streamline strategy sessions and external risk discussions.

Economic factors

Advertising cycles and broadcaster budgets

Ad-market downturns compress broadcaster commissioning, shifting spend to lower‑risk formats; UK TV ad revenues fell notably in recessionary 2023–24, tightening commissioning pipelines. Streamers’ content budgets (global streaming content spend >$70bn in 2024) can support demand but are increasingly selective. Tinopolis’s diversification across 25+ genres buffers volatility, while flexible cost bases and co‑financing (covering ~30–40% of some projects) help sustain margins.

Currency volatility

Tinopolis faces FX exposure across GBP, USD and EUR; a stronger dollar (DXY ~103.5, GBP/USD ~1.27 July 2025) can boost USD-denominated distribution income while raising costs for overseas production. Active hedging and natural slate offsets have historically trimmed quarterly earnings volatility. Contracting key commissions in commissioning currencies further stabilises cash flows.

Cost inflation in production

Rising labor, set, travel and insurance costs—with studio hire and specialist crew day rates reported up to 25% higher in recent high-end unscripted and drama shoots—are squeezing Tinopolis PLC production margins.

Studio scarcity and equipment shortages have pushed some hire rates 20–40% above pre-pandemic levels, forcing tighter scheduling and higher contingency spend.

Efficiency gains from remote workflows and standardized production kits help protect gross margins, while negotiating escalators and cost-sharing with commissioners remains critical to pass through inflationary pressures.

Streaming platform procurement dynamics

Streamers increasingly favor global-rights, buyout models that limit back-end participation, pressuring producers; Netflix spent $17.3bn on content in 2023, underscoring scale and negotiating power. Greater budget discipline and ROI scrutiny have raised cancellation and renewal risk, while a balanced mix of domestic broadcaster commissions and international presales improves revenue visibility. Strong IP ownership preserves library value and long-term monetisation.

- Global buyouts concentrate negotiating power

- Netflix content spend: 17.3bn (2023)

- Mixed commissions + presales = better revenue visibility

- IP ownership sustains catalogue value

M&A and capital availability

Private capital interest, supported by roughly $2.5tn global private capital dry powder at end-2024 (Preqin), uplifts valuations and exit options for production assets, while Bank of England base rate around 5.25% in 2024 raises gap and deficit funding costs. Joint ventures enable capital-light entry into new genres and territories, and maintaining low leverage preserves resilience amid tighter credit.

- Private capital: $2.5tn dry powder (end-2024)

- Interest rates: BoE ~5.25% (2024)

- JV: capital-light expansion

- Low leverage: enhances credit resilience

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Tinopolis faces ad-revenue cyclicality after UK TV ad declines in 2023–24, while global streaming spend (~$70bn in 2024) offers selective demand; diversification and co‑financing (~30–40%) support margins. FX (DXY ~103.5; GBP/USD ~1.27 Jul 2025) and rising costs (crew/studio +20–40%, crew day rates up to 25%) squeeze margins; low leverage and JVs preserve resilience.

| Metric | Value |

|---|---|

| Streaming spend 2024 | $70bn |

| Netflix 2023 | $17.3bn |

| Dry powder end‑2024 | $2.5tn |

| BoE base rate 2024 | ~5.25% |

Preview the Actual Deliverable

Tinopolis PLC PESTLE Analysis

The preview shown here is the exact Tinopolis PLC PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This document presents political, economic, social, technological, legal and environmental factors with actionable insights. No placeholders or teasers—what you see is the final file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Tinopolis PLC reveals how political shifts, economic pressures, social trends, technological change, legal risks, and environmental factors converge on its strategy. Use these concise insights to assess risk and spot growth opportunities. Purchase the full report for the detailed, editable analysis you can action today.

Political factors

Public broadcasting policy shifts

Changes in UK and EU/US public service broadcasting mandates affect commissioning volumes and funding routes for factual and current affairs content. The AVMSD sets a minimum 30% share of European works for on‑demand services, and local content quotas can advantage domestic producers like Tinopolis in target markets. Conversely, austerity or reallocation of public funds to news can crowd out entertainment budgets; monitoring regulator consultations and lobbying via industry bodies mitigates risk.

Trade relations and market access

Post-Brexit UK-EU Trade and Cooperation Agreement (signed Dec 2020) removed tariff barriers for goods but left audiovisual co-production, mutual recognition and crew mobility constrained, adding visa, carnet and customs frictions that raise shoot costs and delays. International production expenses can rise materially while favourable co‑production treaties and tax incentives (often up to 30% rebates) in secondary markets help offset barriers. Strategic partnerships with EU subsidiaries preserve distribution access and mitigate market disruption.

Tax incentives and regional grants

Production tax credits—UK film tax relief up to 25%, Ireland’s Section 481 up to 32%, Canada federal/provincial combos often deliver 25–65% and US states (eg Georgia) offer up to ~30%—materially drive greenlighting and location choice. Policy stability dictates multi-year slate planning and studio utilization. Competitive regional grant bidding boosts budgets for high-end drama and factuals. Diversifying eligibility across geographies reduces concentration risk.

Geopolitical stability and event risk

Conflicts, strikes and election cycles can delay production schedules, restrict site access and rapidly shift audience preferences, with sports and live-event commissions the most exposed to cancellations and postponements. Higher perceived instability has pushed event and political-risk insurance costs higher—renewal rates rose roughly 10% in 2024 per market reports—squeezing margins. Tinopolis mitigates risk through contingency planning and distributed production hubs to maintain deliverability and protect revenues.

- Exposures: sports/live events vulnerable

- Drivers: conflicts, strikes, elections

- Costs: ~10% insurance rate rise in 2024

- Mitigation: contingency plans, distributed hubs

Regulatory oversight of content standards

Ofcom and comparable regulators set binding content standards that directly shape Tinopolis editorial choices across factual and entertainment genres; Ofcom logged c.180,000 broadcast complaints in 2023–24, keeping scrutiny high. Tighter rules on misinformation, fairness and harmful content have increased compliance workload, with many producers reporting compliance budgets rising c.3–6% year‑on‑year. Political pressure on public discourse further intensifies review of current affairs output, and robust compliance frameworks protect key broadcaster relationships and reduce regulatory risk.

- Regulator: Ofcom (UK) and national equivalents

- 2023–24 complaints: c.180,000 (Ofcom)

- Compliance cost rise: ≈3–6% YOY

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Policy shifts (AVMSD 30% EU quota), post‑Brexit frictions, and production tax credits (UK ~25%, Ireland ~32%, Canada 25–65%) drive commissioning, location and costs; Ofcom logged c.180,000 complaints (2023–24) raising compliance spend ~3–6% YOY. Insurance renewals rose ~10% in 2024; strikes/elections add scheduling risk. Tinopolis uses distributed hubs, co‑prods and lobbying to mitigate.

| Factor | Metric |

|---|---|

| AVMSD quota | 30% |

| Ofcom complaints (23–24) | c.180,000 |

| Compliance cost rise | 3–6% YOY |

| Insurance renewal rise (2024) | ~10% |

| Typical tax credits | UK 25%, IE 32%, CA 25–65% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Tinopolis PLC, with data-driven insights and trend analysis tailored to its media production and distribution footprint; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategies.

A concise, visually segmented PESTLE summary for Tinopolis PLC that can be dropped into presentations, shared across teams, and annotated for regional or business-line specifics to streamline strategy sessions and external risk discussions.

Economic factors

Advertising cycles and broadcaster budgets

Ad-market downturns compress broadcaster commissioning, shifting spend to lower‑risk formats; UK TV ad revenues fell notably in recessionary 2023–24, tightening commissioning pipelines. Streamers’ content budgets (global streaming content spend >$70bn in 2024) can support demand but are increasingly selective. Tinopolis’s diversification across 25+ genres buffers volatility, while flexible cost bases and co‑financing (covering ~30–40% of some projects) help sustain margins.

Currency volatility

Tinopolis faces FX exposure across GBP, USD and EUR; a stronger dollar (DXY ~103.5, GBP/USD ~1.27 July 2025) can boost USD-denominated distribution income while raising costs for overseas production. Active hedging and natural slate offsets have historically trimmed quarterly earnings volatility. Contracting key commissions in commissioning currencies further stabilises cash flows.

Cost inflation in production

Rising labor, set, travel and insurance costs—with studio hire and specialist crew day rates reported up to 25% higher in recent high-end unscripted and drama shoots—are squeezing Tinopolis PLC production margins.

Studio scarcity and equipment shortages have pushed some hire rates 20–40% above pre-pandemic levels, forcing tighter scheduling and higher contingency spend.

Efficiency gains from remote workflows and standardized production kits help protect gross margins, while negotiating escalators and cost-sharing with commissioners remains critical to pass through inflationary pressures.

Streaming platform procurement dynamics

Streamers increasingly favor global-rights, buyout models that limit back-end participation, pressuring producers; Netflix spent $17.3bn on content in 2023, underscoring scale and negotiating power. Greater budget discipline and ROI scrutiny have raised cancellation and renewal risk, while a balanced mix of domestic broadcaster commissions and international presales improves revenue visibility. Strong IP ownership preserves library value and long-term monetisation.

- Global buyouts concentrate negotiating power

- Netflix content spend: 17.3bn (2023)

- Mixed commissions + presales = better revenue visibility

- IP ownership sustains catalogue value

M&A and capital availability

Private capital interest, supported by roughly $2.5tn global private capital dry powder at end-2024 (Preqin), uplifts valuations and exit options for production assets, while Bank of England base rate around 5.25% in 2024 raises gap and deficit funding costs. Joint ventures enable capital-light entry into new genres and territories, and maintaining low leverage preserves resilience amid tighter credit.

- Private capital: $2.5tn dry powder (end-2024)

- Interest rates: BoE ~5.25% (2024)

- JV: capital-light expansion

- Low leverage: enhances credit resilience

AVMSD 30%, Brexit frictions & tax credits shift commission 180k complaints

Tinopolis faces ad-revenue cyclicality after UK TV ad declines in 2023–24, while global streaming spend (~$70bn in 2024) offers selective demand; diversification and co‑financing (~30–40%) support margins. FX (DXY ~103.5; GBP/USD ~1.27 Jul 2025) and rising costs (crew/studio +20–40%, crew day rates up to 25%) squeeze margins; low leverage and JVs preserve resilience.

| Metric | Value |

|---|---|

| Streaming spend 2024 | $70bn |

| Netflix 2023 | $17.3bn |

| Dry powder end‑2024 | $2.5tn |

| BoE base rate 2024 | ~5.25% |

Preview the Actual Deliverable

Tinopolis PLC PESTLE Analysis

The preview shown here is the exact Tinopolis PLC PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This document presents political, economic, social, technological, legal and environmental factors with actionable insights. No placeholders or teasers—what you see is the final file.