Tobu Railway Co. SWOT Analysis

Make Insightful Decisions Backed by Expert Research

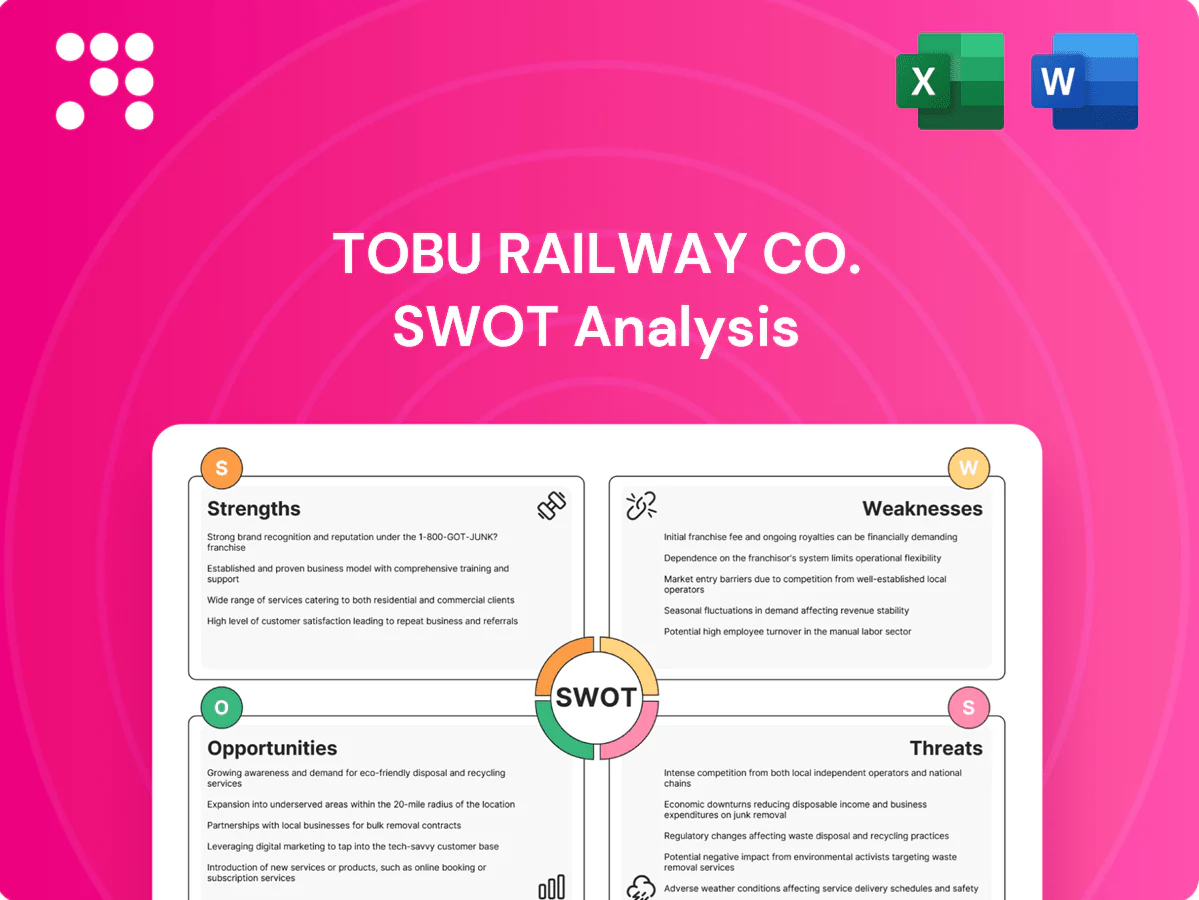

Tobu Railway shows strengths in an extensive rail network, integrated real-estate assets and diversified revenue streams, but faces challenges from Japan’s ageing population and urban ridership shifts. Opportunities include tourism growth and transit-oriented development, while competition and regulatory risks pose threats. Discover the complete picture behind the company’s market position with our full SWOT analysis—ideal for investors and strategists.

Strengths

Dominant Tokyo commuter footprint

Tobu’s dominant Tokyo commuter footprint links a 463 km private-rail network into the Greater Tokyo catchment (population ~37.5 million), yielding resilient daily ridership and recurring cash flows. Urban network effects and high‑value station catchments create natural entry barriers and stickiness for commuters. Strong peak‑hour demand sustains capacity utilization and operating leverage. Proximity to Tokyo’s ~2.0 trillion USD metro economy underpins long‑term traffic stability.

Diversified multi-segment revenues

Diversified revenues across railway, real estate, and leisure/tourism reduce dependence on any single economic cycle, while cross-segment synergies—integrating transport with retail, properties, and resorts—stabilize earnings through downturns. Non-fare income from station retail, advertising, and property leasing enhances margins and complements ticket revenue. This portfolio diversification supports stronger risk-adjusted returns for the group.

Integrated real estate portfolio

Station-area development captures uplift from passenger footfall by converting transit hubs into retail and office demand centers; mixed-use assets boost rent and retail turnover while driving long-term asset appreciation. Transit-oriented projects reinforce ridership and increase dwell time, and integrated planning across Tobu’s railway and real estate operations maximizes land-use efficiency and value creation.

Tourism and leisure synergies

Hotels, resorts and parks under the Tobu Group extend customer spend beyond transport by capturing lodging, dining and attraction revenue, while bundled rail-plus-stay products boost occupancy and off-peak utilization for both properties and trains. Destination development such as Nikko and Kinugawa strengthens Tobu’s regional brand and drives inbound tourism, and tourism assets create multiple touchpoints across planning, transit, stay and repeat-visit cycles.

- Integrated revenue capture

- Higher off-peak yield via bundles

- Stronger regional brand

- Multiple customer touchpoints

Brand, land bank, and long-term concessions

Tobu Railway, founded in 1897, leverages established brand trust to secure premium retail and property partnerships, owning landmark assets including Tokyo Skytree and Tobu Department Store; its rail network spans about 463 km, anchoring high-value station-front development. Long-dated concessions and legacy land holdings near stations provide scarce, strategic real estate and support multi-decade investment horizons, while the physical network scale is costly to replicate.

- Founded: 1897

- Network: ~463 km

- Landbank: station-front holdings, Skytree/department stores

- Concessions: long-dated rights supporting long-term returns

463 km Tokyo commuter network serving 37.5M

Tobu’s 463 km Tokyo commuter network serves a ~37.5M Greater Tokyo catchment, generating resilient daily ridership and recurring cash flows. Diversified revenues from rail, real estate and leisure—anchored by assets like Tokyo Skytree—enable integrated revenue capture and higher off‑peak yield. Long‑dated concessions and station‑front landbank (founded 1897) create strong entry barriers tied to Tokyo’s ~2.0T USD metro economy.

| Metric | Value |

|---|---|

| Network | ~463 km |

| Catchment population | ~37.5M |

| Founded | 1897 |

| Flagship asset | Tokyo Skytree |

| Tokyo metro GDP | ~2.0T USD |

What is included in the product

Delivers a strategic overview of Tobu Railway Co.’s internal strengths and external risks, outlining its network scale, diversified real-estate and retail assets, operational efficiencies and weaknesses, alongside growth opportunities in tourism and urban development and threats from demographic shifts, competition and regulatory pressures.

Provides a concise, editable SWOT matrix for Tobu Railway Co., enabling quick alignment on strengths, weaknesses, opportunities and threats; ideal for executives and analysts needing a strategic snapshot for presentations and rapid planning.

Weaknesses

High capex and maintenance

Rail infrastructure for Tobu Railway demands continuous heavy investment, with planned FY2024 capex of ¥45.0 billion, concentrating on track renewal and rolling stock upgrades. Aging assets elevate lifecycle costs and increase downtime risk, notably on older suburban lines where maintenance frequency has risen. Large capex outlays pressure free cash flow and can raise leverage during downturns. Project overruns or delays—common in complex civil works—can materially dilute returns.

Domestic and demographic concentration

Tobu Railway’s revenue is heavily tied to Japan’s mature Kanto market, limiting upside from overseas growth and non-Japan demand. Japan’s population aged 65+ is about 29% (2024), and long-term population decline contracts the domestic ridership base and retail footfall. Limited geographic diversification increases macro sensitivity, so regional shocks—natural disasters or local economic dips—can ripple across passenger, retail and real estate segments.

Regulated fares limit pricing

Regulated fares limit Tobu Railway’s ability to pass through cost inflation—Japan CPI rose about 3.2% in 2023—constraining revenue optimization despite higher input costs. Lengthy MLIT approval processes slow fare responses to demand shifts and tourism rebounds. Non-fare monetization (retail, real estate, station leasing) must offset constrained ticket yields, so margin expansion relies on efficiency gains rather than pricing power.

Operational complexity across segments

Managing rail, real estate and leisure businesses demands diverse capabilities and cross-functional coordination, increasing execution risk for Tobu Railway as investments and operational priorities conflict between transportation, property development and theme-park operations.

Higher corporate overheads and siloed decision-making across subsidiaries can slow responses to market shifts, while fragmented reporting makes performance transparency and timely capital allocation harder.

- Coordination risk between rail, real estate, leisure

- Elevated overheads and slower agility

- Siloed decision-making hinders integrated strategy

- Fragmented reporting reduces performance transparency

Tourism seasonality exposure

Tobu Railway's leisure assets face sharp seasonal demand swings tied to Golden Week, Obon and year-end peaks, exposing revenue to weather and tourism cycles; Japan recorded 31.9 million inbound visitors in 2023, highlighting recovery but persistent volatility. Off-peak utilization depresses returns and forces higher marketing spend to stabilize occupancy and attendance.

- Seasonal peaks: concentrated demand

- Weather sensitivity: revenue volatility

- Low off-peak utilization: lower yields

- Rising marketing costs: to smooth occupancy

Heavy FY2024 capex ¥45.0bn and aging assets raise lifecycle costs, dilute returns

Heavy FY2024 capex (¥45.0bn) and aging assets raise lifecycle costs and leverage risk; project delays can dilute returns. Reliance on mature Kanto market and Japan 65+ share ~29% (2024) limits ridership upside. Regulated fares (Japan CPI 3.2% in 2023) and seasonal leisure volatility (31.9m inbound visitors 2023) compress revenue flexibility.

| Metric | Value |

|---|---|

| FY2024 capex | ¥45.0bn |

| Japan 65+ (2024) | ~29% |

| Japan CPI (2023) | 3.2% |

| Inbound visitors (2023) | 31.9m |

Preview the Actual Deliverable

Tobu Railway Co. SWOT Analysis

This is the actual SWOT analysis document for Tobu Railway Co. you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same detailed strengths, weaknesses, opportunities and threats; the complete, editable version is unlocked after payment. Buy now to download the full file immediately.

Make Insightful Decisions Backed by Expert Research

Tobu Railway shows strengths in an extensive rail network, integrated real-estate assets and diversified revenue streams, but faces challenges from Japan’s ageing population and urban ridership shifts. Opportunities include tourism growth and transit-oriented development, while competition and regulatory risks pose threats. Discover the complete picture behind the company’s market position with our full SWOT analysis—ideal for investors and strategists.

Strengths

Dominant Tokyo commuter footprint

Tobu’s dominant Tokyo commuter footprint links a 463 km private-rail network into the Greater Tokyo catchment (population ~37.5 million), yielding resilient daily ridership and recurring cash flows. Urban network effects and high‑value station catchments create natural entry barriers and stickiness for commuters. Strong peak‑hour demand sustains capacity utilization and operating leverage. Proximity to Tokyo’s ~2.0 trillion USD metro economy underpins long‑term traffic stability.

Diversified multi-segment revenues

Diversified revenues across railway, real estate, and leisure/tourism reduce dependence on any single economic cycle, while cross-segment synergies—integrating transport with retail, properties, and resorts—stabilize earnings through downturns. Non-fare income from station retail, advertising, and property leasing enhances margins and complements ticket revenue. This portfolio diversification supports stronger risk-adjusted returns for the group.

Integrated real estate portfolio

Station-area development captures uplift from passenger footfall by converting transit hubs into retail and office demand centers; mixed-use assets boost rent and retail turnover while driving long-term asset appreciation. Transit-oriented projects reinforce ridership and increase dwell time, and integrated planning across Tobu’s railway and real estate operations maximizes land-use efficiency and value creation.

Tourism and leisure synergies

Hotels, resorts and parks under the Tobu Group extend customer spend beyond transport by capturing lodging, dining and attraction revenue, while bundled rail-plus-stay products boost occupancy and off-peak utilization for both properties and trains. Destination development such as Nikko and Kinugawa strengthens Tobu’s regional brand and drives inbound tourism, and tourism assets create multiple touchpoints across planning, transit, stay and repeat-visit cycles.

- Integrated revenue capture

- Higher off-peak yield via bundles

- Stronger regional brand

- Multiple customer touchpoints

Brand, land bank, and long-term concessions

Tobu Railway, founded in 1897, leverages established brand trust to secure premium retail and property partnerships, owning landmark assets including Tokyo Skytree and Tobu Department Store; its rail network spans about 463 km, anchoring high-value station-front development. Long-dated concessions and legacy land holdings near stations provide scarce, strategic real estate and support multi-decade investment horizons, while the physical network scale is costly to replicate.

- Founded: 1897

- Network: ~463 km

- Landbank: station-front holdings, Skytree/department stores

- Concessions: long-dated rights supporting long-term returns

463 km Tokyo commuter network serving 37.5M

Tobu’s 463 km Tokyo commuter network serves a ~37.5M Greater Tokyo catchment, generating resilient daily ridership and recurring cash flows. Diversified revenues from rail, real estate and leisure—anchored by assets like Tokyo Skytree—enable integrated revenue capture and higher off‑peak yield. Long‑dated concessions and station‑front landbank (founded 1897) create strong entry barriers tied to Tokyo’s ~2.0T USD metro economy.

| Metric | Value |

|---|---|

| Network | ~463 km |

| Catchment population | ~37.5M |

| Founded | 1897 |

| Flagship asset | Tokyo Skytree |

| Tokyo metro GDP | ~2.0T USD |

What is included in the product

Delivers a strategic overview of Tobu Railway Co.’s internal strengths and external risks, outlining its network scale, diversified real-estate and retail assets, operational efficiencies and weaknesses, alongside growth opportunities in tourism and urban development and threats from demographic shifts, competition and regulatory pressures.

Provides a concise, editable SWOT matrix for Tobu Railway Co., enabling quick alignment on strengths, weaknesses, opportunities and threats; ideal for executives and analysts needing a strategic snapshot for presentations and rapid planning.

Weaknesses

High capex and maintenance

Rail infrastructure for Tobu Railway demands continuous heavy investment, with planned FY2024 capex of ¥45.0 billion, concentrating on track renewal and rolling stock upgrades. Aging assets elevate lifecycle costs and increase downtime risk, notably on older suburban lines where maintenance frequency has risen. Large capex outlays pressure free cash flow and can raise leverage during downturns. Project overruns or delays—common in complex civil works—can materially dilute returns.

Domestic and demographic concentration

Tobu Railway’s revenue is heavily tied to Japan’s mature Kanto market, limiting upside from overseas growth and non-Japan demand. Japan’s population aged 65+ is about 29% (2024), and long-term population decline contracts the domestic ridership base and retail footfall. Limited geographic diversification increases macro sensitivity, so regional shocks—natural disasters or local economic dips—can ripple across passenger, retail and real estate segments.

Regulated fares limit pricing

Regulated fares limit Tobu Railway’s ability to pass through cost inflation—Japan CPI rose about 3.2% in 2023—constraining revenue optimization despite higher input costs. Lengthy MLIT approval processes slow fare responses to demand shifts and tourism rebounds. Non-fare monetization (retail, real estate, station leasing) must offset constrained ticket yields, so margin expansion relies on efficiency gains rather than pricing power.

Operational complexity across segments

Managing rail, real estate and leisure businesses demands diverse capabilities and cross-functional coordination, increasing execution risk for Tobu Railway as investments and operational priorities conflict between transportation, property development and theme-park operations.

Higher corporate overheads and siloed decision-making across subsidiaries can slow responses to market shifts, while fragmented reporting makes performance transparency and timely capital allocation harder.

- Coordination risk between rail, real estate, leisure

- Elevated overheads and slower agility

- Siloed decision-making hinders integrated strategy

- Fragmented reporting reduces performance transparency

Tourism seasonality exposure

Tobu Railway's leisure assets face sharp seasonal demand swings tied to Golden Week, Obon and year-end peaks, exposing revenue to weather and tourism cycles; Japan recorded 31.9 million inbound visitors in 2023, highlighting recovery but persistent volatility. Off-peak utilization depresses returns and forces higher marketing spend to stabilize occupancy and attendance.

- Seasonal peaks: concentrated demand

- Weather sensitivity: revenue volatility

- Low off-peak utilization: lower yields

- Rising marketing costs: to smooth occupancy

Heavy FY2024 capex ¥45.0bn and aging assets raise lifecycle costs, dilute returns

Heavy FY2024 capex (¥45.0bn) and aging assets raise lifecycle costs and leverage risk; project delays can dilute returns. Reliance on mature Kanto market and Japan 65+ share ~29% (2024) limits ridership upside. Regulated fares (Japan CPI 3.2% in 2023) and seasonal leisure volatility (31.9m inbound visitors 2023) compress revenue flexibility.

| Metric | Value |

|---|---|

| FY2024 capex | ¥45.0bn |

| Japan 65+ (2024) | ~29% |

| Japan CPI (2023) | 3.2% |

| Inbound visitors (2023) | 31.9m |

Preview the Actual Deliverable

Tobu Railway Co. SWOT Analysis

This is the actual SWOT analysis document for Tobu Railway Co. you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same detailed strengths, weaknesses, opportunities and threats; the complete, editable version is unlocked after payment. Buy now to download the full file immediately.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Tobu Railway shows strengths in an extensive rail network, integrated real-estate assets and diversified revenue streams, but faces challenges from Japan’s ageing population and urban ridership shifts. Opportunities include tourism growth and transit-oriented development, while competition and regulatory risks pose threats. Discover the complete picture behind the company’s market position with our full SWOT analysis—ideal for investors and strategists.

Strengths

Dominant Tokyo commuter footprint

Tobu’s dominant Tokyo commuter footprint links a 463 km private-rail network into the Greater Tokyo catchment (population ~37.5 million), yielding resilient daily ridership and recurring cash flows. Urban network effects and high‑value station catchments create natural entry barriers and stickiness for commuters. Strong peak‑hour demand sustains capacity utilization and operating leverage. Proximity to Tokyo’s ~2.0 trillion USD metro economy underpins long‑term traffic stability.

Diversified multi-segment revenues

Diversified revenues across railway, real estate, and leisure/tourism reduce dependence on any single economic cycle, while cross-segment synergies—integrating transport with retail, properties, and resorts—stabilize earnings through downturns. Non-fare income from station retail, advertising, and property leasing enhances margins and complements ticket revenue. This portfolio diversification supports stronger risk-adjusted returns for the group.

Integrated real estate portfolio

Station-area development captures uplift from passenger footfall by converting transit hubs into retail and office demand centers; mixed-use assets boost rent and retail turnover while driving long-term asset appreciation. Transit-oriented projects reinforce ridership and increase dwell time, and integrated planning across Tobu’s railway and real estate operations maximizes land-use efficiency and value creation.

Tourism and leisure synergies

Hotels, resorts and parks under the Tobu Group extend customer spend beyond transport by capturing lodging, dining and attraction revenue, while bundled rail-plus-stay products boost occupancy and off-peak utilization for both properties and trains. Destination development such as Nikko and Kinugawa strengthens Tobu’s regional brand and drives inbound tourism, and tourism assets create multiple touchpoints across planning, transit, stay and repeat-visit cycles.

- Integrated revenue capture

- Higher off-peak yield via bundles

- Stronger regional brand

- Multiple customer touchpoints

Brand, land bank, and long-term concessions

Tobu Railway, founded in 1897, leverages established brand trust to secure premium retail and property partnerships, owning landmark assets including Tokyo Skytree and Tobu Department Store; its rail network spans about 463 km, anchoring high-value station-front development. Long-dated concessions and legacy land holdings near stations provide scarce, strategic real estate and support multi-decade investment horizons, while the physical network scale is costly to replicate.

- Founded: 1897

- Network: ~463 km

- Landbank: station-front holdings, Skytree/department stores

- Concessions: long-dated rights supporting long-term returns

463 km Tokyo commuter network serving 37.5M

Tobu’s 463 km Tokyo commuter network serves a ~37.5M Greater Tokyo catchment, generating resilient daily ridership and recurring cash flows. Diversified revenues from rail, real estate and leisure—anchored by assets like Tokyo Skytree—enable integrated revenue capture and higher off‑peak yield. Long‑dated concessions and station‑front landbank (founded 1897) create strong entry barriers tied to Tokyo’s ~2.0T USD metro economy.

| Metric | Value |

|---|---|

| Network | ~463 km |

| Catchment population | ~37.5M |

| Founded | 1897 |

| Flagship asset | Tokyo Skytree |

| Tokyo metro GDP | ~2.0T USD |

What is included in the product

Delivers a strategic overview of Tobu Railway Co.’s internal strengths and external risks, outlining its network scale, diversified real-estate and retail assets, operational efficiencies and weaknesses, alongside growth opportunities in tourism and urban development and threats from demographic shifts, competition and regulatory pressures.

Provides a concise, editable SWOT matrix for Tobu Railway Co., enabling quick alignment on strengths, weaknesses, opportunities and threats; ideal for executives and analysts needing a strategic snapshot for presentations and rapid planning.

Weaknesses

High capex and maintenance

Rail infrastructure for Tobu Railway demands continuous heavy investment, with planned FY2024 capex of ¥45.0 billion, concentrating on track renewal and rolling stock upgrades. Aging assets elevate lifecycle costs and increase downtime risk, notably on older suburban lines where maintenance frequency has risen. Large capex outlays pressure free cash flow and can raise leverage during downturns. Project overruns or delays—common in complex civil works—can materially dilute returns.

Domestic and demographic concentration

Tobu Railway’s revenue is heavily tied to Japan’s mature Kanto market, limiting upside from overseas growth and non-Japan demand. Japan’s population aged 65+ is about 29% (2024), and long-term population decline contracts the domestic ridership base and retail footfall. Limited geographic diversification increases macro sensitivity, so regional shocks—natural disasters or local economic dips—can ripple across passenger, retail and real estate segments.

Regulated fares limit pricing

Regulated fares limit Tobu Railway’s ability to pass through cost inflation—Japan CPI rose about 3.2% in 2023—constraining revenue optimization despite higher input costs. Lengthy MLIT approval processes slow fare responses to demand shifts and tourism rebounds. Non-fare monetization (retail, real estate, station leasing) must offset constrained ticket yields, so margin expansion relies on efficiency gains rather than pricing power.

Operational complexity across segments

Managing rail, real estate and leisure businesses demands diverse capabilities and cross-functional coordination, increasing execution risk for Tobu Railway as investments and operational priorities conflict between transportation, property development and theme-park operations.

Higher corporate overheads and siloed decision-making across subsidiaries can slow responses to market shifts, while fragmented reporting makes performance transparency and timely capital allocation harder.

- Coordination risk between rail, real estate, leisure

- Elevated overheads and slower agility

- Siloed decision-making hinders integrated strategy

- Fragmented reporting reduces performance transparency

Tourism seasonality exposure

Tobu Railway's leisure assets face sharp seasonal demand swings tied to Golden Week, Obon and year-end peaks, exposing revenue to weather and tourism cycles; Japan recorded 31.9 million inbound visitors in 2023, highlighting recovery but persistent volatility. Off-peak utilization depresses returns and forces higher marketing spend to stabilize occupancy and attendance.

- Seasonal peaks: concentrated demand

- Weather sensitivity: revenue volatility

- Low off-peak utilization: lower yields

- Rising marketing costs: to smooth occupancy

Heavy FY2024 capex ¥45.0bn and aging assets raise lifecycle costs, dilute returns

Heavy FY2024 capex (¥45.0bn) and aging assets raise lifecycle costs and leverage risk; project delays can dilute returns. Reliance on mature Kanto market and Japan 65+ share ~29% (2024) limits ridership upside. Regulated fares (Japan CPI 3.2% in 2023) and seasonal leisure volatility (31.9m inbound visitors 2023) compress revenue flexibility.

| Metric | Value |

|---|---|

| FY2024 capex | ¥45.0bn |

| Japan 65+ (2024) | ~29% |

| Japan CPI (2023) | 3.2% |

| Inbound visitors (2023) | 31.9m |

Preview the Actual Deliverable

Tobu Railway Co. SWOT Analysis

This is the actual SWOT analysis document for Tobu Railway Co. you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same detailed strengths, weaknesses, opportunities and threats; the complete, editable version is unlocked after payment. Buy now to download the full file immediately.