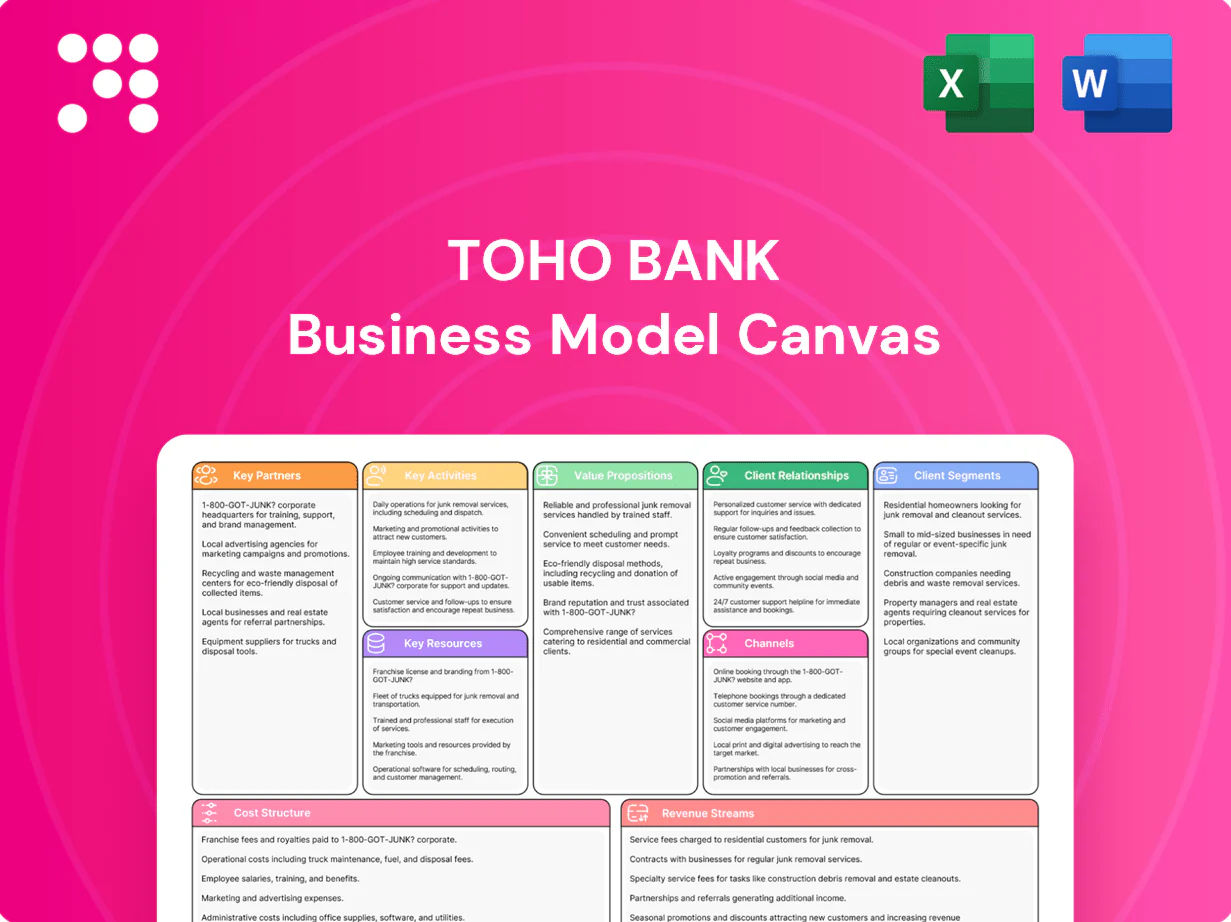

Toho Bank Business Model Canvas

Unlock a concise, actionable Business Model Canvas to map value, customers, revenue and partners

Unlock the full strategic blueprint behind Toho Bank’s business model in a concise, actionable Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants, and founders—download the complete Word/Excel canvas to benchmark strategy and unlock growth opportunities.

Partnerships

Local governments

Partnerships with Fukushima Prefecture and 59 municipal offices support regional development lending and public projects across the prefecture. Coordination enables targeted disaster recovery financing and infrastructure upgrades linked to post-2011 reconstruction efforts. Joint programs enhance financial inclusion and efficiently channel prefectural and national subsidies to local businesses and residents.

SME groups and chambers

Collaboration with SME groups and chambers boosts Toho Bank's reach into Japan's SME sector, which represents 99.7% of firms and employs about 70.7% of the workforce (2024). Co-hosted seminars reveal credit gaps and advisory demand, creating pipelines for loans and services. Data sharing and formal referrals accelerate underwriting and strengthen post-loan support coordination.

Fintech and IT vendors

Alliances with digital payment, core banking, and cybersecurity providers accelerate Toho Bank’s modernization, reducing integration risk and enabling rapid deployment. APIs enable services like eKYC and cashless solutions; Japan’s cashless payment ratio reached 51.2% in 2024 (METI). Vendors help scale securely while controlling costs and time-to-market, often cutting rollout timelines by 30–50% through modular platforms.

Regional financial institutions

Regional financial institutions: Syndications with other regional banks and credit unions diversify risk and, in 2024, Toho Bank joined syndicates covering regional projects totaling about ¥50 billion, lowering single-lender exposure.

Co-lending arrangements expand ticket sizes for larger local infrastructure and SME projects, enabling participation in deals up to ¥5 billion per project in 2024.

Liquidity lines and shared settlement networks with regional partners improved service reliability, cutting settlement disruptions by an estimated 15% in 2024.

- Syndications diversify risk — participated in ¥50bn (2024)

- Co-lending — enables ¥5bn project tickets (2024)

- Liquidity & settlements — ~15% fewer disruptions (2024)

Credit guarantee and public agencies

Ties with credit guarantee corporations let Toho Bank offer guarantees that can cover up to 80% of SME loan principal, materially reducing collateral demands and expanding credit access.

Government-backed programs and interest-subsidy schemes lower effective borrowing costs by roughly 0.5–1.5 percentage points for priority sectors, improving affordability.

Collaboration with public agencies increases approval rates by an estimated 10–20 percentage points and cushions credit risk through shared loss coverage.

- coverage: up to 80%

- rate relief: −0.5–1.5 pp

- approval lift: +10–20 pp

Regional partnerships boost SME lending: ¥50bn syndicates, ¥5bn co-lending, approvals +10–20 pp

Toho Bank’s key partnerships with 59 municipalities, SME groups, fintechs, regional banks and credit guarantee corporations drive regional lending, digital rollout and risk-sharing—supporting ¥50bn syndicates and ¥5bn co-lending capacity in 2024. Collaborations raised SME outreach into a sector that is 99.7% of firms and employs 70.7% of workers, cut settlement disruptions ~15% and leverage guarantees up to 80% to lift approvals +10–20 pp.

| Metric | Value (2024) |

|---|---|

| Municipal partners | 59 |

| Syndicates | ¥50bn |

| Co-lending ticket | ¥5bn |

| Cashless ratio | 51.2% |

| SME share | 99.7% firms / 70.7% workforce |

| Settlement improvement | −15% |

| Guarantee coverage | Up to 80% |

| Rate relief | −0.5–1.5 pp |

| Approval lift | +10–20 pp |

What is included in the product

A concise Business Model Canvas for Toho Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners, plus cost structure and governance. Ideal for presentations, investor discussions and strategic analysis with linked SWOT insights and competitive advantages.

High-level view of Toho Bank’s business model with editable cells, condensing strategy into a digestible one-page snapshot that saves hours of formatting and is perfect for boardrooms or team collaboration.

Activities

Deposit mobilization

Deposit mobilization focuses on attracting and retaining retail and corporate deposits to fund lending, with product design spanning regular, time and foreign-currency accounts tailored to liquidity and FX needs. Pricing and campaigns balance deposit stability and cost of funds through tiered rates and targeted promotions; Japan household deposits stood near ¥1,900 trillion in 2024, underscoring ample retail liquidity to tap.

Lending and underwriting

Origination of mortgages, SME loans and working capital drives Toho Bank’s growth, with targeted product pipelines and branch/digital channels focused on Fukushima and surrounding prefectures. Robust credit assessment, strict collateral management and sector limits contain credit risk. Ongoing portfolio monitoring and stress-testing enable early problem detection and proactive workout measures.

Risk and compliance management

Toho Bank actively manages ALM to control interest-rate and liquidity risk, maintaining compliance with 2024 Basel III minimum CET1 plus conservation buffer (total 7%) and a 100% LCR standard; robust AML/CFT and KYC processes plus timely regulatory reporting safeguard integrity; regular stress tests with multi-year scenarios inform provisioning policies, strengthening capital and liquidity resilience.

Digital platform development

Enhancing online and mobile banking improves convenience for customers and reduces branch load; in 2024 Japan’s cashless payment ratio exceeded 40%, reinforcing digital demand. Integrations enable seamless payments, transfers and remote onboarding, shortening activation times and increasing transaction volume. Continuous UX and security upgrades (biometrics, MFA, API hardening) lift adoption and lower fraud rates.

- 2024 cashless ratio >40%

- Remote onboarding: faster activation

- Biometrics & MFA for security

Community engagement and advisory

- Workshops for entrepreneurs

- Succession, export, cashflow advice

- Financial education for households

- Targets SME retention and deposit growth

Mobilize deposits to fund Fukushima mortgages and SMEs with ¥1,900T pool

Deposit mobilization targets retail/corporate funds (Japan household deposits ≈ ¥1,900T in 2024) to fund mortgages, SME and working-capital loans focused on Fukushima region; strong credit controls and portfolio stress-testing limit losses. ALM maintains Basel III CET1+buffer 7% and LCR 100%. Digital channels (cashless >40% 2024) and SME workshops (SMEs 99.7% of firms) drive acquisition and retention.

| Metric | 2024 |

|---|---|

| Household deposits | ¥1,900T |

| Household assets | ¥2,200T |

| Cashless ratio | >40% |

| SME share | 99.7% |

| CET1+buffer | 7% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual Toho Bank Business Model Canvas, not a mockup or teaser. When you purchase, you’ll receive this exact file—complete, editable, and formatted just as shown. Delivery includes the full document ready for download in Word and Excel formats.

Unlock a concise, actionable Business Model Canvas to map value, customers, revenue and partners

Unlock the full strategic blueprint behind Toho Bank’s business model in a concise, actionable Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants, and founders—download the complete Word/Excel canvas to benchmark strategy and unlock growth opportunities.

Partnerships

Local governments

Partnerships with Fukushima Prefecture and 59 municipal offices support regional development lending and public projects across the prefecture. Coordination enables targeted disaster recovery financing and infrastructure upgrades linked to post-2011 reconstruction efforts. Joint programs enhance financial inclusion and efficiently channel prefectural and national subsidies to local businesses and residents.

SME groups and chambers

Collaboration with SME groups and chambers boosts Toho Bank's reach into Japan's SME sector, which represents 99.7% of firms and employs about 70.7% of the workforce (2024). Co-hosted seminars reveal credit gaps and advisory demand, creating pipelines for loans and services. Data sharing and formal referrals accelerate underwriting and strengthen post-loan support coordination.

Fintech and IT vendors

Alliances with digital payment, core banking, and cybersecurity providers accelerate Toho Bank’s modernization, reducing integration risk and enabling rapid deployment. APIs enable services like eKYC and cashless solutions; Japan’s cashless payment ratio reached 51.2% in 2024 (METI). Vendors help scale securely while controlling costs and time-to-market, often cutting rollout timelines by 30–50% through modular platforms.

Regional financial institutions

Regional financial institutions: Syndications with other regional banks and credit unions diversify risk and, in 2024, Toho Bank joined syndicates covering regional projects totaling about ¥50 billion, lowering single-lender exposure.

Co-lending arrangements expand ticket sizes for larger local infrastructure and SME projects, enabling participation in deals up to ¥5 billion per project in 2024.

Liquidity lines and shared settlement networks with regional partners improved service reliability, cutting settlement disruptions by an estimated 15% in 2024.

- Syndications diversify risk — participated in ¥50bn (2024)

- Co-lending — enables ¥5bn project tickets (2024)

- Liquidity & settlements — ~15% fewer disruptions (2024)

Credit guarantee and public agencies

Ties with credit guarantee corporations let Toho Bank offer guarantees that can cover up to 80% of SME loan principal, materially reducing collateral demands and expanding credit access.

Government-backed programs and interest-subsidy schemes lower effective borrowing costs by roughly 0.5–1.5 percentage points for priority sectors, improving affordability.

Collaboration with public agencies increases approval rates by an estimated 10–20 percentage points and cushions credit risk through shared loss coverage.

- coverage: up to 80%

- rate relief: −0.5–1.5 pp

- approval lift: +10–20 pp

Regional partnerships boost SME lending: ¥50bn syndicates, ¥5bn co-lending, approvals +10–20 pp

Toho Bank’s key partnerships with 59 municipalities, SME groups, fintechs, regional banks and credit guarantee corporations drive regional lending, digital rollout and risk-sharing—supporting ¥50bn syndicates and ¥5bn co-lending capacity in 2024. Collaborations raised SME outreach into a sector that is 99.7% of firms and employs 70.7% of workers, cut settlement disruptions ~15% and leverage guarantees up to 80% to lift approvals +10–20 pp.

| Metric | Value (2024) |

|---|---|

| Municipal partners | 59 |

| Syndicates | ¥50bn |

| Co-lending ticket | ¥5bn |

| Cashless ratio | 51.2% |

| SME share | 99.7% firms / 70.7% workforce |

| Settlement improvement | −15% |

| Guarantee coverage | Up to 80% |

| Rate relief | −0.5–1.5 pp |

| Approval lift | +10–20 pp |

What is included in the product

A concise Business Model Canvas for Toho Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners, plus cost structure and governance. Ideal for presentations, investor discussions and strategic analysis with linked SWOT insights and competitive advantages.

High-level view of Toho Bank’s business model with editable cells, condensing strategy into a digestible one-page snapshot that saves hours of formatting and is perfect for boardrooms or team collaboration.

Activities

Deposit mobilization

Deposit mobilization focuses on attracting and retaining retail and corporate deposits to fund lending, with product design spanning regular, time and foreign-currency accounts tailored to liquidity and FX needs. Pricing and campaigns balance deposit stability and cost of funds through tiered rates and targeted promotions; Japan household deposits stood near ¥1,900 trillion in 2024, underscoring ample retail liquidity to tap.

Lending and underwriting

Origination of mortgages, SME loans and working capital drives Toho Bank’s growth, with targeted product pipelines and branch/digital channels focused on Fukushima and surrounding prefectures. Robust credit assessment, strict collateral management and sector limits contain credit risk. Ongoing portfolio monitoring and stress-testing enable early problem detection and proactive workout measures.

Risk and compliance management

Toho Bank actively manages ALM to control interest-rate and liquidity risk, maintaining compliance with 2024 Basel III minimum CET1 plus conservation buffer (total 7%) and a 100% LCR standard; robust AML/CFT and KYC processes plus timely regulatory reporting safeguard integrity; regular stress tests with multi-year scenarios inform provisioning policies, strengthening capital and liquidity resilience.

Digital platform development

Enhancing online and mobile banking improves convenience for customers and reduces branch load; in 2024 Japan’s cashless payment ratio exceeded 40%, reinforcing digital demand. Integrations enable seamless payments, transfers and remote onboarding, shortening activation times and increasing transaction volume. Continuous UX and security upgrades (biometrics, MFA, API hardening) lift adoption and lower fraud rates.

- 2024 cashless ratio >40%

- Remote onboarding: faster activation

- Biometrics & MFA for security

Community engagement and advisory

- Workshops for entrepreneurs

- Succession, export, cashflow advice

- Financial education for households

- Targets SME retention and deposit growth

Mobilize deposits to fund Fukushima mortgages and SMEs with ¥1,900T pool

Deposit mobilization targets retail/corporate funds (Japan household deposits ≈ ¥1,900T in 2024) to fund mortgages, SME and working-capital loans focused on Fukushima region; strong credit controls and portfolio stress-testing limit losses. ALM maintains Basel III CET1+buffer 7% and LCR 100%. Digital channels (cashless >40% 2024) and SME workshops (SMEs 99.7% of firms) drive acquisition and retention.

| Metric | 2024 |

|---|---|

| Household deposits | ¥1,900T |

| Household assets | ¥2,200T |

| Cashless ratio | >40% |

| SME share | 99.7% |

| CET1+buffer | 7% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual Toho Bank Business Model Canvas, not a mockup or teaser. When you purchase, you’ll receive this exact file—complete, editable, and formatted just as shown. Delivery includes the full document ready for download in Word and Excel formats.

Description

Unlock a concise, actionable Business Model Canvas to map value, customers, revenue and partners

Unlock the full strategic blueprint behind Toho Bank’s business model in a concise, actionable Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. Ideal for investors, consultants, and founders—download the complete Word/Excel canvas to benchmark strategy and unlock growth opportunities.

Partnerships

Local governments

Partnerships with Fukushima Prefecture and 59 municipal offices support regional development lending and public projects across the prefecture. Coordination enables targeted disaster recovery financing and infrastructure upgrades linked to post-2011 reconstruction efforts. Joint programs enhance financial inclusion and efficiently channel prefectural and national subsidies to local businesses and residents.

SME groups and chambers

Collaboration with SME groups and chambers boosts Toho Bank's reach into Japan's SME sector, which represents 99.7% of firms and employs about 70.7% of the workforce (2024). Co-hosted seminars reveal credit gaps and advisory demand, creating pipelines for loans and services. Data sharing and formal referrals accelerate underwriting and strengthen post-loan support coordination.

Fintech and IT vendors

Alliances with digital payment, core banking, and cybersecurity providers accelerate Toho Bank’s modernization, reducing integration risk and enabling rapid deployment. APIs enable services like eKYC and cashless solutions; Japan’s cashless payment ratio reached 51.2% in 2024 (METI). Vendors help scale securely while controlling costs and time-to-market, often cutting rollout timelines by 30–50% through modular platforms.

Regional financial institutions

Regional financial institutions: Syndications with other regional banks and credit unions diversify risk and, in 2024, Toho Bank joined syndicates covering regional projects totaling about ¥50 billion, lowering single-lender exposure.

Co-lending arrangements expand ticket sizes for larger local infrastructure and SME projects, enabling participation in deals up to ¥5 billion per project in 2024.

Liquidity lines and shared settlement networks with regional partners improved service reliability, cutting settlement disruptions by an estimated 15% in 2024.

- Syndications diversify risk — participated in ¥50bn (2024)

- Co-lending — enables ¥5bn project tickets (2024)

- Liquidity & settlements — ~15% fewer disruptions (2024)

Credit guarantee and public agencies

Ties with credit guarantee corporations let Toho Bank offer guarantees that can cover up to 80% of SME loan principal, materially reducing collateral demands and expanding credit access.

Government-backed programs and interest-subsidy schemes lower effective borrowing costs by roughly 0.5–1.5 percentage points for priority sectors, improving affordability.

Collaboration with public agencies increases approval rates by an estimated 10–20 percentage points and cushions credit risk through shared loss coverage.

- coverage: up to 80%

- rate relief: −0.5–1.5 pp

- approval lift: +10–20 pp

Regional partnerships boost SME lending: ¥50bn syndicates, ¥5bn co-lending, approvals +10–20 pp

Toho Bank’s key partnerships with 59 municipalities, SME groups, fintechs, regional banks and credit guarantee corporations drive regional lending, digital rollout and risk-sharing—supporting ¥50bn syndicates and ¥5bn co-lending capacity in 2024. Collaborations raised SME outreach into a sector that is 99.7% of firms and employs 70.7% of workers, cut settlement disruptions ~15% and leverage guarantees up to 80% to lift approvals +10–20 pp.

| Metric | Value (2024) |

|---|---|

| Municipal partners | 59 |

| Syndicates | ¥50bn |

| Co-lending ticket | ¥5bn |

| Cashless ratio | 51.2% |

| SME share | 99.7% firms / 70.7% workforce |

| Settlement improvement | −15% |

| Guarantee coverage | Up to 80% |

| Rate relief | −0.5–1.5 pp |

| Approval lift | +10–20 pp |

What is included in the product

A concise Business Model Canvas for Toho Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners, plus cost structure and governance. Ideal for presentations, investor discussions and strategic analysis with linked SWOT insights and competitive advantages.

High-level view of Toho Bank’s business model with editable cells, condensing strategy into a digestible one-page snapshot that saves hours of formatting and is perfect for boardrooms or team collaboration.

Activities

Deposit mobilization

Deposit mobilization focuses on attracting and retaining retail and corporate deposits to fund lending, with product design spanning regular, time and foreign-currency accounts tailored to liquidity and FX needs. Pricing and campaigns balance deposit stability and cost of funds through tiered rates and targeted promotions; Japan household deposits stood near ¥1,900 trillion in 2024, underscoring ample retail liquidity to tap.

Lending and underwriting

Origination of mortgages, SME loans and working capital drives Toho Bank’s growth, with targeted product pipelines and branch/digital channels focused on Fukushima and surrounding prefectures. Robust credit assessment, strict collateral management and sector limits contain credit risk. Ongoing portfolio monitoring and stress-testing enable early problem detection and proactive workout measures.

Risk and compliance management

Toho Bank actively manages ALM to control interest-rate and liquidity risk, maintaining compliance with 2024 Basel III minimum CET1 plus conservation buffer (total 7%) and a 100% LCR standard; robust AML/CFT and KYC processes plus timely regulatory reporting safeguard integrity; regular stress tests with multi-year scenarios inform provisioning policies, strengthening capital and liquidity resilience.

Digital platform development

Enhancing online and mobile banking improves convenience for customers and reduces branch load; in 2024 Japan’s cashless payment ratio exceeded 40%, reinforcing digital demand. Integrations enable seamless payments, transfers and remote onboarding, shortening activation times and increasing transaction volume. Continuous UX and security upgrades (biometrics, MFA, API hardening) lift adoption and lower fraud rates.

- 2024 cashless ratio >40%

- Remote onboarding: faster activation

- Biometrics & MFA for security

Community engagement and advisory

- Workshops for entrepreneurs

- Succession, export, cashflow advice

- Financial education for households

- Targets SME retention and deposit growth

Mobilize deposits to fund Fukushima mortgages and SMEs with ¥1,900T pool

Deposit mobilization targets retail/corporate funds (Japan household deposits ≈ ¥1,900T in 2024) to fund mortgages, SME and working-capital loans focused on Fukushima region; strong credit controls and portfolio stress-testing limit losses. ALM maintains Basel III CET1+buffer 7% and LCR 100%. Digital channels (cashless >40% 2024) and SME workshops (SMEs 99.7% of firms) drive acquisition and retention.

| Metric | 2024 |

|---|---|

| Household deposits | ¥1,900T |

| Household assets | ¥2,200T |

| Cashless ratio | >40% |

| SME share | 99.7% |

| CET1+buffer | 7% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual Toho Bank Business Model Canvas, not a mockup or teaser. When you purchase, you’ll receive this exact file—complete, editable, and formatted just as shown. Delivery includes the full document ready for download in Word and Excel formats.