Tokai Carbon Porter's Five Forces Analysis

Don't Miss the Bigger Picture

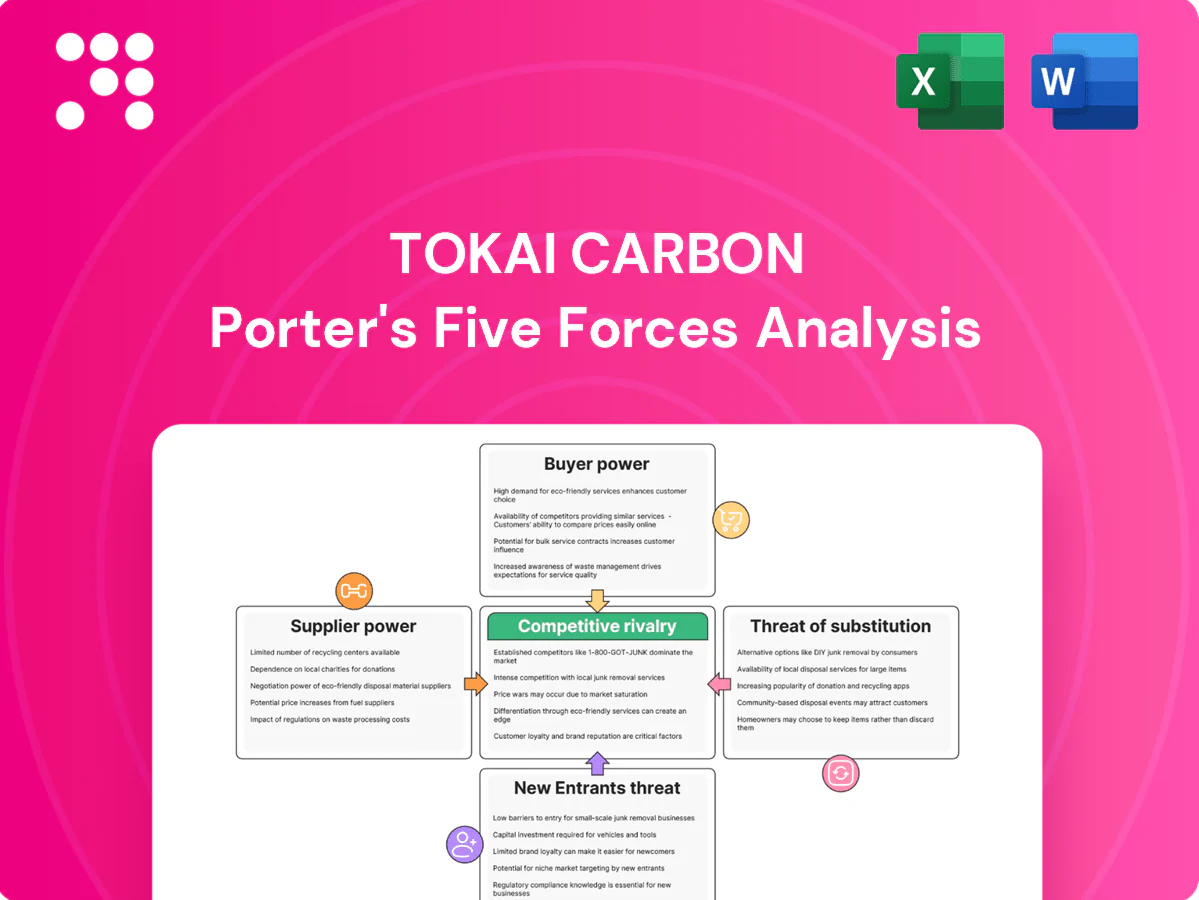

Tokai Carbon's Porter's Five Forces highlights concentrated supplier power for specialty carbon feedstocks, moderate buyer power from industrial clients, high barriers to entry from capital intensity and IP, strong rivalry among global producers, and moderate threat from substitutes tied to material innovation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tokai Carbon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Needle coke, petroleum coke, pitch and specialty precursors come from a highly concentrated global supplier set, giving vendors outsized leverage over Tokai Carbon. Few UHP-grade needle coke producers can set prices and allocation in tight markets, while supplier consolidation and specialization have amplified dependency and pricing power. Tokai Carbon must diversify sources and lock multi-year agreements to mitigate supply shocks.

Energy and logistics exposure

Graphitization and furnace operations are highly energy intensive, tying Tokai Carbon's cost base directly to power and gas market swings and making unit margins sensitive to energy-price volatility. Transport of bulky carbon products and hazardous feedstocks adds freight cost variability and susceptibility to rate spikes during port congestion. Regional energy or port disruptions can compress margins quickly and long-haul import dependence increases exposure to geopolitical and supply-chain interruptions.

Quality and qualification lock-in

Semiconductor-grade graphite demands audited quality systems and ultra-high purity (typically 5N+ or higher), and only a small number of suppliers meet these specs, raising their leverage. Supplier switches risk immediate yield loss and requalification periods often lasting 6–12 months, creating technical lock-in that elevates supplier bargaining power in specialty lines.

Limited backward integration

Tokai Carbon has deep process expertise but limited backward integration into needle coke, so upstream access is partial and constrains supplier leverage; in 2024 needle coke supply remained tight amid rising EV anode demand. Vertical integration by peers and oil majors increases squeeze on independents, and without captive feedstock Tokai’s negotiation power weakens in price upcycles. Strategic alliances mitigate but do not remove exposure.

- Partial upstream access limits leverage

- 2024: tight needle coke market vs pre-2020

- Peers' vertical integration raises pressure

- Alliances reduce but not eliminate supply risk

ESG and regulatory constraints

- 2024 EU ETS ~€95/t

- CBAM raising import tariffs

- REACH/waste rules tightening supplier capacity

- High pass-through and supply-tightening risk for Tokai Carbon

Tight needle coke supply and high EU ETS costs squeeze graphite margins

Suppliers of needle coke, pitch and specialty precursors are highly concentrated, giving vendors strong pricing and allocation power; 2024 needle coke supply remained tight amid rising EV anode demand. Energy and freight cost swings (EU ETS ~€95/t in 2024) amplify margin exposure. Technical lock‑in for 5N+ graphite and limited backward integration constrain Tokai Carbon's bargaining leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Needle coke tightness | High | Price/allocations leverage |

| EU ETS | ~€95/t | Higher feedstock cost pass‑through |

| Supplier count (UHP) | Few | Switching risk 6–12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Tokai Carbon revealing competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that protect margins and market share. Actionable insights pinpoint emerging disruptors, raw-material risks, and areas to strengthen competitive advantage.

Clear one-sheet Porter's Five Forces for Tokai Carbon—customize pressure levels and swap in your data to instantly visualize strategic threats with a spider chart, ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Concentrated customer base

Steel EAF mills, global tire majors and leading semiconductor fabs represent concentrated, high-volume buyers—EAFs accounted for about 28% of global crude steel output in 2023 (World Steel), while top fabs like TSMC invested ~32.6 billion USD in 2023—giving these customers strong leverage on price and service terms.

Price sensitivity in commodities

Price transparency in carbon black and standard electrodes leaves Tokai Carbon exposed as buyers benchmark suppliers globally, and spot carbon black prices fell c.20% year‑on‑year in 2024 amid weak tyre and rubber demand. Buyers push for steep discounts in downturns and index‑linked contracts—common across the industry—limit Tokai’s pricing discretion. Ready substitution across grades and cross‑supplier sourcing further strengthens customer bargaining power.

High switching costs in specialty

In fine carbon and semiconductor graphite requalification is lengthy and risky, often taking months and involving complex process integration and custom machining that curb supplier switches. Buyers prioritize reliability over lowest price, reducing price-driven negotiation and easing margin pressure on suppliers. With global semiconductor wafer fab investment topping roughly $100 billion in 2024, Tokai Carbon captures pockets of pricing power in critical, high-spec niches.

Demand cyclicality

Steel, automotive, and electronics cycles compress order visibility and swing buyer leverage; in downcycles customers commonly delay orders and press for price, extended payment, or volume discounts.

In upcycles allocation shifts power to suppliers but often forces long-term price concessions; Tokai Carbon must balance higher utilization against margin discipline and contract terms.

Global vehicle production reached about 80 million units in 2024 (OICA), amplifying cyclic recovery effects on demand patterns.

- Downcycle: delayed orders, renegotiation

- Upcycle: allocation power, concession risk

- Strategy: prioritize utilization with strict margin controls

Service and solutions expectations

Customers demand application engineering, rapid machining and reliable global delivery, pushing suppliers to offer technical support and inventory programs that win share and raise service cost to serve while embedding performance-based penalties; superior support can soften price pressure in critical accounts.

- Service-driven share gains

- Higher cost-to-serve

- Performance penalties embedded

- Support reduces price negotiation

Buyers gain price leverage as carbon black falls 20% and fabs keep niche pricing

Concentrated buyers (EAFs 28% of crude steel 2023; TSMC capex $32.6bn 2023; wafer‑fab spend ~$100bn 2024) exert strong price/service leverage; spot carbon black fell ~20% YoY in 2024, boosting buyer bargaining in downturns. Long requalification for semiconductor grades limits switches and preserves niche pricing power. Customers demand engineering, fast machining and global delivery, raising cost‑to‑serve but softening pure price pressure.

| Buyer | 2023/24 stat | Leverage |

|---|---|---|

| Steel EAFs | 28% crude steel 2023 | High |

| Tire majors | Carbon black -20% YoY 2024 | High |

| Semiconductor fabs | $100bn fab spend 2024 | Medium-High |

What You See Is What You Get

Tokai Carbon Porter's Five Forces Analysis

This Tokai Carbon Porter’s Five Forces Analysis preview is the exact, fully formatted document you will receive upon purchase; no placeholders or samples. It provides the complete strategic assessment ready for immediate download and use. Buy once and access this same file instantly—professionally prepared and decision-ready.

Don't Miss the Bigger Picture

Tokai Carbon's Porter's Five Forces highlights concentrated supplier power for specialty carbon feedstocks, moderate buyer power from industrial clients, high barriers to entry from capital intensity and IP, strong rivalry among global producers, and moderate threat from substitutes tied to material innovation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tokai Carbon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Needle coke, petroleum coke, pitch and specialty precursors come from a highly concentrated global supplier set, giving vendors outsized leverage over Tokai Carbon. Few UHP-grade needle coke producers can set prices and allocation in tight markets, while supplier consolidation and specialization have amplified dependency and pricing power. Tokai Carbon must diversify sources and lock multi-year agreements to mitigate supply shocks.

Energy and logistics exposure

Graphitization and furnace operations are highly energy intensive, tying Tokai Carbon's cost base directly to power and gas market swings and making unit margins sensitive to energy-price volatility. Transport of bulky carbon products and hazardous feedstocks adds freight cost variability and susceptibility to rate spikes during port congestion. Regional energy or port disruptions can compress margins quickly and long-haul import dependence increases exposure to geopolitical and supply-chain interruptions.

Quality and qualification lock-in

Semiconductor-grade graphite demands audited quality systems and ultra-high purity (typically 5N+ or higher), and only a small number of suppliers meet these specs, raising their leverage. Supplier switches risk immediate yield loss and requalification periods often lasting 6–12 months, creating technical lock-in that elevates supplier bargaining power in specialty lines.

Limited backward integration

Tokai Carbon has deep process expertise but limited backward integration into needle coke, so upstream access is partial and constrains supplier leverage; in 2024 needle coke supply remained tight amid rising EV anode demand. Vertical integration by peers and oil majors increases squeeze on independents, and without captive feedstock Tokai’s negotiation power weakens in price upcycles. Strategic alliances mitigate but do not remove exposure.

- Partial upstream access limits leverage

- 2024: tight needle coke market vs pre-2020

- Peers' vertical integration raises pressure

- Alliances reduce but not eliminate supply risk

ESG and regulatory constraints

- 2024 EU ETS ~€95/t

- CBAM raising import tariffs

- REACH/waste rules tightening supplier capacity

- High pass-through and supply-tightening risk for Tokai Carbon

Tight needle coke supply and high EU ETS costs squeeze graphite margins

Suppliers of needle coke, pitch and specialty precursors are highly concentrated, giving vendors strong pricing and allocation power; 2024 needle coke supply remained tight amid rising EV anode demand. Energy and freight cost swings (EU ETS ~€95/t in 2024) amplify margin exposure. Technical lock‑in for 5N+ graphite and limited backward integration constrain Tokai Carbon's bargaining leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Needle coke tightness | High | Price/allocations leverage |

| EU ETS | ~€95/t | Higher feedstock cost pass‑through |

| Supplier count (UHP) | Few | Switching risk 6–12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Tokai Carbon revealing competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that protect margins and market share. Actionable insights pinpoint emerging disruptors, raw-material risks, and areas to strengthen competitive advantage.

Clear one-sheet Porter's Five Forces for Tokai Carbon—customize pressure levels and swap in your data to instantly visualize strategic threats with a spider chart, ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Concentrated customer base

Steel EAF mills, global tire majors and leading semiconductor fabs represent concentrated, high-volume buyers—EAFs accounted for about 28% of global crude steel output in 2023 (World Steel), while top fabs like TSMC invested ~32.6 billion USD in 2023—giving these customers strong leverage on price and service terms.

Price sensitivity in commodities

Price transparency in carbon black and standard electrodes leaves Tokai Carbon exposed as buyers benchmark suppliers globally, and spot carbon black prices fell c.20% year‑on‑year in 2024 amid weak tyre and rubber demand. Buyers push for steep discounts in downturns and index‑linked contracts—common across the industry—limit Tokai’s pricing discretion. Ready substitution across grades and cross‑supplier sourcing further strengthens customer bargaining power.

High switching costs in specialty

In fine carbon and semiconductor graphite requalification is lengthy and risky, often taking months and involving complex process integration and custom machining that curb supplier switches. Buyers prioritize reliability over lowest price, reducing price-driven negotiation and easing margin pressure on suppliers. With global semiconductor wafer fab investment topping roughly $100 billion in 2024, Tokai Carbon captures pockets of pricing power in critical, high-spec niches.

Demand cyclicality

Steel, automotive, and electronics cycles compress order visibility and swing buyer leverage; in downcycles customers commonly delay orders and press for price, extended payment, or volume discounts.

In upcycles allocation shifts power to suppliers but often forces long-term price concessions; Tokai Carbon must balance higher utilization against margin discipline and contract terms.

Global vehicle production reached about 80 million units in 2024 (OICA), amplifying cyclic recovery effects on demand patterns.

- Downcycle: delayed orders, renegotiation

- Upcycle: allocation power, concession risk

- Strategy: prioritize utilization with strict margin controls

Service and solutions expectations

Customers demand application engineering, rapid machining and reliable global delivery, pushing suppliers to offer technical support and inventory programs that win share and raise service cost to serve while embedding performance-based penalties; superior support can soften price pressure in critical accounts.

- Service-driven share gains

- Higher cost-to-serve

- Performance penalties embedded

- Support reduces price negotiation

Buyers gain price leverage as carbon black falls 20% and fabs keep niche pricing

Concentrated buyers (EAFs 28% of crude steel 2023; TSMC capex $32.6bn 2023; wafer‑fab spend ~$100bn 2024) exert strong price/service leverage; spot carbon black fell ~20% YoY in 2024, boosting buyer bargaining in downturns. Long requalification for semiconductor grades limits switches and preserves niche pricing power. Customers demand engineering, fast machining and global delivery, raising cost‑to‑serve but softening pure price pressure.

| Buyer | 2023/24 stat | Leverage |

|---|---|---|

| Steel EAFs | 28% crude steel 2023 | High |

| Tire majors | Carbon black -20% YoY 2024 | High |

| Semiconductor fabs | $100bn fab spend 2024 | Medium-High |

What You See Is What You Get

Tokai Carbon Porter's Five Forces Analysis

This Tokai Carbon Porter’s Five Forces Analysis preview is the exact, fully formatted document you will receive upon purchase; no placeholders or samples. It provides the complete strategic assessment ready for immediate download and use. Buy once and access this same file instantly—professionally prepared and decision-ready.

Description

Don't Miss the Bigger Picture

Tokai Carbon's Porter's Five Forces highlights concentrated supplier power for specialty carbon feedstocks, moderate buyer power from industrial clients, high barriers to entry from capital intensity and IP, strong rivalry among global producers, and moderate threat from substitutes tied to material innovation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tokai Carbon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Needle coke, petroleum coke, pitch and specialty precursors come from a highly concentrated global supplier set, giving vendors outsized leverage over Tokai Carbon. Few UHP-grade needle coke producers can set prices and allocation in tight markets, while supplier consolidation and specialization have amplified dependency and pricing power. Tokai Carbon must diversify sources and lock multi-year agreements to mitigate supply shocks.

Energy and logistics exposure

Graphitization and furnace operations are highly energy intensive, tying Tokai Carbon's cost base directly to power and gas market swings and making unit margins sensitive to energy-price volatility. Transport of bulky carbon products and hazardous feedstocks adds freight cost variability and susceptibility to rate spikes during port congestion. Regional energy or port disruptions can compress margins quickly and long-haul import dependence increases exposure to geopolitical and supply-chain interruptions.

Quality and qualification lock-in

Semiconductor-grade graphite demands audited quality systems and ultra-high purity (typically 5N+ or higher), and only a small number of suppliers meet these specs, raising their leverage. Supplier switches risk immediate yield loss and requalification periods often lasting 6–12 months, creating technical lock-in that elevates supplier bargaining power in specialty lines.

Limited backward integration

Tokai Carbon has deep process expertise but limited backward integration into needle coke, so upstream access is partial and constrains supplier leverage; in 2024 needle coke supply remained tight amid rising EV anode demand. Vertical integration by peers and oil majors increases squeeze on independents, and without captive feedstock Tokai’s negotiation power weakens in price upcycles. Strategic alliances mitigate but do not remove exposure.

- Partial upstream access limits leverage

- 2024: tight needle coke market vs pre-2020

- Peers' vertical integration raises pressure

- Alliances reduce but not eliminate supply risk

ESG and regulatory constraints

- 2024 EU ETS ~€95/t

- CBAM raising import tariffs

- REACH/waste rules tightening supplier capacity

- High pass-through and supply-tightening risk for Tokai Carbon

Tight needle coke supply and high EU ETS costs squeeze graphite margins

Suppliers of needle coke, pitch and specialty precursors are highly concentrated, giving vendors strong pricing and allocation power; 2024 needle coke supply remained tight amid rising EV anode demand. Energy and freight cost swings (EU ETS ~€95/t in 2024) amplify margin exposure. Technical lock‑in for 5N+ graphite and limited backward integration constrain Tokai Carbon's bargaining leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Needle coke tightness | High | Price/allocations leverage |

| EU ETS | ~€95/t | Higher feedstock cost pass‑through |

| Supplier count (UHP) | Few | Switching risk 6–12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Tokai Carbon revealing competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that protect margins and market share. Actionable insights pinpoint emerging disruptors, raw-material risks, and areas to strengthen competitive advantage.

Clear one-sheet Porter's Five Forces for Tokai Carbon—customize pressure levels and swap in your data to instantly visualize strategic threats with a spider chart, ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Concentrated customer base

Steel EAF mills, global tire majors and leading semiconductor fabs represent concentrated, high-volume buyers—EAFs accounted for about 28% of global crude steel output in 2023 (World Steel), while top fabs like TSMC invested ~32.6 billion USD in 2023—giving these customers strong leverage on price and service terms.

Price sensitivity in commodities

Price transparency in carbon black and standard electrodes leaves Tokai Carbon exposed as buyers benchmark suppliers globally, and spot carbon black prices fell c.20% year‑on‑year in 2024 amid weak tyre and rubber demand. Buyers push for steep discounts in downturns and index‑linked contracts—common across the industry—limit Tokai’s pricing discretion. Ready substitution across grades and cross‑supplier sourcing further strengthens customer bargaining power.

High switching costs in specialty

In fine carbon and semiconductor graphite requalification is lengthy and risky, often taking months and involving complex process integration and custom machining that curb supplier switches. Buyers prioritize reliability over lowest price, reducing price-driven negotiation and easing margin pressure on suppliers. With global semiconductor wafer fab investment topping roughly $100 billion in 2024, Tokai Carbon captures pockets of pricing power in critical, high-spec niches.

Demand cyclicality

Steel, automotive, and electronics cycles compress order visibility and swing buyer leverage; in downcycles customers commonly delay orders and press for price, extended payment, or volume discounts.

In upcycles allocation shifts power to suppliers but often forces long-term price concessions; Tokai Carbon must balance higher utilization against margin discipline and contract terms.

Global vehicle production reached about 80 million units in 2024 (OICA), amplifying cyclic recovery effects on demand patterns.

- Downcycle: delayed orders, renegotiation

- Upcycle: allocation power, concession risk

- Strategy: prioritize utilization with strict margin controls

Service and solutions expectations

Customers demand application engineering, rapid machining and reliable global delivery, pushing suppliers to offer technical support and inventory programs that win share and raise service cost to serve while embedding performance-based penalties; superior support can soften price pressure in critical accounts.

- Service-driven share gains

- Higher cost-to-serve

- Performance penalties embedded

- Support reduces price negotiation

Buyers gain price leverage as carbon black falls 20% and fabs keep niche pricing

Concentrated buyers (EAFs 28% of crude steel 2023; TSMC capex $32.6bn 2023; wafer‑fab spend ~$100bn 2024) exert strong price/service leverage; spot carbon black fell ~20% YoY in 2024, boosting buyer bargaining in downturns. Long requalification for semiconductor grades limits switches and preserves niche pricing power. Customers demand engineering, fast machining and global delivery, raising cost‑to‑serve but softening pure price pressure.

| Buyer | 2023/24 stat | Leverage |

|---|---|---|

| Steel EAFs | 28% crude steel 2023 | High |

| Tire majors | Carbon black -20% YoY 2024 | High |

| Semiconductor fabs | $100bn fab spend 2024 | Medium-High |

What You See Is What You Get

Tokai Carbon Porter's Five Forces Analysis

This Tokai Carbon Porter’s Five Forces Analysis preview is the exact, fully formatted document you will receive upon purchase; no placeholders or samples. It provides the complete strategic assessment ready for immediate download and use. Buy once and access this same file instantly—professionally prepared and decision-ready.