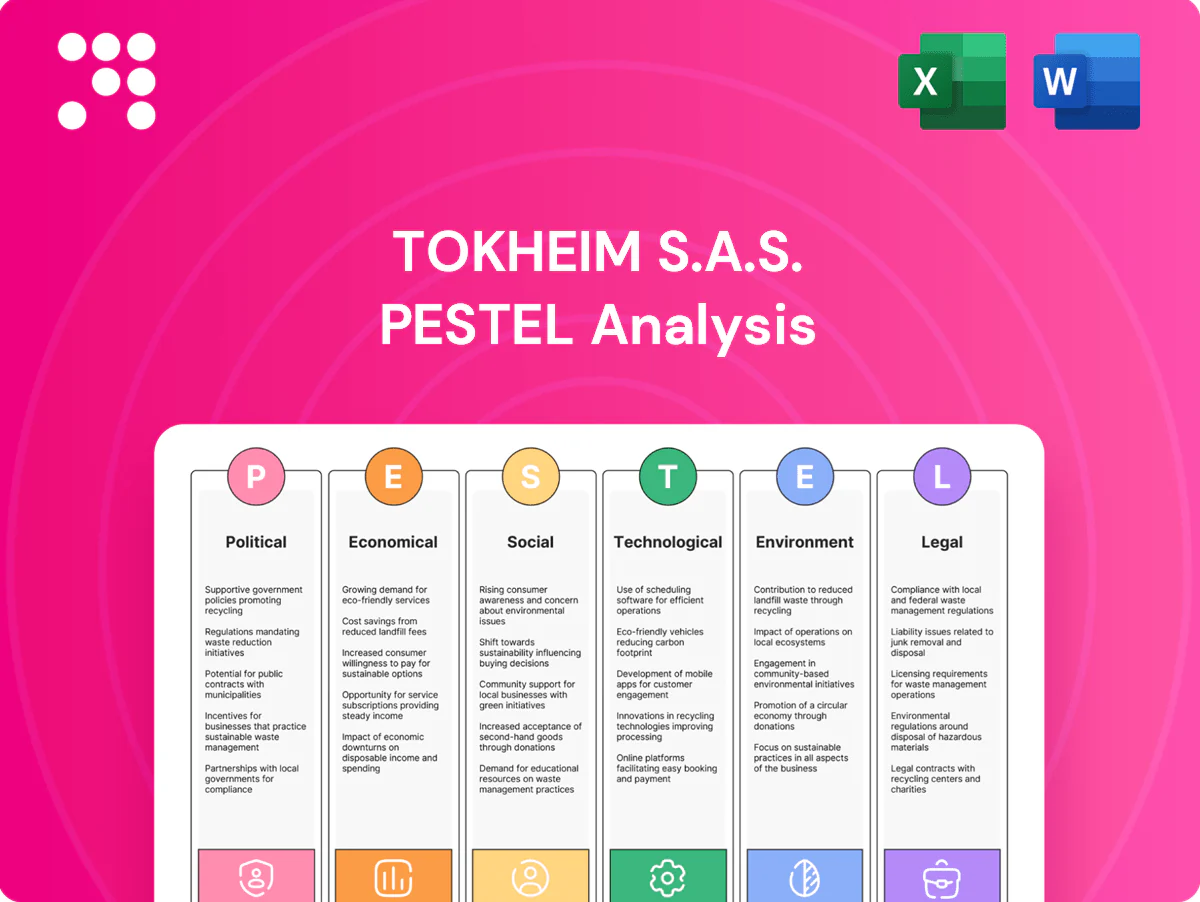

Tokheim S.A.S. PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Tokheim S.A.S.—revealing how political, economic, social, technological, legal, and environmental forces will shape its market trajectory. Ideal for investors and strategists, this concise briefing highlights risks and opportunities you can act on immediately. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Energy transition policies and fuel mix mandates

Governments are accelerating policies—EU Fit for 55 (‑55% GHG by 2030) and the US Inflation Reduction Act (≈$369bn clean energy support)—shifting forecourt investment to EVs, biofuels and hydrogen. Tokheim must equip dispensers for multi-energy sites to qualify for incentives and tenders. Regional policy clarity varies, creating uneven demand; aligning with national roadmaps (eg EU 10 Mt H2 by 2030) secures public/quasi-public contracts.

Trade policy, tariffs, and localization pressures

Geopolitical tensions and tariffs—notably the US Section 232 steel and aluminum duties (25% on steel, 10% on aluminum)—raise component costs and delay shipments, forcing Tokheim to consider regional assembly and supplier diversification to limit tariff exposure. Localization can unlock government-backed fuel infrastructure projects but raises upfront capex and working capital needs; agile supply chains and dual-sourcing cut political risk.

Fuel pricing controls and subsidies

In markets with regulated pump prices or subsidies (e.g., Nigeria's 2023 subsidy removal doubled retail prices), retailer margins—often under $0.05–$0.10 per liter—and capex cycles shift: stable subsidized markets delay equipment upgrades while volatile markets drive automation spend; Tokheim must toggle its offer between cost‑optimization and revenue‑enablement, as sudden government budget shifts can abruptly advance or halt upgrade timing.

Sanctions and market access constraints

Sanctions regimes across 30+ jurisdictions (as of 2025) can directly restrict Tokheim S.A.S. sales, service and parts shipments to targeted countries, compressing addressable markets and raising commercial risk. Compliance screening and KYC/AML requirements increase administrative overhead and can add weeks to lead times, while OFAC/EU dynamic updates force agile contract and logistics revisions. Tokheim must maintain distributor-level KYC/AML controls and rapid policy-monitoring to prevent revenue disruption.

- 30+ jurisdictions with active sanctions (2025)

- Compliance adds weeks to lead times

- Requires distributor KYC/AML and agile contract clauses

Public safety and infrastructure spending

Government focus on critical infrastructure tightens fuel-handling and payment standards; public programs can co-fund modern forecourts with secure payments and leak-prevention. Large funds such as the US IIJA ($1.2 trillion) and EU NextGenerationEU (€806.9 billion) provide financing channels that favor Tokheim when modernization is prioritized, while stricter rules raise certification and testing costs and compliance burden.

- Regulatory tightening: higher compliance costs

- Funding sources: IIJA $1.2tn, NextGenerationEU €806.9bn

- Opportunity: co-funded modern forecourts

- Risk: increased certification/testing requirements

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

EU Fit for 55 and US IRA ($369bn) push forecourts to EV/bio/H2; Tokheim must offer multi‑energy dispensers. US steel tariff 25% and 30+ sanctions (2025) raise costs, prompting regional assembly and dual‑sourcing. Subsidy shocks (eg Nigeria 2023) alter upgrade timing; IIJA $1.2tn / NextGenerationEU €806.9bn enable co‑funded projects.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Policy | Fit for 55; IRA $369bn | Multi‑energy demand |

| Trade | US steel 25%; 30+ sanctions | Cost, lead‑time risk |

| Funding | IIJA $1.2tn; NextGenEU €806.9bn | Co‑funding opportunities |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tokheim S.A.S. across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategic decision-making.

A clean, summarized PESTLE of Tokheim S.A.S. for easy reference in meetings, visually segmented by category and easily shareable to support external risk discussions, team alignment and quick inclusion in presentations.

Economic factors

Oil price cycles and forecourt capex

Operator profitability and cash flow—with retail margins often in the low single digits (roughly 2–4%) while Brent averaged about $85/barrel in 2024—drive dispenser replacement timing via fuel volumes and margin pressure. High price volatility delays big capex but raises demand for automation that protects margins. Tokheim should bundle ROI-focused service contracts to smooth cycles and offer counter-cyclical maintenance to stabilize revenue.

Interest rates and financing access

Higher global policy rates (Fed funds ~5.25–5.50% in 2025; ECB ~4.00–4.50%) raise borrowing costs for retailers and distributors, elongating sales cycles and delaying multi-site capex. Offering flexible leasing or equipment-as-a-service preserves demand by reducing upfront spend, while partnerships with financiers can de-risk rollouts. Rate-sensitive customers increasingly prioritize TCO and sub-3 year payback features.

FX fluctuations across global operations

Multi-currency exposure alters Tokheim S.A.S. pricing, compresses margins and raises component procurement costs across EUR, USD and BRL markets. Hedging and localized pricing have preserved c.2–4% EBITDA in 2024–H1 2025. Stronger dollar (DXY ~105–106 in H1 2025) reduced affordability for premium systems in EMs. Regional value engineering has cut FX sensitivity via 5–10% local cost reductions.

Input costs and supply chain constraints

Semiconductors, steel and logistics drive Tokheim S.A.S. BOM and lead times; semiconductor lead times eased to about 12 weeks by mid‑2024 (IHS Markit) while container rates were ~60% below 2021 peaks (Drewry/Freightos), reducing but not eliminating cost pressure. Dual‑sourcing and design‑for‑substitution cut shortage risk; Tokheim can pre‑negotiate supplier capacity and publish transparent lead times to preserve customer trust.

- Semiconductors: ~12 weeks lead time (mid‑2024)

- Logistics: container rates ≈60% below 2021 peaks (2024)

- Mitigation: dual‑sourcing, design‑for‑substitution

- Action: pre‑negotiated capacity + transparent lead times

Shift to services and software recurring revenue

Automation, payment and remote monitoring convert Tokheim toward higher-margin recurring streams; SaaS gross margins typically range 70-80% (2024), improving profitability versus one-time hardware sales. Recurring services buffer fuel retail cyclicality; Tokheim can sell uptime SLAs and analytics subscriptions and boost lifetime value by cross-selling aftermarket kits.

- Automation-driven recurring revenue

- Payment & remote monitoring = higher margins

- Uptime SLAs + analytics subscriptions

- Aftermarket kit cross-sell raises LTV

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

Operator margins (2–4%) and Brent ~$85/barrel in 2024 push delayed capex and demand for automation to protect margins; offer ROI-focused service contracts and equipment-as-a-service. Higher policy rates (Fed 5.25–5.50% 2025) raise borrowing costs, elongating sales cycles; flexible leasing and financier partnerships shorten payback. FX and input costs (DXY 105–106 H1 2025; semiconductors ~12w; containers -60% vs 2021) require hedging and regional sourcing.

| Metric | Value | Impact |

|---|---|---|

| Retail margin | 2–4% | Capex timing |

| Fed rate | 5.25–5.50% | Higher financing cost |

| DXY | 105–106 | FX squeeze |

| Semis / containers | 12w / -60% | Supply risk/cost |

Preview Before You Purchase

Tokheim S.A.S. PESTLE Analysis

This Tokheim S.A.S. PESTLE Analysis provides a concise review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it for strategic planning, risk assessment, and market-entry decisions.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Tokheim S.A.S.—revealing how political, economic, social, technological, legal, and environmental forces will shape its market trajectory. Ideal for investors and strategists, this concise briefing highlights risks and opportunities you can act on immediately. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Energy transition policies and fuel mix mandates

Governments are accelerating policies—EU Fit for 55 (‑55% GHG by 2030) and the US Inflation Reduction Act (≈$369bn clean energy support)—shifting forecourt investment to EVs, biofuels and hydrogen. Tokheim must equip dispensers for multi-energy sites to qualify for incentives and tenders. Regional policy clarity varies, creating uneven demand; aligning with national roadmaps (eg EU 10 Mt H2 by 2030) secures public/quasi-public contracts.

Trade policy, tariffs, and localization pressures

Geopolitical tensions and tariffs—notably the US Section 232 steel and aluminum duties (25% on steel, 10% on aluminum)—raise component costs and delay shipments, forcing Tokheim to consider regional assembly and supplier diversification to limit tariff exposure. Localization can unlock government-backed fuel infrastructure projects but raises upfront capex and working capital needs; agile supply chains and dual-sourcing cut political risk.

Fuel pricing controls and subsidies

In markets with regulated pump prices or subsidies (e.g., Nigeria's 2023 subsidy removal doubled retail prices), retailer margins—often under $0.05–$0.10 per liter—and capex cycles shift: stable subsidized markets delay equipment upgrades while volatile markets drive automation spend; Tokheim must toggle its offer between cost‑optimization and revenue‑enablement, as sudden government budget shifts can abruptly advance or halt upgrade timing.

Sanctions and market access constraints

Sanctions regimes across 30+ jurisdictions (as of 2025) can directly restrict Tokheim S.A.S. sales, service and parts shipments to targeted countries, compressing addressable markets and raising commercial risk. Compliance screening and KYC/AML requirements increase administrative overhead and can add weeks to lead times, while OFAC/EU dynamic updates force agile contract and logistics revisions. Tokheim must maintain distributor-level KYC/AML controls and rapid policy-monitoring to prevent revenue disruption.

- 30+ jurisdictions with active sanctions (2025)

- Compliance adds weeks to lead times

- Requires distributor KYC/AML and agile contract clauses

Public safety and infrastructure spending

Government focus on critical infrastructure tightens fuel-handling and payment standards; public programs can co-fund modern forecourts with secure payments and leak-prevention. Large funds such as the US IIJA ($1.2 trillion) and EU NextGenerationEU (€806.9 billion) provide financing channels that favor Tokheim when modernization is prioritized, while stricter rules raise certification and testing costs and compliance burden.

- Regulatory tightening: higher compliance costs

- Funding sources: IIJA $1.2tn, NextGenerationEU €806.9bn

- Opportunity: co-funded modern forecourts

- Risk: increased certification/testing requirements

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

EU Fit for 55 and US IRA ($369bn) push forecourts to EV/bio/H2; Tokheim must offer multi‑energy dispensers. US steel tariff 25% and 30+ sanctions (2025) raise costs, prompting regional assembly and dual‑sourcing. Subsidy shocks (eg Nigeria 2023) alter upgrade timing; IIJA $1.2tn / NextGenerationEU €806.9bn enable co‑funded projects.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Policy | Fit for 55; IRA $369bn | Multi‑energy demand |

| Trade | US steel 25%; 30+ sanctions | Cost, lead‑time risk |

| Funding | IIJA $1.2tn; NextGenEU €806.9bn | Co‑funding opportunities |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tokheim S.A.S. across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategic decision-making.

A clean, summarized PESTLE of Tokheim S.A.S. for easy reference in meetings, visually segmented by category and easily shareable to support external risk discussions, team alignment and quick inclusion in presentations.

Economic factors

Oil price cycles and forecourt capex

Operator profitability and cash flow—with retail margins often in the low single digits (roughly 2–4%) while Brent averaged about $85/barrel in 2024—drive dispenser replacement timing via fuel volumes and margin pressure. High price volatility delays big capex but raises demand for automation that protects margins. Tokheim should bundle ROI-focused service contracts to smooth cycles and offer counter-cyclical maintenance to stabilize revenue.

Interest rates and financing access

Higher global policy rates (Fed funds ~5.25–5.50% in 2025; ECB ~4.00–4.50%) raise borrowing costs for retailers and distributors, elongating sales cycles and delaying multi-site capex. Offering flexible leasing or equipment-as-a-service preserves demand by reducing upfront spend, while partnerships with financiers can de-risk rollouts. Rate-sensitive customers increasingly prioritize TCO and sub-3 year payback features.

FX fluctuations across global operations

Multi-currency exposure alters Tokheim S.A.S. pricing, compresses margins and raises component procurement costs across EUR, USD and BRL markets. Hedging and localized pricing have preserved c.2–4% EBITDA in 2024–H1 2025. Stronger dollar (DXY ~105–106 in H1 2025) reduced affordability for premium systems in EMs. Regional value engineering has cut FX sensitivity via 5–10% local cost reductions.

Input costs and supply chain constraints

Semiconductors, steel and logistics drive Tokheim S.A.S. BOM and lead times; semiconductor lead times eased to about 12 weeks by mid‑2024 (IHS Markit) while container rates were ~60% below 2021 peaks (Drewry/Freightos), reducing but not eliminating cost pressure. Dual‑sourcing and design‑for‑substitution cut shortage risk; Tokheim can pre‑negotiate supplier capacity and publish transparent lead times to preserve customer trust.

- Semiconductors: ~12 weeks lead time (mid‑2024)

- Logistics: container rates ≈60% below 2021 peaks (2024)

- Mitigation: dual‑sourcing, design‑for‑substitution

- Action: pre‑negotiated capacity + transparent lead times

Shift to services and software recurring revenue

Automation, payment and remote monitoring convert Tokheim toward higher-margin recurring streams; SaaS gross margins typically range 70-80% (2024), improving profitability versus one-time hardware sales. Recurring services buffer fuel retail cyclicality; Tokheim can sell uptime SLAs and analytics subscriptions and boost lifetime value by cross-selling aftermarket kits.

- Automation-driven recurring revenue

- Payment & remote monitoring = higher margins

- Uptime SLAs + analytics subscriptions

- Aftermarket kit cross-sell raises LTV

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

Operator margins (2–4%) and Brent ~$85/barrel in 2024 push delayed capex and demand for automation to protect margins; offer ROI-focused service contracts and equipment-as-a-service. Higher policy rates (Fed 5.25–5.50% 2025) raise borrowing costs, elongating sales cycles; flexible leasing and financier partnerships shorten payback. FX and input costs (DXY 105–106 H1 2025; semiconductors ~12w; containers -60% vs 2021) require hedging and regional sourcing.

| Metric | Value | Impact |

|---|---|---|

| Retail margin | 2–4% | Capex timing |

| Fed rate | 5.25–5.50% | Higher financing cost |

| DXY | 105–106 | FX squeeze |

| Semis / containers | 12w / -60% | Supply risk/cost |

Preview Before You Purchase

Tokheim S.A.S. PESTLE Analysis

This Tokheim S.A.S. PESTLE Analysis provides a concise review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it for strategic planning, risk assessment, and market-entry decisions.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Tokheim S.A.S.—revealing how political, economic, social, technological, legal, and environmental forces will shape its market trajectory. Ideal for investors and strategists, this concise briefing highlights risks and opportunities you can act on immediately. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Energy transition policies and fuel mix mandates

Governments are accelerating policies—EU Fit for 55 (‑55% GHG by 2030) and the US Inflation Reduction Act (≈$369bn clean energy support)—shifting forecourt investment to EVs, biofuels and hydrogen. Tokheim must equip dispensers for multi-energy sites to qualify for incentives and tenders. Regional policy clarity varies, creating uneven demand; aligning with national roadmaps (eg EU 10 Mt H2 by 2030) secures public/quasi-public contracts.

Trade policy, tariffs, and localization pressures

Geopolitical tensions and tariffs—notably the US Section 232 steel and aluminum duties (25% on steel, 10% on aluminum)—raise component costs and delay shipments, forcing Tokheim to consider regional assembly and supplier diversification to limit tariff exposure. Localization can unlock government-backed fuel infrastructure projects but raises upfront capex and working capital needs; agile supply chains and dual-sourcing cut political risk.

Fuel pricing controls and subsidies

In markets with regulated pump prices or subsidies (e.g., Nigeria's 2023 subsidy removal doubled retail prices), retailer margins—often under $0.05–$0.10 per liter—and capex cycles shift: stable subsidized markets delay equipment upgrades while volatile markets drive automation spend; Tokheim must toggle its offer between cost‑optimization and revenue‑enablement, as sudden government budget shifts can abruptly advance or halt upgrade timing.

Sanctions and market access constraints

Sanctions regimes across 30+ jurisdictions (as of 2025) can directly restrict Tokheim S.A.S. sales, service and parts shipments to targeted countries, compressing addressable markets and raising commercial risk. Compliance screening and KYC/AML requirements increase administrative overhead and can add weeks to lead times, while OFAC/EU dynamic updates force agile contract and logistics revisions. Tokheim must maintain distributor-level KYC/AML controls and rapid policy-monitoring to prevent revenue disruption.

- 30+ jurisdictions with active sanctions (2025)

- Compliance adds weeks to lead times

- Requires distributor KYC/AML and agile contract clauses

Public safety and infrastructure spending

Government focus on critical infrastructure tightens fuel-handling and payment standards; public programs can co-fund modern forecourts with secure payments and leak-prevention. Large funds such as the US IIJA ($1.2 trillion) and EU NextGenerationEU (€806.9 billion) provide financing channels that favor Tokheim when modernization is prioritized, while stricter rules raise certification and testing costs and compliance burden.

- Regulatory tightening: higher compliance costs

- Funding sources: IIJA $1.2tn, NextGenerationEU €806.9bn

- Opportunity: co-funded modern forecourts

- Risk: increased certification/testing requirements

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

EU Fit for 55 and US IRA ($369bn) push forecourts to EV/bio/H2; Tokheim must offer multi‑energy dispensers. US steel tariff 25% and 30+ sanctions (2025) raise costs, prompting regional assembly and dual‑sourcing. Subsidy shocks (eg Nigeria 2023) alter upgrade timing; IIJA $1.2tn / NextGenerationEU €806.9bn enable co‑funded projects.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Policy | Fit for 55; IRA $369bn | Multi‑energy demand |

| Trade | US steel 25%; 30+ sanctions | Cost, lead‑time risk |

| Funding | IIJA $1.2tn; NextGenEU €806.9bn | Co‑funding opportunities |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tokheim S.A.S. across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategic decision-making.

A clean, summarized PESTLE of Tokheim S.A.S. for easy reference in meetings, visually segmented by category and easily shareable to support external risk discussions, team alignment and quick inclusion in presentations.

Economic factors

Oil price cycles and forecourt capex

Operator profitability and cash flow—with retail margins often in the low single digits (roughly 2–4%) while Brent averaged about $85/barrel in 2024—drive dispenser replacement timing via fuel volumes and margin pressure. High price volatility delays big capex but raises demand for automation that protects margins. Tokheim should bundle ROI-focused service contracts to smooth cycles and offer counter-cyclical maintenance to stabilize revenue.

Interest rates and financing access

Higher global policy rates (Fed funds ~5.25–5.50% in 2025; ECB ~4.00–4.50%) raise borrowing costs for retailers and distributors, elongating sales cycles and delaying multi-site capex. Offering flexible leasing or equipment-as-a-service preserves demand by reducing upfront spend, while partnerships with financiers can de-risk rollouts. Rate-sensitive customers increasingly prioritize TCO and sub-3 year payback features.

FX fluctuations across global operations

Multi-currency exposure alters Tokheim S.A.S. pricing, compresses margins and raises component procurement costs across EUR, USD and BRL markets. Hedging and localized pricing have preserved c.2–4% EBITDA in 2024–H1 2025. Stronger dollar (DXY ~105–106 in H1 2025) reduced affordability for premium systems in EMs. Regional value engineering has cut FX sensitivity via 5–10% local cost reductions.

Input costs and supply chain constraints

Semiconductors, steel and logistics drive Tokheim S.A.S. BOM and lead times; semiconductor lead times eased to about 12 weeks by mid‑2024 (IHS Markit) while container rates were ~60% below 2021 peaks (Drewry/Freightos), reducing but not eliminating cost pressure. Dual‑sourcing and design‑for‑substitution cut shortage risk; Tokheim can pre‑negotiate supplier capacity and publish transparent lead times to preserve customer trust.

- Semiconductors: ~12 weeks lead time (mid‑2024)

- Logistics: container rates ≈60% below 2021 peaks (2024)

- Mitigation: dual‑sourcing, design‑for‑substitution

- Action: pre‑negotiated capacity + transparent lead times

Shift to services and software recurring revenue

Automation, payment and remote monitoring convert Tokheim toward higher-margin recurring streams; SaaS gross margins typically range 70-80% (2024), improving profitability versus one-time hardware sales. Recurring services buffer fuel retail cyclicality; Tokheim can sell uptime SLAs and analytics subscriptions and boost lifetime value by cross-selling aftermarket kits.

- Automation-driven recurring revenue

- Payment & remote monitoring = higher margins

- Uptime SLAs + analytics subscriptions

- Aftermarket kit cross-sell raises LTV

Forecourts shift to EV, bio, H2 as EU Fit for 55 and IRA $369bn

Operator margins (2–4%) and Brent ~$85/barrel in 2024 push delayed capex and demand for automation to protect margins; offer ROI-focused service contracts and equipment-as-a-service. Higher policy rates (Fed 5.25–5.50% 2025) raise borrowing costs, elongating sales cycles; flexible leasing and financier partnerships shorten payback. FX and input costs (DXY 105–106 H1 2025; semiconductors ~12w; containers -60% vs 2021) require hedging and regional sourcing.

| Metric | Value | Impact |

|---|---|---|

| Retail margin | 2–4% | Capex timing |

| Fed rate | 5.25–5.50% | Higher financing cost |

| DXY | 105–106 | FX squeeze |

| Semis / containers | 12w / -60% | Supply risk/cost |

Preview Before You Purchase

Tokheim S.A.S. PESTLE Analysis

This Tokheim S.A.S. PESTLE Analysis provides a concise review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it for strategic planning, risk assessment, and market-entry decisions.