TomTom SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

TomTom combines strong mapping IP and automotive partnerships with growing location‑based services, yet faces fierce competition from big tech and margin pressure from hardware decline. Our full SWOT uncovers strategic gaps, monetization levers, and risk scenarios to inform investment or partnership decisions. Purchase the complete report—Word + Excel—for actionable, editable insights.

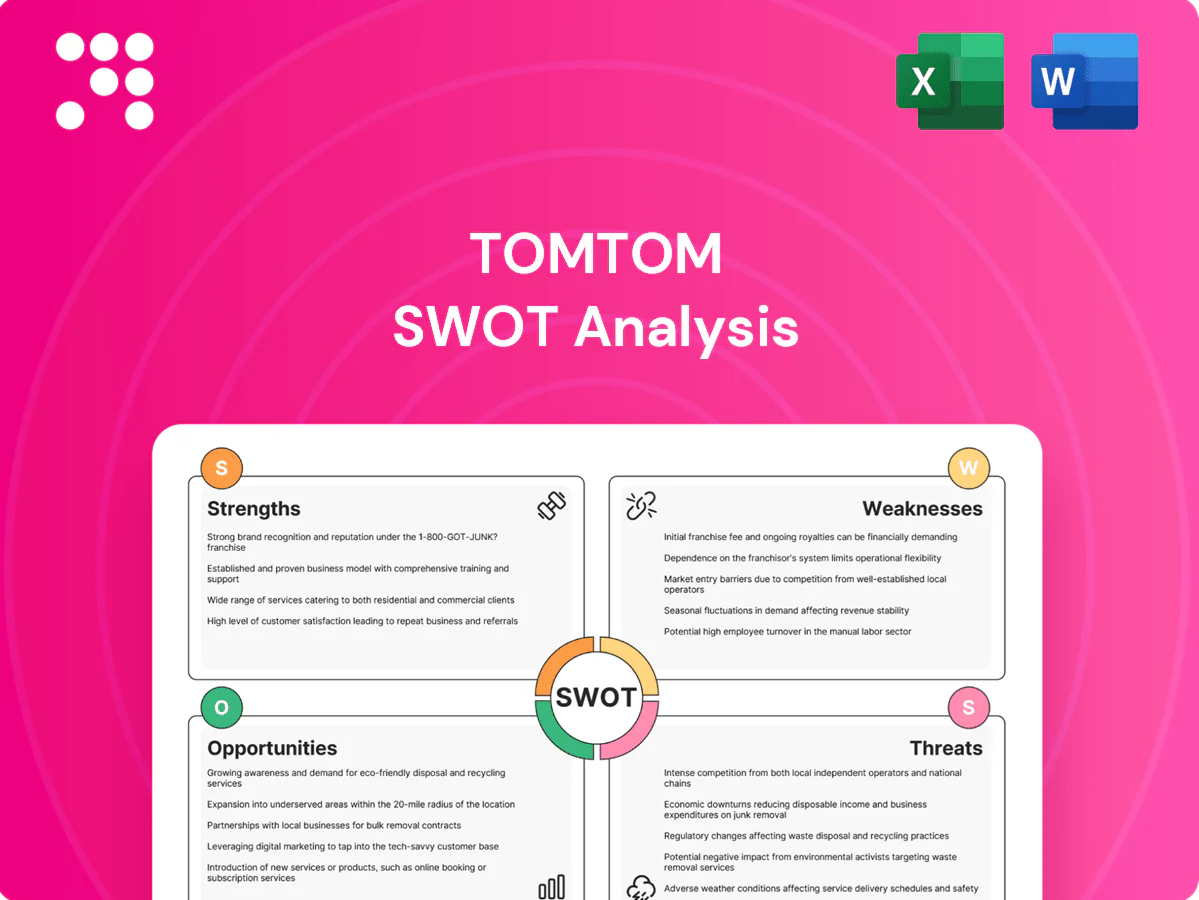

Strengths

Independent maps

TomTom’s independent, high-precision maps—not tied to an ad ecosystem—position the company as a neutral partner for automakers and enterprises, strengthening trust and long-term contracts. Independence supports strict data governance and GDPR-aligned privacy practices, reducing regulatory friction for customers. It also minimizes conflicts of interest with clients’ brands and UX, enabling white-label integrations and OEM relationships.

Automotive ties

TomTom’s software is embedded across in-vehicle infotainment and ADAS stacks, giving it access to millions of vehicles and enabling recurring, long-cycle OEM contracts that drive sticky revenue; automotive contracts represented the majority of TomTom’s sales in recent years. OEM integrations supply at-scale map and traffic data, improving product accuracy and raising switching costs while amplifying TomTom’s influence over OEM roadmaps.

Real-time traffic

TomTom’s real-time traffic and incident data are widely regarded as accurate and timely, with high-quality probe data improving ETA reliability and routing. This leads to measurable reductions in delay and faster route adjustments that enhance driver safety and efficiency. The service is a clear differentiator for consumer navigation and fleet operations, supporting better on-time performance and lower operating costs.

ADAS/HD capability

TomTom provides advanced HD mapping and lane-level content that powers ADAS features such as lane guidance and predictive cruise, forming a foundation for SAE L2+ to L4 automation. The datasets are continuously updated and integrated with OEM stacks, aligning with regulatory safety roadmaps and OEM feature plans.

- HD maps: lane-level precision

- Use cases: lane guidance, predictive cruise

- Automation: foundational for higher SAE levels

- Alignment: OEM and regulatory roadmaps

Platform/API suite

TomTom provides APIs and SDKs for maps, search, routing and real-time traffic, letting developers and enterprises embed location services without building mapping stacks in-house, accelerating time-to-market across logistics, mobility and geospatial analytics.

- Fast integration: reduces build time for mapping

- Cross-industry use: logistics, mobility, analytics

- Monetization: platform fuels scalable subscription-like revenue

High-precision, privacy-first maps powering OEMs, ADAS and logistics integration

TomTom’s independent, high-precision maps and GDPR-aligned privacy make it a trusted neutral partner for OEMs and enterprises, supporting long-term contracts and white-label integrations. Its embedded software reaches millions of vehicles, driving recurring OEM revenue and high switching costs. Market-leading real-time traffic, HD lane-level maps and developer APIs enable ADAS/automation and fast integration across logistics and mobility.

| Metric | Position |

|---|---|

| Installed vehicles | millions (OEM reach) |

What is included in the product

Provides a strategic overview of TomTom’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise TomTom SWOT matrix for fast, visual strategy alignment, highlighting core strengths in mapping tech and revenue streams while flagging competitive and regulatory risks for quick decision-making.

Weaknesses

Scale vs big tech

TomTom competes with hyperscalers that dominate cloud infrastructure — AWS, Microsoft Azure and Google Cloud together held roughly 70% of the global cloud IaaS/PaaS market in 2024, giving them vast data and compute scale advantages. That scale supports broader marketing reach and developer mindshare, areas where TomTom lags, limiting platform adoption. Intense price competition from these players can compress TomTom’s margins, and constrained resources slow feature parity in some advanced mapping and AI-driven services.

Auto cycle exposure

Revenue concentrated in Automotive ties TomTom to vehicle production cycles, so OEM model launch timing drives pronounced quarter-to-quarter swings. Delays or cancellations of OEM programs shift or erase expected revenue recognition, creating multi-million-euro gaps for specific years. Managing forecasts across multi-year pipelines becomes materially more complex and raises working-capital and cash-flow volatility.

Consumer hardware fade

Legacy PND and consumer device segments continue to decline, shrinking TomTom’s hardware revenue base and reducing recurring income stability. The shift to software and services risks diluting near-term top-line results as licensing and subscription ramp-up lags. Channel restructuring to support B2B sales adds one-off and ongoing costs. Strong consumer-device brand recognition can overshadow and slow adoption of TomTom’s software advances.

High data upkeep

Maintaining fresh, global maps is capital- and data-intensive for TomTom; the company reported group revenue of €389m in 2024, while location-data and map upkeep drive steady fixed costs for continuous ingestion, validation and QA. Coverage gaps in long-tail geographies remain hard to close profitably and require ongoing local investment. Map schema changes force coordinated customer updates, raising integration friction and churn risk.

- €389m 2024 group revenue

- Continuous QA/validation raises fixed OPEX

- Profitability challenge in long-tail geographies

- Schema changes require coordinated customer rollouts

Partner dependence

TomTom's heavy reliance on OEMs, fleets and data partners creates concentration risk, making revenue vulnerable to a small set of large contracts and pricing pressure at renewals; shifts in partner strategies can curtail access to critical mapping and traffic data, while tight integration requirements slow product iteration and innovation cadence.

- Concentration risk: dependence on few large partners

- Pricing pressure at contract renewals

- Risk of reduced data access from partner strategy changes

- Integration dependencies slow innovation

Hyperscaler scale gap (~70%) tightens margins; €389m OPEX

TomTom faces a scale gap to hyperscalers (AWS/Azure/GCP ~70% IaaS/PaaS 2024) that limits platform adoption and compresses margins. Automotive revenue concentration drives quarter-to-quarter swings and forecasting volatility. Map upkeep and data-partner dependence create steady fixed OPEX (group revenue €389m in 2024) and raise churn/integration risks.

| Metric | Value |

|---|---|

| Group revenue (2024) | €389m |

| Hyperscaler IaaS/PaaS share (2024) | ~70% |

| Fixed OPEX | High (map QA/validation) |

| Partner concentration | High (OEMs/fleets) |

Full Version Awaits

TomTom SWOT Analysis

This is the actual TomTom SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. It’s structured, actionable, and ready for download after checkout.

Elevate Your Analysis with the Complete SWOT Report

TomTom combines strong mapping IP and automotive partnerships with growing location‑based services, yet faces fierce competition from big tech and margin pressure from hardware decline. Our full SWOT uncovers strategic gaps, monetization levers, and risk scenarios to inform investment or partnership decisions. Purchase the complete report—Word + Excel—for actionable, editable insights.

Strengths

Independent maps

TomTom’s independent, high-precision maps—not tied to an ad ecosystem—position the company as a neutral partner for automakers and enterprises, strengthening trust and long-term contracts. Independence supports strict data governance and GDPR-aligned privacy practices, reducing regulatory friction for customers. It also minimizes conflicts of interest with clients’ brands and UX, enabling white-label integrations and OEM relationships.

Automotive ties

TomTom’s software is embedded across in-vehicle infotainment and ADAS stacks, giving it access to millions of vehicles and enabling recurring, long-cycle OEM contracts that drive sticky revenue; automotive contracts represented the majority of TomTom’s sales in recent years. OEM integrations supply at-scale map and traffic data, improving product accuracy and raising switching costs while amplifying TomTom’s influence over OEM roadmaps.

Real-time traffic

TomTom’s real-time traffic and incident data are widely regarded as accurate and timely, with high-quality probe data improving ETA reliability and routing. This leads to measurable reductions in delay and faster route adjustments that enhance driver safety and efficiency. The service is a clear differentiator for consumer navigation and fleet operations, supporting better on-time performance and lower operating costs.

ADAS/HD capability

TomTom provides advanced HD mapping and lane-level content that powers ADAS features such as lane guidance and predictive cruise, forming a foundation for SAE L2+ to L4 automation. The datasets are continuously updated and integrated with OEM stacks, aligning with regulatory safety roadmaps and OEM feature plans.

- HD maps: lane-level precision

- Use cases: lane guidance, predictive cruise

- Automation: foundational for higher SAE levels

- Alignment: OEM and regulatory roadmaps

Platform/API suite

TomTom provides APIs and SDKs for maps, search, routing and real-time traffic, letting developers and enterprises embed location services without building mapping stacks in-house, accelerating time-to-market across logistics, mobility and geospatial analytics.

- Fast integration: reduces build time for mapping

- Cross-industry use: logistics, mobility, analytics

- Monetization: platform fuels scalable subscription-like revenue

High-precision, privacy-first maps powering OEMs, ADAS and logistics integration

TomTom’s independent, high-precision maps and GDPR-aligned privacy make it a trusted neutral partner for OEMs and enterprises, supporting long-term contracts and white-label integrations. Its embedded software reaches millions of vehicles, driving recurring OEM revenue and high switching costs. Market-leading real-time traffic, HD lane-level maps and developer APIs enable ADAS/automation and fast integration across logistics and mobility.

| Metric | Position |

|---|---|

| Installed vehicles | millions (OEM reach) |

What is included in the product

Provides a strategic overview of TomTom’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise TomTom SWOT matrix for fast, visual strategy alignment, highlighting core strengths in mapping tech and revenue streams while flagging competitive and regulatory risks for quick decision-making.

Weaknesses

Scale vs big tech

TomTom competes with hyperscalers that dominate cloud infrastructure — AWS, Microsoft Azure and Google Cloud together held roughly 70% of the global cloud IaaS/PaaS market in 2024, giving them vast data and compute scale advantages. That scale supports broader marketing reach and developer mindshare, areas where TomTom lags, limiting platform adoption. Intense price competition from these players can compress TomTom’s margins, and constrained resources slow feature parity in some advanced mapping and AI-driven services.

Auto cycle exposure

Revenue concentrated in Automotive ties TomTom to vehicle production cycles, so OEM model launch timing drives pronounced quarter-to-quarter swings. Delays or cancellations of OEM programs shift or erase expected revenue recognition, creating multi-million-euro gaps for specific years. Managing forecasts across multi-year pipelines becomes materially more complex and raises working-capital and cash-flow volatility.

Consumer hardware fade

Legacy PND and consumer device segments continue to decline, shrinking TomTom’s hardware revenue base and reducing recurring income stability. The shift to software and services risks diluting near-term top-line results as licensing and subscription ramp-up lags. Channel restructuring to support B2B sales adds one-off and ongoing costs. Strong consumer-device brand recognition can overshadow and slow adoption of TomTom’s software advances.

High data upkeep

Maintaining fresh, global maps is capital- and data-intensive for TomTom; the company reported group revenue of €389m in 2024, while location-data and map upkeep drive steady fixed costs for continuous ingestion, validation and QA. Coverage gaps in long-tail geographies remain hard to close profitably and require ongoing local investment. Map schema changes force coordinated customer updates, raising integration friction and churn risk.

- €389m 2024 group revenue

- Continuous QA/validation raises fixed OPEX

- Profitability challenge in long-tail geographies

- Schema changes require coordinated customer rollouts

Partner dependence

TomTom's heavy reliance on OEMs, fleets and data partners creates concentration risk, making revenue vulnerable to a small set of large contracts and pricing pressure at renewals; shifts in partner strategies can curtail access to critical mapping and traffic data, while tight integration requirements slow product iteration and innovation cadence.

- Concentration risk: dependence on few large partners

- Pricing pressure at contract renewals

- Risk of reduced data access from partner strategy changes

- Integration dependencies slow innovation

Hyperscaler scale gap (~70%) tightens margins; €389m OPEX

TomTom faces a scale gap to hyperscalers (AWS/Azure/GCP ~70% IaaS/PaaS 2024) that limits platform adoption and compresses margins. Automotive revenue concentration drives quarter-to-quarter swings and forecasting volatility. Map upkeep and data-partner dependence create steady fixed OPEX (group revenue €389m in 2024) and raise churn/integration risks.

| Metric | Value |

|---|---|

| Group revenue (2024) | €389m |

| Hyperscaler IaaS/PaaS share (2024) | ~70% |

| Fixed OPEX | High (map QA/validation) |

| Partner concentration | High (OEMs/fleets) |

Full Version Awaits

TomTom SWOT Analysis

This is the actual TomTom SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. It’s structured, actionable, and ready for download after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

TomTom combines strong mapping IP and automotive partnerships with growing location‑based services, yet faces fierce competition from big tech and margin pressure from hardware decline. Our full SWOT uncovers strategic gaps, monetization levers, and risk scenarios to inform investment or partnership decisions. Purchase the complete report—Word + Excel—for actionable, editable insights.

Strengths

Independent maps

TomTom’s independent, high-precision maps—not tied to an ad ecosystem—position the company as a neutral partner for automakers and enterprises, strengthening trust and long-term contracts. Independence supports strict data governance and GDPR-aligned privacy practices, reducing regulatory friction for customers. It also minimizes conflicts of interest with clients’ brands and UX, enabling white-label integrations and OEM relationships.

Automotive ties

TomTom’s software is embedded across in-vehicle infotainment and ADAS stacks, giving it access to millions of vehicles and enabling recurring, long-cycle OEM contracts that drive sticky revenue; automotive contracts represented the majority of TomTom’s sales in recent years. OEM integrations supply at-scale map and traffic data, improving product accuracy and raising switching costs while amplifying TomTom’s influence over OEM roadmaps.

Real-time traffic

TomTom’s real-time traffic and incident data are widely regarded as accurate and timely, with high-quality probe data improving ETA reliability and routing. This leads to measurable reductions in delay and faster route adjustments that enhance driver safety and efficiency. The service is a clear differentiator for consumer navigation and fleet operations, supporting better on-time performance and lower operating costs.

ADAS/HD capability

TomTom provides advanced HD mapping and lane-level content that powers ADAS features such as lane guidance and predictive cruise, forming a foundation for SAE L2+ to L4 automation. The datasets are continuously updated and integrated with OEM stacks, aligning with regulatory safety roadmaps and OEM feature plans.

- HD maps: lane-level precision

- Use cases: lane guidance, predictive cruise

- Automation: foundational for higher SAE levels

- Alignment: OEM and regulatory roadmaps

Platform/API suite

TomTom provides APIs and SDKs for maps, search, routing and real-time traffic, letting developers and enterprises embed location services without building mapping stacks in-house, accelerating time-to-market across logistics, mobility and geospatial analytics.

- Fast integration: reduces build time for mapping

- Cross-industry use: logistics, mobility, analytics

- Monetization: platform fuels scalable subscription-like revenue

High-precision, privacy-first maps powering OEMs, ADAS and logistics integration

TomTom’s independent, high-precision maps and GDPR-aligned privacy make it a trusted neutral partner for OEMs and enterprises, supporting long-term contracts and white-label integrations. Its embedded software reaches millions of vehicles, driving recurring OEM revenue and high switching costs. Market-leading real-time traffic, HD lane-level maps and developer APIs enable ADAS/automation and fast integration across logistics and mobility.

| Metric | Position |

|---|---|

| Installed vehicles | millions (OEM reach) |

What is included in the product

Provides a strategic overview of TomTom’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise TomTom SWOT matrix for fast, visual strategy alignment, highlighting core strengths in mapping tech and revenue streams while flagging competitive and regulatory risks for quick decision-making.

Weaknesses

Scale vs big tech

TomTom competes with hyperscalers that dominate cloud infrastructure — AWS, Microsoft Azure and Google Cloud together held roughly 70% of the global cloud IaaS/PaaS market in 2024, giving them vast data and compute scale advantages. That scale supports broader marketing reach and developer mindshare, areas where TomTom lags, limiting platform adoption. Intense price competition from these players can compress TomTom’s margins, and constrained resources slow feature parity in some advanced mapping and AI-driven services.

Auto cycle exposure

Revenue concentrated in Automotive ties TomTom to vehicle production cycles, so OEM model launch timing drives pronounced quarter-to-quarter swings. Delays or cancellations of OEM programs shift or erase expected revenue recognition, creating multi-million-euro gaps for specific years. Managing forecasts across multi-year pipelines becomes materially more complex and raises working-capital and cash-flow volatility.

Consumer hardware fade

Legacy PND and consumer device segments continue to decline, shrinking TomTom’s hardware revenue base and reducing recurring income stability. The shift to software and services risks diluting near-term top-line results as licensing and subscription ramp-up lags. Channel restructuring to support B2B sales adds one-off and ongoing costs. Strong consumer-device brand recognition can overshadow and slow adoption of TomTom’s software advances.

High data upkeep

Maintaining fresh, global maps is capital- and data-intensive for TomTom; the company reported group revenue of €389m in 2024, while location-data and map upkeep drive steady fixed costs for continuous ingestion, validation and QA. Coverage gaps in long-tail geographies remain hard to close profitably and require ongoing local investment. Map schema changes force coordinated customer updates, raising integration friction and churn risk.

- €389m 2024 group revenue

- Continuous QA/validation raises fixed OPEX

- Profitability challenge in long-tail geographies

- Schema changes require coordinated customer rollouts

Partner dependence

TomTom's heavy reliance on OEMs, fleets and data partners creates concentration risk, making revenue vulnerable to a small set of large contracts and pricing pressure at renewals; shifts in partner strategies can curtail access to critical mapping and traffic data, while tight integration requirements slow product iteration and innovation cadence.

- Concentration risk: dependence on few large partners

- Pricing pressure at contract renewals

- Risk of reduced data access from partner strategy changes

- Integration dependencies slow innovation

Hyperscaler scale gap (~70%) tightens margins; €389m OPEX

TomTom faces a scale gap to hyperscalers (AWS/Azure/GCP ~70% IaaS/PaaS 2024) that limits platform adoption and compresses margins. Automotive revenue concentration drives quarter-to-quarter swings and forecasting volatility. Map upkeep and data-partner dependence create steady fixed OPEX (group revenue €389m in 2024) and raise churn/integration risks.

| Metric | Value |

|---|---|

| Group revenue (2024) | €389m |

| Hyperscaler IaaS/PaaS share (2024) | ~70% |

| Fixed OPEX | High (map QA/validation) |

| Partner concentration | High (OEMs/fleets) |

Full Version Awaits

TomTom SWOT Analysis

This is the actual TomTom SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. It’s structured, actionable, and ready for download after checkout.