T.O.M. Vehicle Rental PESTLE Analysis

Skip the Research. Get the Strategy.

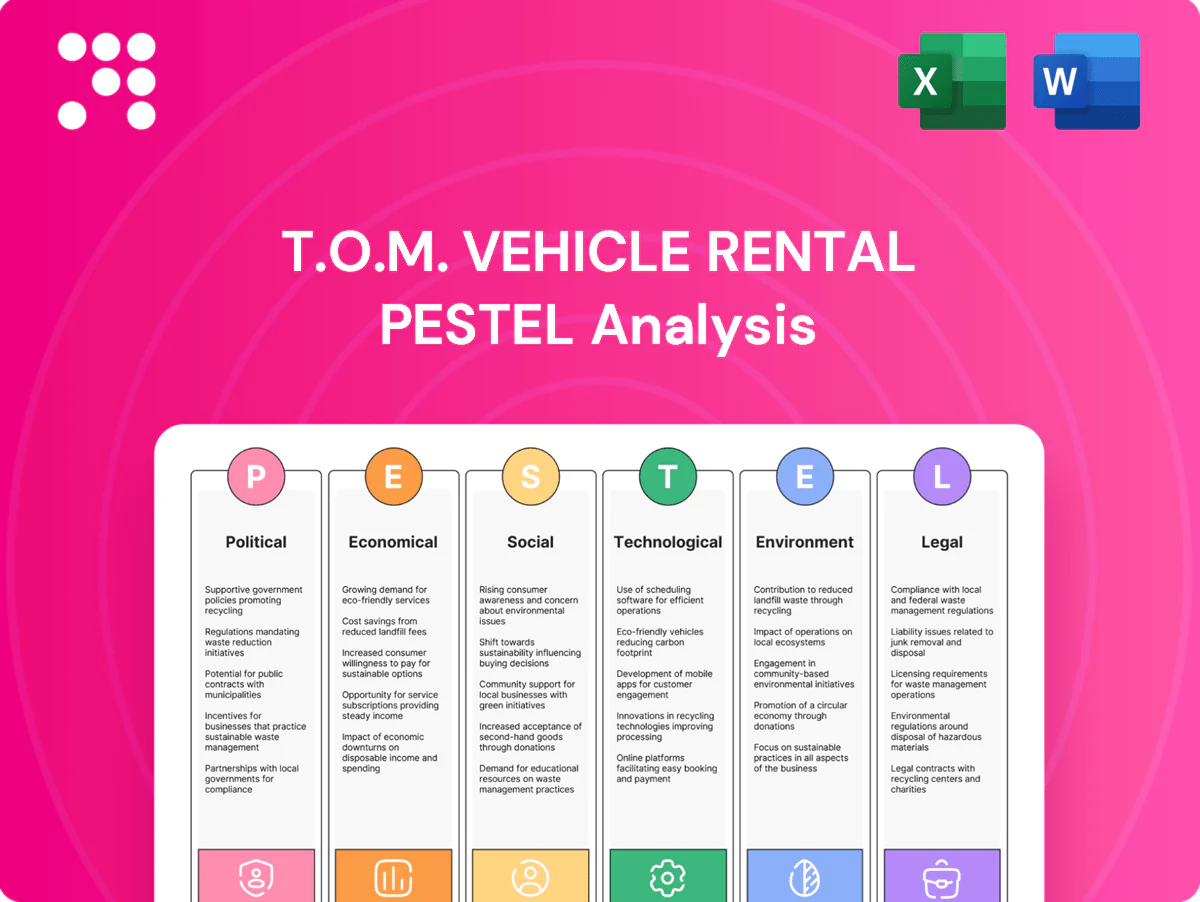

Gain strategic clarity with our PESTLE Analysis of T.O.M. Vehicle Rental—uncover political, economic, social, technological, legal and environmental factors shaping its future. Actionable insights highlight risks and growth levers. Ideal for investors and strategists. Purchase the full report to get the complete, downloadable analysis now.

Political factors

UK transport policy shifts

Changes to UK transport priorities can reshape demand for commercial rental and contract hire; the government’s ban on new petrol and diesel cars and vans from 2030 (with non-zero-emission hybrids to 2035) accelerates electrification. Over 40 local authorities have introduced or proposed clean-air mandates and low-emission zones, shifting fleet needs toward EVs and ULEVs. T.O.M. should align inventory to policy trends, anticipate regional variation, and actively engage policymakers and trade bodies to surface early signals.

Public sector procurement cycles

Government tenders for vans and specialist vehicles drive utilization and pricing, with public procurement accounting for roughly 12–14% of GDP in OECD/EU economies (2023–24), concentrating significant fleet spend into cyclical tenders. Budget timelines, periodic spending reviews and election cycles create lumpiness in demand. T.O.M. can offer 3–5 year terms and flexible options to align with public-sector frameworks. Achieving preferred supplier status can stabilize volumes across cycles.

Infrastructure and regional levelling-up

Investment in roads and logistics through the UK Levelling Up Fund (total £4.8bn) and major projects drives localized fleet needs, raising demand for HGVs and specialist units in growth corridors. Regional funding disparities create rental hotspots in funded areas, so T.O.M. should site depots close to corridor projects to cut lead times. Flexible cross-depot transfers will smooth short-term imbalances and optimize utilization.

Devolution and local regulations

- Policy variability: regional access rules, congestion and CAZ fees

- Operational impact: harder national fleet allocation and route planning

- Service offering: compliance guidance bundled with rentals

- Pricing: dynamic, location-aware fees to reflect local charges

Trade and import dynamics

Tariffs, customs frictions and rules-of-origin are adding 5–12% to landed vehicle and parts costs and have pushed lead times for new units to roughly 20–30 weeks in 2024, with EU–UK checks and global logistics shifts the main drivers. T.O.M. should diversify OEM relationships, stock critical spares and use forward contracts to hedge component price volatility and FX risk.

- Tariff impact: +5–12% landed cost

- Lead times: ~20–30 weeks (2024)

- Mitigation: diversify OEMs, hold spares

- Hedge: forward contracts for parts/FX

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

Political shifts—2030 petrol/diesel ban, 2035 hybrids, and expanded clean-air zones (ULEZ ~8.6m residents) drive urgent EV conversion and regional compliance costs. Public procurement remains a major, lumpy demand source (public spend ~12–14% GDP), so securing preferred-supplier status smooths volumes. Tariffs and customs add ~5–12% to landed costs and pushed lead times to ~20–30 weeks; diversify suppliers and hold spares to mitigate.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| Clean-air rules | ULEZ ~8.6m | Fleet electrification | Shift EV inventory |

| Public procurement | 12–14% GDP | Lumpy demand | 3–5yr contracts |

| Tariffs/lead times | +5–12% / 20–30w | Cost, availability | Diversify, hedge |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect T.O.M. Vehicle Rental, with data-driven trends and region-specific examples that surface risks and growth opportunities. Designed for executives and investors, it delivers forward-looking insights for strategy, funding and scenario planning.

A condensed, visually segmented PESTLE summary for T.O.M. Vehicle Rental that highlights external risks and market drivers for quick inclusion in presentations or planning sessions; editable notes and a shareable format streamline cross-team alignment and consultant reporting.

Economic factors

UK growth and SME health

SMEs—99.9% of UK businesses, supplying 61.3% of private-sector jobs and 51.6% of turnover (UK Business Population Estimates 2023)—drive van rental demand across trades, delivery and services. GDP volatility in 2023–24 from ONS maps into fleet utilization swings; T.O.M. can scale flexible terms to capture upside and limit downside. Tiered pricing and pause options increase retention in downturns.

Interest rates and financing costs

Contract hire economics are highly sensitive to base rates and credit spreads; US Fed funds at 5.25–5.50% (mid‑2025) and investment‑grade spreads around 120–140 bps materially raise cost of capital and lease pricing. Higher rates push monthly rents up and compress margins unless pricing is adjusted. T.O.M. can optimize tenors, residual assumptions and refinancing windows to lower funding costs. Offering fixed‑rate packages de‑risks client budgets and improves dealability.

Fuel and energy price volatility

Diesel retail averaged about $3.80/gal in the US in 2024 while commercial electricity ran near 15.5¢/kWh, so swings in these prices can shift TCO materially for ICE versus EV fleets and change payback timelines. Customers may alter vehicle mix or lease term in response to operating-cost changes. T.O.M. can offer transparent TCO calculators and fuel-hedging options; mixed fleets provide resilience during price shocks.

Residual value cycles

Residual value cycles drive lease rates and profitability as used commercial vehicle prices directly set end-of-lease RVs; recent remarketing data show certified pre-owned premiums of 5-15% and double-digit RV volatility in 2023–24, so supply constraints can lift RVs while oversupply crushes margins. T.O.M. needs robust RV forecasting, dynamic disposal channels and certified used programs to maximize proceeds.

- RV sensitivity to used prices

- Supply constraints vs oversupply

- Forecasting accuracy target >90%

- Certified used premium 5-15%

Labour market and wage pressure

Technician shortages and driver scarcity drive higher operating costs and downtime; ManpowerGroup 2024 found 45% of employers report difficulty filling skilled roles, pushing wage inflation into maintenance and logistics budgets. T.O.M. should build training pipelines and retention incentives while using predictive maintenance to cut labour‑intensive emergency repairs.

- Impact: higher OPEX, increased downtime

- Wage pressure: compresses margins

- Action: training pipelines & retention

- Tech: predictive maintenance lowers emergency labor

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

GDP volatility 2023–24 cut fleet utilization; flexible terms and tiered pricing protect revenue. Fed funds 5.25–5.50% (mid‑2025) and IG spreads 120–140bps raise funding costs; optimize tenors/RVs to defend margins. Energy and RV swings (diesel $3.80/gal 2024; electricity 15.5¢/kWh; CPO premium 5–15%) shift TCO and disposal proceeds.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Diesel (US 2024) | $3.80/gal |

| CPO premium | 5–15% |

Preview Before You Purchase

T.O.M. Vehicle Rental PESTLE Analysis

The preview shown here is the exact T.O.M. Vehicle Rental PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The content, layout and insights visible in this preview match the final downloadable file with no placeholders or surprises.

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of T.O.M. Vehicle Rental—uncover political, economic, social, technological, legal and environmental factors shaping its future. Actionable insights highlight risks and growth levers. Ideal for investors and strategists. Purchase the full report to get the complete, downloadable analysis now.

Political factors

UK transport policy shifts

Changes to UK transport priorities can reshape demand for commercial rental and contract hire; the government’s ban on new petrol and diesel cars and vans from 2030 (with non-zero-emission hybrids to 2035) accelerates electrification. Over 40 local authorities have introduced or proposed clean-air mandates and low-emission zones, shifting fleet needs toward EVs and ULEVs. T.O.M. should align inventory to policy trends, anticipate regional variation, and actively engage policymakers and trade bodies to surface early signals.

Public sector procurement cycles

Government tenders for vans and specialist vehicles drive utilization and pricing, with public procurement accounting for roughly 12–14% of GDP in OECD/EU economies (2023–24), concentrating significant fleet spend into cyclical tenders. Budget timelines, periodic spending reviews and election cycles create lumpiness in demand. T.O.M. can offer 3–5 year terms and flexible options to align with public-sector frameworks. Achieving preferred supplier status can stabilize volumes across cycles.

Infrastructure and regional levelling-up

Investment in roads and logistics through the UK Levelling Up Fund (total £4.8bn) and major projects drives localized fleet needs, raising demand for HGVs and specialist units in growth corridors. Regional funding disparities create rental hotspots in funded areas, so T.O.M. should site depots close to corridor projects to cut lead times. Flexible cross-depot transfers will smooth short-term imbalances and optimize utilization.

Devolution and local regulations

- Policy variability: regional access rules, congestion and CAZ fees

- Operational impact: harder national fleet allocation and route planning

- Service offering: compliance guidance bundled with rentals

- Pricing: dynamic, location-aware fees to reflect local charges

Trade and import dynamics

Tariffs, customs frictions and rules-of-origin are adding 5–12% to landed vehicle and parts costs and have pushed lead times for new units to roughly 20–30 weeks in 2024, with EU–UK checks and global logistics shifts the main drivers. T.O.M. should diversify OEM relationships, stock critical spares and use forward contracts to hedge component price volatility and FX risk.

- Tariff impact: +5–12% landed cost

- Lead times: ~20–30 weeks (2024)

- Mitigation: diversify OEMs, hold spares

- Hedge: forward contracts for parts/FX

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

Political shifts—2030 petrol/diesel ban, 2035 hybrids, and expanded clean-air zones (ULEZ ~8.6m residents) drive urgent EV conversion and regional compliance costs. Public procurement remains a major, lumpy demand source (public spend ~12–14% GDP), so securing preferred-supplier status smooths volumes. Tariffs and customs add ~5–12% to landed costs and pushed lead times to ~20–30 weeks; diversify suppliers and hold spares to mitigate.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| Clean-air rules | ULEZ ~8.6m | Fleet electrification | Shift EV inventory |

| Public procurement | 12–14% GDP | Lumpy demand | 3–5yr contracts |

| Tariffs/lead times | +5–12% / 20–30w | Cost, availability | Diversify, hedge |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect T.O.M. Vehicle Rental, with data-driven trends and region-specific examples that surface risks and growth opportunities. Designed for executives and investors, it delivers forward-looking insights for strategy, funding and scenario planning.

A condensed, visually segmented PESTLE summary for T.O.M. Vehicle Rental that highlights external risks and market drivers for quick inclusion in presentations or planning sessions; editable notes and a shareable format streamline cross-team alignment and consultant reporting.

Economic factors

UK growth and SME health

SMEs—99.9% of UK businesses, supplying 61.3% of private-sector jobs and 51.6% of turnover (UK Business Population Estimates 2023)—drive van rental demand across trades, delivery and services. GDP volatility in 2023–24 from ONS maps into fleet utilization swings; T.O.M. can scale flexible terms to capture upside and limit downside. Tiered pricing and pause options increase retention in downturns.

Interest rates and financing costs

Contract hire economics are highly sensitive to base rates and credit spreads; US Fed funds at 5.25–5.50% (mid‑2025) and investment‑grade spreads around 120–140 bps materially raise cost of capital and lease pricing. Higher rates push monthly rents up and compress margins unless pricing is adjusted. T.O.M. can optimize tenors, residual assumptions and refinancing windows to lower funding costs. Offering fixed‑rate packages de‑risks client budgets and improves dealability.

Fuel and energy price volatility

Diesel retail averaged about $3.80/gal in the US in 2024 while commercial electricity ran near 15.5¢/kWh, so swings in these prices can shift TCO materially for ICE versus EV fleets and change payback timelines. Customers may alter vehicle mix or lease term in response to operating-cost changes. T.O.M. can offer transparent TCO calculators and fuel-hedging options; mixed fleets provide resilience during price shocks.

Residual value cycles

Residual value cycles drive lease rates and profitability as used commercial vehicle prices directly set end-of-lease RVs; recent remarketing data show certified pre-owned premiums of 5-15% and double-digit RV volatility in 2023–24, so supply constraints can lift RVs while oversupply crushes margins. T.O.M. needs robust RV forecasting, dynamic disposal channels and certified used programs to maximize proceeds.

- RV sensitivity to used prices

- Supply constraints vs oversupply

- Forecasting accuracy target >90%

- Certified used premium 5-15%

Labour market and wage pressure

Technician shortages and driver scarcity drive higher operating costs and downtime; ManpowerGroup 2024 found 45% of employers report difficulty filling skilled roles, pushing wage inflation into maintenance and logistics budgets. T.O.M. should build training pipelines and retention incentives while using predictive maintenance to cut labour‑intensive emergency repairs.

- Impact: higher OPEX, increased downtime

- Wage pressure: compresses margins

- Action: training pipelines & retention

- Tech: predictive maintenance lowers emergency labor

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

GDP volatility 2023–24 cut fleet utilization; flexible terms and tiered pricing protect revenue. Fed funds 5.25–5.50% (mid‑2025) and IG spreads 120–140bps raise funding costs; optimize tenors/RVs to defend margins. Energy and RV swings (diesel $3.80/gal 2024; electricity 15.5¢/kWh; CPO premium 5–15%) shift TCO and disposal proceeds.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Diesel (US 2024) | $3.80/gal |

| CPO premium | 5–15% |

Preview Before You Purchase

T.O.M. Vehicle Rental PESTLE Analysis

The preview shown here is the exact T.O.M. Vehicle Rental PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The content, layout and insights visible in this preview match the final downloadable file with no placeholders or surprises.

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of T.O.M. Vehicle Rental—uncover political, economic, social, technological, legal and environmental factors shaping its future. Actionable insights highlight risks and growth levers. Ideal for investors and strategists. Purchase the full report to get the complete, downloadable analysis now.

Political factors

UK transport policy shifts

Changes to UK transport priorities can reshape demand for commercial rental and contract hire; the government’s ban on new petrol and diesel cars and vans from 2030 (with non-zero-emission hybrids to 2035) accelerates electrification. Over 40 local authorities have introduced or proposed clean-air mandates and low-emission zones, shifting fleet needs toward EVs and ULEVs. T.O.M. should align inventory to policy trends, anticipate regional variation, and actively engage policymakers and trade bodies to surface early signals.

Public sector procurement cycles

Government tenders for vans and specialist vehicles drive utilization and pricing, with public procurement accounting for roughly 12–14% of GDP in OECD/EU economies (2023–24), concentrating significant fleet spend into cyclical tenders. Budget timelines, periodic spending reviews and election cycles create lumpiness in demand. T.O.M. can offer 3–5 year terms and flexible options to align with public-sector frameworks. Achieving preferred supplier status can stabilize volumes across cycles.

Infrastructure and regional levelling-up

Investment in roads and logistics through the UK Levelling Up Fund (total £4.8bn) and major projects drives localized fleet needs, raising demand for HGVs and specialist units in growth corridors. Regional funding disparities create rental hotspots in funded areas, so T.O.M. should site depots close to corridor projects to cut lead times. Flexible cross-depot transfers will smooth short-term imbalances and optimize utilization.

Devolution and local regulations

- Policy variability: regional access rules, congestion and CAZ fees

- Operational impact: harder national fleet allocation and route planning

- Service offering: compliance guidance bundled with rentals

- Pricing: dynamic, location-aware fees to reflect local charges

Trade and import dynamics

Tariffs, customs frictions and rules-of-origin are adding 5–12% to landed vehicle and parts costs and have pushed lead times for new units to roughly 20–30 weeks in 2024, with EU–UK checks and global logistics shifts the main drivers. T.O.M. should diversify OEM relationships, stock critical spares and use forward contracts to hedge component price volatility and FX risk.

- Tariff impact: +5–12% landed cost

- Lead times: ~20–30 weeks (2024)

- Mitigation: diversify OEMs, hold spares

- Hedge: forward contracts for parts/FX

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

Political shifts—2030 petrol/diesel ban, 2035 hybrids, and expanded clean-air zones (ULEZ ~8.6m residents) drive urgent EV conversion and regional compliance costs. Public procurement remains a major, lumpy demand source (public spend ~12–14% GDP), so securing preferred-supplier status smooths volumes. Tariffs and customs add ~5–12% to landed costs and pushed lead times to ~20–30 weeks; diversify suppliers and hold spares to mitigate.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| Clean-air rules | ULEZ ~8.6m | Fleet electrification | Shift EV inventory |

| Public procurement | 12–14% GDP | Lumpy demand | 3–5yr contracts |

| Tariffs/lead times | +5–12% / 20–30w | Cost, availability | Diversify, hedge |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect T.O.M. Vehicle Rental, with data-driven trends and region-specific examples that surface risks and growth opportunities. Designed for executives and investors, it delivers forward-looking insights for strategy, funding and scenario planning.

A condensed, visually segmented PESTLE summary for T.O.M. Vehicle Rental that highlights external risks and market drivers for quick inclusion in presentations or planning sessions; editable notes and a shareable format streamline cross-team alignment and consultant reporting.

Economic factors

UK growth and SME health

SMEs—99.9% of UK businesses, supplying 61.3% of private-sector jobs and 51.6% of turnover (UK Business Population Estimates 2023)—drive van rental demand across trades, delivery and services. GDP volatility in 2023–24 from ONS maps into fleet utilization swings; T.O.M. can scale flexible terms to capture upside and limit downside. Tiered pricing and pause options increase retention in downturns.

Interest rates and financing costs

Contract hire economics are highly sensitive to base rates and credit spreads; US Fed funds at 5.25–5.50% (mid‑2025) and investment‑grade spreads around 120–140 bps materially raise cost of capital and lease pricing. Higher rates push monthly rents up and compress margins unless pricing is adjusted. T.O.M. can optimize tenors, residual assumptions and refinancing windows to lower funding costs. Offering fixed‑rate packages de‑risks client budgets and improves dealability.

Fuel and energy price volatility

Diesel retail averaged about $3.80/gal in the US in 2024 while commercial electricity ran near 15.5¢/kWh, so swings in these prices can shift TCO materially for ICE versus EV fleets and change payback timelines. Customers may alter vehicle mix or lease term in response to operating-cost changes. T.O.M. can offer transparent TCO calculators and fuel-hedging options; mixed fleets provide resilience during price shocks.

Residual value cycles

Residual value cycles drive lease rates and profitability as used commercial vehicle prices directly set end-of-lease RVs; recent remarketing data show certified pre-owned premiums of 5-15% and double-digit RV volatility in 2023–24, so supply constraints can lift RVs while oversupply crushes margins. T.O.M. needs robust RV forecasting, dynamic disposal channels and certified used programs to maximize proceeds.

- RV sensitivity to used prices

- Supply constraints vs oversupply

- Forecasting accuracy target >90%

- Certified used premium 5-15%

Labour market and wage pressure

Technician shortages and driver scarcity drive higher operating costs and downtime; ManpowerGroup 2024 found 45% of employers report difficulty filling skilled roles, pushing wage inflation into maintenance and logistics budgets. T.O.M. should build training pipelines and retention incentives while using predictive maintenance to cut labour‑intensive emergency repairs.

- Impact: higher OPEX, increased downtime

- Wage pressure: compresses margins

- Action: training pipelines & retention

- Tech: predictive maintenance lowers emergency labor

2030/2035 policy push and ULEZ 8.6m — secure public contracts, diversify supply

GDP volatility 2023–24 cut fleet utilization; flexible terms and tiered pricing protect revenue. Fed funds 5.25–5.50% (mid‑2025) and IG spreads 120–140bps raise funding costs; optimize tenors/RVs to defend margins. Energy and RV swings (diesel $3.80/gal 2024; electricity 15.5¢/kWh; CPO premium 5–15%) shift TCO and disposal proceeds.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Diesel (US 2024) | $3.80/gal |

| CPO premium | 5–15% |

Preview Before You Purchase

T.O.M. Vehicle Rental PESTLE Analysis

The preview shown here is the exact T.O.M. Vehicle Rental PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The content, layout and insights visible in this preview match the final downloadable file with no placeholders or surprises.