T.O.M. Vehicle Rental SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

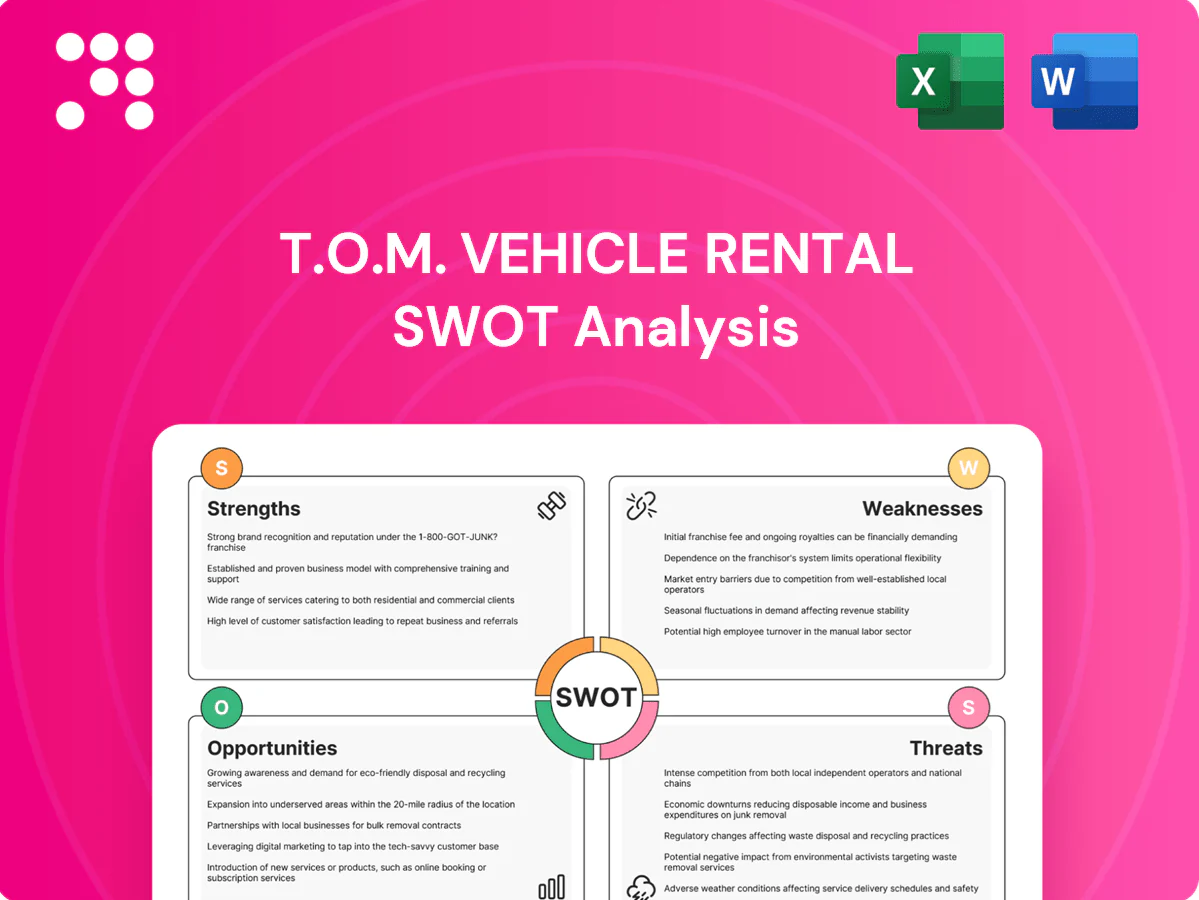

T.O.M. Vehicle Rental's SWOT preview highlights strong fleet scalability and local brand recognition alongside technology gaps and intense competitive pressure. Ready to turn insight into strategy? Purchase the full SWOT analysis for a detailed, editable Word + Excel report with actionable recommendations.

Strengths

Diverse commercial fleet

Diverse commercial fleet spanning vans, trucks and specialist units lets T.O.M. match seasonal and project needs precisely, supporting industry-average utilization around 75% in 2024 and lowering churn; cross-selling across classes can lift ancillary revenue by about 10% and improves pricing power, enabling premium rates versus single-class peers.

Flexible rental and contract hire

Flexible short- and long-term options let T.O.M. align rental costs with customer demand cycles, with subscription/contract models achieving estimated >10% penetration in key markets by 2024.

Flexible terms shift capex to opex, improving client cash flow and stickiness; corporate clients report up to 20% faster procurement cycles when using hire solutions.

Pricing tiers and duration mix optimize yield, driving 8–12% higher revenue per vehicle on mixed-tenure portfolios, while agility strengthens win rates in tenders versus fixed-term rivals.

Integrated fleet management and maintenance

End-to-end fleet management cuts client downtime and total cost of ownership—industry reports cite downtime falls up to 50% with integrated programs and TCO reductions commonly in the 10–15% range. Predictive maintenance and compliance support lower maintenance spend 10–40% and simplify operations. Bundled services deepen customer ties, raising switching costs, while documented service history can boost residual values ~3–7%.

Used vehicle sales channel

Internal remarketing boosts residual value recovery and speeds fleet refresh, helping balance age/mileage profiles; used-to-new transaction ratios are roughly 3:1 in many markets (2024), so selling directly captures sizable value and smooths seasonal rental-sales cycles while informing procurement and vehicle specs.

- Improves recovery: direct remarketing

- Faster refresh: better age/mileage mix

- Revenue diversification: smooths cycles

- Data loop: sales inform procurement

UK-wide customer-centric coverage

UK-wide customer-centric coverage enables T.O.M. to win multi-site contracts and deliver rapid turnaround, supporting tighter SLAs through a local service ethos. Proximity to clients cuts logistics lead times and downtime, while a reputation for responsiveness drives higher referrals and retention. The UK transport and storage sector contributed roughly 5% to UK GDP in 2023 (ONS), and industry bodies like BVRLA represent over 1,000 member firms.

- National footprint: multi-site contracts

- Local ethos: stronger SLA adherence

- Proximity: lower logistics costs/downtime

- Responsiveness: improved referrals/retention

Fleet: utilization 75%, ancillary +10%, subs > 10%

Diverse fleet and cross-sell lift utilization (~75% in 2024) and ancillary revenue +10%, enabling premium pricing.

Flexible short/long rentals and subscriptions (>10% penetration in key markets 2024) improve client stickiness and cashflow.

Integrated fleet mgmt cuts downtime up to 50%, lowers TCO 10–15% and boosts residuals ~3–7%.

| Metric | 2024 |

|---|---|

| Utilization | 75% |

| Ancillary rev | +10% |

| Subs penetration | >10% |

What is included in the product

Provides a strategic overview of T.O.M. Vehicle Rental by outlining its strengths and weaknesses and mapping external opportunities and threats to assess competitive position, growth drivers, operational gaps, and risks shaping the company’s future.

Delivers a concise, visual SWOT matrix tailored to T.O.M. Vehicle Rental for rapid strategy alignment and stakeholder-ready summaries; editable format enables quick updates to reflect shifting market priorities.

Weaknesses

Capital-intensive business model

Large upfront fleet investments squeeze cash and leverage — fleet capex often accounts for more than 60% of total capex at major rental operators, leaving balance sheets sensitive to rate moves. Depreciation and financing expenses (often 15–25% of operating costs) compress margins, while utilization dips of a few percentage points can rapidly turn EBITDA negative. Tight credit markets further limit balance sheet flexibility and growth.

Exposure to B2B demand cycles

Construction, logistics and SME activity account for roughly 65% of T.O.M. Vehicle Rental volumes, so project slowdowns can reduce rental days and rates by up to 20%. Client procurement freezes commonly extend sales cycles 3–6 months. This sector concentration has driven EBITDA volatility swings near ±25% during recent downturns (2020–2023).

Residual value and aging fleet risk

Market shifts compressed resale values after the 2021–22 peak: Manheim reported used-vehicle values down roughly 25% from March 2022 to end‑2024, pressuring defleet proceeds. Misjudged holding periods raise maintenance and capex as average repair costs climb with age, increasing per-unit spend and working-capital needs. EV transition uncertainty—global BEV share ~14% in 2023 (IEA)—complicates RV forecasting and remarketing. Significant write-downs on residuals can erode asset values and risk covenant breaches, constraining investment capacity.

Operational complexity and downtime

Maintaining diverse vehicle types strains workshops and parts supply, expanding SKU counts and technician training needs and increasing turnaround times; fleet downtime is estimated to cost operators roughly $300–$700 per vehicle per day in 2024 industry reports. Scheduling, compliance, and accident management add administrative overhead and can elevate operating costs by several percentage points of revenue. Downtime directly hits revenue and triggers SLA penalties; IT integration with customer systems is resource-intensive, often requiring multi-month projects and dedicated API teams.

- Operational complexity: higher SKU and training burden

- Downtime cost: $300–$700/vehicle/day (2024)

- SLA exposure: lost revenue plus penalties

- IT integration: multi-month, specialized resource need

Geographic concentration in the UK

Geographic concentration in the UK ties T.O.M. Vehicle Rental’s performance closely to UK macro and regulatory moves, with IMF projecting UK GDP growth at about 0.6% for 2024, raising exposure to local shocks and policy shifts. Currency advantages are limited as revenues and costs are predominantly in GBP, and meaningful diversification or pan-European expansion would require new capabilities and substantial capital investment.

- Single-country exposure: higher policy risk

- Limited shock diversification: UK-centric demand

- Minimal FX hedge: GBP-dominated P&L

- Expansion: requires capabilities and capital

Fleet-heavy capex (>60%), 15-25% depreciation pressure, -25% resale shock

High fleet capex (>60% of capex) and 15–25% depreciation/finance pressure margins; small utilization drops swing EBITDA heavily. Resale values fell ~25% from Mar 2022–end‑2024, raising write‑down risk and capex. Operational complexity, $300–$700/vehicle/day downtime, and UK concentration (GDP ~0.6% 2024) limit flexibility.

| Metric | Value |

|---|---|

| Fleet capex share | >60% |

| Depreciation & finance | 15–25% opex |

| Resale change | -25% (Mar22–end24) |

| Downtime cost | $300–$700/veh/day |

| UK GDP 2024 | ~0.6% |

What You See Is What You Get

T.O.M. Vehicle Rental SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full T.O.M. Vehicle Rental report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the exact file available for immediate download after checkout.

Go Beyond the Preview—Access the Full Strategic Report

T.O.M. Vehicle Rental's SWOT preview highlights strong fleet scalability and local brand recognition alongside technology gaps and intense competitive pressure. Ready to turn insight into strategy? Purchase the full SWOT analysis for a detailed, editable Word + Excel report with actionable recommendations.

Strengths

Diverse commercial fleet

Diverse commercial fleet spanning vans, trucks and specialist units lets T.O.M. match seasonal and project needs precisely, supporting industry-average utilization around 75% in 2024 and lowering churn; cross-selling across classes can lift ancillary revenue by about 10% and improves pricing power, enabling premium rates versus single-class peers.

Flexible rental and contract hire

Flexible short- and long-term options let T.O.M. align rental costs with customer demand cycles, with subscription/contract models achieving estimated >10% penetration in key markets by 2024.

Flexible terms shift capex to opex, improving client cash flow and stickiness; corporate clients report up to 20% faster procurement cycles when using hire solutions.

Pricing tiers and duration mix optimize yield, driving 8–12% higher revenue per vehicle on mixed-tenure portfolios, while agility strengthens win rates in tenders versus fixed-term rivals.

Integrated fleet management and maintenance

End-to-end fleet management cuts client downtime and total cost of ownership—industry reports cite downtime falls up to 50% with integrated programs and TCO reductions commonly in the 10–15% range. Predictive maintenance and compliance support lower maintenance spend 10–40% and simplify operations. Bundled services deepen customer ties, raising switching costs, while documented service history can boost residual values ~3–7%.

Used vehicle sales channel

Internal remarketing boosts residual value recovery and speeds fleet refresh, helping balance age/mileage profiles; used-to-new transaction ratios are roughly 3:1 in many markets (2024), so selling directly captures sizable value and smooths seasonal rental-sales cycles while informing procurement and vehicle specs.

- Improves recovery: direct remarketing

- Faster refresh: better age/mileage mix

- Revenue diversification: smooths cycles

- Data loop: sales inform procurement

UK-wide customer-centric coverage

UK-wide customer-centric coverage enables T.O.M. to win multi-site contracts and deliver rapid turnaround, supporting tighter SLAs through a local service ethos. Proximity to clients cuts logistics lead times and downtime, while a reputation for responsiveness drives higher referrals and retention. The UK transport and storage sector contributed roughly 5% to UK GDP in 2023 (ONS), and industry bodies like BVRLA represent over 1,000 member firms.

- National footprint: multi-site contracts

- Local ethos: stronger SLA adherence

- Proximity: lower logistics costs/downtime

- Responsiveness: improved referrals/retention

Fleet: utilization 75%, ancillary +10%, subs > 10%

Diverse fleet and cross-sell lift utilization (~75% in 2024) and ancillary revenue +10%, enabling premium pricing.

Flexible short/long rentals and subscriptions (>10% penetration in key markets 2024) improve client stickiness and cashflow.

Integrated fleet mgmt cuts downtime up to 50%, lowers TCO 10–15% and boosts residuals ~3–7%.

| Metric | 2024 |

|---|---|

| Utilization | 75% |

| Ancillary rev | +10% |

| Subs penetration | >10% |

What is included in the product

Provides a strategic overview of T.O.M. Vehicle Rental by outlining its strengths and weaknesses and mapping external opportunities and threats to assess competitive position, growth drivers, operational gaps, and risks shaping the company’s future.

Delivers a concise, visual SWOT matrix tailored to T.O.M. Vehicle Rental for rapid strategy alignment and stakeholder-ready summaries; editable format enables quick updates to reflect shifting market priorities.

Weaknesses

Capital-intensive business model

Large upfront fleet investments squeeze cash and leverage — fleet capex often accounts for more than 60% of total capex at major rental operators, leaving balance sheets sensitive to rate moves. Depreciation and financing expenses (often 15–25% of operating costs) compress margins, while utilization dips of a few percentage points can rapidly turn EBITDA negative. Tight credit markets further limit balance sheet flexibility and growth.

Exposure to B2B demand cycles

Construction, logistics and SME activity account for roughly 65% of T.O.M. Vehicle Rental volumes, so project slowdowns can reduce rental days and rates by up to 20%. Client procurement freezes commonly extend sales cycles 3–6 months. This sector concentration has driven EBITDA volatility swings near ±25% during recent downturns (2020–2023).

Residual value and aging fleet risk

Market shifts compressed resale values after the 2021–22 peak: Manheim reported used-vehicle values down roughly 25% from March 2022 to end‑2024, pressuring defleet proceeds. Misjudged holding periods raise maintenance and capex as average repair costs climb with age, increasing per-unit spend and working-capital needs. EV transition uncertainty—global BEV share ~14% in 2023 (IEA)—complicates RV forecasting and remarketing. Significant write-downs on residuals can erode asset values and risk covenant breaches, constraining investment capacity.

Operational complexity and downtime

Maintaining diverse vehicle types strains workshops and parts supply, expanding SKU counts and technician training needs and increasing turnaround times; fleet downtime is estimated to cost operators roughly $300–$700 per vehicle per day in 2024 industry reports. Scheduling, compliance, and accident management add administrative overhead and can elevate operating costs by several percentage points of revenue. Downtime directly hits revenue and triggers SLA penalties; IT integration with customer systems is resource-intensive, often requiring multi-month projects and dedicated API teams.

- Operational complexity: higher SKU and training burden

- Downtime cost: $300–$700/vehicle/day (2024)

- SLA exposure: lost revenue plus penalties

- IT integration: multi-month, specialized resource need

Geographic concentration in the UK

Geographic concentration in the UK ties T.O.M. Vehicle Rental’s performance closely to UK macro and regulatory moves, with IMF projecting UK GDP growth at about 0.6% for 2024, raising exposure to local shocks and policy shifts. Currency advantages are limited as revenues and costs are predominantly in GBP, and meaningful diversification or pan-European expansion would require new capabilities and substantial capital investment.

- Single-country exposure: higher policy risk

- Limited shock diversification: UK-centric demand

- Minimal FX hedge: GBP-dominated P&L

- Expansion: requires capabilities and capital

Fleet-heavy capex (>60%), 15-25% depreciation pressure, -25% resale shock

High fleet capex (>60% of capex) and 15–25% depreciation/finance pressure margins; small utilization drops swing EBITDA heavily. Resale values fell ~25% from Mar 2022–end‑2024, raising write‑down risk and capex. Operational complexity, $300–$700/vehicle/day downtime, and UK concentration (GDP ~0.6% 2024) limit flexibility.

| Metric | Value |

|---|---|

| Fleet capex share | >60% |

| Depreciation & finance | 15–25% opex |

| Resale change | -25% (Mar22–end24) |

| Downtime cost | $300–$700/veh/day |

| UK GDP 2024 | ~0.6% |

What You See Is What You Get

T.O.M. Vehicle Rental SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full T.O.M. Vehicle Rental report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the exact file available for immediate download after checkout.

Description

Go Beyond the Preview—Access the Full Strategic Report

T.O.M. Vehicle Rental's SWOT preview highlights strong fleet scalability and local brand recognition alongside technology gaps and intense competitive pressure. Ready to turn insight into strategy? Purchase the full SWOT analysis for a detailed, editable Word + Excel report with actionable recommendations.

Strengths

Diverse commercial fleet

Diverse commercial fleet spanning vans, trucks and specialist units lets T.O.M. match seasonal and project needs precisely, supporting industry-average utilization around 75% in 2024 and lowering churn; cross-selling across classes can lift ancillary revenue by about 10% and improves pricing power, enabling premium rates versus single-class peers.

Flexible rental and contract hire

Flexible short- and long-term options let T.O.M. align rental costs with customer demand cycles, with subscription/contract models achieving estimated >10% penetration in key markets by 2024.

Flexible terms shift capex to opex, improving client cash flow and stickiness; corporate clients report up to 20% faster procurement cycles when using hire solutions.

Pricing tiers and duration mix optimize yield, driving 8–12% higher revenue per vehicle on mixed-tenure portfolios, while agility strengthens win rates in tenders versus fixed-term rivals.

Integrated fleet management and maintenance

End-to-end fleet management cuts client downtime and total cost of ownership—industry reports cite downtime falls up to 50% with integrated programs and TCO reductions commonly in the 10–15% range. Predictive maintenance and compliance support lower maintenance spend 10–40% and simplify operations. Bundled services deepen customer ties, raising switching costs, while documented service history can boost residual values ~3–7%.

Used vehicle sales channel

Internal remarketing boosts residual value recovery and speeds fleet refresh, helping balance age/mileage profiles; used-to-new transaction ratios are roughly 3:1 in many markets (2024), so selling directly captures sizable value and smooths seasonal rental-sales cycles while informing procurement and vehicle specs.

- Improves recovery: direct remarketing

- Faster refresh: better age/mileage mix

- Revenue diversification: smooths cycles

- Data loop: sales inform procurement

UK-wide customer-centric coverage

UK-wide customer-centric coverage enables T.O.M. to win multi-site contracts and deliver rapid turnaround, supporting tighter SLAs through a local service ethos. Proximity to clients cuts logistics lead times and downtime, while a reputation for responsiveness drives higher referrals and retention. The UK transport and storage sector contributed roughly 5% to UK GDP in 2023 (ONS), and industry bodies like BVRLA represent over 1,000 member firms.

- National footprint: multi-site contracts

- Local ethos: stronger SLA adherence

- Proximity: lower logistics costs/downtime

- Responsiveness: improved referrals/retention

Fleet: utilization 75%, ancillary +10%, subs > 10%

Diverse fleet and cross-sell lift utilization (~75% in 2024) and ancillary revenue +10%, enabling premium pricing.

Flexible short/long rentals and subscriptions (>10% penetration in key markets 2024) improve client stickiness and cashflow.

Integrated fleet mgmt cuts downtime up to 50%, lowers TCO 10–15% and boosts residuals ~3–7%.

| Metric | 2024 |

|---|---|

| Utilization | 75% |

| Ancillary rev | +10% |

| Subs penetration | >10% |

What is included in the product

Provides a strategic overview of T.O.M. Vehicle Rental by outlining its strengths and weaknesses and mapping external opportunities and threats to assess competitive position, growth drivers, operational gaps, and risks shaping the company’s future.

Delivers a concise, visual SWOT matrix tailored to T.O.M. Vehicle Rental for rapid strategy alignment and stakeholder-ready summaries; editable format enables quick updates to reflect shifting market priorities.

Weaknesses

Capital-intensive business model

Large upfront fleet investments squeeze cash and leverage — fleet capex often accounts for more than 60% of total capex at major rental operators, leaving balance sheets sensitive to rate moves. Depreciation and financing expenses (often 15–25% of operating costs) compress margins, while utilization dips of a few percentage points can rapidly turn EBITDA negative. Tight credit markets further limit balance sheet flexibility and growth.

Exposure to B2B demand cycles

Construction, logistics and SME activity account for roughly 65% of T.O.M. Vehicle Rental volumes, so project slowdowns can reduce rental days and rates by up to 20%. Client procurement freezes commonly extend sales cycles 3–6 months. This sector concentration has driven EBITDA volatility swings near ±25% during recent downturns (2020–2023).

Residual value and aging fleet risk

Market shifts compressed resale values after the 2021–22 peak: Manheim reported used-vehicle values down roughly 25% from March 2022 to end‑2024, pressuring defleet proceeds. Misjudged holding periods raise maintenance and capex as average repair costs climb with age, increasing per-unit spend and working-capital needs. EV transition uncertainty—global BEV share ~14% in 2023 (IEA)—complicates RV forecasting and remarketing. Significant write-downs on residuals can erode asset values and risk covenant breaches, constraining investment capacity.

Operational complexity and downtime

Maintaining diverse vehicle types strains workshops and parts supply, expanding SKU counts and technician training needs and increasing turnaround times; fleet downtime is estimated to cost operators roughly $300–$700 per vehicle per day in 2024 industry reports. Scheduling, compliance, and accident management add administrative overhead and can elevate operating costs by several percentage points of revenue. Downtime directly hits revenue and triggers SLA penalties; IT integration with customer systems is resource-intensive, often requiring multi-month projects and dedicated API teams.

- Operational complexity: higher SKU and training burden

- Downtime cost: $300–$700/vehicle/day (2024)

- SLA exposure: lost revenue plus penalties

- IT integration: multi-month, specialized resource need

Geographic concentration in the UK

Geographic concentration in the UK ties T.O.M. Vehicle Rental’s performance closely to UK macro and regulatory moves, with IMF projecting UK GDP growth at about 0.6% for 2024, raising exposure to local shocks and policy shifts. Currency advantages are limited as revenues and costs are predominantly in GBP, and meaningful diversification or pan-European expansion would require new capabilities and substantial capital investment.

- Single-country exposure: higher policy risk

- Limited shock diversification: UK-centric demand

- Minimal FX hedge: GBP-dominated P&L

- Expansion: requires capabilities and capital

Fleet-heavy capex (>60%), 15-25% depreciation pressure, -25% resale shock

High fleet capex (>60% of capex) and 15–25% depreciation/finance pressure margins; small utilization drops swing EBITDA heavily. Resale values fell ~25% from Mar 2022–end‑2024, raising write‑down risk and capex. Operational complexity, $300–$700/vehicle/day downtime, and UK concentration (GDP ~0.6% 2024) limit flexibility.

| Metric | Value |

|---|---|

| Fleet capex share | >60% |

| Depreciation & finance | 15–25% opex |

| Resale change | -25% (Mar22–end24) |

| Downtime cost | $300–$700/veh/day |

| UK GDP 2024 | ~0.6% |

What You See Is What You Get

T.O.M. Vehicle Rental SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full T.O.M. Vehicle Rental report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the exact file available for immediate download after checkout.