Topcon Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

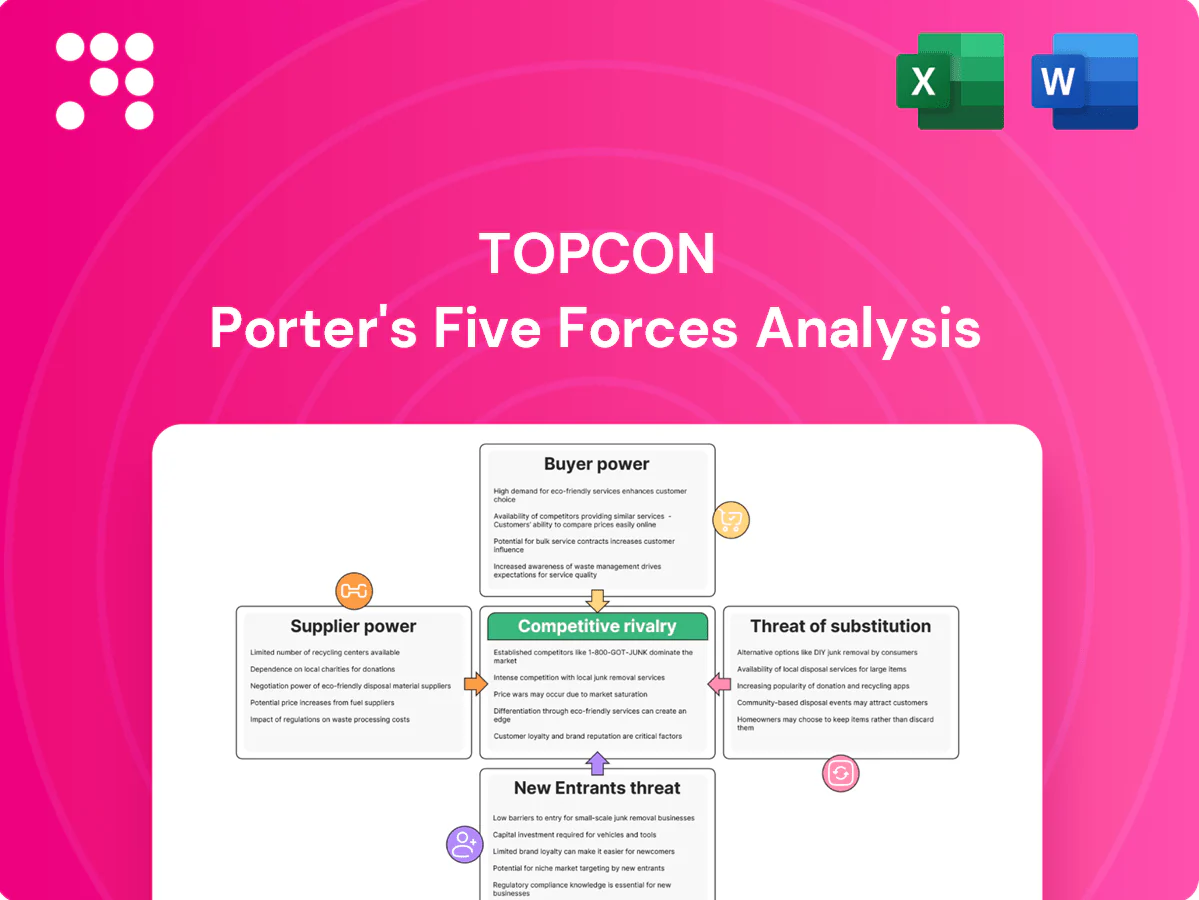

Topcon’s Porter's Five Forces snapshot highlights moderate supplier leverage, differentiated product positioning, and rising competitive intensity from new entrants and substitutes. Strategic strengths include niche tech leadership, but margins face pressure from price-sensitive buyers. This brief hints at critical market dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized optics and sensors

Precision lenses, image sensors and laser diodes are sourced from a small set of qualified vendors—Sony held roughly 40% of the global CMOS image sensor market in 2024—so supplier concentration raises switching costs. Validation cycles commonly run 6–12+ months, making requalification slow. Any capacity or yield shortfall can delay Topcon production, and dual-sourcing, while possible, typically adds significant cost and lead time.

Semiconductors and GNSS modules

GNSS chipsets, FPGAs and high-end processors are highly cyclical and faced allocation risk during the 2020–22 supply crunch, with lead times commonly stretching beyond 20 weeks, amplifying supplier leverage through design-in lock. Long lead times force Topcon into higher safety stocks or redesign risk, increasing working capital and NRE exposure. Strategic supply agreements and rolling forecasts mitigate but do not eliminate this supplier concentration risk.

Software, maps, and data services

Dependencies on mapping data, RTK correction networks, and embedded software toolchains create strong ecosystem lock-in for Topcon; 2024 industry reports estimate up to 60% of workflows rely on third-party corrections. Licensing terms and API changes can shift bargaining power to providers, with RTK subscriptions commonly ranging several hundred dollars per year. Migration to alternatives risks service disruption and downtime, while bundled data-service contracts can recover partial negotiating leverage, shifting 10–30% of supplier power back to buyers.

Medical-grade components and compliance

Geographic supply chain risks

Optics and electronics supply chains are highly concentrated in regions such as Taiwan, Japan and Germany, exposing Topcon to logistics and geopolitical shocks; TSMC held roughly 54 percent of global foundry revenue in 2023, illustrating supplier concentration. Currency swings (the DXY rose sharply in 2022) continue to alter input pricing and margins. Nearshoring or multisourcing lowers exposure but cannot eliminate single‑region shocks. Long‑term contracts smooth cost volatility yet constrain buying flexibility and rapid supplier switches.

- Regional concentration: Taiwan/Japan/Germany hubs

- Market share example: TSMC ~54% foundry revenue (2023)

- Currency risk: DXY spike 2022 impacted input costs

- Mitigants: nearshoring/multisourcing and long‑term contracts

Supplier leverage high; revalidation $0.5–2M and RTK lock-in raise switching costs

Supplier concentration (Sony ~40% CMOS share in 2024; TSMC ~54% foundry rev 2023) and long requalification (0.5–2M, 6–12 months) give suppliers strong leverage. Long lead times and RTK/data lock-in (≈60% workflows rely on third-party corrections in 2024) raise switching costs. Nearshoring/multi‑sourcing and contracts partially mitigate risk.

| Metric | 2023/24 |

|---|---|

| CMOS share (Sony) | ~40% (2024) |

| Foundry rev (TSMC) | ~54% (2023) |

| RTK reliance | ~60% (2024) |

| Revalidation cost/time | $0.5–2M; 6–12m (2024 est.) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry risks specific to Topcon, identifying disruptive threats and strategic levers to protect market share and inform investor or management decision-making.

One-sheet Topcon Porter's Five Forces summary that instantly highlights competitive pain points and actions, with adjustable pressure levels and a ready-to-use spider chart for fast boardroom decisions.

Customers Bargaining Power

Enterprise and government procurement

Construction firms, survey agencies and public buyers drive aggressive tendering, where large order sizes win double-digit price concessions and service-level guarantees; public procurement and infrastructure contracts often run as multi-year frameworks (3–5 years) that compress margins but improve revenue visibility. Lifecycle support and training frequently decide awards, shifting value from hardware to recurring services and spare parts.

Clinical ophthalmology buyers

Clinical ophthalmology buyers prioritize measurement accuracy, workflow efficiency and reimbursement impact when selecting devices; recent 2024 surveys show these factors drive 70%+ procurement decisions. Group purchasing organizations consolidate ~90% of US hospital buying power in 2024, increasing price leverage. Robust peer-reviewed clinical evidence for Topcon products reduces pure price pressure. Deep EMR/PACS integration—EHR adoption >96% in US hospitals—raises switching costs in Topcon’s favor.

Dealer and distributor leverage

Regional dealers and distributors wield strong leverage in fragmented markets, controlling access and local pricing and enabling cross-vendor substitution through broad portfolios. Performance rebates and co-marketing agreements align distributor incentives toward larger suppliers, while product availability and after-sales service amplify bargaining power. Strengthening Topcon's direct channels and digital sales ecosystems can reduce intermediary dependence and margin leakage.

Total cost and interoperability

Buyers price total cost of ownership in 2024, weighing device price plus integration, training and data migration; compatibility with existing fleets and software often creates vendor lock-in that preserves supplier margins. Open standards adopted in 2024 increase buyer leverage by easing integration and reducing switching friction, while multi-week training and migration efforts continue to deter frequent vendor changes and soften aggressive price demands.

- Total cost of ownership focus

- Compatibility drives lock-in

- Open standards raise buyer power

- Training and migration deter switching

Outcome-based expectations

Customers demand outcome-based contracts from Topcon, prioritizing productivity gains, accuracy, and uptime guarantees; service-level and warranty terms become key negotiation levers as remote diagnostics and subscription models shift value toward ongoing services. Demonstrable ROI from deployed systems reduces price discount pressure and strengthens renewal rates.

- Uptime guarantees

- Service-level terms

- Remote diagnostics/subscriptions

- ROI-driven pricing

GPOs control ~90%; EHRs >96% raise switching costs; lifecycle services push recurring revenue

Customers exert strong price and service leverage: GPOs control ~90% of US hospital buying power (2024) and EHR adoption >96% raises switching costs; 2024 surveys show measurement accuracy, workflow and reimbursement drive 70%+ of device purchases. Multi-year public/infrastructure contracts (3–5 years) compress margins while lifecycle services shift value to recurring revenue.

| Metric | 2024 |

|---|---|

| GPO buying power | ~90% |

| EHR adoption (US hospitals) | >96% |

| Procurement drivers: accuracy/workflow | >70% |

| Public contract length | 3–5 years |

Full Version Awaits

Topcon Porter's Five Forces Analysis

This preview shows the exact Topcon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Topcon’s Porter's Five Forces snapshot highlights moderate supplier leverage, differentiated product positioning, and rising competitive intensity from new entrants and substitutes. Strategic strengths include niche tech leadership, but margins face pressure from price-sensitive buyers. This brief hints at critical market dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized optics and sensors

Precision lenses, image sensors and laser diodes are sourced from a small set of qualified vendors—Sony held roughly 40% of the global CMOS image sensor market in 2024—so supplier concentration raises switching costs. Validation cycles commonly run 6–12+ months, making requalification slow. Any capacity or yield shortfall can delay Topcon production, and dual-sourcing, while possible, typically adds significant cost and lead time.

Semiconductors and GNSS modules

GNSS chipsets, FPGAs and high-end processors are highly cyclical and faced allocation risk during the 2020–22 supply crunch, with lead times commonly stretching beyond 20 weeks, amplifying supplier leverage through design-in lock. Long lead times force Topcon into higher safety stocks or redesign risk, increasing working capital and NRE exposure. Strategic supply agreements and rolling forecasts mitigate but do not eliminate this supplier concentration risk.

Software, maps, and data services

Dependencies on mapping data, RTK correction networks, and embedded software toolchains create strong ecosystem lock-in for Topcon; 2024 industry reports estimate up to 60% of workflows rely on third-party corrections. Licensing terms and API changes can shift bargaining power to providers, with RTK subscriptions commonly ranging several hundred dollars per year. Migration to alternatives risks service disruption and downtime, while bundled data-service contracts can recover partial negotiating leverage, shifting 10–30% of supplier power back to buyers.

Medical-grade components and compliance

Geographic supply chain risks

Optics and electronics supply chains are highly concentrated in regions such as Taiwan, Japan and Germany, exposing Topcon to logistics and geopolitical shocks; TSMC held roughly 54 percent of global foundry revenue in 2023, illustrating supplier concentration. Currency swings (the DXY rose sharply in 2022) continue to alter input pricing and margins. Nearshoring or multisourcing lowers exposure but cannot eliminate single‑region shocks. Long‑term contracts smooth cost volatility yet constrain buying flexibility and rapid supplier switches.

- Regional concentration: Taiwan/Japan/Germany hubs

- Market share example: TSMC ~54% foundry revenue (2023)

- Currency risk: DXY spike 2022 impacted input costs

- Mitigants: nearshoring/multisourcing and long‑term contracts

Supplier leverage high; revalidation $0.5–2M and RTK lock-in raise switching costs

Supplier concentration (Sony ~40% CMOS share in 2024; TSMC ~54% foundry rev 2023) and long requalification (0.5–2M, 6–12 months) give suppliers strong leverage. Long lead times and RTK/data lock-in (≈60% workflows rely on third-party corrections in 2024) raise switching costs. Nearshoring/multi‑sourcing and contracts partially mitigate risk.

| Metric | 2023/24 |

|---|---|

| CMOS share (Sony) | ~40% (2024) |

| Foundry rev (TSMC) | ~54% (2023) |

| RTK reliance | ~60% (2024) |

| Revalidation cost/time | $0.5–2M; 6–12m (2024 est.) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry risks specific to Topcon, identifying disruptive threats and strategic levers to protect market share and inform investor or management decision-making.

One-sheet Topcon Porter's Five Forces summary that instantly highlights competitive pain points and actions, with adjustable pressure levels and a ready-to-use spider chart for fast boardroom decisions.

Customers Bargaining Power

Enterprise and government procurement

Construction firms, survey agencies and public buyers drive aggressive tendering, where large order sizes win double-digit price concessions and service-level guarantees; public procurement and infrastructure contracts often run as multi-year frameworks (3–5 years) that compress margins but improve revenue visibility. Lifecycle support and training frequently decide awards, shifting value from hardware to recurring services and spare parts.

Clinical ophthalmology buyers

Clinical ophthalmology buyers prioritize measurement accuracy, workflow efficiency and reimbursement impact when selecting devices; recent 2024 surveys show these factors drive 70%+ procurement decisions. Group purchasing organizations consolidate ~90% of US hospital buying power in 2024, increasing price leverage. Robust peer-reviewed clinical evidence for Topcon products reduces pure price pressure. Deep EMR/PACS integration—EHR adoption >96% in US hospitals—raises switching costs in Topcon’s favor.

Dealer and distributor leverage

Regional dealers and distributors wield strong leverage in fragmented markets, controlling access and local pricing and enabling cross-vendor substitution through broad portfolios. Performance rebates and co-marketing agreements align distributor incentives toward larger suppliers, while product availability and after-sales service amplify bargaining power. Strengthening Topcon's direct channels and digital sales ecosystems can reduce intermediary dependence and margin leakage.

Total cost and interoperability

Buyers price total cost of ownership in 2024, weighing device price plus integration, training and data migration; compatibility with existing fleets and software often creates vendor lock-in that preserves supplier margins. Open standards adopted in 2024 increase buyer leverage by easing integration and reducing switching friction, while multi-week training and migration efforts continue to deter frequent vendor changes and soften aggressive price demands.

- Total cost of ownership focus

- Compatibility drives lock-in

- Open standards raise buyer power

- Training and migration deter switching

Outcome-based expectations

Customers demand outcome-based contracts from Topcon, prioritizing productivity gains, accuracy, and uptime guarantees; service-level and warranty terms become key negotiation levers as remote diagnostics and subscription models shift value toward ongoing services. Demonstrable ROI from deployed systems reduces price discount pressure and strengthens renewal rates.

- Uptime guarantees

- Service-level terms

- Remote diagnostics/subscriptions

- ROI-driven pricing

GPOs control ~90%; EHRs >96% raise switching costs; lifecycle services push recurring revenue

Customers exert strong price and service leverage: GPOs control ~90% of US hospital buying power (2024) and EHR adoption >96% raises switching costs; 2024 surveys show measurement accuracy, workflow and reimbursement drive 70%+ of device purchases. Multi-year public/infrastructure contracts (3–5 years) compress margins while lifecycle services shift value to recurring revenue.

| Metric | 2024 |

|---|---|

| GPO buying power | ~90% |

| EHR adoption (US hospitals) | >96% |

| Procurement drivers: accuracy/workflow | >70% |

| Public contract length | 3–5 years |

Full Version Awaits

Topcon Porter's Five Forces Analysis

This preview shows the exact Topcon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Topcon’s Porter's Five Forces snapshot highlights moderate supplier leverage, differentiated product positioning, and rising competitive intensity from new entrants and substitutes. Strategic strengths include niche tech leadership, but margins face pressure from price-sensitive buyers. This brief hints at critical market dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized optics and sensors

Precision lenses, image sensors and laser diodes are sourced from a small set of qualified vendors—Sony held roughly 40% of the global CMOS image sensor market in 2024—so supplier concentration raises switching costs. Validation cycles commonly run 6–12+ months, making requalification slow. Any capacity or yield shortfall can delay Topcon production, and dual-sourcing, while possible, typically adds significant cost and lead time.

Semiconductors and GNSS modules

GNSS chipsets, FPGAs and high-end processors are highly cyclical and faced allocation risk during the 2020–22 supply crunch, with lead times commonly stretching beyond 20 weeks, amplifying supplier leverage through design-in lock. Long lead times force Topcon into higher safety stocks or redesign risk, increasing working capital and NRE exposure. Strategic supply agreements and rolling forecasts mitigate but do not eliminate this supplier concentration risk.

Software, maps, and data services

Dependencies on mapping data, RTK correction networks, and embedded software toolchains create strong ecosystem lock-in for Topcon; 2024 industry reports estimate up to 60% of workflows rely on third-party corrections. Licensing terms and API changes can shift bargaining power to providers, with RTK subscriptions commonly ranging several hundred dollars per year. Migration to alternatives risks service disruption and downtime, while bundled data-service contracts can recover partial negotiating leverage, shifting 10–30% of supplier power back to buyers.

Medical-grade components and compliance

Geographic supply chain risks

Optics and electronics supply chains are highly concentrated in regions such as Taiwan, Japan and Germany, exposing Topcon to logistics and geopolitical shocks; TSMC held roughly 54 percent of global foundry revenue in 2023, illustrating supplier concentration. Currency swings (the DXY rose sharply in 2022) continue to alter input pricing and margins. Nearshoring or multisourcing lowers exposure but cannot eliminate single‑region shocks. Long‑term contracts smooth cost volatility yet constrain buying flexibility and rapid supplier switches.

- Regional concentration: Taiwan/Japan/Germany hubs

- Market share example: TSMC ~54% foundry revenue (2023)

- Currency risk: DXY spike 2022 impacted input costs

- Mitigants: nearshoring/multisourcing and long‑term contracts

Supplier leverage high; revalidation $0.5–2M and RTK lock-in raise switching costs

Supplier concentration (Sony ~40% CMOS share in 2024; TSMC ~54% foundry rev 2023) and long requalification (0.5–2M, 6–12 months) give suppliers strong leverage. Long lead times and RTK/data lock-in (≈60% workflows rely on third-party corrections in 2024) raise switching costs. Nearshoring/multi‑sourcing and contracts partially mitigate risk.

| Metric | 2023/24 |

|---|---|

| CMOS share (Sony) | ~40% (2024) |

| Foundry rev (TSMC) | ~54% (2023) |

| RTK reliance | ~60% (2024) |

| Revalidation cost/time | $0.5–2M; 6–12m (2024 est.) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry risks specific to Topcon, identifying disruptive threats and strategic levers to protect market share and inform investor or management decision-making.

One-sheet Topcon Porter's Five Forces summary that instantly highlights competitive pain points and actions, with adjustable pressure levels and a ready-to-use spider chart for fast boardroom decisions.

Customers Bargaining Power

Enterprise and government procurement

Construction firms, survey agencies and public buyers drive aggressive tendering, where large order sizes win double-digit price concessions and service-level guarantees; public procurement and infrastructure contracts often run as multi-year frameworks (3–5 years) that compress margins but improve revenue visibility. Lifecycle support and training frequently decide awards, shifting value from hardware to recurring services and spare parts.

Clinical ophthalmology buyers

Clinical ophthalmology buyers prioritize measurement accuracy, workflow efficiency and reimbursement impact when selecting devices; recent 2024 surveys show these factors drive 70%+ procurement decisions. Group purchasing organizations consolidate ~90% of US hospital buying power in 2024, increasing price leverage. Robust peer-reviewed clinical evidence for Topcon products reduces pure price pressure. Deep EMR/PACS integration—EHR adoption >96% in US hospitals—raises switching costs in Topcon’s favor.

Dealer and distributor leverage

Regional dealers and distributors wield strong leverage in fragmented markets, controlling access and local pricing and enabling cross-vendor substitution through broad portfolios. Performance rebates and co-marketing agreements align distributor incentives toward larger suppliers, while product availability and after-sales service amplify bargaining power. Strengthening Topcon's direct channels and digital sales ecosystems can reduce intermediary dependence and margin leakage.

Total cost and interoperability

Buyers price total cost of ownership in 2024, weighing device price plus integration, training and data migration; compatibility with existing fleets and software often creates vendor lock-in that preserves supplier margins. Open standards adopted in 2024 increase buyer leverage by easing integration and reducing switching friction, while multi-week training and migration efforts continue to deter frequent vendor changes and soften aggressive price demands.

- Total cost of ownership focus

- Compatibility drives lock-in

- Open standards raise buyer power

- Training and migration deter switching

Outcome-based expectations

Customers demand outcome-based contracts from Topcon, prioritizing productivity gains, accuracy, and uptime guarantees; service-level and warranty terms become key negotiation levers as remote diagnostics and subscription models shift value toward ongoing services. Demonstrable ROI from deployed systems reduces price discount pressure and strengthens renewal rates.

- Uptime guarantees

- Service-level terms

- Remote diagnostics/subscriptions

- ROI-driven pricing

GPOs control ~90%; EHRs >96% raise switching costs; lifecycle services push recurring revenue

Customers exert strong price and service leverage: GPOs control ~90% of US hospital buying power (2024) and EHR adoption >96% raises switching costs; 2024 surveys show measurement accuracy, workflow and reimbursement drive 70%+ of device purchases. Multi-year public/infrastructure contracts (3–5 years) compress margins while lifecycle services shift value to recurring revenue.

| Metric | 2024 |

|---|---|

| GPO buying power | ~90% |

| EHR adoption (US hospitals) | >96% |

| Procurement drivers: accuracy/workflow | >70% |

| Public contract length | 3–5 years |

Full Version Awaits

Topcon Porter's Five Forces Analysis

This preview shows the exact Topcon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is what you get.