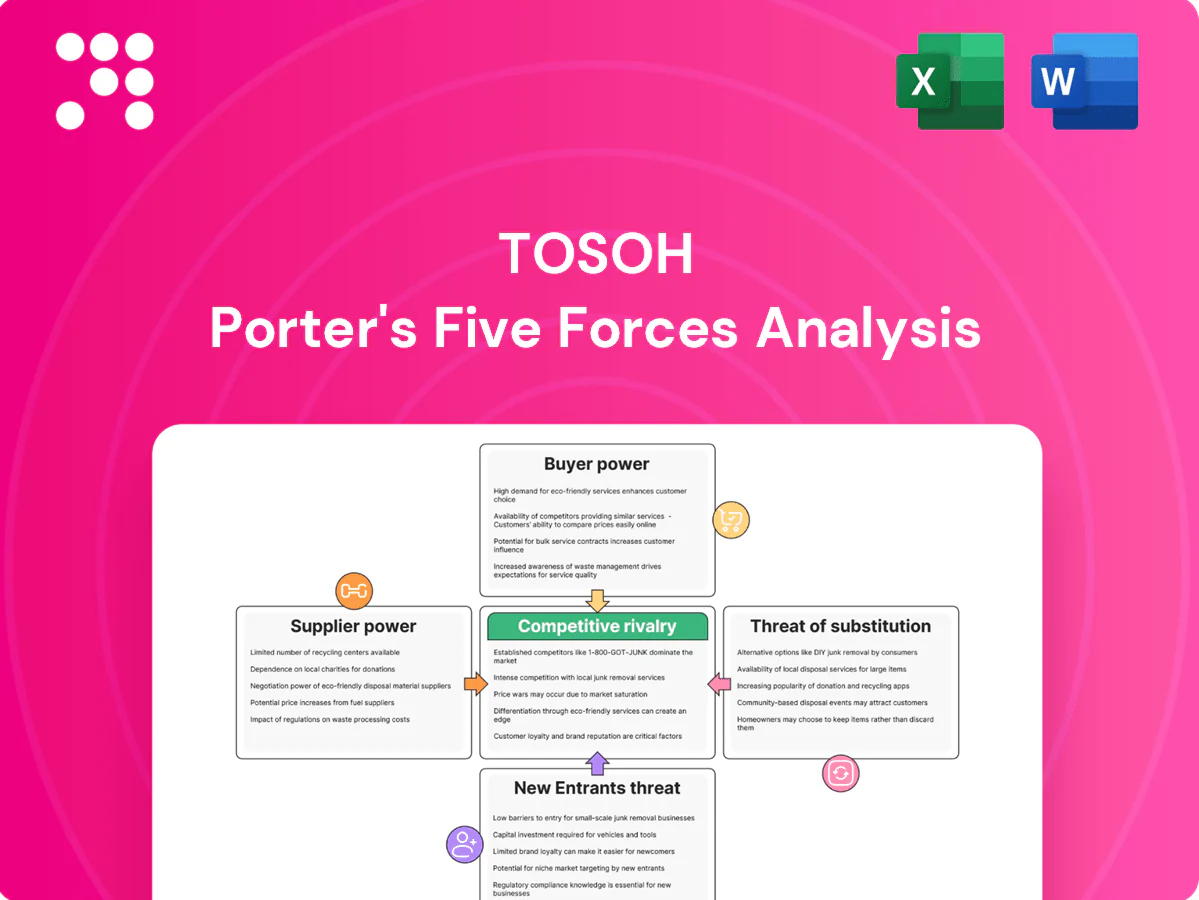

Tosoh Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Tosoh operates in capital‑intensive, technology‑driven chemical markets where supplier concentration, regulatory barriers, and substitute threats shape margins; competitive rivalry is fierce but scale and specialty products create defensive advantages. This snapshot outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Supplier Power 1

Feedstock suppliers for naphtha, ethylene intermediates, chlorine precursors and energy are relatively concentrated among global oil/gas majors and trading houses, giving suppliers clear negotiation leverage. Japan relies on imports for >90% of its oil and most LNG, amplifying exposure to those suppliers. Long-term contracts and hedging reduce but do not remove pricing power. Geopolitical shocks can rapidly tighten supply and push input costs higher.

Supplier Power 2

Tosoh’s partial vertical integration in chlor-alkali and intermediates reduces supplier leverage by internalizing key feedstocks, improving supply certainty and cost visibility. Backward integration into caustic soda and vinyl chloride precursors lowers exposure to spot-price volatility. Gaps remain for specialty precursors and rare metals, where stringent purity specifications force reliance on a small set of qualified upstream partners. This limited supplier pool sustains pockets of bargaining power.

Supplier Power 3

Logistics and energy constraints in Japan raise supplier pass-through power for Tosoh, with LNG accounting for roughly 40% of thermal power and Japan importing ~70–80 million tonnes of LNG annually, tightening feedstock costs. Industrial electricity prices, often 15–20 JPY/kWh range regionally, plus port capacity limits and elevated shipping rates in 2023–24, add supplier-linked cost pressure. Supply-chain disruptions have delayed feedstock and export schedules by weeks, amplifying margin volatility.

Supplier Power 4

Premiums for low-carbon or fully traceable feedstocks compress margins as procurement pays a quality/traceability premium.

- ESG-driven supplier consolidation

- Lower substitutability for hazardous materials

- Certification/audit switching frictions

- Input-premium pressure on margins

Supplier Power 5

Supplier Power 5 — Currency fluctuations materially shift supplier leverage for Tosoh: a weaker yen raises imported input costs even under fixed-volume contracts; USD/JPY traded near 155 in mid-2024, lifting import bills. Financial hedges cut volatility but leave residual exposure; supplier pricing clauses commonly permit partial pass-through of FX-driven cost increases.

- FX rate (mid-2024): USD/JPY ~155

- Hedges: lower volatility, not full neutral

- Contracts: partial pass-through common

Supplier leverage rises as Japan's >90% oil dependence and FX (~155) squeeze margins

Feedstock suppliers (oil/LNG/trading houses) hold strong leverage given Japan's >90% oil import dependence and limited qualified specialty-chemical vendors; Tosoh's chlor-alkali vertical integration mitigates but does not eliminate pockets of supplier power, ESG certification narrows suppliers and raises premiums, and FX (USD/JPY ~155 mid-2024) amplifies import cost pass-through.

| Metric | Value |

|---|---|

| Japan oil import dependence | >90% |

| LNG annual imports (2023–24) | 70–80 Mt |

| LNG share of thermal power | ~40% |

| USD/JPY (mid-2024) | ~155 |

What is included in the product

Concise Porter's Five Forces analysis for Tosoh that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications to inform investor materials, internal strategy, and academic work.

Concise Tosoh Porter's Five Forces one-sheet that clarifies competitive pressures instantly—customize force levels with current data and export clean visuals for pitch decks or boardroom slides to remove analysis bottlenecks.

Customers Bargaining Power

Buyer Power 1

Large industrial buyers in electronics, automotive and petrochemicals concentrate purchasing power and push hard on price and service; global semiconductor revenue surpassed $600 billion in 2024, amplifying buyer leverage over suppliers like Tosoh. Volume commitments are routinely exchanged for double-digit discounts and priority allocation. Rigorous vendor scorecards (KPIs: on-time delivery, defect ppm) intensify performance pressure.

Buyer Power 2

Switching costs for Tosoh specialty grades are medium–high: qualification and purity demands typically require 6–12 months and validation costs often range from $50,000 to $500,000, deterring rapid supplier shifts. Process revalidation and potential yield losses further raise barriers. For commodity chemicals, buyers switch more easily, increasing price sensitivity. Widespread dual-sourcing (used by over 50% of purchasers) keeps pricing competitive.

Buyer Power 3

Cyclical demand swings in 2024 amplified buyer power as downstream customers pushed for extended payment terms and spot index-linking when industry capacity was long. When markets tightened, Tosoh regained leverage by controlling allocations and prioritizing higher-margin contracts. Contract structures commonly use formula pricing tied to feedstock indices, shifting feedstock cost volatility onto buyers.

Buyer Power 4

- Co-development embeds Tosoh in customer processes

- Technical service/joint R&D increases switching costs

- Proprietary specs enable supply lock-in

- Buyers press for IP-sharing and cost reductions

Buyer Power 5

Global buyers benchmark Tosoh offers against international peers using ICIS and Platts PVC, caustic soda and solvent indices (widely referenced in 2024), driving tighter competitive quotes; logistics-to-door and on-time reliability feed into delivered cost comparisons, and any quality variance often triggers contractual price concessions.

- Indices referenced: ICIS, Platts (2024)

- Logistics/reliability part of delivered cost

- Quality variance → price concessions

Buyer consolidation boosts leverage as semiconductor market tops $600B+

Large industrial buyers (electronics, auto, petrochem) concentrate purchasing power and pressure price/service; global semiconductor revenue exceeded $600B in 2024, amplifying buyer leverage.

Switching costs for specialty grades are medium–high: qualification 6–12 months, validation $50,000–$500,000; >50% of buyers use dual‑sourcing.

Co‑development and technical service increase stickiness; Tosoh consolidated net sales ≈620 billion yen FY2024.

| Metric | Value |

|---|---|

| Semiconductor revenue 2024 | $600B+ |

| Tosoh sales FY2024 | ≈620B JPY |

| Dual‑sourcing | >50% |

| Qualification | 6–12 months |

Preview the Actual Deliverable

Tosoh Porter's Five Forces Analysis

This preview shows the exact Tosoh Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re getting the final file as shown, with complete findings and actionable insights for strategic decision-making.

From Overview to Strategy Blueprint

Tosoh operates in capital‑intensive, technology‑driven chemical markets where supplier concentration, regulatory barriers, and substitute threats shape margins; competitive rivalry is fierce but scale and specialty products create defensive advantages. This snapshot outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Supplier Power 1

Feedstock suppliers for naphtha, ethylene intermediates, chlorine precursors and energy are relatively concentrated among global oil/gas majors and trading houses, giving suppliers clear negotiation leverage. Japan relies on imports for >90% of its oil and most LNG, amplifying exposure to those suppliers. Long-term contracts and hedging reduce but do not remove pricing power. Geopolitical shocks can rapidly tighten supply and push input costs higher.

Supplier Power 2

Tosoh’s partial vertical integration in chlor-alkali and intermediates reduces supplier leverage by internalizing key feedstocks, improving supply certainty and cost visibility. Backward integration into caustic soda and vinyl chloride precursors lowers exposure to spot-price volatility. Gaps remain for specialty precursors and rare metals, where stringent purity specifications force reliance on a small set of qualified upstream partners. This limited supplier pool sustains pockets of bargaining power.

Supplier Power 3

Logistics and energy constraints in Japan raise supplier pass-through power for Tosoh, with LNG accounting for roughly 40% of thermal power and Japan importing ~70–80 million tonnes of LNG annually, tightening feedstock costs. Industrial electricity prices, often 15–20 JPY/kWh range regionally, plus port capacity limits and elevated shipping rates in 2023–24, add supplier-linked cost pressure. Supply-chain disruptions have delayed feedstock and export schedules by weeks, amplifying margin volatility.

Supplier Power 4

Premiums for low-carbon or fully traceable feedstocks compress margins as procurement pays a quality/traceability premium.

- ESG-driven supplier consolidation

- Lower substitutability for hazardous materials

- Certification/audit switching frictions

- Input-premium pressure on margins

Supplier Power 5

Supplier Power 5 — Currency fluctuations materially shift supplier leverage for Tosoh: a weaker yen raises imported input costs even under fixed-volume contracts; USD/JPY traded near 155 in mid-2024, lifting import bills. Financial hedges cut volatility but leave residual exposure; supplier pricing clauses commonly permit partial pass-through of FX-driven cost increases.

- FX rate (mid-2024): USD/JPY ~155

- Hedges: lower volatility, not full neutral

- Contracts: partial pass-through common

Supplier leverage rises as Japan's >90% oil dependence and FX (~155) squeeze margins

Feedstock suppliers (oil/LNG/trading houses) hold strong leverage given Japan's >90% oil import dependence and limited qualified specialty-chemical vendors; Tosoh's chlor-alkali vertical integration mitigates but does not eliminate pockets of supplier power, ESG certification narrows suppliers and raises premiums, and FX (USD/JPY ~155 mid-2024) amplifies import cost pass-through.

| Metric | Value |

|---|---|

| Japan oil import dependence | >90% |

| LNG annual imports (2023–24) | 70–80 Mt |

| LNG share of thermal power | ~40% |

| USD/JPY (mid-2024) | ~155 |

What is included in the product

Concise Porter's Five Forces analysis for Tosoh that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications to inform investor materials, internal strategy, and academic work.

Concise Tosoh Porter's Five Forces one-sheet that clarifies competitive pressures instantly—customize force levels with current data and export clean visuals for pitch decks or boardroom slides to remove analysis bottlenecks.

Customers Bargaining Power

Buyer Power 1

Large industrial buyers in electronics, automotive and petrochemicals concentrate purchasing power and push hard on price and service; global semiconductor revenue surpassed $600 billion in 2024, amplifying buyer leverage over suppliers like Tosoh. Volume commitments are routinely exchanged for double-digit discounts and priority allocation. Rigorous vendor scorecards (KPIs: on-time delivery, defect ppm) intensify performance pressure.

Buyer Power 2

Switching costs for Tosoh specialty grades are medium–high: qualification and purity demands typically require 6–12 months and validation costs often range from $50,000 to $500,000, deterring rapid supplier shifts. Process revalidation and potential yield losses further raise barriers. For commodity chemicals, buyers switch more easily, increasing price sensitivity. Widespread dual-sourcing (used by over 50% of purchasers) keeps pricing competitive.

Buyer Power 3

Cyclical demand swings in 2024 amplified buyer power as downstream customers pushed for extended payment terms and spot index-linking when industry capacity was long. When markets tightened, Tosoh regained leverage by controlling allocations and prioritizing higher-margin contracts. Contract structures commonly use formula pricing tied to feedstock indices, shifting feedstock cost volatility onto buyers.

Buyer Power 4

- Co-development embeds Tosoh in customer processes

- Technical service/joint R&D increases switching costs

- Proprietary specs enable supply lock-in

- Buyers press for IP-sharing and cost reductions

Buyer Power 5

Global buyers benchmark Tosoh offers against international peers using ICIS and Platts PVC, caustic soda and solvent indices (widely referenced in 2024), driving tighter competitive quotes; logistics-to-door and on-time reliability feed into delivered cost comparisons, and any quality variance often triggers contractual price concessions.

- Indices referenced: ICIS, Platts (2024)

- Logistics/reliability part of delivered cost

- Quality variance → price concessions

Buyer consolidation boosts leverage as semiconductor market tops $600B+

Large industrial buyers (electronics, auto, petrochem) concentrate purchasing power and pressure price/service; global semiconductor revenue exceeded $600B in 2024, amplifying buyer leverage.

Switching costs for specialty grades are medium–high: qualification 6–12 months, validation $50,000–$500,000; >50% of buyers use dual‑sourcing.

Co‑development and technical service increase stickiness; Tosoh consolidated net sales ≈620 billion yen FY2024.

| Metric | Value |

|---|---|

| Semiconductor revenue 2024 | $600B+ |

| Tosoh sales FY2024 | ≈620B JPY |

| Dual‑sourcing | >50% |

| Qualification | 6–12 months |

Preview the Actual Deliverable

Tosoh Porter's Five Forces Analysis

This preview shows the exact Tosoh Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re getting the final file as shown, with complete findings and actionable insights for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Tosoh operates in capital‑intensive, technology‑driven chemical markets where supplier concentration, regulatory barriers, and substitute threats shape margins; competitive rivalry is fierce but scale and specialty products create defensive advantages. This snapshot outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Supplier Power 1

Feedstock suppliers for naphtha, ethylene intermediates, chlorine precursors and energy are relatively concentrated among global oil/gas majors and trading houses, giving suppliers clear negotiation leverage. Japan relies on imports for >90% of its oil and most LNG, amplifying exposure to those suppliers. Long-term contracts and hedging reduce but do not remove pricing power. Geopolitical shocks can rapidly tighten supply and push input costs higher.

Supplier Power 2

Tosoh’s partial vertical integration in chlor-alkali and intermediates reduces supplier leverage by internalizing key feedstocks, improving supply certainty and cost visibility. Backward integration into caustic soda and vinyl chloride precursors lowers exposure to spot-price volatility. Gaps remain for specialty precursors and rare metals, where stringent purity specifications force reliance on a small set of qualified upstream partners. This limited supplier pool sustains pockets of bargaining power.

Supplier Power 3

Logistics and energy constraints in Japan raise supplier pass-through power for Tosoh, with LNG accounting for roughly 40% of thermal power and Japan importing ~70–80 million tonnes of LNG annually, tightening feedstock costs. Industrial electricity prices, often 15–20 JPY/kWh range regionally, plus port capacity limits and elevated shipping rates in 2023–24, add supplier-linked cost pressure. Supply-chain disruptions have delayed feedstock and export schedules by weeks, amplifying margin volatility.

Supplier Power 4

Premiums for low-carbon or fully traceable feedstocks compress margins as procurement pays a quality/traceability premium.

- ESG-driven supplier consolidation

- Lower substitutability for hazardous materials

- Certification/audit switching frictions

- Input-premium pressure on margins

Supplier Power 5

Supplier Power 5 — Currency fluctuations materially shift supplier leverage for Tosoh: a weaker yen raises imported input costs even under fixed-volume contracts; USD/JPY traded near 155 in mid-2024, lifting import bills. Financial hedges cut volatility but leave residual exposure; supplier pricing clauses commonly permit partial pass-through of FX-driven cost increases.

- FX rate (mid-2024): USD/JPY ~155

- Hedges: lower volatility, not full neutral

- Contracts: partial pass-through common

Supplier leverage rises as Japan's >90% oil dependence and FX (~155) squeeze margins

Feedstock suppliers (oil/LNG/trading houses) hold strong leverage given Japan's >90% oil import dependence and limited qualified specialty-chemical vendors; Tosoh's chlor-alkali vertical integration mitigates but does not eliminate pockets of supplier power, ESG certification narrows suppliers and raises premiums, and FX (USD/JPY ~155 mid-2024) amplifies import cost pass-through.

| Metric | Value |

|---|---|

| Japan oil import dependence | >90% |

| LNG annual imports (2023–24) | 70–80 Mt |

| LNG share of thermal power | ~40% |

| USD/JPY (mid-2024) | ~155 |

What is included in the product

Concise Porter's Five Forces analysis for Tosoh that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications to inform investor materials, internal strategy, and academic work.

Concise Tosoh Porter's Five Forces one-sheet that clarifies competitive pressures instantly—customize force levels with current data and export clean visuals for pitch decks or boardroom slides to remove analysis bottlenecks.

Customers Bargaining Power

Buyer Power 1

Large industrial buyers in electronics, automotive and petrochemicals concentrate purchasing power and push hard on price and service; global semiconductor revenue surpassed $600 billion in 2024, amplifying buyer leverage over suppliers like Tosoh. Volume commitments are routinely exchanged for double-digit discounts and priority allocation. Rigorous vendor scorecards (KPIs: on-time delivery, defect ppm) intensify performance pressure.

Buyer Power 2

Switching costs for Tosoh specialty grades are medium–high: qualification and purity demands typically require 6–12 months and validation costs often range from $50,000 to $500,000, deterring rapid supplier shifts. Process revalidation and potential yield losses further raise barriers. For commodity chemicals, buyers switch more easily, increasing price sensitivity. Widespread dual-sourcing (used by over 50% of purchasers) keeps pricing competitive.

Buyer Power 3

Cyclical demand swings in 2024 amplified buyer power as downstream customers pushed for extended payment terms and spot index-linking when industry capacity was long. When markets tightened, Tosoh regained leverage by controlling allocations and prioritizing higher-margin contracts. Contract structures commonly use formula pricing tied to feedstock indices, shifting feedstock cost volatility onto buyers.

Buyer Power 4

- Co-development embeds Tosoh in customer processes

- Technical service/joint R&D increases switching costs

- Proprietary specs enable supply lock-in

- Buyers press for IP-sharing and cost reductions

Buyer Power 5

Global buyers benchmark Tosoh offers against international peers using ICIS and Platts PVC, caustic soda and solvent indices (widely referenced in 2024), driving tighter competitive quotes; logistics-to-door and on-time reliability feed into delivered cost comparisons, and any quality variance often triggers contractual price concessions.

- Indices referenced: ICIS, Platts (2024)

- Logistics/reliability part of delivered cost

- Quality variance → price concessions

Buyer consolidation boosts leverage as semiconductor market tops $600B+

Large industrial buyers (electronics, auto, petrochem) concentrate purchasing power and pressure price/service; global semiconductor revenue exceeded $600B in 2024, amplifying buyer leverage.

Switching costs for specialty grades are medium–high: qualification 6–12 months, validation $50,000–$500,000; >50% of buyers use dual‑sourcing.

Co‑development and technical service increase stickiness; Tosoh consolidated net sales ≈620 billion yen FY2024.

| Metric | Value |

|---|---|

| Semiconductor revenue 2024 | $600B+ |

| Tosoh sales FY2024 | ≈620B JPY |

| Dual‑sourcing | >50% |

| Qualification | 6–12 months |

Preview the Actual Deliverable

Tosoh Porter's Five Forces Analysis

This preview shows the exact Tosoh Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re getting the final file as shown, with complete findings and actionable insights for strategic decision-making.