TotalEnergies PESTLE Analysis

Skip the Research. Get the Strategy.

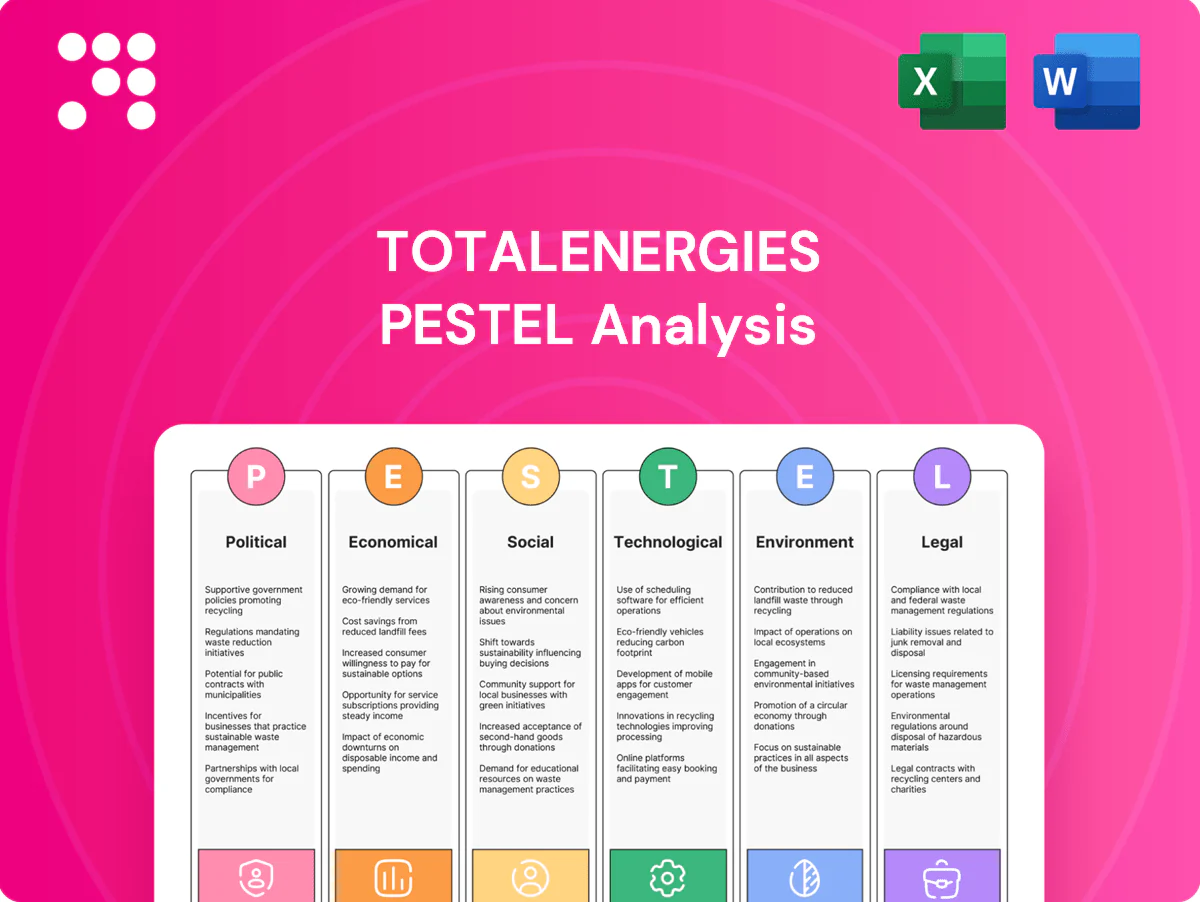

Our PESTLE analysis of TotalEnergies distils how political regulation, economic volatility, social expectations, technological shifts, and environmental and legal pressures shape the company’s strategy and risk profile. Actionable insights highlight regulatory hotspots and growth levers across energy transition and global markets. Ideal for investors and strategists, the full report provides detailed factors, implications and recommended actions. Purchase the complete analysis to gain instant, board-ready intelligence.

Political factors

Geopolitics and supply security

TotalEnergies operates in more than 130 countries, exposing upstream assets and trading flows to conflict, sanctions, and regime change that have historically caused multi-month outages in key basins. Diversified portfolios and flexible logistics — including LNG and shipping assets — mitigate risk but increase coordination complexity across ~40 major hubs. Strategic reserves and government-to-government supply pacts stabilize flows yet can impose political conditions; scenario planning for chokepoints and sanction cascades is essential.

Energy transition policies

National decarbonization roadmaps, notably the EU Green Deal aiming for net-zero by 2050 and a legally binding -55% GHG target by 2030, and the US Inflation Reduction Act’s roughly $369 billion energy/climate package, are shifting capital from hydrocarbons to low-carbon assets. FITs, CfDs and renewable auctions improve project bankability and access to financing, while sudden policy reversals can erode expected returns. Consistent industry advocacy helps align TotalEnergies’ project pipeline with evolving policy trajectories.

Carbon pricing and taxation

ETS expansions and EU CBAM (transitional reporting 2023–25; full payments from 2026) have pushed EUA prices toward €90–100/t in 2024–25, reshaping refining margins and product slates. Higher carbon costs accelerate CCS, biofuels and efficiency investments while compressing fossil fuel profitability. Jurisdictional tax volatility raises after-tax IRRs and required hurdle rates. Hedging and fiscal stabilization clauses are used to mitigate exposure.

Host-country local content

Governments require local procurement, employment and tech transfer in upstream and LNG projects; Nigeria's NOGIC Act (2010) and TotalEnergies' long‑standing JV model with Sonatrach in Algeria exemplify this. Compliance strengthens social license but raises costs and can extend schedules. Joint ventures with national champions reduce political risk while capability‑building programs boost long‑term productivity.

- Local procurement mandates: NOGIC Act (2010)

- Political risk mitigation: JV with Sonatrach

- Cost/timeline impact: higher CAPEX/OPEX and delays

- Capacity building: improves productivity over years

Strategic energy diplomacy

Strategic energy diplomacy ties TotalEnergies into cross-border pipelines, interconnectors and LNG SPAs that link outcomes to state-level diplomacy; global LNG trade is roughly 380 mtpa (2023–24), supporting multi-year revenues via long-term SPAs and MOUs with SOEs that underpin predictable cash flows. Political shifts can force renegotiation or domestic-first supply, while portfolio optionality lets the company rebalance offtake exposure and mitigate sovereign risk.

- Cross-border pipelines: state-linked terms

- Long-term SPAs/MOUs: underpin multi-year cash flows

- Political risk: renegotiation/domestic prioritization

- Portfolio optionality: rebalances offtake exposure

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

TotalEnergies faces state risk across >130 countries and ~40 major hubs; LNG trade ~380 mtpa (2023–24) supports long‑term SPAs. EU EUA ~€90–100/t (2024–25) and US IRA ~$369bn shift capital to low‑carbon assets, raising carbon and fiscal costs. Local content rules and JVs (e.g., Sonatrach) mitigate but increase CAPEX/OPEX and timeline risk.

| Metric | Value |

|---|---|

| Countries/hubs | >130 / ~40 |

| EUA price | €90–100/t (24–25) |

| LNG trade | ~380 mtpa (23–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect TotalEnergies across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, offers forward-looking insights and detailed sub-points to help executives, investors and strategists identify risks, opportunities and support scenario planning.

A concise, visually segmented PESTLE summary of TotalEnergies that can be dropped into presentations, shared across teams, and annotated for region-specific risks—helping streamline planning, align stakeholders, and accelerate risk discussions.

Economic factors

Commodity price volatility

Oil, gas and power price swings (Brent ~USD85/bbl avg 2024) drive earnings variability across TotalEnergies’ upstream, gas and power segments, while integrated trading, hedging and flexible refinery runs have smoothed margins; gas hub decoupling and power price cannibalization are compressing project IRRs, yet a robust balance sheet (around €18bn liquidity/end‑2024) underpins countercyclical investment.

Interest rates and capital access

Rising benchmark yields (US 10y ~4.4% mid‑2025) push WACC up ~100–200bps, squeezing marginal renewables and CCS returns; TotalEnergies’ S&P A‑ rating (A‑, 2024) helps lower funding costs. Use of green bonds and sustainability‑linked loans and project finance (sustainable debt >€5bn issued by 2024) can optimize the capital stack, while disciplined capex (organic spend targeted ~€15bn p.a.) preserves dividends and buybacks.

Global demand and electrification

Global oil demand plateaued in developed markets after reaching about 101 mb/d in 2023 (IEA), with petrochemicals and aviation sustaining barrels. Gas and LNG act as a bridge for intermittent renewables in emerging markets, with global LNG trade near 380 mt in 2023. Electrification lifts power sales—electricity is roughly 20% of final energy—while pressuring liquid fuels. Demand scenarios from IEA and peers steer the balance of molecules versus electrons.

FX and inflation pressures

Import‑intensive equipment and multi‑currency revenues leave TotalEnergies margins exposed to FX swings; EUR/USD volatility (~8% range in 2023–24) amplified translation and transaction impacts. Euro area inflation averaged 2.4% in 2024 while energy EPC/O&M input costs rose about 6–8% y/y, raising budget‑overrun risk. Indexation clauses, local sourcing and active treasury hedging are used to stabilise cash flows.

- FX exposure: transactional + translational

- 2024 inflation: euro area 2.4%

- EPC/O&M cost rise: ~6–8% y/y (2024)

- Mitigants: indexation, local sourcing, treasury hedging

Portfolio resilience and diversification

TotalEnergies balances exposure across upstream, LNG, refining, petrochemicals, renewables and power to smooth commodity cycles; renewables capacity target 35 GW by 2025 supports earnings diversification. Optionality in biofuels, green gases and storage improves margins and volatility resilience, while asset rotation (targeted €2–3bn annual disposals) recycles capital into higher-return, lower-carbon projects and dynamic allocation follows relative economics.

- 35 GW renewables by 2025

- €2–3bn disposals target p.a.

- Upstream to power mix smooths cycles

- Biofuels/green gases/storage optionality

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

Commodity price swings (Brent ~USD85/bbl avg 2024) and gas/LNG dynamics drive earnings volatility; robust liquidity (~€18bn end‑2024) and A‑ rating contain funding stress. Rising yields (US 10y ~4.4% mid‑2025) raise WACC, squeezing renewables/CCS returns; disciplined capex (~€15bn p.a.) and €2–3bn disposals preserve cash.

| Metric | Value |

|---|---|

| Brent 2024 | ~USD85/bbl |

| Liquidity | ~€18bn (end‑2024) |

| US 10y | ~4.4% (mid‑2025) |

| Capex target | ~€15bn p.a. |

Full Version Awaits

TotalEnergies PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This TotalEnergies PESTLE Analysis covers political, economic, social, technological, legal and environmental factors with actionable insights and data-driven observations. The layout and content are final and ready to download immediately after payment.

Skip the Research. Get the Strategy.

Our PESTLE analysis of TotalEnergies distils how political regulation, economic volatility, social expectations, technological shifts, and environmental and legal pressures shape the company’s strategy and risk profile. Actionable insights highlight regulatory hotspots and growth levers across energy transition and global markets. Ideal for investors and strategists, the full report provides detailed factors, implications and recommended actions. Purchase the complete analysis to gain instant, board-ready intelligence.

Political factors

Geopolitics and supply security

TotalEnergies operates in more than 130 countries, exposing upstream assets and trading flows to conflict, sanctions, and regime change that have historically caused multi-month outages in key basins. Diversified portfolios and flexible logistics — including LNG and shipping assets — mitigate risk but increase coordination complexity across ~40 major hubs. Strategic reserves and government-to-government supply pacts stabilize flows yet can impose political conditions; scenario planning for chokepoints and sanction cascades is essential.

Energy transition policies

National decarbonization roadmaps, notably the EU Green Deal aiming for net-zero by 2050 and a legally binding -55% GHG target by 2030, and the US Inflation Reduction Act’s roughly $369 billion energy/climate package, are shifting capital from hydrocarbons to low-carbon assets. FITs, CfDs and renewable auctions improve project bankability and access to financing, while sudden policy reversals can erode expected returns. Consistent industry advocacy helps align TotalEnergies’ project pipeline with evolving policy trajectories.

Carbon pricing and taxation

ETS expansions and EU CBAM (transitional reporting 2023–25; full payments from 2026) have pushed EUA prices toward €90–100/t in 2024–25, reshaping refining margins and product slates. Higher carbon costs accelerate CCS, biofuels and efficiency investments while compressing fossil fuel profitability. Jurisdictional tax volatility raises after-tax IRRs and required hurdle rates. Hedging and fiscal stabilization clauses are used to mitigate exposure.

Host-country local content

Governments require local procurement, employment and tech transfer in upstream and LNG projects; Nigeria's NOGIC Act (2010) and TotalEnergies' long‑standing JV model with Sonatrach in Algeria exemplify this. Compliance strengthens social license but raises costs and can extend schedules. Joint ventures with national champions reduce political risk while capability‑building programs boost long‑term productivity.

- Local procurement mandates: NOGIC Act (2010)

- Political risk mitigation: JV with Sonatrach

- Cost/timeline impact: higher CAPEX/OPEX and delays

- Capacity building: improves productivity over years

Strategic energy diplomacy

Strategic energy diplomacy ties TotalEnergies into cross-border pipelines, interconnectors and LNG SPAs that link outcomes to state-level diplomacy; global LNG trade is roughly 380 mtpa (2023–24), supporting multi-year revenues via long-term SPAs and MOUs with SOEs that underpin predictable cash flows. Political shifts can force renegotiation or domestic-first supply, while portfolio optionality lets the company rebalance offtake exposure and mitigate sovereign risk.

- Cross-border pipelines: state-linked terms

- Long-term SPAs/MOUs: underpin multi-year cash flows

- Political risk: renegotiation/domestic prioritization

- Portfolio optionality: rebalances offtake exposure

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

TotalEnergies faces state risk across >130 countries and ~40 major hubs; LNG trade ~380 mtpa (2023–24) supports long‑term SPAs. EU EUA ~€90–100/t (2024–25) and US IRA ~$369bn shift capital to low‑carbon assets, raising carbon and fiscal costs. Local content rules and JVs (e.g., Sonatrach) mitigate but increase CAPEX/OPEX and timeline risk.

| Metric | Value |

|---|---|

| Countries/hubs | >130 / ~40 |

| EUA price | €90–100/t (24–25) |

| LNG trade | ~380 mtpa (23–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect TotalEnergies across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, offers forward-looking insights and detailed sub-points to help executives, investors and strategists identify risks, opportunities and support scenario planning.

A concise, visually segmented PESTLE summary of TotalEnergies that can be dropped into presentations, shared across teams, and annotated for region-specific risks—helping streamline planning, align stakeholders, and accelerate risk discussions.

Economic factors

Commodity price volatility

Oil, gas and power price swings (Brent ~USD85/bbl avg 2024) drive earnings variability across TotalEnergies’ upstream, gas and power segments, while integrated trading, hedging and flexible refinery runs have smoothed margins; gas hub decoupling and power price cannibalization are compressing project IRRs, yet a robust balance sheet (around €18bn liquidity/end‑2024) underpins countercyclical investment.

Interest rates and capital access

Rising benchmark yields (US 10y ~4.4% mid‑2025) push WACC up ~100–200bps, squeezing marginal renewables and CCS returns; TotalEnergies’ S&P A‑ rating (A‑, 2024) helps lower funding costs. Use of green bonds and sustainability‑linked loans and project finance (sustainable debt >€5bn issued by 2024) can optimize the capital stack, while disciplined capex (organic spend targeted ~€15bn p.a.) preserves dividends and buybacks.

Global demand and electrification

Global oil demand plateaued in developed markets after reaching about 101 mb/d in 2023 (IEA), with petrochemicals and aviation sustaining barrels. Gas and LNG act as a bridge for intermittent renewables in emerging markets, with global LNG trade near 380 mt in 2023. Electrification lifts power sales—electricity is roughly 20% of final energy—while pressuring liquid fuels. Demand scenarios from IEA and peers steer the balance of molecules versus electrons.

FX and inflation pressures

Import‑intensive equipment and multi‑currency revenues leave TotalEnergies margins exposed to FX swings; EUR/USD volatility (~8% range in 2023–24) amplified translation and transaction impacts. Euro area inflation averaged 2.4% in 2024 while energy EPC/O&M input costs rose about 6–8% y/y, raising budget‑overrun risk. Indexation clauses, local sourcing and active treasury hedging are used to stabilise cash flows.

- FX exposure: transactional + translational

- 2024 inflation: euro area 2.4%

- EPC/O&M cost rise: ~6–8% y/y (2024)

- Mitigants: indexation, local sourcing, treasury hedging

Portfolio resilience and diversification

TotalEnergies balances exposure across upstream, LNG, refining, petrochemicals, renewables and power to smooth commodity cycles; renewables capacity target 35 GW by 2025 supports earnings diversification. Optionality in biofuels, green gases and storage improves margins and volatility resilience, while asset rotation (targeted €2–3bn annual disposals) recycles capital into higher-return, lower-carbon projects and dynamic allocation follows relative economics.

- 35 GW renewables by 2025

- €2–3bn disposals target p.a.

- Upstream to power mix smooths cycles

- Biofuels/green gases/storage optionality

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

Commodity price swings (Brent ~USD85/bbl avg 2024) and gas/LNG dynamics drive earnings volatility; robust liquidity (~€18bn end‑2024) and A‑ rating contain funding stress. Rising yields (US 10y ~4.4% mid‑2025) raise WACC, squeezing renewables/CCS returns; disciplined capex (~€15bn p.a.) and €2–3bn disposals preserve cash.

| Metric | Value |

|---|---|

| Brent 2024 | ~USD85/bbl |

| Liquidity | ~€18bn (end‑2024) |

| US 10y | ~4.4% (mid‑2025) |

| Capex target | ~€15bn p.a. |

Full Version Awaits

TotalEnergies PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This TotalEnergies PESTLE Analysis covers political, economic, social, technological, legal and environmental factors with actionable insights and data-driven observations. The layout and content are final and ready to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE analysis of TotalEnergies distils how political regulation, economic volatility, social expectations, technological shifts, and environmental and legal pressures shape the company’s strategy and risk profile. Actionable insights highlight regulatory hotspots and growth levers across energy transition and global markets. Ideal for investors and strategists, the full report provides detailed factors, implications and recommended actions. Purchase the complete analysis to gain instant, board-ready intelligence.

Political factors

Geopolitics and supply security

TotalEnergies operates in more than 130 countries, exposing upstream assets and trading flows to conflict, sanctions, and regime change that have historically caused multi-month outages in key basins. Diversified portfolios and flexible logistics — including LNG and shipping assets — mitigate risk but increase coordination complexity across ~40 major hubs. Strategic reserves and government-to-government supply pacts stabilize flows yet can impose political conditions; scenario planning for chokepoints and sanction cascades is essential.

Energy transition policies

National decarbonization roadmaps, notably the EU Green Deal aiming for net-zero by 2050 and a legally binding -55% GHG target by 2030, and the US Inflation Reduction Act’s roughly $369 billion energy/climate package, are shifting capital from hydrocarbons to low-carbon assets. FITs, CfDs and renewable auctions improve project bankability and access to financing, while sudden policy reversals can erode expected returns. Consistent industry advocacy helps align TotalEnergies’ project pipeline with evolving policy trajectories.

Carbon pricing and taxation

ETS expansions and EU CBAM (transitional reporting 2023–25; full payments from 2026) have pushed EUA prices toward €90–100/t in 2024–25, reshaping refining margins and product slates. Higher carbon costs accelerate CCS, biofuels and efficiency investments while compressing fossil fuel profitability. Jurisdictional tax volatility raises after-tax IRRs and required hurdle rates. Hedging and fiscal stabilization clauses are used to mitigate exposure.

Host-country local content

Governments require local procurement, employment and tech transfer in upstream and LNG projects; Nigeria's NOGIC Act (2010) and TotalEnergies' long‑standing JV model with Sonatrach in Algeria exemplify this. Compliance strengthens social license but raises costs and can extend schedules. Joint ventures with national champions reduce political risk while capability‑building programs boost long‑term productivity.

- Local procurement mandates: NOGIC Act (2010)

- Political risk mitigation: JV with Sonatrach

- Cost/timeline impact: higher CAPEX/OPEX and delays

- Capacity building: improves productivity over years

Strategic energy diplomacy

Strategic energy diplomacy ties TotalEnergies into cross-border pipelines, interconnectors and LNG SPAs that link outcomes to state-level diplomacy; global LNG trade is roughly 380 mtpa (2023–24), supporting multi-year revenues via long-term SPAs and MOUs with SOEs that underpin predictable cash flows. Political shifts can force renegotiation or domestic-first supply, while portfolio optionality lets the company rebalance offtake exposure and mitigate sovereign risk.

- Cross-border pipelines: state-linked terms

- Long-term SPAs/MOUs: underpin multi-year cash flows

- Political risk: renegotiation/domestic prioritization

- Portfolio optionality: rebalances offtake exposure

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

TotalEnergies faces state risk across >130 countries and ~40 major hubs; LNG trade ~380 mtpa (2023–24) supports long‑term SPAs. EU EUA ~€90–100/t (2024–25) and US IRA ~$369bn shift capital to low‑carbon assets, raising carbon and fiscal costs. Local content rules and JVs (e.g., Sonatrach) mitigate but increase CAPEX/OPEX and timeline risk.

| Metric | Value |

|---|---|

| Countries/hubs | >130 / ~40 |

| EUA price | €90–100/t (24–25) |

| LNG trade | ~380 mtpa (23–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect TotalEnergies across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, offers forward-looking insights and detailed sub-points to help executives, investors and strategists identify risks, opportunities and support scenario planning.

A concise, visually segmented PESTLE summary of TotalEnergies that can be dropped into presentations, shared across teams, and annotated for region-specific risks—helping streamline planning, align stakeholders, and accelerate risk discussions.

Economic factors

Commodity price volatility

Oil, gas and power price swings (Brent ~USD85/bbl avg 2024) drive earnings variability across TotalEnergies’ upstream, gas and power segments, while integrated trading, hedging and flexible refinery runs have smoothed margins; gas hub decoupling and power price cannibalization are compressing project IRRs, yet a robust balance sheet (around €18bn liquidity/end‑2024) underpins countercyclical investment.

Interest rates and capital access

Rising benchmark yields (US 10y ~4.4% mid‑2025) push WACC up ~100–200bps, squeezing marginal renewables and CCS returns; TotalEnergies’ S&P A‑ rating (A‑, 2024) helps lower funding costs. Use of green bonds and sustainability‑linked loans and project finance (sustainable debt >€5bn issued by 2024) can optimize the capital stack, while disciplined capex (organic spend targeted ~€15bn p.a.) preserves dividends and buybacks.

Global demand and electrification

Global oil demand plateaued in developed markets after reaching about 101 mb/d in 2023 (IEA), with petrochemicals and aviation sustaining barrels. Gas and LNG act as a bridge for intermittent renewables in emerging markets, with global LNG trade near 380 mt in 2023. Electrification lifts power sales—electricity is roughly 20% of final energy—while pressuring liquid fuels. Demand scenarios from IEA and peers steer the balance of molecules versus electrons.

FX and inflation pressures

Import‑intensive equipment and multi‑currency revenues leave TotalEnergies margins exposed to FX swings; EUR/USD volatility (~8% range in 2023–24) amplified translation and transaction impacts. Euro area inflation averaged 2.4% in 2024 while energy EPC/O&M input costs rose about 6–8% y/y, raising budget‑overrun risk. Indexation clauses, local sourcing and active treasury hedging are used to stabilise cash flows.

- FX exposure: transactional + translational

- 2024 inflation: euro area 2.4%

- EPC/O&M cost rise: ~6–8% y/y (2024)

- Mitigants: indexation, local sourcing, treasury hedging

Portfolio resilience and diversification

TotalEnergies balances exposure across upstream, LNG, refining, petrochemicals, renewables and power to smooth commodity cycles; renewables capacity target 35 GW by 2025 supports earnings diversification. Optionality in biofuels, green gases and storage improves margins and volatility resilience, while asset rotation (targeted €2–3bn annual disposals) recycles capital into higher-return, lower-carbon projects and dynamic allocation follows relative economics.

- 35 GW renewables by 2025

- €2–3bn disposals target p.a.

- Upstream to power mix smooths cycles

- Biofuels/green gases/storage optionality

State risk, carbon pricing and LNG trade drive higher CAPEX/OPEX and timeline risk

Commodity price swings (Brent ~USD85/bbl avg 2024) and gas/LNG dynamics drive earnings volatility; robust liquidity (~€18bn end‑2024) and A‑ rating contain funding stress. Rising yields (US 10y ~4.4% mid‑2025) raise WACC, squeezing renewables/CCS returns; disciplined capex (~€15bn p.a.) and €2–3bn disposals preserve cash.

| Metric | Value |

|---|---|

| Brent 2024 | ~USD85/bbl |

| Liquidity | ~€18bn (end‑2024) |

| US 10y | ~4.4% (mid‑2025) |

| Capex target | ~€15bn p.a. |

Full Version Awaits

TotalEnergies PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This TotalEnergies PESTLE Analysis covers political, economic, social, technological, legal and environmental factors with actionable insights and data-driven observations. The layout and content are final and ready to download immediately after payment.