Towne Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

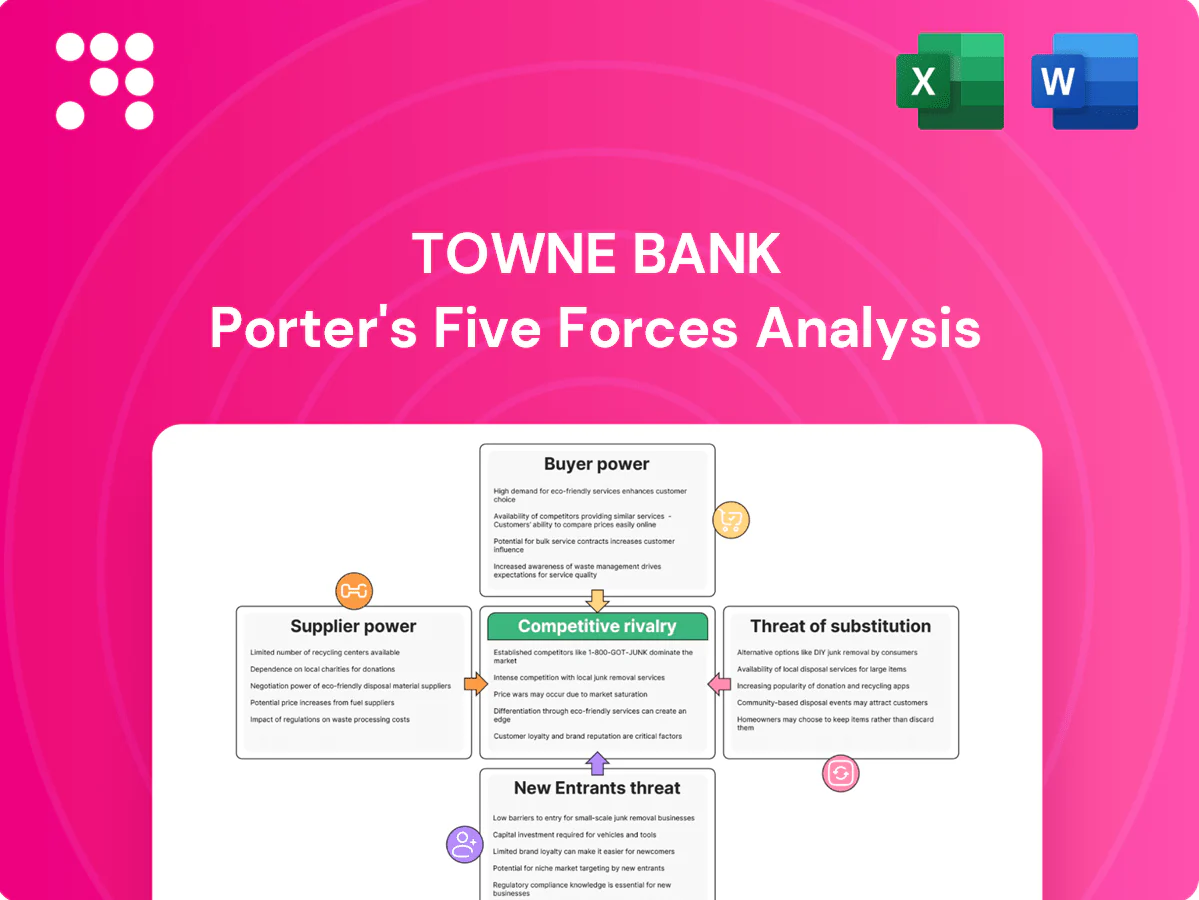

Towne Bank faces moderate buyer power, intense regulatory pressure, and niche local competition that shape its earnings potential. Our snapshot highlights key threats and strategic levers but omits detailed ratings and visuals. Ready to see force-by-force analysis and actionable recommendations? Unlock the full Porter's Five Forces report for Towne Bank now.

Suppliers Bargaining Power

Core deposit funding

Depositors are TowneBank’s primary suppliers of low-cost funding; in 2024 the Fed funds target sat at 5.25–5.50%, pushing depositors to seek higher yields.

As rates rose, customers demanded greater returns or shifted to higher-paying alternatives, lifting TowneBank’s cost of funds and compressing net interest margins.

Strong relationship deposits and treasury clients partially temper this supplier power by providing stickier, lower-beta funding.

Wholesale liquidity providers

Wholesale liquidity providers such as brokered CDs, FHLB advances and correspondent lines supply incremental funding but can reprice quickly and tighten terms in stress; the FHLB system reported roughly $1.1 trillion in advances in 2024, underscoring dependence risk. Covenants, collateral requirements and haircuts increase supplier leverage and cost, while diversifying facilities reduces concentration risk.

Technology and core vendors

Core banking processors remain concentrated: the top three vendors held about 60% of the U.S. core market in 2024, while cloud infra leaders AWS, Azure and GCP commanded roughly 32%, 23% and 11% share, and Visa plus Mastercard accounted for ~75% of card volume, giving suppliers leverage. High switching costs and integration complexity—core replacements often range from $1M–$10M for regional banks—and heavy regulatory scrutiny amplify that leverage. Vendors control pricing, SLAs and product roadmaps, pressuring margins and speed to market, though multi-vendor strategies and open APIs can reduce lock-in.

Talent and professional services

Experienced bankers, lenders and wealth advisors are scarce in regional markets, pushing supplier power higher as 2024 industry surveys show salary growth of roughly 6–8% and turnover near 12–15% at regional banks; lateral hiring markets increasingly bid up compensation and sign-on/retention pay. Culture, career pathways and equity-based incentives are used to mitigate churn and contain wage inflation pressure.

- 2024 salary growth: 6–8%

- Regional bank attrition: ~12–15%

- Sign-on/retention pay: double-digit impact on total comp

- Equity incentives reduce voluntary exits

Regulators as gatekeepers

Regulatory licenses, examinations, and compliance approvals act as non-price supplier constraints for Towne Bank, with rule changes in 2024 tightening capital and reporting requirements and raising implementation costs while limiting product flexibility. Supervisory findings can delay digital or vendor-led initiatives, increasing dependence on incumbent vendors and slowing time-to-market. Proactive compliance investment reduces this implicit supplier power by preserving autonomy and accelerating approvals.

- Licenses/exams: non-price constraints

- 2024 rule changes: higher implementation costs

- Supervisory findings: delay initiatives → vendor dependence

- Proactive compliance: lowers implicit supplier power

Elevated supplier power from higher Fed funds, concentrated tech/vendors and tight labor market

TowneBank faces moderate-to-high supplier power as depositors reacted to 2024 Fed funds at 5.25–5.50%, raising funding costs and compressing NIMs.

Wholesale providers (FHLB advances ~$1.1T in 2024) and concentrated core/cloud/card vendors (top3 core ~60%, AWS/Azure/GCP 32/23/11%, Visa+MC ~75%) can reprice quickly.

Tight labor market (2024 salary growth 6–8%, attrition ~12–15%) and regulatory compliance further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| FHLB advances | $1.1T |

| Top3 core share | ~60% |

| AWS/Azure/GCP | 32/23/11% |

| Visa+MC | ~75% |

| Salary growth | 6–8% |

| Attrition | ~12–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Towne Bank, uncovering key drivers of competition, buyer and supplier power, and risks from substitutes and new entrants. Identifies emerging threats to market share, evaluates pricing influence and profitability, and highlights strategic barriers that protect incumbency.

A concise Porter's Five Forces snapshot tailored to Towne Bank—quickly highlights competitive pressures, regulatory and credit risks, and consolidation threats so leadership can prioritize strategic moves and risk mitigations.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare yields across banks and fintechs; with policy rates near 5% in 2024 and money-market yields often above 4%, price sensitivity intensified. Rapid digital account opening—often under 10 minutes—lowers switching friction, boosting depositor bargaining power. Towne Bank offsets this with loyalty programs and bundled services to reduce elasticity.

Commercial borrowers’ leverage

Middle-market and real estate clients negotiate pricing, covenants and ancillary fees and commonly syndicate or multi-bank to extract better terms, often involving 2–3 lenders. 2024 SLOOS signaled easing credit appetite, shifting bargaining power toward borrowers during growth phases. Deep relationships and faster speed-to-close at banks like Towne Bank partially counterbalance price pressure by preserving deal flow and fee income.

Wealth and private banking

Affluent clients shop advisory fees (commonly 0.5–1.0% annually), platform breadth and performance; transparent schedules and robo-advisors (roughly $1 trillion AUM in 2024) intensify price pressure. Asset portability is low friction (US ACATS transfers ~7–10 business days), while bespoke planning and trust services materially increase client stickiness.

Digital convenience expectations

Buyers now demand seamless mobile experiences, instant payments and 24/7 support; in 2024 about 83% of US retail banking customers use mobile apps, making service lapses immediate churn drivers. With easy fintech alternatives, UX becomes a negotiation lever beyond price, pressuring Towne Bank to invest in continuous app enhancements that shrink perceived switching benefits. Continuous updates cut attrition and raise retention ROI.

- High mobile adoption: 83% (2024)

- 24/7 support expectation

- UX > price in retention

- Ongoing app updates reduce switching gains

Small business ecosystem

Small businesses prioritize integrated payments, payroll and treasury tools, and platform partners increasingly steer bank choice, boosting buyer power; 99.9% of US firms are SMBs, amplifying this effect. Bundled pricing and embedded finance make vendor offers more comparable, while tailored lending and local decisioning remain key differentiators that can offset commoditization.

- Integrated services drive switching

- Platform partners amplify influence

- Bundling raises comparability

- Local lending offsets standardization

Policy ~5%, MM >4%, 83% mobile and $1T robo AUM squeeze margins

Towne Bank faces elevated depositor price sensitivity with policy rates ~5% and money-market yields >4% in 2024; digital onboarding under 10 minutes raises switching. Middle-market borrowers negotiate covenants and multi-bank deals; banks offset with faster closings. Mobile adoption 83% (2024) and ~$1T robo AUM increase fee pressure; bundled services and local lending boost stickiness.

| Metric | 2024 |

|---|---|

| Mobile adoption | 83% |

| Policy rate | ~5% |

| MM yields | >4% |

| Robo AUM | ~$1T |

Full Version Awaits

Towne Bank Porter's Five Forces Analysis

This preview shows the exact Towne Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, comprehensive, and ready for download and use the moment you buy. You're viewing the final deliverable, not a mockup or sample.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Towne Bank faces moderate buyer power, intense regulatory pressure, and niche local competition that shape its earnings potential. Our snapshot highlights key threats and strategic levers but omits detailed ratings and visuals. Ready to see force-by-force analysis and actionable recommendations? Unlock the full Porter's Five Forces report for Towne Bank now.

Suppliers Bargaining Power

Core deposit funding

Depositors are TowneBank’s primary suppliers of low-cost funding; in 2024 the Fed funds target sat at 5.25–5.50%, pushing depositors to seek higher yields.

As rates rose, customers demanded greater returns or shifted to higher-paying alternatives, lifting TowneBank’s cost of funds and compressing net interest margins.

Strong relationship deposits and treasury clients partially temper this supplier power by providing stickier, lower-beta funding.

Wholesale liquidity providers

Wholesale liquidity providers such as brokered CDs, FHLB advances and correspondent lines supply incremental funding but can reprice quickly and tighten terms in stress; the FHLB system reported roughly $1.1 trillion in advances in 2024, underscoring dependence risk. Covenants, collateral requirements and haircuts increase supplier leverage and cost, while diversifying facilities reduces concentration risk.

Technology and core vendors

Core banking processors remain concentrated: the top three vendors held about 60% of the U.S. core market in 2024, while cloud infra leaders AWS, Azure and GCP commanded roughly 32%, 23% and 11% share, and Visa plus Mastercard accounted for ~75% of card volume, giving suppliers leverage. High switching costs and integration complexity—core replacements often range from $1M–$10M for regional banks—and heavy regulatory scrutiny amplify that leverage. Vendors control pricing, SLAs and product roadmaps, pressuring margins and speed to market, though multi-vendor strategies and open APIs can reduce lock-in.

Talent and professional services

Experienced bankers, lenders and wealth advisors are scarce in regional markets, pushing supplier power higher as 2024 industry surveys show salary growth of roughly 6–8% and turnover near 12–15% at regional banks; lateral hiring markets increasingly bid up compensation and sign-on/retention pay. Culture, career pathways and equity-based incentives are used to mitigate churn and contain wage inflation pressure.

- 2024 salary growth: 6–8%

- Regional bank attrition: ~12–15%

- Sign-on/retention pay: double-digit impact on total comp

- Equity incentives reduce voluntary exits

Regulators as gatekeepers

Regulatory licenses, examinations, and compliance approvals act as non-price supplier constraints for Towne Bank, with rule changes in 2024 tightening capital and reporting requirements and raising implementation costs while limiting product flexibility. Supervisory findings can delay digital or vendor-led initiatives, increasing dependence on incumbent vendors and slowing time-to-market. Proactive compliance investment reduces this implicit supplier power by preserving autonomy and accelerating approvals.

- Licenses/exams: non-price constraints

- 2024 rule changes: higher implementation costs

- Supervisory findings: delay initiatives → vendor dependence

- Proactive compliance: lowers implicit supplier power

Elevated supplier power from higher Fed funds, concentrated tech/vendors and tight labor market

TowneBank faces moderate-to-high supplier power as depositors reacted to 2024 Fed funds at 5.25–5.50%, raising funding costs and compressing NIMs.

Wholesale providers (FHLB advances ~$1.1T in 2024) and concentrated core/cloud/card vendors (top3 core ~60%, AWS/Azure/GCP 32/23/11%, Visa+MC ~75%) can reprice quickly.

Tight labor market (2024 salary growth 6–8%, attrition ~12–15%) and regulatory compliance further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| FHLB advances | $1.1T |

| Top3 core share | ~60% |

| AWS/Azure/GCP | 32/23/11% |

| Visa+MC | ~75% |

| Salary growth | 6–8% |

| Attrition | ~12–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Towne Bank, uncovering key drivers of competition, buyer and supplier power, and risks from substitutes and new entrants. Identifies emerging threats to market share, evaluates pricing influence and profitability, and highlights strategic barriers that protect incumbency.

A concise Porter's Five Forces snapshot tailored to Towne Bank—quickly highlights competitive pressures, regulatory and credit risks, and consolidation threats so leadership can prioritize strategic moves and risk mitigations.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare yields across banks and fintechs; with policy rates near 5% in 2024 and money-market yields often above 4%, price sensitivity intensified. Rapid digital account opening—often under 10 minutes—lowers switching friction, boosting depositor bargaining power. Towne Bank offsets this with loyalty programs and bundled services to reduce elasticity.

Commercial borrowers’ leverage

Middle-market and real estate clients negotiate pricing, covenants and ancillary fees and commonly syndicate or multi-bank to extract better terms, often involving 2–3 lenders. 2024 SLOOS signaled easing credit appetite, shifting bargaining power toward borrowers during growth phases. Deep relationships and faster speed-to-close at banks like Towne Bank partially counterbalance price pressure by preserving deal flow and fee income.

Wealth and private banking

Affluent clients shop advisory fees (commonly 0.5–1.0% annually), platform breadth and performance; transparent schedules and robo-advisors (roughly $1 trillion AUM in 2024) intensify price pressure. Asset portability is low friction (US ACATS transfers ~7–10 business days), while bespoke planning and trust services materially increase client stickiness.

Digital convenience expectations

Buyers now demand seamless mobile experiences, instant payments and 24/7 support; in 2024 about 83% of US retail banking customers use mobile apps, making service lapses immediate churn drivers. With easy fintech alternatives, UX becomes a negotiation lever beyond price, pressuring Towne Bank to invest in continuous app enhancements that shrink perceived switching benefits. Continuous updates cut attrition and raise retention ROI.

- High mobile adoption: 83% (2024)

- 24/7 support expectation

- UX > price in retention

- Ongoing app updates reduce switching gains

Small business ecosystem

Small businesses prioritize integrated payments, payroll and treasury tools, and platform partners increasingly steer bank choice, boosting buyer power; 99.9% of US firms are SMBs, amplifying this effect. Bundled pricing and embedded finance make vendor offers more comparable, while tailored lending and local decisioning remain key differentiators that can offset commoditization.

- Integrated services drive switching

- Platform partners amplify influence

- Bundling raises comparability

- Local lending offsets standardization

Policy ~5%, MM >4%, 83% mobile and $1T robo AUM squeeze margins

Towne Bank faces elevated depositor price sensitivity with policy rates ~5% and money-market yields >4% in 2024; digital onboarding under 10 minutes raises switching. Middle-market borrowers negotiate covenants and multi-bank deals; banks offset with faster closings. Mobile adoption 83% (2024) and ~$1T robo AUM increase fee pressure; bundled services and local lending boost stickiness.

| Metric | 2024 |

|---|---|

| Mobile adoption | 83% |

| Policy rate | ~5% |

| MM yields | >4% |

| Robo AUM | ~$1T |

Full Version Awaits

Towne Bank Porter's Five Forces Analysis

This preview shows the exact Towne Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, comprehensive, and ready for download and use the moment you buy. You're viewing the final deliverable, not a mockup or sample.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Towne Bank faces moderate buyer power, intense regulatory pressure, and niche local competition that shape its earnings potential. Our snapshot highlights key threats and strategic levers but omits detailed ratings and visuals. Ready to see force-by-force analysis and actionable recommendations? Unlock the full Porter's Five Forces report for Towne Bank now.

Suppliers Bargaining Power

Core deposit funding

Depositors are TowneBank’s primary suppliers of low-cost funding; in 2024 the Fed funds target sat at 5.25–5.50%, pushing depositors to seek higher yields.

As rates rose, customers demanded greater returns or shifted to higher-paying alternatives, lifting TowneBank’s cost of funds and compressing net interest margins.

Strong relationship deposits and treasury clients partially temper this supplier power by providing stickier, lower-beta funding.

Wholesale liquidity providers

Wholesale liquidity providers such as brokered CDs, FHLB advances and correspondent lines supply incremental funding but can reprice quickly and tighten terms in stress; the FHLB system reported roughly $1.1 trillion in advances in 2024, underscoring dependence risk. Covenants, collateral requirements and haircuts increase supplier leverage and cost, while diversifying facilities reduces concentration risk.

Technology and core vendors

Core banking processors remain concentrated: the top three vendors held about 60% of the U.S. core market in 2024, while cloud infra leaders AWS, Azure and GCP commanded roughly 32%, 23% and 11% share, and Visa plus Mastercard accounted for ~75% of card volume, giving suppliers leverage. High switching costs and integration complexity—core replacements often range from $1M–$10M for regional banks—and heavy regulatory scrutiny amplify that leverage. Vendors control pricing, SLAs and product roadmaps, pressuring margins and speed to market, though multi-vendor strategies and open APIs can reduce lock-in.

Talent and professional services

Experienced bankers, lenders and wealth advisors are scarce in regional markets, pushing supplier power higher as 2024 industry surveys show salary growth of roughly 6–8% and turnover near 12–15% at regional banks; lateral hiring markets increasingly bid up compensation and sign-on/retention pay. Culture, career pathways and equity-based incentives are used to mitigate churn and contain wage inflation pressure.

- 2024 salary growth: 6–8%

- Regional bank attrition: ~12–15%

- Sign-on/retention pay: double-digit impact on total comp

- Equity incentives reduce voluntary exits

Regulators as gatekeepers

Regulatory licenses, examinations, and compliance approvals act as non-price supplier constraints for Towne Bank, with rule changes in 2024 tightening capital and reporting requirements and raising implementation costs while limiting product flexibility. Supervisory findings can delay digital or vendor-led initiatives, increasing dependence on incumbent vendors and slowing time-to-market. Proactive compliance investment reduces this implicit supplier power by preserving autonomy and accelerating approvals.

- Licenses/exams: non-price constraints

- 2024 rule changes: higher implementation costs

- Supervisory findings: delay initiatives → vendor dependence

- Proactive compliance: lowers implicit supplier power

Elevated supplier power from higher Fed funds, concentrated tech/vendors and tight labor market

TowneBank faces moderate-to-high supplier power as depositors reacted to 2024 Fed funds at 5.25–5.50%, raising funding costs and compressing NIMs.

Wholesale providers (FHLB advances ~$1.1T in 2024) and concentrated core/cloud/card vendors (top3 core ~60%, AWS/Azure/GCP 32/23/11%, Visa+MC ~75%) can reprice quickly.

Tight labor market (2024 salary growth 6–8%, attrition ~12–15%) and regulatory compliance further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| FHLB advances | $1.1T |

| Top3 core share | ~60% |

| AWS/Azure/GCP | 32/23/11% |

| Visa+MC | ~75% |

| Salary growth | 6–8% |

| Attrition | ~12–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Towne Bank, uncovering key drivers of competition, buyer and supplier power, and risks from substitutes and new entrants. Identifies emerging threats to market share, evaluates pricing influence and profitability, and highlights strategic barriers that protect incumbency.

A concise Porter's Five Forces snapshot tailored to Towne Bank—quickly highlights competitive pressures, regulatory and credit risks, and consolidation threats so leadership can prioritize strategic moves and risk mitigations.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare yields across banks and fintechs; with policy rates near 5% in 2024 and money-market yields often above 4%, price sensitivity intensified. Rapid digital account opening—often under 10 minutes—lowers switching friction, boosting depositor bargaining power. Towne Bank offsets this with loyalty programs and bundled services to reduce elasticity.

Commercial borrowers’ leverage

Middle-market and real estate clients negotiate pricing, covenants and ancillary fees and commonly syndicate or multi-bank to extract better terms, often involving 2–3 lenders. 2024 SLOOS signaled easing credit appetite, shifting bargaining power toward borrowers during growth phases. Deep relationships and faster speed-to-close at banks like Towne Bank partially counterbalance price pressure by preserving deal flow and fee income.

Wealth and private banking

Affluent clients shop advisory fees (commonly 0.5–1.0% annually), platform breadth and performance; transparent schedules and robo-advisors (roughly $1 trillion AUM in 2024) intensify price pressure. Asset portability is low friction (US ACATS transfers ~7–10 business days), while bespoke planning and trust services materially increase client stickiness.

Digital convenience expectations

Buyers now demand seamless mobile experiences, instant payments and 24/7 support; in 2024 about 83% of US retail banking customers use mobile apps, making service lapses immediate churn drivers. With easy fintech alternatives, UX becomes a negotiation lever beyond price, pressuring Towne Bank to invest in continuous app enhancements that shrink perceived switching benefits. Continuous updates cut attrition and raise retention ROI.

- High mobile adoption: 83% (2024)

- 24/7 support expectation

- UX > price in retention

- Ongoing app updates reduce switching gains

Small business ecosystem

Small businesses prioritize integrated payments, payroll and treasury tools, and platform partners increasingly steer bank choice, boosting buyer power; 99.9% of US firms are SMBs, amplifying this effect. Bundled pricing and embedded finance make vendor offers more comparable, while tailored lending and local decisioning remain key differentiators that can offset commoditization.

- Integrated services drive switching

- Platform partners amplify influence

- Bundling raises comparability

- Local lending offsets standardization

Policy ~5%, MM >4%, 83% mobile and $1T robo AUM squeeze margins

Towne Bank faces elevated depositor price sensitivity with policy rates ~5% and money-market yields >4% in 2024; digital onboarding under 10 minutes raises switching. Middle-market borrowers negotiate covenants and multi-bank deals; banks offset with faster closings. Mobile adoption 83% (2024) and ~$1T robo AUM increase fee pressure; bundled services and local lending boost stickiness.

| Metric | 2024 |

|---|---|

| Mobile adoption | 83% |

| Policy rate | ~5% |

| MM yields | >4% |

| Robo AUM | ~$1T |

Full Version Awaits

Towne Bank Porter's Five Forces Analysis

This preview shows the exact Towne Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, comprehensive, and ready for download and use the moment you buy. You're viewing the final deliverable, not a mockup or sample.