Shenzhen Transsion Holding Porter's Five Forces Analysis

From Overview to Strategy Blueprint

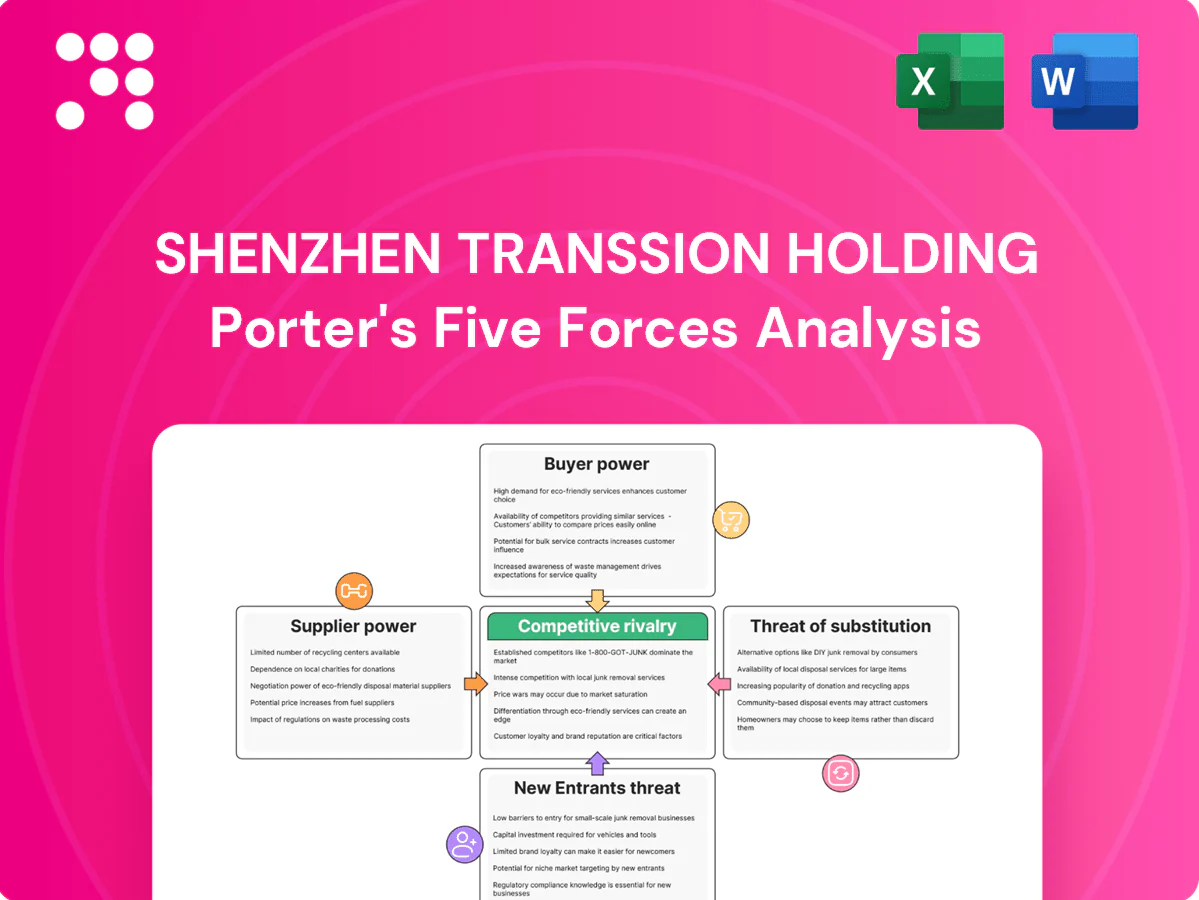

Shenzhen Transsion Holding faces intense rivalry from global smartphone makers, rising buyer power in emerging markets, and supplier concentration risks for key components, while low switching costs and nascent substitutes pressure margins. This snapshot highlights strategic vulnerabilities and growth levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated chipset sources

Smartphone SoCs are concentrated among a few vendors—MediaTek (≈45% shipments in 2024) and Qualcomm (≈30%)—giving upstream bargaining power. Transsion offsets this via volume commitments and platform reuse across Tecno, Itel and Infinix. Roadmap or pricing shifts at a key chipmaker can raise costs and delay launches. Diversifying into multiple SKUs per chipset generation reduces dependency risk.

Display and memory volatility

Panels and NAND/DRAM supply cycles drive price swings that suppliers pass through, with display+memory representing ≈30% of a smartphone BOM in 2024. Transsion’s scale in emerging markets (≈40% smartphone share in Africa) gives it some leverage, but premium suppliers still prioritize larger global OEMs. Long-term agreements and second-sourcing temper spikes yet cannot fully neutralize tight-cycle pricing. Engineering for component interchangeability helps sustain margins.

EMS/ODM and manufacturing partners

Reliance on EMS/ODM partners like Wingtech for cost-efficient assembly creates coordination dependence, with standardized Transsion designs enabling faster capacity switches but line requalification and yield learning often taking 2–6 weeks and causing friction. EMS players frequently run >85–90% utilization in peak quarters, giving suppliers leverage during demand surges. Co-locating procurement, NPI, and QA shortens ramp times and materially reduces switching pain.

Logistics and local service networks

Shipping into Africa, South Asia and LATAM needs freight, customs brokers and local last-mile partners; capacity or regulatory delays can give these intermediaries pricing power, but Transsion’s Carlcare after-sales network (over 1,000 service points in Africa by 2024) and established channels generate repeat business that mitigates supplier leverage.

- Local expertise crucial

- Regulatory delays = pricing power

- Carlcare >1,000 points (2024)

- Multi-country tenders improve terms ~15%

Currency and geopolitical exposure

Inputs for Transsion are largely USD-denominated while many sales are in local currencies, so FX stress amplifies supplier leverage and can force higher local costs; sanctions and export controls have periodically limited access to certain components, raising replacement and lead-time risks. Hedging and staggered purchasing mitigate some exposure but suppliers still extract prepayments or tighter terms, while localized sourcing reduces vulnerability.

- USD invoicing vs local revenues increases FX pass-through risk

- Sanctions/export controls limit component access and raise sourcing costs

- Hedging/staggered buys reduce but do not eliminate supplier leverage

- Localized sourcing lowers geopolitical exposure

SoC concentration boosts supplier leverage; display+memory ~30% BOM forces pass-through

Key chip supply is concentrated (MediaTek ≈45% shipments, Qualcomm ≈30% in 2024), giving upstream leverage; Transsion offsets with platform reuse and volume commitments. Display+NAND/DRAM ≈30% of BOM; panel/memory cycles drive cost pass-through despite Transsion’s ≈40% AFR smartphone share. EMS utilization >85–90% and Carlcare >1,000 Africa points (2024) create operational dependencies; hedging and multi-country tenders trim but do not remove supplier power.

| Item | 2024 Metric |

|---|---|

| SoC concentration | MediaTek ~45%, Qualcomm ~30% |

| Display+Memory BOM | ~30% |

| Africa market share | ~40% |

| EMS peak util. | >85–90% |

| Carlcare points | >1,000 |

What is included in the product

Tailored exclusively for Shenzhen Transsion Holding, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers, and disruptive substitutes shaping pricing, profitability and market share dynamics.

A concise, one-sheet Porter's Five Forces for Shenzhen Transsion Holding—instantly highlights supplier, buyer, entrant, substitute and competitive rivalry pressures to guide rapid strategic decisions and slide-ready recommendations.

Customers Bargaining Power

Highly price-sensitive consumers

Emerging-market buyers are extremely value-driven, amplifying price pressure and contributing to sub-$150 average selling prices in many African and South Asian markets; Transsion holds over 40% smartphone share in Africa, intensifying competition. Small feature gaps trigger switching, keeping ARPUs depressed. Transsion counters with aggressive pricing and localized specs—long battery life, multi-SIM—and uses bundled offers and financing to soften price elasticity.

Powerful retail and distributor channels

Independent retailers, wholesalers and carriers across Africa and South Asia control shelf space and can switch brands, forcing rebates and extended credit; Transsion faced this dynamic despite holding roughly 54% of African smartphone shipments in 2024. Transsion’s deep channel relationships and broad distribution network secure favorable positioning. Aggressive sell-out support and retailer training increase partner stickiness and reduce switching.

Low switching costs

Android ecosystem parity (Android ~72% global share in 2024, StatCounter) and frequent promotions make switching nearly frictionless, letting buyers compare specs and prices instantly on online marketplaces. Transsion raises perceived switching costs with localized UX (HiOS/XOS) and expansive after-sales support across key markets. Trade-in programs further increase retention by offering cash discounts and upgrade paths.

After-sales expectations

Reliability and fast turnaround drive Transsion repeat purchases; global smartphone return rates ran about 2% in 2023–24, so timely service directly limits churn. Customers demand affordable repairs and spare parts; shortages amplify buyer power via negative word-of-mouth. Carlcare’s broad service network reduces escalation and raises trust, while transparent warranty terms curb return pressure.

- after-sales reliability: decisive for repeat buys

- repair/spares affordability: reduces buyer bargaining

- Carlcare network: lowers complaint escalation

- warranty transparency: limits returns (~2% industry rate)

Digital channels and transparency

E-commerce and social platforms expose real-time prices and reviews, empowering buyers and compressing margins via flash sales and cross-border sites; Transsion has rolled out D2C pilots and controlled marketplace stores in 2024 to protect pricing integrity while using influencer marketing and community engagement to sustain demand at target ASPs.

- 2024 D2C pilots: deployed in Nigeria and India

- Controlled stores: used to limit price dispersion

- Influencer push: supports ASP retention

Sub-$150 demand and Android parity intensify pricing pressure; D2C pilots defend ARPUs

Emerging-market buyers drive sub-$150 ASPs, amplifying price pressure despite Transsion’s ~54% Africa smartphone share in 2024; small feature gaps spur switching so ARPUs remain low. Android parity (~72% global share in 2024) and marketplaces make switching easy; Transsion uses HiOS/XOS, trade-ins and D2C pilots (Nigeria, India 2024) to defend pricing. Carlcare after-sales and ~2% industry return rates limit churn.

| Metric | Value (2023–24) |

|---|---|

| Africa share | ~54% (2024) |

| ASP | <$150 |

| Android share | ~72% (2024) |

| Return rate | ~2% |

| D2C pilots | Nigeria, India (2024) |

Preview Before You Purchase

Shenzhen Transsion Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Shenzhen Transsion Holding evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic positioning and risks; it highlights mobile device market dynamics, distribution strengths, and pricing pressures. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

From Overview to Strategy Blueprint

Shenzhen Transsion Holding faces intense rivalry from global smartphone makers, rising buyer power in emerging markets, and supplier concentration risks for key components, while low switching costs and nascent substitutes pressure margins. This snapshot highlights strategic vulnerabilities and growth levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated chipset sources

Smartphone SoCs are concentrated among a few vendors—MediaTek (≈45% shipments in 2024) and Qualcomm (≈30%)—giving upstream bargaining power. Transsion offsets this via volume commitments and platform reuse across Tecno, Itel and Infinix. Roadmap or pricing shifts at a key chipmaker can raise costs and delay launches. Diversifying into multiple SKUs per chipset generation reduces dependency risk.

Display and memory volatility

Panels and NAND/DRAM supply cycles drive price swings that suppliers pass through, with display+memory representing ≈30% of a smartphone BOM in 2024. Transsion’s scale in emerging markets (≈40% smartphone share in Africa) gives it some leverage, but premium suppliers still prioritize larger global OEMs. Long-term agreements and second-sourcing temper spikes yet cannot fully neutralize tight-cycle pricing. Engineering for component interchangeability helps sustain margins.

EMS/ODM and manufacturing partners

Reliance on EMS/ODM partners like Wingtech for cost-efficient assembly creates coordination dependence, with standardized Transsion designs enabling faster capacity switches but line requalification and yield learning often taking 2–6 weeks and causing friction. EMS players frequently run >85–90% utilization in peak quarters, giving suppliers leverage during demand surges. Co-locating procurement, NPI, and QA shortens ramp times and materially reduces switching pain.

Logistics and local service networks

Shipping into Africa, South Asia and LATAM needs freight, customs brokers and local last-mile partners; capacity or regulatory delays can give these intermediaries pricing power, but Transsion’s Carlcare after-sales network (over 1,000 service points in Africa by 2024) and established channels generate repeat business that mitigates supplier leverage.

- Local expertise crucial

- Regulatory delays = pricing power

- Carlcare >1,000 points (2024)

- Multi-country tenders improve terms ~15%

Currency and geopolitical exposure

Inputs for Transsion are largely USD-denominated while many sales are in local currencies, so FX stress amplifies supplier leverage and can force higher local costs; sanctions and export controls have periodically limited access to certain components, raising replacement and lead-time risks. Hedging and staggered purchasing mitigate some exposure but suppliers still extract prepayments or tighter terms, while localized sourcing reduces vulnerability.

- USD invoicing vs local revenues increases FX pass-through risk

- Sanctions/export controls limit component access and raise sourcing costs

- Hedging/staggered buys reduce but do not eliminate supplier leverage

- Localized sourcing lowers geopolitical exposure

SoC concentration boosts supplier leverage; display+memory ~30% BOM forces pass-through

Key chip supply is concentrated (MediaTek ≈45% shipments, Qualcomm ≈30% in 2024), giving upstream leverage; Transsion offsets with platform reuse and volume commitments. Display+NAND/DRAM ≈30% of BOM; panel/memory cycles drive cost pass-through despite Transsion’s ≈40% AFR smartphone share. EMS utilization >85–90% and Carlcare >1,000 Africa points (2024) create operational dependencies; hedging and multi-country tenders trim but do not remove supplier power.

| Item | 2024 Metric |

|---|---|

| SoC concentration | MediaTek ~45%, Qualcomm ~30% |

| Display+Memory BOM | ~30% |

| Africa market share | ~40% |

| EMS peak util. | >85–90% |

| Carlcare points | >1,000 |

What is included in the product

Tailored exclusively for Shenzhen Transsion Holding, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers, and disruptive substitutes shaping pricing, profitability and market share dynamics.

A concise, one-sheet Porter's Five Forces for Shenzhen Transsion Holding—instantly highlights supplier, buyer, entrant, substitute and competitive rivalry pressures to guide rapid strategic decisions and slide-ready recommendations.

Customers Bargaining Power

Highly price-sensitive consumers

Emerging-market buyers are extremely value-driven, amplifying price pressure and contributing to sub-$150 average selling prices in many African and South Asian markets; Transsion holds over 40% smartphone share in Africa, intensifying competition. Small feature gaps trigger switching, keeping ARPUs depressed. Transsion counters with aggressive pricing and localized specs—long battery life, multi-SIM—and uses bundled offers and financing to soften price elasticity.

Powerful retail and distributor channels

Independent retailers, wholesalers and carriers across Africa and South Asia control shelf space and can switch brands, forcing rebates and extended credit; Transsion faced this dynamic despite holding roughly 54% of African smartphone shipments in 2024. Transsion’s deep channel relationships and broad distribution network secure favorable positioning. Aggressive sell-out support and retailer training increase partner stickiness and reduce switching.

Low switching costs

Android ecosystem parity (Android ~72% global share in 2024, StatCounter) and frequent promotions make switching nearly frictionless, letting buyers compare specs and prices instantly on online marketplaces. Transsion raises perceived switching costs with localized UX (HiOS/XOS) and expansive after-sales support across key markets. Trade-in programs further increase retention by offering cash discounts and upgrade paths.

After-sales expectations

Reliability and fast turnaround drive Transsion repeat purchases; global smartphone return rates ran about 2% in 2023–24, so timely service directly limits churn. Customers demand affordable repairs and spare parts; shortages amplify buyer power via negative word-of-mouth. Carlcare’s broad service network reduces escalation and raises trust, while transparent warranty terms curb return pressure.

- after-sales reliability: decisive for repeat buys

- repair/spares affordability: reduces buyer bargaining

- Carlcare network: lowers complaint escalation

- warranty transparency: limits returns (~2% industry rate)

Digital channels and transparency

E-commerce and social platforms expose real-time prices and reviews, empowering buyers and compressing margins via flash sales and cross-border sites; Transsion has rolled out D2C pilots and controlled marketplace stores in 2024 to protect pricing integrity while using influencer marketing and community engagement to sustain demand at target ASPs.

- 2024 D2C pilots: deployed in Nigeria and India

- Controlled stores: used to limit price dispersion

- Influencer push: supports ASP retention

Sub-$150 demand and Android parity intensify pricing pressure; D2C pilots defend ARPUs

Emerging-market buyers drive sub-$150 ASPs, amplifying price pressure despite Transsion’s ~54% Africa smartphone share in 2024; small feature gaps spur switching so ARPUs remain low. Android parity (~72% global share in 2024) and marketplaces make switching easy; Transsion uses HiOS/XOS, trade-ins and D2C pilots (Nigeria, India 2024) to defend pricing. Carlcare after-sales and ~2% industry return rates limit churn.

| Metric | Value (2023–24) |

|---|---|

| Africa share | ~54% (2024) |

| ASP | <$150 |

| Android share | ~72% (2024) |

| Return rate | ~2% |

| D2C pilots | Nigeria, India (2024) |

Preview Before You Purchase

Shenzhen Transsion Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Shenzhen Transsion Holding evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic positioning and risks; it highlights mobile device market dynamics, distribution strengths, and pricing pressures. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Description

From Overview to Strategy Blueprint

Shenzhen Transsion Holding faces intense rivalry from global smartphone makers, rising buyer power in emerging markets, and supplier concentration risks for key components, while low switching costs and nascent substitutes pressure margins. This snapshot highlights strategic vulnerabilities and growth levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated chipset sources

Smartphone SoCs are concentrated among a few vendors—MediaTek (≈45% shipments in 2024) and Qualcomm (≈30%)—giving upstream bargaining power. Transsion offsets this via volume commitments and platform reuse across Tecno, Itel and Infinix. Roadmap or pricing shifts at a key chipmaker can raise costs and delay launches. Diversifying into multiple SKUs per chipset generation reduces dependency risk.

Display and memory volatility

Panels and NAND/DRAM supply cycles drive price swings that suppliers pass through, with display+memory representing ≈30% of a smartphone BOM in 2024. Transsion’s scale in emerging markets (≈40% smartphone share in Africa) gives it some leverage, but premium suppliers still prioritize larger global OEMs. Long-term agreements and second-sourcing temper spikes yet cannot fully neutralize tight-cycle pricing. Engineering for component interchangeability helps sustain margins.

EMS/ODM and manufacturing partners

Reliance on EMS/ODM partners like Wingtech for cost-efficient assembly creates coordination dependence, with standardized Transsion designs enabling faster capacity switches but line requalification and yield learning often taking 2–6 weeks and causing friction. EMS players frequently run >85–90% utilization in peak quarters, giving suppliers leverage during demand surges. Co-locating procurement, NPI, and QA shortens ramp times and materially reduces switching pain.

Logistics and local service networks

Shipping into Africa, South Asia and LATAM needs freight, customs brokers and local last-mile partners; capacity or regulatory delays can give these intermediaries pricing power, but Transsion’s Carlcare after-sales network (over 1,000 service points in Africa by 2024) and established channels generate repeat business that mitigates supplier leverage.

- Local expertise crucial

- Regulatory delays = pricing power

- Carlcare >1,000 points (2024)

- Multi-country tenders improve terms ~15%

Currency and geopolitical exposure

Inputs for Transsion are largely USD-denominated while many sales are in local currencies, so FX stress amplifies supplier leverage and can force higher local costs; sanctions and export controls have periodically limited access to certain components, raising replacement and lead-time risks. Hedging and staggered purchasing mitigate some exposure but suppliers still extract prepayments or tighter terms, while localized sourcing reduces vulnerability.

- USD invoicing vs local revenues increases FX pass-through risk

- Sanctions/export controls limit component access and raise sourcing costs

- Hedging/staggered buys reduce but do not eliminate supplier leverage

- Localized sourcing lowers geopolitical exposure

SoC concentration boosts supplier leverage; display+memory ~30% BOM forces pass-through

Key chip supply is concentrated (MediaTek ≈45% shipments, Qualcomm ≈30% in 2024), giving upstream leverage; Transsion offsets with platform reuse and volume commitments. Display+NAND/DRAM ≈30% of BOM; panel/memory cycles drive cost pass-through despite Transsion’s ≈40% AFR smartphone share. EMS utilization >85–90% and Carlcare >1,000 Africa points (2024) create operational dependencies; hedging and multi-country tenders trim but do not remove supplier power.

| Item | 2024 Metric |

|---|---|

| SoC concentration | MediaTek ~45%, Qualcomm ~30% |

| Display+Memory BOM | ~30% |

| Africa market share | ~40% |

| EMS peak util. | >85–90% |

| Carlcare points | >1,000 |

What is included in the product

Tailored exclusively for Shenzhen Transsion Holding, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers, and disruptive substitutes shaping pricing, profitability and market share dynamics.

A concise, one-sheet Porter's Five Forces for Shenzhen Transsion Holding—instantly highlights supplier, buyer, entrant, substitute and competitive rivalry pressures to guide rapid strategic decisions and slide-ready recommendations.

Customers Bargaining Power

Highly price-sensitive consumers

Emerging-market buyers are extremely value-driven, amplifying price pressure and contributing to sub-$150 average selling prices in many African and South Asian markets; Transsion holds over 40% smartphone share in Africa, intensifying competition. Small feature gaps trigger switching, keeping ARPUs depressed. Transsion counters with aggressive pricing and localized specs—long battery life, multi-SIM—and uses bundled offers and financing to soften price elasticity.

Powerful retail and distributor channels

Independent retailers, wholesalers and carriers across Africa and South Asia control shelf space and can switch brands, forcing rebates and extended credit; Transsion faced this dynamic despite holding roughly 54% of African smartphone shipments in 2024. Transsion’s deep channel relationships and broad distribution network secure favorable positioning. Aggressive sell-out support and retailer training increase partner stickiness and reduce switching.

Low switching costs

Android ecosystem parity (Android ~72% global share in 2024, StatCounter) and frequent promotions make switching nearly frictionless, letting buyers compare specs and prices instantly on online marketplaces. Transsion raises perceived switching costs with localized UX (HiOS/XOS) and expansive after-sales support across key markets. Trade-in programs further increase retention by offering cash discounts and upgrade paths.

After-sales expectations

Reliability and fast turnaround drive Transsion repeat purchases; global smartphone return rates ran about 2% in 2023–24, so timely service directly limits churn. Customers demand affordable repairs and spare parts; shortages amplify buyer power via negative word-of-mouth. Carlcare’s broad service network reduces escalation and raises trust, while transparent warranty terms curb return pressure.

- after-sales reliability: decisive for repeat buys

- repair/spares affordability: reduces buyer bargaining

- Carlcare network: lowers complaint escalation

- warranty transparency: limits returns (~2% industry rate)

Digital channels and transparency

E-commerce and social platforms expose real-time prices and reviews, empowering buyers and compressing margins via flash sales and cross-border sites; Transsion has rolled out D2C pilots and controlled marketplace stores in 2024 to protect pricing integrity while using influencer marketing and community engagement to sustain demand at target ASPs.

- 2024 D2C pilots: deployed in Nigeria and India

- Controlled stores: used to limit price dispersion

- Influencer push: supports ASP retention

Sub-$150 demand and Android parity intensify pricing pressure; D2C pilots defend ARPUs

Emerging-market buyers drive sub-$150 ASPs, amplifying price pressure despite Transsion’s ~54% Africa smartphone share in 2024; small feature gaps spur switching so ARPUs remain low. Android parity (~72% global share in 2024) and marketplaces make switching easy; Transsion uses HiOS/XOS, trade-ins and D2C pilots (Nigeria, India 2024) to defend pricing. Carlcare after-sales and ~2% industry return rates limit churn.

| Metric | Value (2023–24) |

|---|---|

| Africa share | ~54% (2024) |

| ASP | <$150 |

| Android share | ~72% (2024) |

| Return rate | ~2% |

| D2C pilots | Nigeria, India (2024) |

Preview Before You Purchase

Shenzhen Transsion Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Shenzhen Transsion Holding evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic positioning and risks; it highlights mobile device market dynamics, distribution strengths, and pricing pressures. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.