TransUnion Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

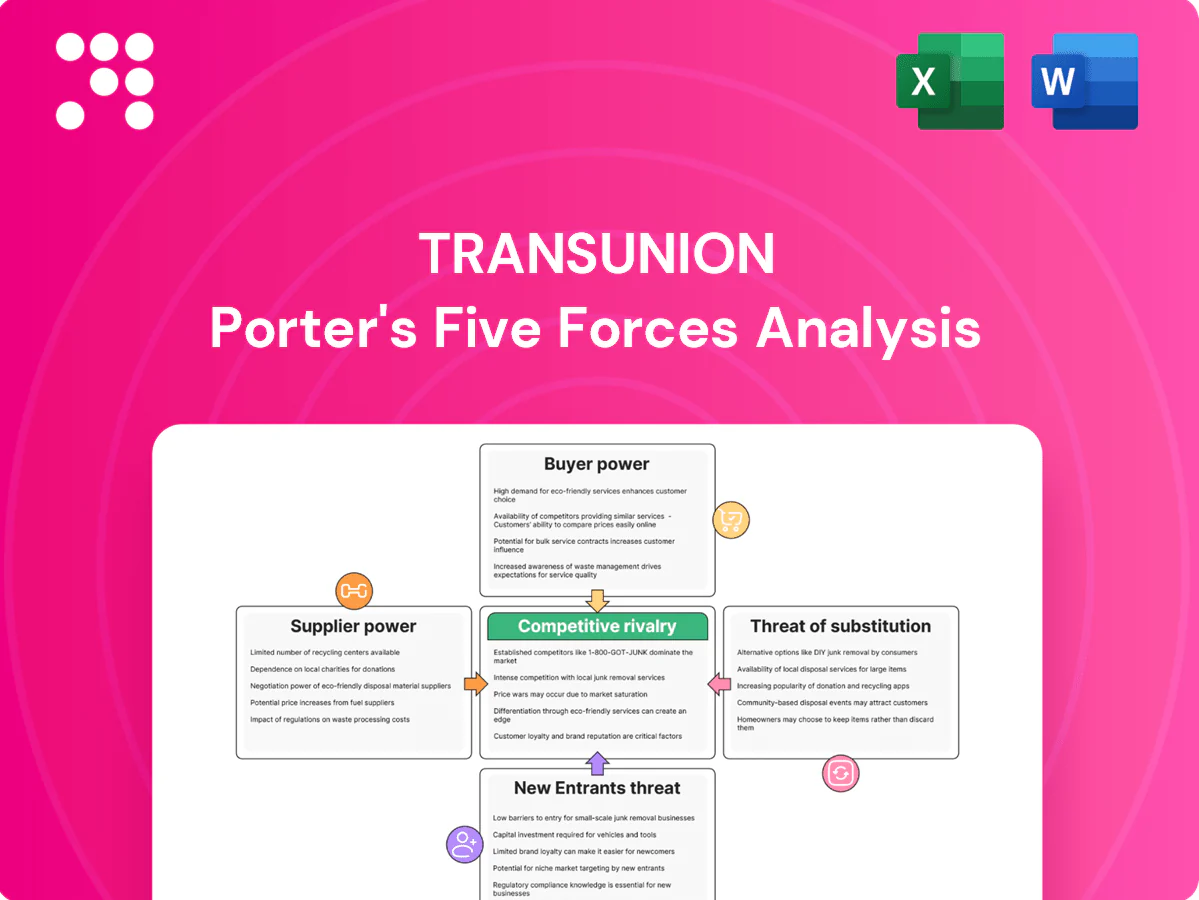

TransUnion faces moderate buyer power, high competitive rivalry from fintech and credit bureaus, and disruptive substitute risks from alternative data and identity platforms, while regulatory and supplier pressures shape margins; strategic positioning and data assets offer resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated data furnishers

Credit file depth depends on large banks, lenders, telcos and public agencies that furnish data; these suppliers are relatively concentrated and thus hold negotiation leverage over data use and reciprocity. TransUnion operates in 30+ countries and works with thousands of lenders, giving furnishers access but also dependence on TU’s distribution reach and compliance infrastructure. Multi-bureau furnishing norms materially reduce single-supplier hold-up risk.

Alternative data sources

Utilities, rental, BNPL and device/identity alternative data providers broaden TransUnions coverage but can control access terms and refresh rates, tightening supplier bargaining power; TransUnion reported FY2024 revenue of approximately $5.27 billion, underscoring reliance on diverse data inputs to sustain growth.

Scarcity of high-signal alt-data strengthens supplier leverage, which TransUnion counters through strategic partnerships, negotiating exclusivity where feasible, building proprietary networks and diversifying sources to reduce single-supplier dependency.

Cloud and tech stack vendors

Reliance on major cloud, analytics and cybersecurity providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024 cloud market share) creates switching costs and vendor bargaining power; pricing or SLA changes can compress margins and threaten uptime. TransUnion mitigates risk via multi-cloud deployment (92% of enterprises use multi-cloud in 2024), long-term contracts and in-house tooling. Regulatory moves such as DORA (effective 2025) push stricter SLAs and third-party resilience.

Public records and government feeds

Access to courts, motor vehicle, sanctions, and identity registries is essential and heavily regulated; agencies can change access rules, formats, or fees and thereby exert structural supplier power. As of 2024 TransUnion operates in 30+ countries and maintains compliance and ingestion pipelines to adapt quickly, while geographic diversification reduces exposure to any single authority.

- 30+ countries — geographic spread

- Regulatory control — access, format, fees

- Compliance pipelines — rapid adaptation

Data quality and timeliness

Supplier power rises when contributors control timeliness and cleanliness of the feeds that drive model accuracy; TransUnion aggregates data on over 1 billion consumers across 30+ markets, so stale or incomplete inputs can materially degrade scoring and force commercial concessions.

- Quality scorecards + feedback loops tied to value exchange

- Contractual SLAs and performance incentives

- Stale feeds risk higher dispute rates and model drift

Concentrated credit feeds give suppliers leverage; multi-cloud and partnerships mitigate risk

Large banks, telcos and public registries (30+ countries) supply critical credit and identity feeds, giving concentrated suppliers leverage over access, formats and fees. TransUnion (FY2024 revenue $5.27B; >1B consumer records) mitigates via diversification, SLAs, partnerships and multi-cloud. Scarce high-signal alt-data and major cloud vendors increase switching costs and supplier bargaining power.

| Metric | Value |

|---|---|

| Countries | 30+ |

| FY2024 revenue | $5.27B |

| Consumer records | >1B |

| AWS market share (2024) | ~32% |

What is included in the product

Tailored Porter's Five Forces analysis for TransUnion uncovering competitive intensity, buyer/supplier power, substitute threats, new-entrant barriers, and disruptive forces shaping its pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for TransUnion—visualize competitive pressure with an editable radar chart, customize inputs for evolving risks and regulations, and export a clean slide-ready summary to accelerate strategic decisions.

Customers Bargaining Power

Large enterprise RFP leverage

Major banks, insurers, telcos and fintechs procure multi-bureau solutions via competitive RFPs, leveraging scale to extract volume discounts, pilots and bundled pricing; enterprise deals drove a large share of TransUnion’s 2024 revenue of $3.08 billion. TransUnion defends price through superior accuracy, data coverage and seamless integration into client workflows. Long, embedded contracts and workflow integrations materially reduce churn risk and raise switching costs.

Multi-bureau switching options

Buyers can switch or dual-source among the three major bureaus — TransUnion, Equifax, and Experian — which materially enhances customer bargaining power. Interchangeable credit pulls are highly price-sensitive in commoditized use cases, pushing volume-based pricing pressure. Differentiated analytics and identity products reduce direct comparability and sustain premium pricing for advanced services. Deep API integration and compliance tooling raise effective switching costs for enterprise clients.

Regulatory and compliance needs

Highly regulated buyers demand auditability, dispute workflows and fair-lending support, pushing purchasing beyond pure price and preserving TransUnion pricing power. TransUnion reported fiscal 2024 revenue of about $4.4 billion, letting it emphasize compliance-driven value and risk reduction in negotiations. Buyers still press for indemnities and tight SLAs, but framing offerings around compliance helps TransUnion defend margin.

Consumer segment sensitivity

Individual consumers are highly fragmented and have low negotiating power; TransUnion reports serving over 1 billion consumers globally, while regulators such as the CFPB and GDPR limit fees and certain reporting practices. Upsell to monitoring, identity protection and restoration faces price anchoring from free credit-score offerings by competitors. UX, timeliness of alerts and breach response quality materially drive perceived value, and partnerships with banks and employers extend distribution.

- Consumers: fragmented, low bargaining power

- Regulation: CFPB/GDPR caps on fees/practices

- Competition: free score offerings anchor price

- Value drivers: UX, alerts, breach response

- Distribution: bank/employer partnerships

Integration and workflow lock-in

Embedded TransUnion scores, IDs and fraud signals sit inside underwriting and onboarding stacks, making replacement costly due to downtime, revalidation and model drift; this integration materially reduces buyer power. TransUnion deepens lock-in via SDKs, case-management and decisioning platforms, while outcome-based pricing (used with large lenders and fintechs) aligns incentives and limits price erosion. As of 2024 TransUnion serves >60,000 business clients and profiles ~1 billion consumers, reinforcing stickiness.

- Integration risk: high — downtime/revalidation costs

- Products: SDKs, case management, decisioning

- Pricing: outcome-based — mitigates discount pressure

- Scale: >60,000 clients; ~1B consumer profiles (2024)

Enterprise buyers push discounts; major bureau holds pricing with superior data and long contracts

Large enterprise buyers wield bargaining power via RFPs and multi-bureau sourcing, pressuring volume discounts, yet TransUnion defends pricing with superior data, long contracts and integrated workflows; 2024 revenue ~$4.4B, >60,000 business clients and ~1B consumer profiles increase stickiness. Commodity credit pulls remain price-sensitive among the three major bureaus, but compliance and advanced analytics sustain premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | $4.4B | Negotiation leverage |

| Business clients | >60,000 | High integration |

| Consumer profiles | ~1B | Switching cost |

| Major bureaus | 3 | Price competition |

Preview Before You Purchase

TransUnion Porter's Five Forces Analysis

This preview shows the exact TransUnion Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the final, fully formatted analysis, ready to download and use the moment you buy. You're viewing the identical file that will be delivered instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

TransUnion faces moderate buyer power, high competitive rivalry from fintech and credit bureaus, and disruptive substitute risks from alternative data and identity platforms, while regulatory and supplier pressures shape margins; strategic positioning and data assets offer resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated data furnishers

Credit file depth depends on large banks, lenders, telcos and public agencies that furnish data; these suppliers are relatively concentrated and thus hold negotiation leverage over data use and reciprocity. TransUnion operates in 30+ countries and works with thousands of lenders, giving furnishers access but also dependence on TU’s distribution reach and compliance infrastructure. Multi-bureau furnishing norms materially reduce single-supplier hold-up risk.

Alternative data sources

Utilities, rental, BNPL and device/identity alternative data providers broaden TransUnions coverage but can control access terms and refresh rates, tightening supplier bargaining power; TransUnion reported FY2024 revenue of approximately $5.27 billion, underscoring reliance on diverse data inputs to sustain growth.

Scarcity of high-signal alt-data strengthens supplier leverage, which TransUnion counters through strategic partnerships, negotiating exclusivity where feasible, building proprietary networks and diversifying sources to reduce single-supplier dependency.

Cloud and tech stack vendors

Reliance on major cloud, analytics and cybersecurity providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024 cloud market share) creates switching costs and vendor bargaining power; pricing or SLA changes can compress margins and threaten uptime. TransUnion mitigates risk via multi-cloud deployment (92% of enterprises use multi-cloud in 2024), long-term contracts and in-house tooling. Regulatory moves such as DORA (effective 2025) push stricter SLAs and third-party resilience.

Public records and government feeds

Access to courts, motor vehicle, sanctions, and identity registries is essential and heavily regulated; agencies can change access rules, formats, or fees and thereby exert structural supplier power. As of 2024 TransUnion operates in 30+ countries and maintains compliance and ingestion pipelines to adapt quickly, while geographic diversification reduces exposure to any single authority.

- 30+ countries — geographic spread

- Regulatory control — access, format, fees

- Compliance pipelines — rapid adaptation

Data quality and timeliness

Supplier power rises when contributors control timeliness and cleanliness of the feeds that drive model accuracy; TransUnion aggregates data on over 1 billion consumers across 30+ markets, so stale or incomplete inputs can materially degrade scoring and force commercial concessions.

- Quality scorecards + feedback loops tied to value exchange

- Contractual SLAs and performance incentives

- Stale feeds risk higher dispute rates and model drift

Concentrated credit feeds give suppliers leverage; multi-cloud and partnerships mitigate risk

Large banks, telcos and public registries (30+ countries) supply critical credit and identity feeds, giving concentrated suppliers leverage over access, formats and fees. TransUnion (FY2024 revenue $5.27B; >1B consumer records) mitigates via diversification, SLAs, partnerships and multi-cloud. Scarce high-signal alt-data and major cloud vendors increase switching costs and supplier bargaining power.

| Metric | Value |

|---|---|

| Countries | 30+ |

| FY2024 revenue | $5.27B |

| Consumer records | >1B |

| AWS market share (2024) | ~32% |

What is included in the product

Tailored Porter's Five Forces analysis for TransUnion uncovering competitive intensity, buyer/supplier power, substitute threats, new-entrant barriers, and disruptive forces shaping its pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for TransUnion—visualize competitive pressure with an editable radar chart, customize inputs for evolving risks and regulations, and export a clean slide-ready summary to accelerate strategic decisions.

Customers Bargaining Power

Large enterprise RFP leverage

Major banks, insurers, telcos and fintechs procure multi-bureau solutions via competitive RFPs, leveraging scale to extract volume discounts, pilots and bundled pricing; enterprise deals drove a large share of TransUnion’s 2024 revenue of $3.08 billion. TransUnion defends price through superior accuracy, data coverage and seamless integration into client workflows. Long, embedded contracts and workflow integrations materially reduce churn risk and raise switching costs.

Multi-bureau switching options

Buyers can switch or dual-source among the three major bureaus — TransUnion, Equifax, and Experian — which materially enhances customer bargaining power. Interchangeable credit pulls are highly price-sensitive in commoditized use cases, pushing volume-based pricing pressure. Differentiated analytics and identity products reduce direct comparability and sustain premium pricing for advanced services. Deep API integration and compliance tooling raise effective switching costs for enterprise clients.

Regulatory and compliance needs

Highly regulated buyers demand auditability, dispute workflows and fair-lending support, pushing purchasing beyond pure price and preserving TransUnion pricing power. TransUnion reported fiscal 2024 revenue of about $4.4 billion, letting it emphasize compliance-driven value and risk reduction in negotiations. Buyers still press for indemnities and tight SLAs, but framing offerings around compliance helps TransUnion defend margin.

Consumer segment sensitivity

Individual consumers are highly fragmented and have low negotiating power; TransUnion reports serving over 1 billion consumers globally, while regulators such as the CFPB and GDPR limit fees and certain reporting practices. Upsell to monitoring, identity protection and restoration faces price anchoring from free credit-score offerings by competitors. UX, timeliness of alerts and breach response quality materially drive perceived value, and partnerships with banks and employers extend distribution.

- Consumers: fragmented, low bargaining power

- Regulation: CFPB/GDPR caps on fees/practices

- Competition: free score offerings anchor price

- Value drivers: UX, alerts, breach response

- Distribution: bank/employer partnerships

Integration and workflow lock-in

Embedded TransUnion scores, IDs and fraud signals sit inside underwriting and onboarding stacks, making replacement costly due to downtime, revalidation and model drift; this integration materially reduces buyer power. TransUnion deepens lock-in via SDKs, case-management and decisioning platforms, while outcome-based pricing (used with large lenders and fintechs) aligns incentives and limits price erosion. As of 2024 TransUnion serves >60,000 business clients and profiles ~1 billion consumers, reinforcing stickiness.

- Integration risk: high — downtime/revalidation costs

- Products: SDKs, case management, decisioning

- Pricing: outcome-based — mitigates discount pressure

- Scale: >60,000 clients; ~1B consumer profiles (2024)

Enterprise buyers push discounts; major bureau holds pricing with superior data and long contracts

Large enterprise buyers wield bargaining power via RFPs and multi-bureau sourcing, pressuring volume discounts, yet TransUnion defends pricing with superior data, long contracts and integrated workflows; 2024 revenue ~$4.4B, >60,000 business clients and ~1B consumer profiles increase stickiness. Commodity credit pulls remain price-sensitive among the three major bureaus, but compliance and advanced analytics sustain premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | $4.4B | Negotiation leverage |

| Business clients | >60,000 | High integration |

| Consumer profiles | ~1B | Switching cost |

| Major bureaus | 3 | Price competition |

Preview Before You Purchase

TransUnion Porter's Five Forces Analysis

This preview shows the exact TransUnion Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the final, fully formatted analysis, ready to download and use the moment you buy. You're viewing the identical file that will be delivered instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

TransUnion faces moderate buyer power, high competitive rivalry from fintech and credit bureaus, and disruptive substitute risks from alternative data and identity platforms, while regulatory and supplier pressures shape margins; strategic positioning and data assets offer resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated data furnishers

Credit file depth depends on large banks, lenders, telcos and public agencies that furnish data; these suppliers are relatively concentrated and thus hold negotiation leverage over data use and reciprocity. TransUnion operates in 30+ countries and works with thousands of lenders, giving furnishers access but also dependence on TU’s distribution reach and compliance infrastructure. Multi-bureau furnishing norms materially reduce single-supplier hold-up risk.

Alternative data sources

Utilities, rental, BNPL and device/identity alternative data providers broaden TransUnions coverage but can control access terms and refresh rates, tightening supplier bargaining power; TransUnion reported FY2024 revenue of approximately $5.27 billion, underscoring reliance on diverse data inputs to sustain growth.

Scarcity of high-signal alt-data strengthens supplier leverage, which TransUnion counters through strategic partnerships, negotiating exclusivity where feasible, building proprietary networks and diversifying sources to reduce single-supplier dependency.

Cloud and tech stack vendors

Reliance on major cloud, analytics and cybersecurity providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024 cloud market share) creates switching costs and vendor bargaining power; pricing or SLA changes can compress margins and threaten uptime. TransUnion mitigates risk via multi-cloud deployment (92% of enterprises use multi-cloud in 2024), long-term contracts and in-house tooling. Regulatory moves such as DORA (effective 2025) push stricter SLAs and third-party resilience.

Public records and government feeds

Access to courts, motor vehicle, sanctions, and identity registries is essential and heavily regulated; agencies can change access rules, formats, or fees and thereby exert structural supplier power. As of 2024 TransUnion operates in 30+ countries and maintains compliance and ingestion pipelines to adapt quickly, while geographic diversification reduces exposure to any single authority.

- 30+ countries — geographic spread

- Regulatory control — access, format, fees

- Compliance pipelines — rapid adaptation

Data quality and timeliness

Supplier power rises when contributors control timeliness and cleanliness of the feeds that drive model accuracy; TransUnion aggregates data on over 1 billion consumers across 30+ markets, so stale or incomplete inputs can materially degrade scoring and force commercial concessions.

- Quality scorecards + feedback loops tied to value exchange

- Contractual SLAs and performance incentives

- Stale feeds risk higher dispute rates and model drift

Concentrated credit feeds give suppliers leverage; multi-cloud and partnerships mitigate risk

Large banks, telcos and public registries (30+ countries) supply critical credit and identity feeds, giving concentrated suppliers leverage over access, formats and fees. TransUnion (FY2024 revenue $5.27B; >1B consumer records) mitigates via diversification, SLAs, partnerships and multi-cloud. Scarce high-signal alt-data and major cloud vendors increase switching costs and supplier bargaining power.

| Metric | Value |

|---|---|

| Countries | 30+ |

| FY2024 revenue | $5.27B |

| Consumer records | >1B |

| AWS market share (2024) | ~32% |

What is included in the product

Tailored Porter's Five Forces analysis for TransUnion uncovering competitive intensity, buyer/supplier power, substitute threats, new-entrant barriers, and disruptive forces shaping its pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for TransUnion—visualize competitive pressure with an editable radar chart, customize inputs for evolving risks and regulations, and export a clean slide-ready summary to accelerate strategic decisions.

Customers Bargaining Power

Large enterprise RFP leverage

Major banks, insurers, telcos and fintechs procure multi-bureau solutions via competitive RFPs, leveraging scale to extract volume discounts, pilots and bundled pricing; enterprise deals drove a large share of TransUnion’s 2024 revenue of $3.08 billion. TransUnion defends price through superior accuracy, data coverage and seamless integration into client workflows. Long, embedded contracts and workflow integrations materially reduce churn risk and raise switching costs.

Multi-bureau switching options

Buyers can switch or dual-source among the three major bureaus — TransUnion, Equifax, and Experian — which materially enhances customer bargaining power. Interchangeable credit pulls are highly price-sensitive in commoditized use cases, pushing volume-based pricing pressure. Differentiated analytics and identity products reduce direct comparability and sustain premium pricing for advanced services. Deep API integration and compliance tooling raise effective switching costs for enterprise clients.

Regulatory and compliance needs

Highly regulated buyers demand auditability, dispute workflows and fair-lending support, pushing purchasing beyond pure price and preserving TransUnion pricing power. TransUnion reported fiscal 2024 revenue of about $4.4 billion, letting it emphasize compliance-driven value and risk reduction in negotiations. Buyers still press for indemnities and tight SLAs, but framing offerings around compliance helps TransUnion defend margin.

Consumer segment sensitivity

Individual consumers are highly fragmented and have low negotiating power; TransUnion reports serving over 1 billion consumers globally, while regulators such as the CFPB and GDPR limit fees and certain reporting practices. Upsell to monitoring, identity protection and restoration faces price anchoring from free credit-score offerings by competitors. UX, timeliness of alerts and breach response quality materially drive perceived value, and partnerships with banks and employers extend distribution.

- Consumers: fragmented, low bargaining power

- Regulation: CFPB/GDPR caps on fees/practices

- Competition: free score offerings anchor price

- Value drivers: UX, alerts, breach response

- Distribution: bank/employer partnerships

Integration and workflow lock-in

Embedded TransUnion scores, IDs and fraud signals sit inside underwriting and onboarding stacks, making replacement costly due to downtime, revalidation and model drift; this integration materially reduces buyer power. TransUnion deepens lock-in via SDKs, case-management and decisioning platforms, while outcome-based pricing (used with large lenders and fintechs) aligns incentives and limits price erosion. As of 2024 TransUnion serves >60,000 business clients and profiles ~1 billion consumers, reinforcing stickiness.

- Integration risk: high — downtime/revalidation costs

- Products: SDKs, case management, decisioning

- Pricing: outcome-based — mitigates discount pressure

- Scale: >60,000 clients; ~1B consumer profiles (2024)

Enterprise buyers push discounts; major bureau holds pricing with superior data and long contracts

Large enterprise buyers wield bargaining power via RFPs and multi-bureau sourcing, pressuring volume discounts, yet TransUnion defends pricing with superior data, long contracts and integrated workflows; 2024 revenue ~$4.4B, >60,000 business clients and ~1B consumer profiles increase stickiness. Commodity credit pulls remain price-sensitive among the three major bureaus, but compliance and advanced analytics sustain premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | $4.4B | Negotiation leverage |

| Business clients | >60,000 | High integration |

| Consumer profiles | ~1B | Switching cost |

| Major bureaus | 3 | Price competition |

Preview Before You Purchase

TransUnion Porter's Five Forces Analysis

This preview shows the exact TransUnion Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the final, fully formatted analysis, ready to download and use the moment you buy. You're viewing the identical file that will be delivered instantly upon payment.