Trifast Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Trifast faces moderate supplier power, niche customer leverage, steady rivalry, limited substitute threats and manageable entry barriers, shaping a cautiously optimistic outlook for growth and margin resilience. This Porter's Five Forces snapshot highlights where strategic focus can mitigate risks and capture opportunity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Trifast’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity steel and alloy dependence

TR Fastenings' reliance on carbon steel, stainless and specialty alloys exposes it to raw-material price volatility, heightened in 2024 by supply-chain tightness across mills. Upstream consolidation in steel producers has compressed availability and enabled rapid cost pass-through to buyers. Hedging and multi-sourcing reduce but do not eliminate exposure, while customer-approved material specs restrict substitution and bargaining flexibility.

Fragmented component suppliers

Many tooling, plating and secondary-process suppliers remain regionally fragmented, limiting individual supplier leverage but increasing coordination and logistics costs. In 2024 Trifast and peers accelerated Vendor Managed Inventory and supplier development programs to standardize lead-times and quality. Dual-qualification of components is widely used to preserve continuity and mitigate single-source risk.

Quality and certification requirements

Automotive and electronics end-markets mandate IATF 16949, ISO certifications, PPAP submissions and full traceability, making certification a gating factor for Trifast suppliers. Approved vendor lists concentrate spend among qualified suppliers and raise switching frictions, increasing supplier bargaining power. Failures carry high recall and warranty exposure that can run into hundreds of millions to billions, reinforcing reliance on trusted sources. Long audit cycles, commonly 6–12 months in 2024, slow onboarding of alternatives.

Specialized tooling and dies

Specialized cold-heading and thread-forming rely on custom tooling with lead times typically 4–12 weeks, giving niche toolmakers leverage to command premiums and rush fees often up to 30% in 2024. Tool wear and scheduled maintenance create recurring capital and service spend commonly representing 5–12% of manufacturing operating costs annually. In-house tooling design reduces exposure but does not eliminate dependency on skilled toolmakers.

- Lead times: 4–12 weeks

- Rush fees/premiums: up to 30%

- Ongoing tooling spend: 5–12% of ops costs

- In-house design lowers but does not remove supplier dependency

Logistics and geopolitical exposure

- Freight volatility: Drewry WCI down ~75% vs 2021

- Supplier leverage: capacity squeezes in Asia/Eastern Europe

- Mitigation: nearshoring and safety stock ↑ working capital

- Hedging: long-term indexed contracts share pricing risk

Supplier power moderate-high: steel concentration, 4-12 week tooling, rush premiums 30%

Supplier power is moderate-high: raw-material concentration in steel and alloys plus certification gating give suppliers pricing power and switching friction in 2024. Tooling lead-times (4–12 weeks) and rush premiums (up to 30%) add cost and risk. Freight volatility and regional capacity squeezes concentrate leverage during shortages; hedging and dual-qualification partly mitigate exposure.

| Metric | 2024 |

|---|---|

| Steel price volatility | elevated vs 2023 |

| Tool lead-time | 4–12 weeks |

| Rush premiums | up to 30% |

| Drewry WCI vs 2021 | −~75% |

What is included in the product

Tailored exclusively for Trifast, this Porter’s Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to its fastener distribution and manufacturing niche. It identifies disruptive substitutes, emerging threats, and strategic barriers that influence Trifast’s pricing power and long-term profitability.

A concise one-sheet Porter's Five Forces for Trifast that clarifies supplier, customer and competitive pressure—plug-and-play for rapid strategic decisions and investor briefings; customize pressure levels and export clean charts ready for pitch decks.

Customers Bargaining Power

Large OEM and Tier-1 leverage

Automotive and electronics OEMs buy very high volumes and negotiate aggressively, using leverage over suppliers on price, lead times and quality. Vendor consolidation funnels spend to fewer partners, pressuring margins as OEMs push supplier rationalization. Annual cost-down expectations of about 2–4% are common via productivity sharing, and long-term agreements trade lower prices for multi-year volume and forecast visibility.

Switching costs and requalification

Fasteners require drawings, samples, PPAP and line trials that typically take 6–12 weeks to validate, raising switching costs and reducing buyer leverage once a program is underway.

End-of-program rebids, commonly every 3–7 years in automotive cycles, reset pricing pressure, while strict engineering change control during the lifecycle often entrenches incumbents.

Price sensitivity on commoditized SKUs

Standard fasteners are routinely subject to benchmarking and e-auctions, enabling buyers to drive price reductions and threaten imports or private-label substitutes to secure discounts. Differentiation through application engineering and vendor-managed inventory reduces direct unit‑price comparisons and supports higher margins. Framing value as total cost of ownership — service, inventory turns, warranty reduction — defends pricing beyond unit cost, with procurement programs often reporting single‑digit to low‑teens percent price pressure.

Service-level and JIT dependencies

JIT and line-side delivery make continuity and OTIF paramount, with many OEMs demanding OTIF >98% and penalizing misses; stockouts that cause stoppages sharply raise buyer scrutiny and bargaining clout. Robust forecasting, kitting and VMI embed suppliers operationally, reducing churn but increasing dependency. Penalties and scorecards institutionalize performance pressure, shifting negotiation power toward vigilant buyers.

- OTIF target: >98%

- Stockouts → immediate line stoppage risk

- VMI/kitting embeds supplier operations

- Scorecards/penalties formalize buyer leverage

Specification influence by design teams

Design engineers often standardize on specific fastener geometries or brands, and early design-in materially reduces later substitution, limiting procurement leverage. Suppliers offering DFM and application support can steer specs toward their strengths, entrenching their position. Conversely, late-stage engineering changes reopen competitive options and restore buyer bargaining power.

- Design-in locks: decreases substitution

- DFM/A: shapes specs toward supplier

- Early lock-in: weakens procurement leverage

- Late changes: restore competition

Buyers force 2–4% cost‑downs, OTIF > 98% locks suppliers

Buyers exert strong price and delivery leverage, driving 2–4% annual cost‑downs and single‑digit to low‑teens percent price pressure (2024). High OEM volumes and vendor consolidation increase bargaining power, but design‑in, PPAP lead times (6–12 weeks) and JIT/OTIF>98% raise switching costs. Program rebids (3–7 years) periodically reset pricing dynamics.

| Metric | Typical (2024) |

|---|---|

| OTIF target | >98% |

| Cost‑down | 2–4% p.a. |

| Price pressure | Single‑digit–low‑teens % |

| PPAP/validation | 6–12 weeks |

| Rebid cycle | 3–7 years |

What You See Is What You Get

Trifast Porter's Five Forces Analysis

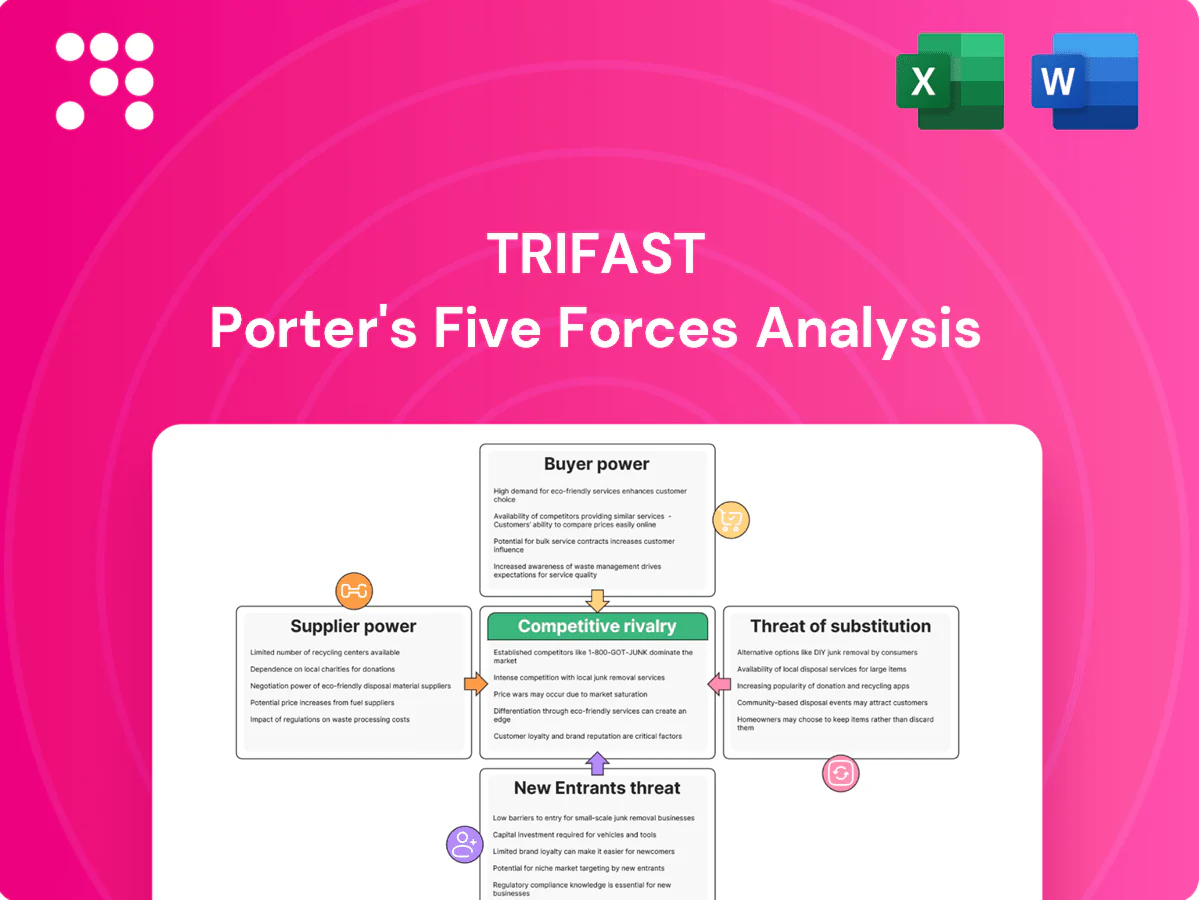

This preview shows the exact Trifast Porter's Five Forces analysis you'll receive—no surprises, no placeholders. The document provides a thorough evaluation of competitive rivalry, supplier power, buyer power, threat of substitution and entry specific to Trifast. It's fully formatted and ready for immediate download and use once you complete your purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Trifast faces moderate supplier power, niche customer leverage, steady rivalry, limited substitute threats and manageable entry barriers, shaping a cautiously optimistic outlook for growth and margin resilience. This Porter's Five Forces snapshot highlights where strategic focus can mitigate risks and capture opportunity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Trifast’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity steel and alloy dependence

TR Fastenings' reliance on carbon steel, stainless and specialty alloys exposes it to raw-material price volatility, heightened in 2024 by supply-chain tightness across mills. Upstream consolidation in steel producers has compressed availability and enabled rapid cost pass-through to buyers. Hedging and multi-sourcing reduce but do not eliminate exposure, while customer-approved material specs restrict substitution and bargaining flexibility.

Fragmented component suppliers

Many tooling, plating and secondary-process suppliers remain regionally fragmented, limiting individual supplier leverage but increasing coordination and logistics costs. In 2024 Trifast and peers accelerated Vendor Managed Inventory and supplier development programs to standardize lead-times and quality. Dual-qualification of components is widely used to preserve continuity and mitigate single-source risk.

Quality and certification requirements

Automotive and electronics end-markets mandate IATF 16949, ISO certifications, PPAP submissions and full traceability, making certification a gating factor for Trifast suppliers. Approved vendor lists concentrate spend among qualified suppliers and raise switching frictions, increasing supplier bargaining power. Failures carry high recall and warranty exposure that can run into hundreds of millions to billions, reinforcing reliance on trusted sources. Long audit cycles, commonly 6–12 months in 2024, slow onboarding of alternatives.

Specialized tooling and dies

Specialized cold-heading and thread-forming rely on custom tooling with lead times typically 4–12 weeks, giving niche toolmakers leverage to command premiums and rush fees often up to 30% in 2024. Tool wear and scheduled maintenance create recurring capital and service spend commonly representing 5–12% of manufacturing operating costs annually. In-house tooling design reduces exposure but does not eliminate dependency on skilled toolmakers.

- Lead times: 4–12 weeks

- Rush fees/premiums: up to 30%

- Ongoing tooling spend: 5–12% of ops costs

- In-house design lowers but does not remove supplier dependency

Logistics and geopolitical exposure

- Freight volatility: Drewry WCI down ~75% vs 2021

- Supplier leverage: capacity squeezes in Asia/Eastern Europe

- Mitigation: nearshoring and safety stock ↑ working capital

- Hedging: long-term indexed contracts share pricing risk

Supplier power moderate-high: steel concentration, 4-12 week tooling, rush premiums 30%

Supplier power is moderate-high: raw-material concentration in steel and alloys plus certification gating give suppliers pricing power and switching friction in 2024. Tooling lead-times (4–12 weeks) and rush premiums (up to 30%) add cost and risk. Freight volatility and regional capacity squeezes concentrate leverage during shortages; hedging and dual-qualification partly mitigate exposure.

| Metric | 2024 |

|---|---|

| Steel price volatility | elevated vs 2023 |

| Tool lead-time | 4–12 weeks |

| Rush premiums | up to 30% |

| Drewry WCI vs 2021 | −~75% |

What is included in the product

Tailored exclusively for Trifast, this Porter’s Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to its fastener distribution and manufacturing niche. It identifies disruptive substitutes, emerging threats, and strategic barriers that influence Trifast’s pricing power and long-term profitability.

A concise one-sheet Porter's Five Forces for Trifast that clarifies supplier, customer and competitive pressure—plug-and-play for rapid strategic decisions and investor briefings; customize pressure levels and export clean charts ready for pitch decks.

Customers Bargaining Power

Large OEM and Tier-1 leverage

Automotive and electronics OEMs buy very high volumes and negotiate aggressively, using leverage over suppliers on price, lead times and quality. Vendor consolidation funnels spend to fewer partners, pressuring margins as OEMs push supplier rationalization. Annual cost-down expectations of about 2–4% are common via productivity sharing, and long-term agreements trade lower prices for multi-year volume and forecast visibility.

Switching costs and requalification

Fasteners require drawings, samples, PPAP and line trials that typically take 6–12 weeks to validate, raising switching costs and reducing buyer leverage once a program is underway.

End-of-program rebids, commonly every 3–7 years in automotive cycles, reset pricing pressure, while strict engineering change control during the lifecycle often entrenches incumbents.

Price sensitivity on commoditized SKUs

Standard fasteners are routinely subject to benchmarking and e-auctions, enabling buyers to drive price reductions and threaten imports or private-label substitutes to secure discounts. Differentiation through application engineering and vendor-managed inventory reduces direct unit‑price comparisons and supports higher margins. Framing value as total cost of ownership — service, inventory turns, warranty reduction — defends pricing beyond unit cost, with procurement programs often reporting single‑digit to low‑teens percent price pressure.

Service-level and JIT dependencies

JIT and line-side delivery make continuity and OTIF paramount, with many OEMs demanding OTIF >98% and penalizing misses; stockouts that cause stoppages sharply raise buyer scrutiny and bargaining clout. Robust forecasting, kitting and VMI embed suppliers operationally, reducing churn but increasing dependency. Penalties and scorecards institutionalize performance pressure, shifting negotiation power toward vigilant buyers.

- OTIF target: >98%

- Stockouts → immediate line stoppage risk

- VMI/kitting embeds supplier operations

- Scorecards/penalties formalize buyer leverage

Specification influence by design teams

Design engineers often standardize on specific fastener geometries or brands, and early design-in materially reduces later substitution, limiting procurement leverage. Suppliers offering DFM and application support can steer specs toward their strengths, entrenching their position. Conversely, late-stage engineering changes reopen competitive options and restore buyer bargaining power.

- Design-in locks: decreases substitution

- DFM/A: shapes specs toward supplier

- Early lock-in: weakens procurement leverage

- Late changes: restore competition

Buyers force 2–4% cost‑downs, OTIF > 98% locks suppliers

Buyers exert strong price and delivery leverage, driving 2–4% annual cost‑downs and single‑digit to low‑teens percent price pressure (2024). High OEM volumes and vendor consolidation increase bargaining power, but design‑in, PPAP lead times (6–12 weeks) and JIT/OTIF>98% raise switching costs. Program rebids (3–7 years) periodically reset pricing dynamics.

| Metric | Typical (2024) |

|---|---|

| OTIF target | >98% |

| Cost‑down | 2–4% p.a. |

| Price pressure | Single‑digit–low‑teens % |

| PPAP/validation | 6–12 weeks |

| Rebid cycle | 3–7 years |

What You See Is What You Get

Trifast Porter's Five Forces Analysis

This preview shows the exact Trifast Porter's Five Forces analysis you'll receive—no surprises, no placeholders. The document provides a thorough evaluation of competitive rivalry, supplier power, buyer power, threat of substitution and entry specific to Trifast. It's fully formatted and ready for immediate download and use once you complete your purchase.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Trifast faces moderate supplier power, niche customer leverage, steady rivalry, limited substitute threats and manageable entry barriers, shaping a cautiously optimistic outlook for growth and margin resilience. This Porter's Five Forces snapshot highlights where strategic focus can mitigate risks and capture opportunity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Trifast’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity steel and alloy dependence

TR Fastenings' reliance on carbon steel, stainless and specialty alloys exposes it to raw-material price volatility, heightened in 2024 by supply-chain tightness across mills. Upstream consolidation in steel producers has compressed availability and enabled rapid cost pass-through to buyers. Hedging and multi-sourcing reduce but do not eliminate exposure, while customer-approved material specs restrict substitution and bargaining flexibility.

Fragmented component suppliers

Many tooling, plating and secondary-process suppliers remain regionally fragmented, limiting individual supplier leverage but increasing coordination and logistics costs. In 2024 Trifast and peers accelerated Vendor Managed Inventory and supplier development programs to standardize lead-times and quality. Dual-qualification of components is widely used to preserve continuity and mitigate single-source risk.

Quality and certification requirements

Automotive and electronics end-markets mandate IATF 16949, ISO certifications, PPAP submissions and full traceability, making certification a gating factor for Trifast suppliers. Approved vendor lists concentrate spend among qualified suppliers and raise switching frictions, increasing supplier bargaining power. Failures carry high recall and warranty exposure that can run into hundreds of millions to billions, reinforcing reliance on trusted sources. Long audit cycles, commonly 6–12 months in 2024, slow onboarding of alternatives.

Specialized tooling and dies

Specialized cold-heading and thread-forming rely on custom tooling with lead times typically 4–12 weeks, giving niche toolmakers leverage to command premiums and rush fees often up to 30% in 2024. Tool wear and scheduled maintenance create recurring capital and service spend commonly representing 5–12% of manufacturing operating costs annually. In-house tooling design reduces exposure but does not eliminate dependency on skilled toolmakers.

- Lead times: 4–12 weeks

- Rush fees/premiums: up to 30%

- Ongoing tooling spend: 5–12% of ops costs

- In-house design lowers but does not remove supplier dependency

Logistics and geopolitical exposure

- Freight volatility: Drewry WCI down ~75% vs 2021

- Supplier leverage: capacity squeezes in Asia/Eastern Europe

- Mitigation: nearshoring and safety stock ↑ working capital

- Hedging: long-term indexed contracts share pricing risk

Supplier power moderate-high: steel concentration, 4-12 week tooling, rush premiums 30%

Supplier power is moderate-high: raw-material concentration in steel and alloys plus certification gating give suppliers pricing power and switching friction in 2024. Tooling lead-times (4–12 weeks) and rush premiums (up to 30%) add cost and risk. Freight volatility and regional capacity squeezes concentrate leverage during shortages; hedging and dual-qualification partly mitigate exposure.

| Metric | 2024 |

|---|---|

| Steel price volatility | elevated vs 2023 |

| Tool lead-time | 4–12 weeks |

| Rush premiums | up to 30% |

| Drewry WCI vs 2021 | −~75% |

What is included in the product

Tailored exclusively for Trifast, this Porter’s Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to its fastener distribution and manufacturing niche. It identifies disruptive substitutes, emerging threats, and strategic barriers that influence Trifast’s pricing power and long-term profitability.

A concise one-sheet Porter's Five Forces for Trifast that clarifies supplier, customer and competitive pressure—plug-and-play for rapid strategic decisions and investor briefings; customize pressure levels and export clean charts ready for pitch decks.

Customers Bargaining Power

Large OEM and Tier-1 leverage

Automotive and electronics OEMs buy very high volumes and negotiate aggressively, using leverage over suppliers on price, lead times and quality. Vendor consolidation funnels spend to fewer partners, pressuring margins as OEMs push supplier rationalization. Annual cost-down expectations of about 2–4% are common via productivity sharing, and long-term agreements trade lower prices for multi-year volume and forecast visibility.

Switching costs and requalification

Fasteners require drawings, samples, PPAP and line trials that typically take 6–12 weeks to validate, raising switching costs and reducing buyer leverage once a program is underway.

End-of-program rebids, commonly every 3–7 years in automotive cycles, reset pricing pressure, while strict engineering change control during the lifecycle often entrenches incumbents.

Price sensitivity on commoditized SKUs

Standard fasteners are routinely subject to benchmarking and e-auctions, enabling buyers to drive price reductions and threaten imports or private-label substitutes to secure discounts. Differentiation through application engineering and vendor-managed inventory reduces direct unit‑price comparisons and supports higher margins. Framing value as total cost of ownership — service, inventory turns, warranty reduction — defends pricing beyond unit cost, with procurement programs often reporting single‑digit to low‑teens percent price pressure.

Service-level and JIT dependencies

JIT and line-side delivery make continuity and OTIF paramount, with many OEMs demanding OTIF >98% and penalizing misses; stockouts that cause stoppages sharply raise buyer scrutiny and bargaining clout. Robust forecasting, kitting and VMI embed suppliers operationally, reducing churn but increasing dependency. Penalties and scorecards institutionalize performance pressure, shifting negotiation power toward vigilant buyers.

- OTIF target: >98%

- Stockouts → immediate line stoppage risk

- VMI/kitting embeds supplier operations

- Scorecards/penalties formalize buyer leverage

Specification influence by design teams

Design engineers often standardize on specific fastener geometries or brands, and early design-in materially reduces later substitution, limiting procurement leverage. Suppliers offering DFM and application support can steer specs toward their strengths, entrenching their position. Conversely, late-stage engineering changes reopen competitive options and restore buyer bargaining power.

- Design-in locks: decreases substitution

- DFM/A: shapes specs toward supplier

- Early lock-in: weakens procurement leverage

- Late changes: restore competition

Buyers force 2–4% cost‑downs, OTIF > 98% locks suppliers

Buyers exert strong price and delivery leverage, driving 2–4% annual cost‑downs and single‑digit to low‑teens percent price pressure (2024). High OEM volumes and vendor consolidation increase bargaining power, but design‑in, PPAP lead times (6–12 weeks) and JIT/OTIF>98% raise switching costs. Program rebids (3–7 years) periodically reset pricing dynamics.

| Metric | Typical (2024) |

|---|---|

| OTIF target | >98% |

| Cost‑down | 2–4% p.a. |

| Price pressure | Single‑digit–low‑teens % |

| PPAP/validation | 6–12 weeks |

| Rebid cycle | 3–7 years |

What You See Is What You Get

Trifast Porter's Five Forces Analysis

This preview shows the exact Trifast Porter's Five Forces analysis you'll receive—no surprises, no placeholders. The document provides a thorough evaluation of competitive rivalry, supplier power, buyer power, threat of substitution and entry specific to Trifast. It's fully formatted and ready for immediate download and use once you complete your purchase.