Saddle Ranch Media, Inc. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Saddle Ranch Media, Inc. faces moderate supplier leverage, rising buyer sophistication, and significant rivalry from digital-first publishers, while barriers to entry are lowering with programmatic ad tools and substitutes like social platforms intensifying pressure on margins. Strategic positioning and content differentiation will determine whether SRM can sustain pricing power and audience growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Saddle Ranch Media, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated chip and radio suppliers

Core 5G and IoT components are concentrated: TSMC held roughly 54% of global foundry capacity in 2023 and Qualcomm supplied the majority of 5G smartphone modems in 2023, raising switching costs and lead-time risk. Dependence on baseband, RF modules and edge silicon gives suppliers pricing leverage while US export controls through 2023–24 tightened access to advanced nodes. Multi-sourcing and design-for-substitution can partially offset this power.

Telecom IP and standards licensing

SEP and protocol-stack licenses for 5G/NR, NB-IoT and LTE-M are concentrated with Qualcomm, Ericsson, Nokia, Huawei and Samsung per 2024 ETSI declarations, giving suppliers strong leverage. Royalty schemes—commonly cited in studies at roughly 0.5–2% of device price—can compress device and gateway margins. Ongoing standard updates create recurring engineering and testing costs. Negotiating portfolio licenses and adopting open RAN stacks can materially lower dependency and royalty exposure.

Contract manufacturers and ODMs

Hardware production for Saddle Ranch Media depends on EMS/ODM partners in a global EMS market exceeding $500 billion (2024), giving scale advantages to large manufacturers; in tight capacity cycles smaller runs suffer price and allocation disadvantages. FCC/CE and carrier certification needs raise supplier lock-in; dual-EMS footprints and strict SLA/QBR regimes help rebalance pricing, priority and risk.

Cloud and edge platform providers

ONENET likely depends on hyperscale IaaS/PaaS and edge services, where AWS/Azure/GCP controlled roughly 65% of global IaaS/PaaS spend in 2024; egress, AI/ML and managed data service pricing can swing unit economics materially, while proprietary APIs create soft lock-in that raises switching costs; multi-cloud designs and reserved capacity contracts—discounts up to ~50%—can temper supplier power.

- Dependence: hyperscalers ~65% share (2024)

- Cost levers: egress/AI/data pricing

- Risk: proprietary API lock-in

- Mitigation: multi-cloud, reserved capacity (~30–50% discounts)

Energy hardware and sensor ecosystems

Suppliers of meters, inverters, batteries and sensors control critical interfaces and certifications, creating gateway points for integration and compliance; closed protocols often force vendor-specific integrations and require volume commitments for favorable pricing, raising switching costs for companies like Saddle Ranch Media; adopting open standards such as Matter and OpenADR in 2024 reduces supplier dependence and lowers integration risk.

- Supplier control: interfaces, certifications, vendor lock-in

- Commercial pressure: volume commitments for discounts

- Risk mitigation: Matter, OpenADR adoption in 2024

Concentrated suppliers (54%, 65%, $500B) raise pricing and lock-in; pursue multi-sourcing

Suppliers hold significant leverage: TSMC ~54% foundry (2023), hyperscalers ~65% IaaS/PaaS (2024) and EMS market >$500B (2024) concentrate pricing/lock-in and raise switching costs; SEP royalties (~0.5–2% device price) and vendor-specific energy hardware add margin pressure. Mitigations: multi-sourcing, open standards, multi-cloud, reserved capacity.

| Supplier | Share | Impact |

|---|---|---|

| Foundry | TSMC 54% (2023) | High pricing/lead-time |

| Hyperscalers | 65% (2024) | Egress/API lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Saddle Ranch Media, Inc. uncovering key competitors, buyer/supplier power, substitution risks and entry barriers, with strategic insights on disruptive threats and pricing leverage to inform investor and management decisions.

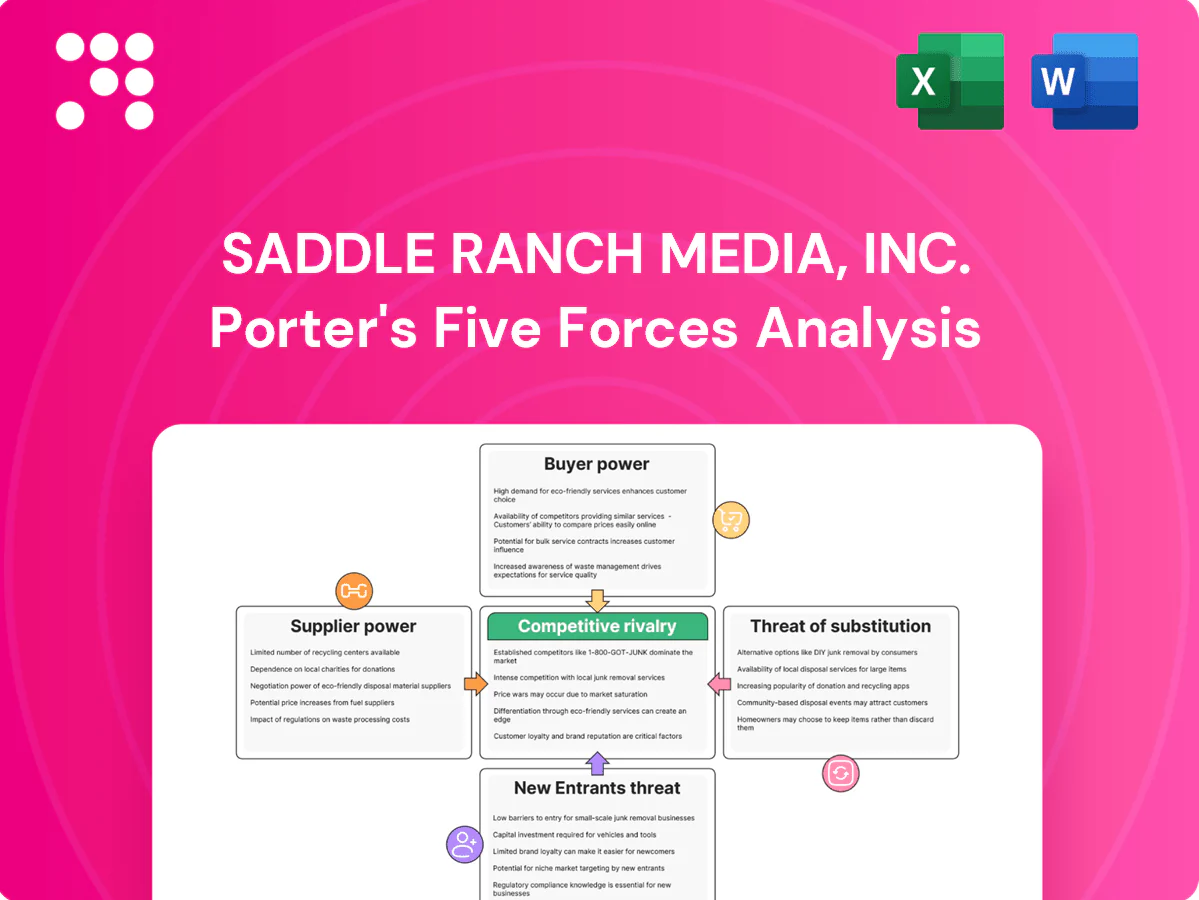

A one-sheet Porter's Five Forces for Saddle Ranch Media, Inc. relieves analytical pain points with a visual spider chart and customizable pressure levels to quickly reveal competitive threats and strategic opportunities; copy-ready layout for pitch decks, easy data swap (no macros), and seamless integration into Excel dashboards or paired Word reports.

Customers Bargaining Power

Enterprise and carrier procurement strength

Telcos, utilities and large enterprises buy at scale via formal RFPs, driving demands for discounts, SLAs and custom integrations. Long sales cycles—commonly 6–9 months—and buying committees of 6–10 stakeholders shift leverage to buyers. Proving ROI and offering outcome-based pricing mitigates margin pressure and shortens procurement friction.

Switching costs and platform lock-in

Integration with ONENET, device firmware, and proprietary data models raises switching costs for Saddle Ranch Media by creating technical lock-in and operational friction. If APIs are open and data portable, buyer power increases—2024 surveys found about 63% of enterprises rate portability as a key procurement factor. Robust migration tools can accelerate adoption while reducing negotiating leverage, and building ecosystems and marketplaces increases customer stickiness.

Price sensitivity in smart energy

Energy management buyers prioritize short payback periods—commonly targeting 2–4 years—and total cost of ownership when evaluating Saddle Ranch Media offerings; 2024 procurement surveys show payback remains the top KPI. Subsidies and utility incentives under 2024 programs frequently tip decisions toward projects with higher upfront costs. Commoditization has driven sensor prices and margins down, while bundled analytics and services help defend value and sustain recurring revenue.

Security, reliability, and compliance demands

Buyers demand robust cybersecurity, 99.99%+ uptime and regulatory alignment—Gartner estimates global security spending reached about $188B in 2024—failure to meet standards leads to vendor swaps, contract penalties or regulatory fines. Certifications such as ISO 27001 and SOC 2 are table stakes buyers use to negotiate pricing and SLAs; proactive audits and transparent roadmaps reduce buyer leverage and churn risk.

- Security spend 2024: ~$188B (Gartner)

- Uptime expectation: 99.99%+

- Certifications: ISO 27001 / SOC 2 used in negotiations

- Proactive audits/roadmaps lower buyer bargaining power

Channel partners and system integrators

Channel partners and system integrators (SIs) heavily shape Saddle Ranch Media’s vendor selection, with Gartner 2024 noting partners influence roughly 70% of enterprise tech purchasing decisions. Aggregators and resellers frequently pit vendors against each other, compressing margins and driving average vendor price concessions of 5–15% in competitive bids. Co-selling programs and enablement tools align incentives and can recoup margin pressure by boosting deal win rates and partner-led ARR growth.

- Partner influence ~70% (Gartner 2024)

- Price concessions 5–15% in competitive deals

- Co-selling increases partner-led ARR and win rates

RFP Power Shifts: Portability, SLAs and Partners Define Buyer Negotiation Leverage

Buyers (telcos, utilities, large enterprises) wield strong leverage via RFPs, long sales cycles and multi‑stakeholder committees; portability (63% importance in 2024) and SLAs drive negotiations. Technical lock‑in (ONENET, firmware) raises switching costs, but open APIs and migration tools reduce buyer power. Partners influence ~70% of deals, compressing margins 5–15% without strong co‑sell programs.

| Metric | 2024 Value |

|---|---|

| Portability importance | 63% |

| Security spend | $188B |

| Partner influence | ~70% |

| Price concessions | 5–15% |

| Uptime expectation | 99.99%+ |

What You See Is What You Get

Saddle Ranch Media, Inc. Porter's Five Forces Analysis

This preview displays the full Porter's Five Forces analysis for Saddle Ranch Media, Inc., covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. The file shown is the exact document you'll receive upon purchase. No placeholders or samples—fully formatted and ready to download. Instant access after payment.

Don't Miss the Bigger Picture

Saddle Ranch Media, Inc. faces moderate supplier leverage, rising buyer sophistication, and significant rivalry from digital-first publishers, while barriers to entry are lowering with programmatic ad tools and substitutes like social platforms intensifying pressure on margins. Strategic positioning and content differentiation will determine whether SRM can sustain pricing power and audience growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Saddle Ranch Media, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated chip and radio suppliers

Core 5G and IoT components are concentrated: TSMC held roughly 54% of global foundry capacity in 2023 and Qualcomm supplied the majority of 5G smartphone modems in 2023, raising switching costs and lead-time risk. Dependence on baseband, RF modules and edge silicon gives suppliers pricing leverage while US export controls through 2023–24 tightened access to advanced nodes. Multi-sourcing and design-for-substitution can partially offset this power.

Telecom IP and standards licensing

SEP and protocol-stack licenses for 5G/NR, NB-IoT and LTE-M are concentrated with Qualcomm, Ericsson, Nokia, Huawei and Samsung per 2024 ETSI declarations, giving suppliers strong leverage. Royalty schemes—commonly cited in studies at roughly 0.5–2% of device price—can compress device and gateway margins. Ongoing standard updates create recurring engineering and testing costs. Negotiating portfolio licenses and adopting open RAN stacks can materially lower dependency and royalty exposure.

Contract manufacturers and ODMs

Hardware production for Saddle Ranch Media depends on EMS/ODM partners in a global EMS market exceeding $500 billion (2024), giving scale advantages to large manufacturers; in tight capacity cycles smaller runs suffer price and allocation disadvantages. FCC/CE and carrier certification needs raise supplier lock-in; dual-EMS footprints and strict SLA/QBR regimes help rebalance pricing, priority and risk.

Cloud and edge platform providers

ONENET likely depends on hyperscale IaaS/PaaS and edge services, where AWS/Azure/GCP controlled roughly 65% of global IaaS/PaaS spend in 2024; egress, AI/ML and managed data service pricing can swing unit economics materially, while proprietary APIs create soft lock-in that raises switching costs; multi-cloud designs and reserved capacity contracts—discounts up to ~50%—can temper supplier power.

- Dependence: hyperscalers ~65% share (2024)

- Cost levers: egress/AI/data pricing

- Risk: proprietary API lock-in

- Mitigation: multi-cloud, reserved capacity (~30–50% discounts)

Energy hardware and sensor ecosystems

Suppliers of meters, inverters, batteries and sensors control critical interfaces and certifications, creating gateway points for integration and compliance; closed protocols often force vendor-specific integrations and require volume commitments for favorable pricing, raising switching costs for companies like Saddle Ranch Media; adopting open standards such as Matter and OpenADR in 2024 reduces supplier dependence and lowers integration risk.

- Supplier control: interfaces, certifications, vendor lock-in

- Commercial pressure: volume commitments for discounts

- Risk mitigation: Matter, OpenADR adoption in 2024

Concentrated suppliers (54%, 65%, $500B) raise pricing and lock-in; pursue multi-sourcing

Suppliers hold significant leverage: TSMC ~54% foundry (2023), hyperscalers ~65% IaaS/PaaS (2024) and EMS market >$500B (2024) concentrate pricing/lock-in and raise switching costs; SEP royalties (~0.5–2% device price) and vendor-specific energy hardware add margin pressure. Mitigations: multi-sourcing, open standards, multi-cloud, reserved capacity.

| Supplier | Share | Impact |

|---|---|---|

| Foundry | TSMC 54% (2023) | High pricing/lead-time |

| Hyperscalers | 65% (2024) | Egress/API lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Saddle Ranch Media, Inc. uncovering key competitors, buyer/supplier power, substitution risks and entry barriers, with strategic insights on disruptive threats and pricing leverage to inform investor and management decisions.

A one-sheet Porter's Five Forces for Saddle Ranch Media, Inc. relieves analytical pain points with a visual spider chart and customizable pressure levels to quickly reveal competitive threats and strategic opportunities; copy-ready layout for pitch decks, easy data swap (no macros), and seamless integration into Excel dashboards or paired Word reports.

Customers Bargaining Power

Enterprise and carrier procurement strength

Telcos, utilities and large enterprises buy at scale via formal RFPs, driving demands for discounts, SLAs and custom integrations. Long sales cycles—commonly 6–9 months—and buying committees of 6–10 stakeholders shift leverage to buyers. Proving ROI and offering outcome-based pricing mitigates margin pressure and shortens procurement friction.

Switching costs and platform lock-in

Integration with ONENET, device firmware, and proprietary data models raises switching costs for Saddle Ranch Media by creating technical lock-in and operational friction. If APIs are open and data portable, buyer power increases—2024 surveys found about 63% of enterprises rate portability as a key procurement factor. Robust migration tools can accelerate adoption while reducing negotiating leverage, and building ecosystems and marketplaces increases customer stickiness.

Price sensitivity in smart energy

Energy management buyers prioritize short payback periods—commonly targeting 2–4 years—and total cost of ownership when evaluating Saddle Ranch Media offerings; 2024 procurement surveys show payback remains the top KPI. Subsidies and utility incentives under 2024 programs frequently tip decisions toward projects with higher upfront costs. Commoditization has driven sensor prices and margins down, while bundled analytics and services help defend value and sustain recurring revenue.

Security, reliability, and compliance demands

Buyers demand robust cybersecurity, 99.99%+ uptime and regulatory alignment—Gartner estimates global security spending reached about $188B in 2024—failure to meet standards leads to vendor swaps, contract penalties or regulatory fines. Certifications such as ISO 27001 and SOC 2 are table stakes buyers use to negotiate pricing and SLAs; proactive audits and transparent roadmaps reduce buyer leverage and churn risk.

- Security spend 2024: ~$188B (Gartner)

- Uptime expectation: 99.99%+

- Certifications: ISO 27001 / SOC 2 used in negotiations

- Proactive audits/roadmaps lower buyer bargaining power

Channel partners and system integrators

Channel partners and system integrators (SIs) heavily shape Saddle Ranch Media’s vendor selection, with Gartner 2024 noting partners influence roughly 70% of enterprise tech purchasing decisions. Aggregators and resellers frequently pit vendors against each other, compressing margins and driving average vendor price concessions of 5–15% in competitive bids. Co-selling programs and enablement tools align incentives and can recoup margin pressure by boosting deal win rates and partner-led ARR growth.

- Partner influence ~70% (Gartner 2024)

- Price concessions 5–15% in competitive deals

- Co-selling increases partner-led ARR and win rates

RFP Power Shifts: Portability, SLAs and Partners Define Buyer Negotiation Leverage

Buyers (telcos, utilities, large enterprises) wield strong leverage via RFPs, long sales cycles and multi‑stakeholder committees; portability (63% importance in 2024) and SLAs drive negotiations. Technical lock‑in (ONENET, firmware) raises switching costs, but open APIs and migration tools reduce buyer power. Partners influence ~70% of deals, compressing margins 5–15% without strong co‑sell programs.

| Metric | 2024 Value |

|---|---|

| Portability importance | 63% |

| Security spend | $188B |

| Partner influence | ~70% |

| Price concessions | 5–15% |

| Uptime expectation | 99.99%+ |

What You See Is What You Get

Saddle Ranch Media, Inc. Porter's Five Forces Analysis

This preview displays the full Porter's Five Forces analysis for Saddle Ranch Media, Inc., covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. The file shown is the exact document you'll receive upon purchase. No placeholders or samples—fully formatted and ready to download. Instant access after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Saddle Ranch Media, Inc. faces moderate supplier leverage, rising buyer sophistication, and significant rivalry from digital-first publishers, while barriers to entry are lowering with programmatic ad tools and substitutes like social platforms intensifying pressure on margins. Strategic positioning and content differentiation will determine whether SRM can sustain pricing power and audience growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Saddle Ranch Media, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated chip and radio suppliers

Core 5G and IoT components are concentrated: TSMC held roughly 54% of global foundry capacity in 2023 and Qualcomm supplied the majority of 5G smartphone modems in 2023, raising switching costs and lead-time risk. Dependence on baseband, RF modules and edge silicon gives suppliers pricing leverage while US export controls through 2023–24 tightened access to advanced nodes. Multi-sourcing and design-for-substitution can partially offset this power.

Telecom IP and standards licensing

SEP and protocol-stack licenses for 5G/NR, NB-IoT and LTE-M are concentrated with Qualcomm, Ericsson, Nokia, Huawei and Samsung per 2024 ETSI declarations, giving suppliers strong leverage. Royalty schemes—commonly cited in studies at roughly 0.5–2% of device price—can compress device and gateway margins. Ongoing standard updates create recurring engineering and testing costs. Negotiating portfolio licenses and adopting open RAN stacks can materially lower dependency and royalty exposure.

Contract manufacturers and ODMs

Hardware production for Saddle Ranch Media depends on EMS/ODM partners in a global EMS market exceeding $500 billion (2024), giving scale advantages to large manufacturers; in tight capacity cycles smaller runs suffer price and allocation disadvantages. FCC/CE and carrier certification needs raise supplier lock-in; dual-EMS footprints and strict SLA/QBR regimes help rebalance pricing, priority and risk.

Cloud and edge platform providers

ONENET likely depends on hyperscale IaaS/PaaS and edge services, where AWS/Azure/GCP controlled roughly 65% of global IaaS/PaaS spend in 2024; egress, AI/ML and managed data service pricing can swing unit economics materially, while proprietary APIs create soft lock-in that raises switching costs; multi-cloud designs and reserved capacity contracts—discounts up to ~50%—can temper supplier power.

- Dependence: hyperscalers ~65% share (2024)

- Cost levers: egress/AI/data pricing

- Risk: proprietary API lock-in

- Mitigation: multi-cloud, reserved capacity (~30–50% discounts)

Energy hardware and sensor ecosystems

Suppliers of meters, inverters, batteries and sensors control critical interfaces and certifications, creating gateway points for integration and compliance; closed protocols often force vendor-specific integrations and require volume commitments for favorable pricing, raising switching costs for companies like Saddle Ranch Media; adopting open standards such as Matter and OpenADR in 2024 reduces supplier dependence and lowers integration risk.

- Supplier control: interfaces, certifications, vendor lock-in

- Commercial pressure: volume commitments for discounts

- Risk mitigation: Matter, OpenADR adoption in 2024

Concentrated suppliers (54%, 65%, $500B) raise pricing and lock-in; pursue multi-sourcing

Suppliers hold significant leverage: TSMC ~54% foundry (2023), hyperscalers ~65% IaaS/PaaS (2024) and EMS market >$500B (2024) concentrate pricing/lock-in and raise switching costs; SEP royalties (~0.5–2% device price) and vendor-specific energy hardware add margin pressure. Mitigations: multi-sourcing, open standards, multi-cloud, reserved capacity.

| Supplier | Share | Impact |

|---|---|---|

| Foundry | TSMC 54% (2023) | High pricing/lead-time |

| Hyperscalers | 65% (2024) | Egress/API lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Saddle Ranch Media, Inc. uncovering key competitors, buyer/supplier power, substitution risks and entry barriers, with strategic insights on disruptive threats and pricing leverage to inform investor and management decisions.

A one-sheet Porter's Five Forces for Saddle Ranch Media, Inc. relieves analytical pain points with a visual spider chart and customizable pressure levels to quickly reveal competitive threats and strategic opportunities; copy-ready layout for pitch decks, easy data swap (no macros), and seamless integration into Excel dashboards or paired Word reports.

Customers Bargaining Power

Enterprise and carrier procurement strength

Telcos, utilities and large enterprises buy at scale via formal RFPs, driving demands for discounts, SLAs and custom integrations. Long sales cycles—commonly 6–9 months—and buying committees of 6–10 stakeholders shift leverage to buyers. Proving ROI and offering outcome-based pricing mitigates margin pressure and shortens procurement friction.

Switching costs and platform lock-in

Integration with ONENET, device firmware, and proprietary data models raises switching costs for Saddle Ranch Media by creating technical lock-in and operational friction. If APIs are open and data portable, buyer power increases—2024 surveys found about 63% of enterprises rate portability as a key procurement factor. Robust migration tools can accelerate adoption while reducing negotiating leverage, and building ecosystems and marketplaces increases customer stickiness.

Price sensitivity in smart energy

Energy management buyers prioritize short payback periods—commonly targeting 2–4 years—and total cost of ownership when evaluating Saddle Ranch Media offerings; 2024 procurement surveys show payback remains the top KPI. Subsidies and utility incentives under 2024 programs frequently tip decisions toward projects with higher upfront costs. Commoditization has driven sensor prices and margins down, while bundled analytics and services help defend value and sustain recurring revenue.

Security, reliability, and compliance demands

Buyers demand robust cybersecurity, 99.99%+ uptime and regulatory alignment—Gartner estimates global security spending reached about $188B in 2024—failure to meet standards leads to vendor swaps, contract penalties or regulatory fines. Certifications such as ISO 27001 and SOC 2 are table stakes buyers use to negotiate pricing and SLAs; proactive audits and transparent roadmaps reduce buyer leverage and churn risk.

- Security spend 2024: ~$188B (Gartner)

- Uptime expectation: 99.99%+

- Certifications: ISO 27001 / SOC 2 used in negotiations

- Proactive audits/roadmaps lower buyer bargaining power

Channel partners and system integrators

Channel partners and system integrators (SIs) heavily shape Saddle Ranch Media’s vendor selection, with Gartner 2024 noting partners influence roughly 70% of enterprise tech purchasing decisions. Aggregators and resellers frequently pit vendors against each other, compressing margins and driving average vendor price concessions of 5–15% in competitive bids. Co-selling programs and enablement tools align incentives and can recoup margin pressure by boosting deal win rates and partner-led ARR growth.

- Partner influence ~70% (Gartner 2024)

- Price concessions 5–15% in competitive deals

- Co-selling increases partner-led ARR and win rates

RFP Power Shifts: Portability, SLAs and Partners Define Buyer Negotiation Leverage

Buyers (telcos, utilities, large enterprises) wield strong leverage via RFPs, long sales cycles and multi‑stakeholder committees; portability (63% importance in 2024) and SLAs drive negotiations. Technical lock‑in (ONENET, firmware) raises switching costs, but open APIs and migration tools reduce buyer power. Partners influence ~70% of deals, compressing margins 5–15% without strong co‑sell programs.

| Metric | 2024 Value |

|---|---|

| Portability importance | 63% |

| Security spend | $188B |

| Partner influence | ~70% |

| Price concessions | 5–15% |

| Uptime expectation | 99.99%+ |

What You See Is What You Get

Saddle Ranch Media, Inc. Porter's Five Forces Analysis

This preview displays the full Porter's Five Forces analysis for Saddle Ranch Media, Inc., covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. The file shown is the exact document you'll receive upon purchase. No placeholders or samples—fully formatted and ready to download. Instant access after payment.