Trisura Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Our Trisura Group SWOT analysis highlights robust specialty-insurance underwriting and diversified distribution as key strengths, with regulatory exposure and capital sensitivity as primary risks. The report pinpoints strategic growth levers and competitive gaps you need to monitor. Purchase the full SWOT to get a research-backed, editable Word and Excel package. Ideal for investors, advisors, and strategists seeking actionable insights.

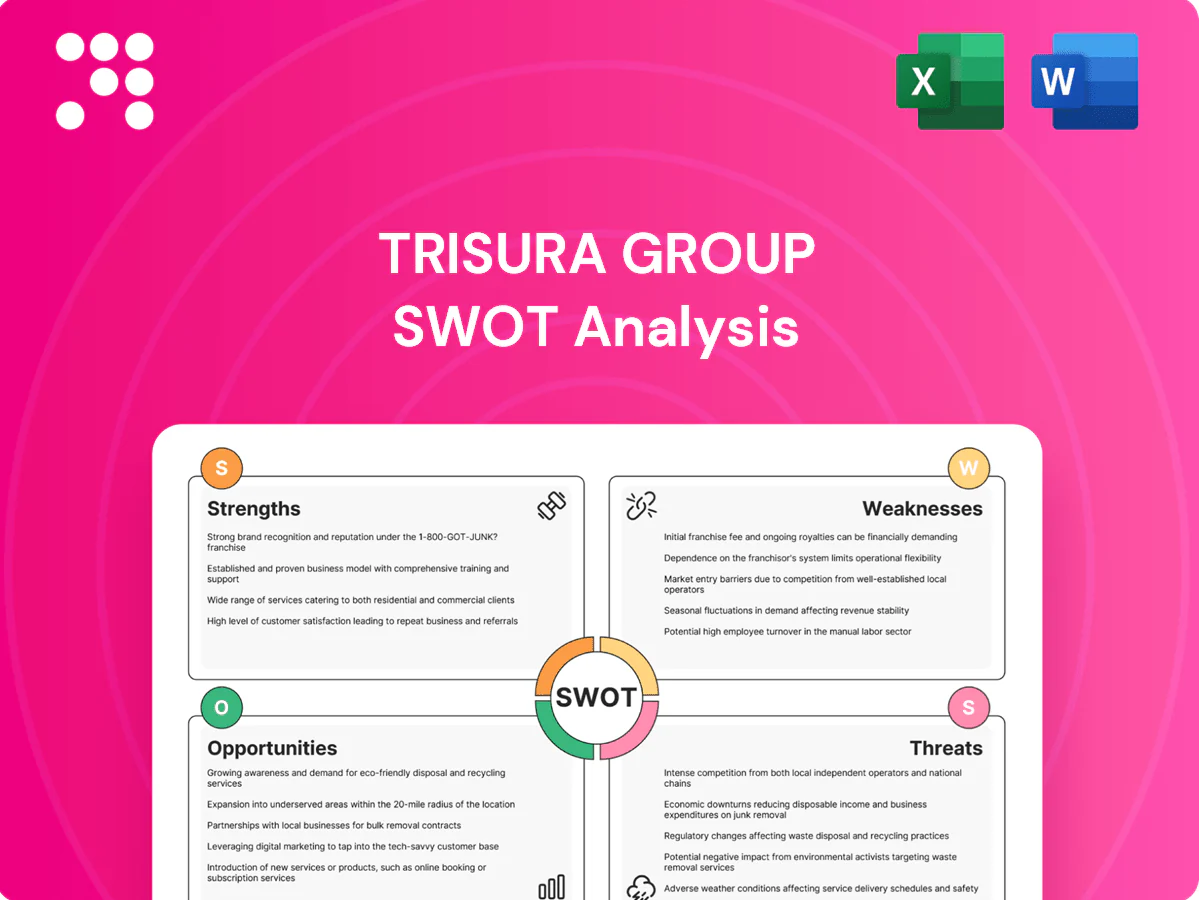

Strengths

Niche specialty focus

Trisura (TSX: TSU), founded 2004, concentrates on surety, fronting and tailored corporate risks where larger carriers are less agile, enabling superior underwriting selection and pricing power in underserved segments. This niche focus historically drives stronger loss ratios and underwriting margins versus commodity lines. Deep specialist expertise also fortifies broker relationships seeking bespoke solutions.

Capital-light fronting model

Trisura’s capital-light fronting model generates fee-based revenue while ceding the majority of policy risk to reinsurers (typically >90%), preserving balance-sheet capital. This structure is highly capital-efficient and supports scalable growth and elevated returns on equity versus traditional insurers. Fronting diversifies earnings beyond underwriting margin, with fronting/program fees growing as a share of revenue in 2024. It also attracts program partners and MGAs seeking capacity solutions.

Strong reinsurance partnerships

Deep reinsurer panels give Trisura capacity to underwrite complex or large programs, enabling placement where primary capacity is limited. Access to high-quality reinsurance paper supports competitive pricing and bolsters client confidence. Co-development with reinsurers refines product design and pricing while reducing balance-sheet concentration risk.

Geographic diversification

Trisura operates across Canada, the U.S., and select international markets, which spreads regulatory and market risk and allows regional cycles to offset each other, smoothing premium growth and loss volatility. This footprint enables cross-border program underwriting and accelerates distribution through global brokers and MGAs, strengthening brand presence and deal flow. The diversified geography supports scalable product placement and risk pooling.

- Geographic reach: Canada, U.S., international

- Risk smoothing: regionally offset cycles

- Distribution: enhanced via global brokers and MGAs

- Growth: cross-border program opportunities

Broker and MGA distribution

Trusted broker and MGA relationships drive steady deal flow into specialty niches, leveraging established credibility with intermediaries. MGAs supply specialized underwriting talent and channel access to fragmented, hard-to-reach markets. This distribution model supports efficient customer acquisition and rapid program entry or exit, enhancing portfolio agility.

- Trusted intermediaries

- MGA underwriting expertise

- Efficient acquisition

- Program flexibility

Capital-light surety & fronting; >90% ceded to reinsurers

Trisura (founded 2004) focuses on surety, fronting and tailored corporate risks, delivering superior underwriting margins in niche, underserved segments. Capital-light fronting cedes >90% of policy risk to reinsurers, boosting capital efficiency and fee-based revenue, with fronting fees rising as a share of revenue in 2024. Strong reinsurer panels and broker/MGA ties enable large/complex program placement across Canada, the U.S. and select international markets.

| Metric | Fact (2024) |

|---|---|

| Founding year | 2004 |

| Reinsurance cession | >90% |

| Geography | Canada, U.S., selective international |

What is included in the product

Provides a concise SWOT overview of Trisura Group, highlighting underwriting expertise, diversified specialty insurance products and strong capital position as strengths; limited scale and exposure concentration as weaknesses; expansion into specialty lines, strategic M&A and digitization as opportunities; and regulatory shifts, catastrophic loss exposure and intensifying competition as threats.

Provides a concise, editable SWOT matrix for Trisura Group to align strategy quickly, clarify competitive strengths and risk exposures, and accelerate stakeholder decision-making.

Weaknesses

Reliance on reinsurance capacity

Reliance on reinsurance capacity means Trisura’s fronting arrangements and large programs are exposed to reinsurer appetite and pricing, so tight market cycles can compress fronting fees or force program shrinkage. Sudden counterparty changes or capacity withdrawal can disrupt placements and coverage continuity. This reliance also adds reinsurer credit risk and collateral pressures that can strain liquidity and capital planning.

Smaller scale vs. global carriers

Smaller scale limits Trisura’s negotiating leverage on reinsurance and distribution, while scale disadvantages raise per-unit costs for technology and compliance; top global reinsurers capture roughly half of worldwide reinsurance premiums, intensifying price and capacity pressure. Reduced scale can constrain the firm’s ability to retain large risks profitably, enabling larger rivals to undercut rates or out-resource Trisura in target niches.

Earnings sensitivity to program performance

Fee income for Trisura (TSU, TSX) can fall sharply if large programs are terminated or downsized, a material risk given the firm's program-driven model in 2024. Adverse loss development or mounting cession disputes can materially depress earnings and capital levels. Concentration in a few sizable programs amplifies quarter-to-quarter volatility. Onboarding new programs demands significant underwriting and operational oversight, stretching bandwidth.

Regulatory complexity

Trisura Group (TSX: TSU) operates across Canada and the US, and multi-jurisdiction operations amplify licensing, capital and reporting burdens, raising administrative overhead. Fronting structures face heightened regulator scrutiny and larger collateral demands, while recent shifts in surety and excess & surplus (E&S) rules—after ~10% E&S premium growth in North America in 2023—force rapid product and capital adjustments, pressuring margins.

- Cross-border licensing: higher fixed compliance costs

- Fronting: increased collateral and capital strain

- Regulatory shifts: need for swift capital/product repricing

- Compliance cost squeeze: margin pressure

Brand awareness in retail markets

As a specialty insurer listed on the Toronto Stock Exchange (TSU), Trisura remains less visible to end consumers than multiline retail carriers, relying heavily on brokers and MGAs which can dilute control over client experience and underwriting messaging. Limited direct brand equity makes cross-sell into adjacent personal and small commercial lines more difficult, constraining organic retail expansion. Dependence on intermediaries increases execution risk in customer retention and price positioning.

- Low consumer visibility (TSU on TSX)

- Intermediary dependence dilutes control

- Harder to build direct brand equity vs multiline carriers

- Limits cross-sell and retail growth potential

Reinsurance dependence raises credit/collateral risk, higher per-unit costs and volatile fee income

Reliance on reinsurance/fronting exposes Trisura to reinsurer appetite, credit and collateral strain, while smaller scale raises per-unit tech/compliance costs and limits negotiating leverage; fee income and capital are volatile given program concentration and multi-jurisdiction regulatory burdens.

| Metric | Value |

|---|---|

| Listing | TSX (TSU) |

| E&S growth (NA 2023) | ~10% |

| Top global reinsurers' share | ~50% of premiums |

Same Document Delivered

Trisura Group SWOT Analysis

This is the actual Trisura Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the real, structured analysis. Buy now to unlock the complete, editable version immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Our Trisura Group SWOT analysis highlights robust specialty-insurance underwriting and diversified distribution as key strengths, with regulatory exposure and capital sensitivity as primary risks. The report pinpoints strategic growth levers and competitive gaps you need to monitor. Purchase the full SWOT to get a research-backed, editable Word and Excel package. Ideal for investors, advisors, and strategists seeking actionable insights.

Strengths

Niche specialty focus

Trisura (TSX: TSU), founded 2004, concentrates on surety, fronting and tailored corporate risks where larger carriers are less agile, enabling superior underwriting selection and pricing power in underserved segments. This niche focus historically drives stronger loss ratios and underwriting margins versus commodity lines. Deep specialist expertise also fortifies broker relationships seeking bespoke solutions.

Capital-light fronting model

Trisura’s capital-light fronting model generates fee-based revenue while ceding the majority of policy risk to reinsurers (typically >90%), preserving balance-sheet capital. This structure is highly capital-efficient and supports scalable growth and elevated returns on equity versus traditional insurers. Fronting diversifies earnings beyond underwriting margin, with fronting/program fees growing as a share of revenue in 2024. It also attracts program partners and MGAs seeking capacity solutions.

Strong reinsurance partnerships

Deep reinsurer panels give Trisura capacity to underwrite complex or large programs, enabling placement where primary capacity is limited. Access to high-quality reinsurance paper supports competitive pricing and bolsters client confidence. Co-development with reinsurers refines product design and pricing while reducing balance-sheet concentration risk.

Geographic diversification

Trisura operates across Canada, the U.S., and select international markets, which spreads regulatory and market risk and allows regional cycles to offset each other, smoothing premium growth and loss volatility. This footprint enables cross-border program underwriting and accelerates distribution through global brokers and MGAs, strengthening brand presence and deal flow. The diversified geography supports scalable product placement and risk pooling.

- Geographic reach: Canada, U.S., international

- Risk smoothing: regionally offset cycles

- Distribution: enhanced via global brokers and MGAs

- Growth: cross-border program opportunities

Broker and MGA distribution

Trusted broker and MGA relationships drive steady deal flow into specialty niches, leveraging established credibility with intermediaries. MGAs supply specialized underwriting talent and channel access to fragmented, hard-to-reach markets. This distribution model supports efficient customer acquisition and rapid program entry or exit, enhancing portfolio agility.

- Trusted intermediaries

- MGA underwriting expertise

- Efficient acquisition

- Program flexibility

Capital-light surety & fronting; >90% ceded to reinsurers

Trisura (founded 2004) focuses on surety, fronting and tailored corporate risks, delivering superior underwriting margins in niche, underserved segments. Capital-light fronting cedes >90% of policy risk to reinsurers, boosting capital efficiency and fee-based revenue, with fronting fees rising as a share of revenue in 2024. Strong reinsurer panels and broker/MGA ties enable large/complex program placement across Canada, the U.S. and select international markets.

| Metric | Fact (2024) |

|---|---|

| Founding year | 2004 |

| Reinsurance cession | >90% |

| Geography | Canada, U.S., selective international |

What is included in the product

Provides a concise SWOT overview of Trisura Group, highlighting underwriting expertise, diversified specialty insurance products and strong capital position as strengths; limited scale and exposure concentration as weaknesses; expansion into specialty lines, strategic M&A and digitization as opportunities; and regulatory shifts, catastrophic loss exposure and intensifying competition as threats.

Provides a concise, editable SWOT matrix for Trisura Group to align strategy quickly, clarify competitive strengths and risk exposures, and accelerate stakeholder decision-making.

Weaknesses

Reliance on reinsurance capacity

Reliance on reinsurance capacity means Trisura’s fronting arrangements and large programs are exposed to reinsurer appetite and pricing, so tight market cycles can compress fronting fees or force program shrinkage. Sudden counterparty changes or capacity withdrawal can disrupt placements and coverage continuity. This reliance also adds reinsurer credit risk and collateral pressures that can strain liquidity and capital planning.

Smaller scale vs. global carriers

Smaller scale limits Trisura’s negotiating leverage on reinsurance and distribution, while scale disadvantages raise per-unit costs for technology and compliance; top global reinsurers capture roughly half of worldwide reinsurance premiums, intensifying price and capacity pressure. Reduced scale can constrain the firm’s ability to retain large risks profitably, enabling larger rivals to undercut rates or out-resource Trisura in target niches.

Earnings sensitivity to program performance

Fee income for Trisura (TSU, TSX) can fall sharply if large programs are terminated or downsized, a material risk given the firm's program-driven model in 2024. Adverse loss development or mounting cession disputes can materially depress earnings and capital levels. Concentration in a few sizable programs amplifies quarter-to-quarter volatility. Onboarding new programs demands significant underwriting and operational oversight, stretching bandwidth.

Regulatory complexity

Trisura Group (TSX: TSU) operates across Canada and the US, and multi-jurisdiction operations amplify licensing, capital and reporting burdens, raising administrative overhead. Fronting structures face heightened regulator scrutiny and larger collateral demands, while recent shifts in surety and excess & surplus (E&S) rules—after ~10% E&S premium growth in North America in 2023—force rapid product and capital adjustments, pressuring margins.

- Cross-border licensing: higher fixed compliance costs

- Fronting: increased collateral and capital strain

- Regulatory shifts: need for swift capital/product repricing

- Compliance cost squeeze: margin pressure

Brand awareness in retail markets

As a specialty insurer listed on the Toronto Stock Exchange (TSU), Trisura remains less visible to end consumers than multiline retail carriers, relying heavily on brokers and MGAs which can dilute control over client experience and underwriting messaging. Limited direct brand equity makes cross-sell into adjacent personal and small commercial lines more difficult, constraining organic retail expansion. Dependence on intermediaries increases execution risk in customer retention and price positioning.

- Low consumer visibility (TSU on TSX)

- Intermediary dependence dilutes control

- Harder to build direct brand equity vs multiline carriers

- Limits cross-sell and retail growth potential

Reinsurance dependence raises credit/collateral risk, higher per-unit costs and volatile fee income

Reliance on reinsurance/fronting exposes Trisura to reinsurer appetite, credit and collateral strain, while smaller scale raises per-unit tech/compliance costs and limits negotiating leverage; fee income and capital are volatile given program concentration and multi-jurisdiction regulatory burdens.

| Metric | Value |

|---|---|

| Listing | TSX (TSU) |

| E&S growth (NA 2023) | ~10% |

| Top global reinsurers' share | ~50% of premiums |

Same Document Delivered

Trisura Group SWOT Analysis

This is the actual Trisura Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the real, structured analysis. Buy now to unlock the complete, editable version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Our Trisura Group SWOT analysis highlights robust specialty-insurance underwriting and diversified distribution as key strengths, with regulatory exposure and capital sensitivity as primary risks. The report pinpoints strategic growth levers and competitive gaps you need to monitor. Purchase the full SWOT to get a research-backed, editable Word and Excel package. Ideal for investors, advisors, and strategists seeking actionable insights.

Strengths

Niche specialty focus

Trisura (TSX: TSU), founded 2004, concentrates on surety, fronting and tailored corporate risks where larger carriers are less agile, enabling superior underwriting selection and pricing power in underserved segments. This niche focus historically drives stronger loss ratios and underwriting margins versus commodity lines. Deep specialist expertise also fortifies broker relationships seeking bespoke solutions.

Capital-light fronting model

Trisura’s capital-light fronting model generates fee-based revenue while ceding the majority of policy risk to reinsurers (typically >90%), preserving balance-sheet capital. This structure is highly capital-efficient and supports scalable growth and elevated returns on equity versus traditional insurers. Fronting diversifies earnings beyond underwriting margin, with fronting/program fees growing as a share of revenue in 2024. It also attracts program partners and MGAs seeking capacity solutions.

Strong reinsurance partnerships

Deep reinsurer panels give Trisura capacity to underwrite complex or large programs, enabling placement where primary capacity is limited. Access to high-quality reinsurance paper supports competitive pricing and bolsters client confidence. Co-development with reinsurers refines product design and pricing while reducing balance-sheet concentration risk.

Geographic diversification

Trisura operates across Canada, the U.S., and select international markets, which spreads regulatory and market risk and allows regional cycles to offset each other, smoothing premium growth and loss volatility. This footprint enables cross-border program underwriting and accelerates distribution through global brokers and MGAs, strengthening brand presence and deal flow. The diversified geography supports scalable product placement and risk pooling.

- Geographic reach: Canada, U.S., international

- Risk smoothing: regionally offset cycles

- Distribution: enhanced via global brokers and MGAs

- Growth: cross-border program opportunities

Broker and MGA distribution

Trusted broker and MGA relationships drive steady deal flow into specialty niches, leveraging established credibility with intermediaries. MGAs supply specialized underwriting talent and channel access to fragmented, hard-to-reach markets. This distribution model supports efficient customer acquisition and rapid program entry or exit, enhancing portfolio agility.

- Trusted intermediaries

- MGA underwriting expertise

- Efficient acquisition

- Program flexibility

Capital-light surety & fronting; >90% ceded to reinsurers

Trisura (founded 2004) focuses on surety, fronting and tailored corporate risks, delivering superior underwriting margins in niche, underserved segments. Capital-light fronting cedes >90% of policy risk to reinsurers, boosting capital efficiency and fee-based revenue, with fronting fees rising as a share of revenue in 2024. Strong reinsurer panels and broker/MGA ties enable large/complex program placement across Canada, the U.S. and select international markets.

| Metric | Fact (2024) |

|---|---|

| Founding year | 2004 |

| Reinsurance cession | >90% |

| Geography | Canada, U.S., selective international |

What is included in the product

Provides a concise SWOT overview of Trisura Group, highlighting underwriting expertise, diversified specialty insurance products and strong capital position as strengths; limited scale and exposure concentration as weaknesses; expansion into specialty lines, strategic M&A and digitization as opportunities; and regulatory shifts, catastrophic loss exposure and intensifying competition as threats.

Provides a concise, editable SWOT matrix for Trisura Group to align strategy quickly, clarify competitive strengths and risk exposures, and accelerate stakeholder decision-making.

Weaknesses

Reliance on reinsurance capacity

Reliance on reinsurance capacity means Trisura’s fronting arrangements and large programs are exposed to reinsurer appetite and pricing, so tight market cycles can compress fronting fees or force program shrinkage. Sudden counterparty changes or capacity withdrawal can disrupt placements and coverage continuity. This reliance also adds reinsurer credit risk and collateral pressures that can strain liquidity and capital planning.

Smaller scale vs. global carriers

Smaller scale limits Trisura’s negotiating leverage on reinsurance and distribution, while scale disadvantages raise per-unit costs for technology and compliance; top global reinsurers capture roughly half of worldwide reinsurance premiums, intensifying price and capacity pressure. Reduced scale can constrain the firm’s ability to retain large risks profitably, enabling larger rivals to undercut rates or out-resource Trisura in target niches.

Earnings sensitivity to program performance

Fee income for Trisura (TSU, TSX) can fall sharply if large programs are terminated or downsized, a material risk given the firm's program-driven model in 2024. Adverse loss development or mounting cession disputes can materially depress earnings and capital levels. Concentration in a few sizable programs amplifies quarter-to-quarter volatility. Onboarding new programs demands significant underwriting and operational oversight, stretching bandwidth.

Regulatory complexity

Trisura Group (TSX: TSU) operates across Canada and the US, and multi-jurisdiction operations amplify licensing, capital and reporting burdens, raising administrative overhead. Fronting structures face heightened regulator scrutiny and larger collateral demands, while recent shifts in surety and excess & surplus (E&S) rules—after ~10% E&S premium growth in North America in 2023—force rapid product and capital adjustments, pressuring margins.

- Cross-border licensing: higher fixed compliance costs

- Fronting: increased collateral and capital strain

- Regulatory shifts: need for swift capital/product repricing

- Compliance cost squeeze: margin pressure

Brand awareness in retail markets

As a specialty insurer listed on the Toronto Stock Exchange (TSU), Trisura remains less visible to end consumers than multiline retail carriers, relying heavily on brokers and MGAs which can dilute control over client experience and underwriting messaging. Limited direct brand equity makes cross-sell into adjacent personal and small commercial lines more difficult, constraining organic retail expansion. Dependence on intermediaries increases execution risk in customer retention and price positioning.

- Low consumer visibility (TSU on TSX)

- Intermediary dependence dilutes control

- Harder to build direct brand equity vs multiline carriers

- Limits cross-sell and retail growth potential

Reinsurance dependence raises credit/collateral risk, higher per-unit costs and volatile fee income

Reliance on reinsurance/fronting exposes Trisura to reinsurer appetite, credit and collateral strain, while smaller scale raises per-unit tech/compliance costs and limits negotiating leverage; fee income and capital are volatile given program concentration and multi-jurisdiction regulatory burdens.

| Metric | Value |

|---|---|

| Listing | TSX (TSU) |

| E&S growth (NA 2023) | ~10% |

| Top global reinsurers' share | ~50% of premiums |

Same Document Delivered

Trisura Group SWOT Analysis

This is the actual Trisura Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the real, structured analysis. Buy now to unlock the complete, editable version immediately after checkout.