TrueBlue Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

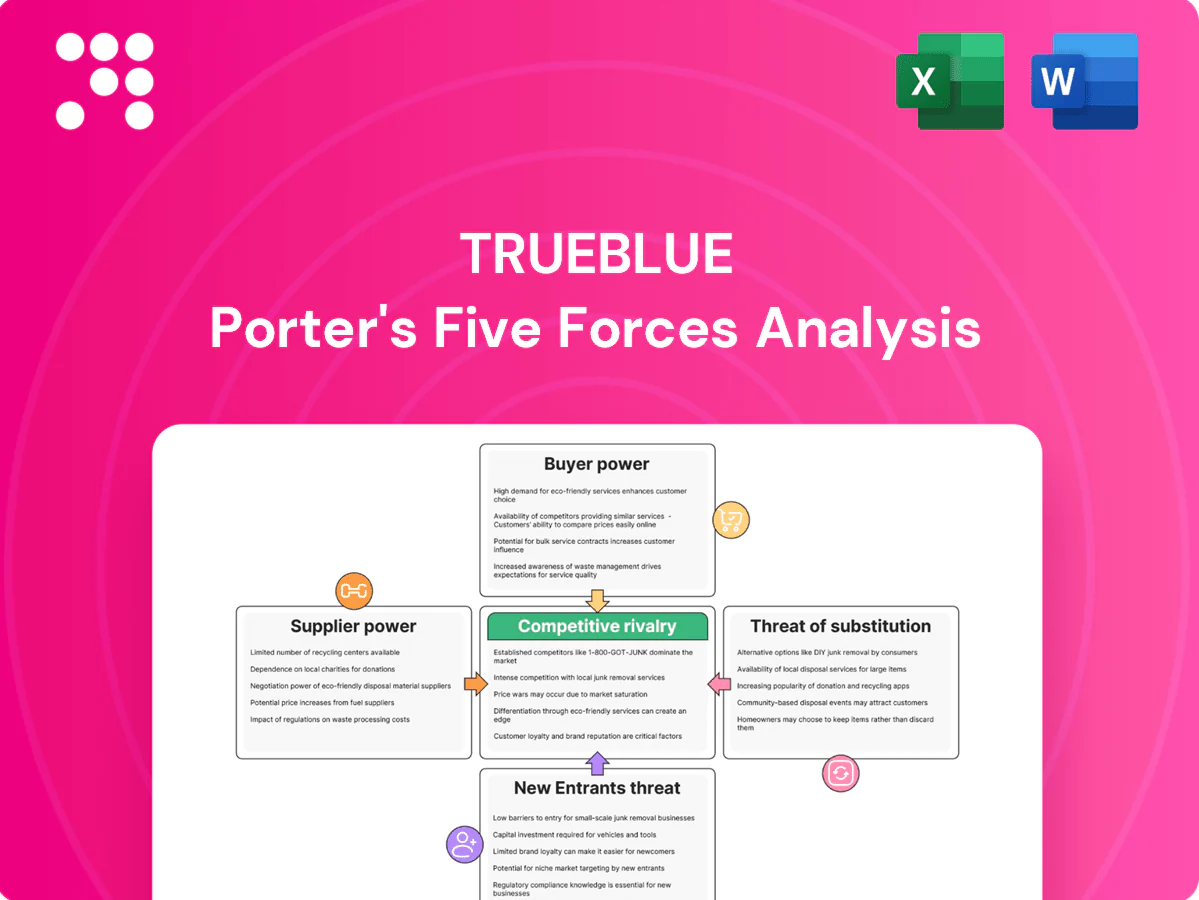

TrueBlue’s Porter's Five Forces distills the staffing firm's competitive landscape—examining buyer leverage, supplier constraints, substitute threats, entry barriers, and rivalry intensity to clarify strategic pressure points. This snapshot highlights key risks and positioning. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for TrueBlue.

Suppliers Bargaining Power

Scarce skilled labor raises leverage

When US unemployment was about 3.8% in mid‑2024, scarce skilled labor and niche recruiters commanded higher rates, squeezing TrueBlue’s gross margins or forcing client rate increases; longer fill times raised operational costs and reduced utilization, and while supplier leverage eases in downturns it spikes sharply in tight 2024 labor cycles.

Dependence on VMS/MSP and job boards

Vendor Management Systems and Managed Service Providers act as gatekeepers to TrueBlue’s demand and candidate flow, with over 60% of large employers using VMS/MSP programs in 2024, concentrating access to contracts and pay terms.

Major job boards like LinkedIn and Indeed dominate online job ad traffic, and their listing fees, platform rules, and data-access terms can compress TrueBlue’s margins.

Concentration in a few VMS/MSP and job-board platforms amplifies supplier power, forcing TrueBlue to comply to retain listings and program inclusion.

Background checks, payroll, and benefits vendors

Background checks, payroll funding, and benefits administrators are mission-critical upstream partners for TrueBlue; SHRM 2024 cites median U.S. time-to-fill near 30 days, so vendor pricing changes or service disruptions can materially lengthen placement cycles and raise compliance risk.

Technology stack and integrations

ATS/CRM, analytics and API integrations are core to TrueBlue delivery, with 2024 surveys reporting 63% of workforce platforms cite integration complexity as a top constraint. Vendor lock-in and multi-million migration costs give software providers clear leverage; bespoke workflows and custom data models raise switching friction, while uptime and data portability clauses materially shape bargaining power.

- Integration dependence: ATS/CRM + APIs

- Lock-in: high migration cost

- Switching friction: custom workflows/data models

- Contracts: uptime & data portability drive leverage

Local labor pools and seasonality

TrueBlue depends on geographically dispersed talent pools that fluctuate seasonally, with US unemployment averaging about 4.0% in 2024 increasing competition for workers during peak construction and logistics cycles and boosting worker bargaining power. Premiums and sign-on incentives are often required to secure supply, while regional wage floors and commuting constraints create added rigidity in staffing costs and fill rates.

- Seasonal peaks raise worker leverage

- 2024 US unemployment ~4.0% intensifies competition

- Premiums/incentives needed to secure supply

- Regional wages and commute limits reduce flexibility

Supplier power tightens: ~4.0% jobless, >60% VMS

Supplier power is high: 2024 US unemployment ~4.0% tightened skilled supply, driving premiums and longer fill times (median US time‑to‑fill ~30 days) that squeeze TrueBlue margins. Over 60% of large employers use VMS/MSP, concentrating contract terms. ATS/API lock‑in (63% cite integration complexity) and dominant job boards further amplify supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| US unemployment | ~4.0% | tighter labor supply |

| VMS/MSP adoption | >60% (large employers) | concentrated access/terms |

| Median time‑to‑fill | ~30 days | longer placement cycles |

| Integration complexity | 63% | vendor lock‑in/switching cost |

What is included in the product

Comprehensive Porter’s Five Forces assessment for TrueBlue, uncovering competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers to protect and grow market share.

One-sheet Porter's Five Forces for TrueBlue that maps competitive pressures, lets you tweak force levels per scenario, and produces slide-ready visuals for faster, clearer strategic decisions.

Customers Bargaining Power

Enterprise consolidation and MSP-led buying

Large enterprise clients increasingly centralize supplier selection through MSPs, which by 2024 managed roughly half of contingent workforce spend (Staffing Industry Analysts), enforcing standardized pricing that compresses TrueBlue margins and stretches payment terms into 45–75 day windows for many staffing suppliers. Preferred supplier lists restrict volume unless TrueBlue wins via tight bids, forcing delivery of scale, KPIs and reduced unit costs to retain share.

Low switching costs across agencies

Staffing services are often seen as interchangeable, especially for general labor, so buyers exercise strong bargaining power; in 2024 TrueBlue emphasized service-level and on-site program differentiation to counter this dynamic. Clients can rebid contracts frequently with minimal transition friction, driving price competition and short contract durations (often under 12 months). Differentiation via elevated service levels, safety programs and managed onsite teams is crucial to reduce churn.

RFP pressure and rate transparency

Competitive RFPs create head-to-head rate visibility, with enterprise buyers in 2024 citing benchmark data that has driven bill-rate compressions of roughly 3–7% in staffing RFPs. Volume-for-discount structures increasingly favor the lowest-cost provider, often pressuring gross margins by 150–300 basis points. TrueBlue must balance higher win rates against disciplined margin targets to avoid eroding EBITDA.

Demand cyclicality and budget sensitivity

Client volumes swing with macro cycles, shifting negotiation power; downturns see buyers squeeze rates and cut requisitions while upcycles demand rapid scaling and fill speed without proportional price increases, creating margin pressure for TrueBlue (TBI). Volatility complicates capacity planning and scheduling across contingent workforce channels; US staffing industry revenue was about 176 billion in 2023.

- Downturns: reduced requisitions, higher rate pressure

- Upcycles: rapid scale demands, limited price uplift

- Impact: staffing volatility complicates capacity and margins

High service expectations and SLAs

Buyers demand strict compliance, safety, and performance SLAs, with a 2024 industry survey finding 68% of large purchasers enforcing financial penalties for breaches; scorecards and penalties transfer risk to suppliers and compress margins. Custom reporting and onsite support raise cost-to-serve, and while meeting SLAs improves retention, it often reduces gross margin by several percentage points.

- Buyers enforce SLAs: 68% (2024 survey)

- Penalties shift risk and compress margins

- Custom reporting/on-site raises cost-to-serve

- Compliance aids retention but tightens profitability

MSPs control ~50%; bill rates down 3-7% and margins 150-300bps

Buyers wield strong leverage via MSPs (manage ~50% contingent spend in 2024), standardized pricing and 45–75 day terms, forcing tight bids and lower margins. RFP benchmarking cut bill rates ~3–7% in 2024, pressuring gross margins by 150–300 bps; clients rebid frequently with <12‑month terms. 68% of large buyers enforce SLA penalties, raising cost‑to‑serve and shifting risk to suppliers.

| Metric | Value |

|---|---|

| MSP share (2024) | ~50% |

| Payment terms | 45–75 days |

| Bill-rate compression (2024) | 3–7% |

| Margin pressure | 150–300 bps |

| SLA penalties (2024) | 68% |

Preview Before You Purchase

TrueBlue Porter's Five Forces Analysis

This preview displays the exact TrueBlue Porter's Five Forces Analysis you'll receive after purchase—no placeholders, no mockups. The file is fully formatted, complete, and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.

Go Beyond the Preview—Access the Full Strategic Report

TrueBlue’s Porter's Five Forces distills the staffing firm's competitive landscape—examining buyer leverage, supplier constraints, substitute threats, entry barriers, and rivalry intensity to clarify strategic pressure points. This snapshot highlights key risks and positioning. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for TrueBlue.

Suppliers Bargaining Power

Scarce skilled labor raises leverage

When US unemployment was about 3.8% in mid‑2024, scarce skilled labor and niche recruiters commanded higher rates, squeezing TrueBlue’s gross margins or forcing client rate increases; longer fill times raised operational costs and reduced utilization, and while supplier leverage eases in downturns it spikes sharply in tight 2024 labor cycles.

Dependence on VMS/MSP and job boards

Vendor Management Systems and Managed Service Providers act as gatekeepers to TrueBlue’s demand and candidate flow, with over 60% of large employers using VMS/MSP programs in 2024, concentrating access to contracts and pay terms.

Major job boards like LinkedIn and Indeed dominate online job ad traffic, and their listing fees, platform rules, and data-access terms can compress TrueBlue’s margins.

Concentration in a few VMS/MSP and job-board platforms amplifies supplier power, forcing TrueBlue to comply to retain listings and program inclusion.

Background checks, payroll, and benefits vendors

Background checks, payroll funding, and benefits administrators are mission-critical upstream partners for TrueBlue; SHRM 2024 cites median U.S. time-to-fill near 30 days, so vendor pricing changes or service disruptions can materially lengthen placement cycles and raise compliance risk.

Technology stack and integrations

ATS/CRM, analytics and API integrations are core to TrueBlue delivery, with 2024 surveys reporting 63% of workforce platforms cite integration complexity as a top constraint. Vendor lock-in and multi-million migration costs give software providers clear leverage; bespoke workflows and custom data models raise switching friction, while uptime and data portability clauses materially shape bargaining power.

- Integration dependence: ATS/CRM + APIs

- Lock-in: high migration cost

- Switching friction: custom workflows/data models

- Contracts: uptime & data portability drive leverage

Local labor pools and seasonality

TrueBlue depends on geographically dispersed talent pools that fluctuate seasonally, with US unemployment averaging about 4.0% in 2024 increasing competition for workers during peak construction and logistics cycles and boosting worker bargaining power. Premiums and sign-on incentives are often required to secure supply, while regional wage floors and commuting constraints create added rigidity in staffing costs and fill rates.

- Seasonal peaks raise worker leverage

- 2024 US unemployment ~4.0% intensifies competition

- Premiums/incentives needed to secure supply

- Regional wages and commute limits reduce flexibility

Supplier power tightens: ~4.0% jobless, >60% VMS

Supplier power is high: 2024 US unemployment ~4.0% tightened skilled supply, driving premiums and longer fill times (median US time‑to‑fill ~30 days) that squeeze TrueBlue margins. Over 60% of large employers use VMS/MSP, concentrating contract terms. ATS/API lock‑in (63% cite integration complexity) and dominant job boards further amplify supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| US unemployment | ~4.0% | tighter labor supply |

| VMS/MSP adoption | >60% (large employers) | concentrated access/terms |

| Median time‑to‑fill | ~30 days | longer placement cycles |

| Integration complexity | 63% | vendor lock‑in/switching cost |

What is included in the product

Comprehensive Porter’s Five Forces assessment for TrueBlue, uncovering competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers to protect and grow market share.

One-sheet Porter's Five Forces for TrueBlue that maps competitive pressures, lets you tweak force levels per scenario, and produces slide-ready visuals for faster, clearer strategic decisions.

Customers Bargaining Power

Enterprise consolidation and MSP-led buying

Large enterprise clients increasingly centralize supplier selection through MSPs, which by 2024 managed roughly half of contingent workforce spend (Staffing Industry Analysts), enforcing standardized pricing that compresses TrueBlue margins and stretches payment terms into 45–75 day windows for many staffing suppliers. Preferred supplier lists restrict volume unless TrueBlue wins via tight bids, forcing delivery of scale, KPIs and reduced unit costs to retain share.

Low switching costs across agencies

Staffing services are often seen as interchangeable, especially for general labor, so buyers exercise strong bargaining power; in 2024 TrueBlue emphasized service-level and on-site program differentiation to counter this dynamic. Clients can rebid contracts frequently with minimal transition friction, driving price competition and short contract durations (often under 12 months). Differentiation via elevated service levels, safety programs and managed onsite teams is crucial to reduce churn.

RFP pressure and rate transparency

Competitive RFPs create head-to-head rate visibility, with enterprise buyers in 2024 citing benchmark data that has driven bill-rate compressions of roughly 3–7% in staffing RFPs. Volume-for-discount structures increasingly favor the lowest-cost provider, often pressuring gross margins by 150–300 basis points. TrueBlue must balance higher win rates against disciplined margin targets to avoid eroding EBITDA.

Demand cyclicality and budget sensitivity

Client volumes swing with macro cycles, shifting negotiation power; downturns see buyers squeeze rates and cut requisitions while upcycles demand rapid scaling and fill speed without proportional price increases, creating margin pressure for TrueBlue (TBI). Volatility complicates capacity planning and scheduling across contingent workforce channels; US staffing industry revenue was about 176 billion in 2023.

- Downturns: reduced requisitions, higher rate pressure

- Upcycles: rapid scale demands, limited price uplift

- Impact: staffing volatility complicates capacity and margins

High service expectations and SLAs

Buyers demand strict compliance, safety, and performance SLAs, with a 2024 industry survey finding 68% of large purchasers enforcing financial penalties for breaches; scorecards and penalties transfer risk to suppliers and compress margins. Custom reporting and onsite support raise cost-to-serve, and while meeting SLAs improves retention, it often reduces gross margin by several percentage points.

- Buyers enforce SLAs: 68% (2024 survey)

- Penalties shift risk and compress margins

- Custom reporting/on-site raises cost-to-serve

- Compliance aids retention but tightens profitability

MSPs control ~50%; bill rates down 3-7% and margins 150-300bps

Buyers wield strong leverage via MSPs (manage ~50% contingent spend in 2024), standardized pricing and 45–75 day terms, forcing tight bids and lower margins. RFP benchmarking cut bill rates ~3–7% in 2024, pressuring gross margins by 150–300 bps; clients rebid frequently with <12‑month terms. 68% of large buyers enforce SLA penalties, raising cost‑to‑serve and shifting risk to suppliers.

| Metric | Value |

|---|---|

| MSP share (2024) | ~50% |

| Payment terms | 45–75 days |

| Bill-rate compression (2024) | 3–7% |

| Margin pressure | 150–300 bps |

| SLA penalties (2024) | 68% |

Preview Before You Purchase

TrueBlue Porter's Five Forces Analysis

This preview displays the exact TrueBlue Porter's Five Forces Analysis you'll receive after purchase—no placeholders, no mockups. The file is fully formatted, complete, and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

TrueBlue’s Porter's Five Forces distills the staffing firm's competitive landscape—examining buyer leverage, supplier constraints, substitute threats, entry barriers, and rivalry intensity to clarify strategic pressure points. This snapshot highlights key risks and positioning. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for TrueBlue.

Suppliers Bargaining Power

Scarce skilled labor raises leverage

When US unemployment was about 3.8% in mid‑2024, scarce skilled labor and niche recruiters commanded higher rates, squeezing TrueBlue’s gross margins or forcing client rate increases; longer fill times raised operational costs and reduced utilization, and while supplier leverage eases in downturns it spikes sharply in tight 2024 labor cycles.

Dependence on VMS/MSP and job boards

Vendor Management Systems and Managed Service Providers act as gatekeepers to TrueBlue’s demand and candidate flow, with over 60% of large employers using VMS/MSP programs in 2024, concentrating access to contracts and pay terms.

Major job boards like LinkedIn and Indeed dominate online job ad traffic, and their listing fees, platform rules, and data-access terms can compress TrueBlue’s margins.

Concentration in a few VMS/MSP and job-board platforms amplifies supplier power, forcing TrueBlue to comply to retain listings and program inclusion.

Background checks, payroll, and benefits vendors

Background checks, payroll funding, and benefits administrators are mission-critical upstream partners for TrueBlue; SHRM 2024 cites median U.S. time-to-fill near 30 days, so vendor pricing changes or service disruptions can materially lengthen placement cycles and raise compliance risk.

Technology stack and integrations

ATS/CRM, analytics and API integrations are core to TrueBlue delivery, with 2024 surveys reporting 63% of workforce platforms cite integration complexity as a top constraint. Vendor lock-in and multi-million migration costs give software providers clear leverage; bespoke workflows and custom data models raise switching friction, while uptime and data portability clauses materially shape bargaining power.

- Integration dependence: ATS/CRM + APIs

- Lock-in: high migration cost

- Switching friction: custom workflows/data models

- Contracts: uptime & data portability drive leverage

Local labor pools and seasonality

TrueBlue depends on geographically dispersed talent pools that fluctuate seasonally, with US unemployment averaging about 4.0% in 2024 increasing competition for workers during peak construction and logistics cycles and boosting worker bargaining power. Premiums and sign-on incentives are often required to secure supply, while regional wage floors and commuting constraints create added rigidity in staffing costs and fill rates.

- Seasonal peaks raise worker leverage

- 2024 US unemployment ~4.0% intensifies competition

- Premiums/incentives needed to secure supply

- Regional wages and commute limits reduce flexibility

Supplier power tightens: ~4.0% jobless, >60% VMS

Supplier power is high: 2024 US unemployment ~4.0% tightened skilled supply, driving premiums and longer fill times (median US time‑to‑fill ~30 days) that squeeze TrueBlue margins. Over 60% of large employers use VMS/MSP, concentrating contract terms. ATS/API lock‑in (63% cite integration complexity) and dominant job boards further amplify supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| US unemployment | ~4.0% | tighter labor supply |

| VMS/MSP adoption | >60% (large employers) | concentrated access/terms |

| Median time‑to‑fill | ~30 days | longer placement cycles |

| Integration complexity | 63% | vendor lock‑in/switching cost |

What is included in the product

Comprehensive Porter’s Five Forces assessment for TrueBlue, uncovering competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers to protect and grow market share.

One-sheet Porter's Five Forces for TrueBlue that maps competitive pressures, lets you tweak force levels per scenario, and produces slide-ready visuals for faster, clearer strategic decisions.

Customers Bargaining Power

Enterprise consolidation and MSP-led buying

Large enterprise clients increasingly centralize supplier selection through MSPs, which by 2024 managed roughly half of contingent workforce spend (Staffing Industry Analysts), enforcing standardized pricing that compresses TrueBlue margins and stretches payment terms into 45–75 day windows for many staffing suppliers. Preferred supplier lists restrict volume unless TrueBlue wins via tight bids, forcing delivery of scale, KPIs and reduced unit costs to retain share.

Low switching costs across agencies

Staffing services are often seen as interchangeable, especially for general labor, so buyers exercise strong bargaining power; in 2024 TrueBlue emphasized service-level and on-site program differentiation to counter this dynamic. Clients can rebid contracts frequently with minimal transition friction, driving price competition and short contract durations (often under 12 months). Differentiation via elevated service levels, safety programs and managed onsite teams is crucial to reduce churn.

RFP pressure and rate transparency

Competitive RFPs create head-to-head rate visibility, with enterprise buyers in 2024 citing benchmark data that has driven bill-rate compressions of roughly 3–7% in staffing RFPs. Volume-for-discount structures increasingly favor the lowest-cost provider, often pressuring gross margins by 150–300 basis points. TrueBlue must balance higher win rates against disciplined margin targets to avoid eroding EBITDA.

Demand cyclicality and budget sensitivity

Client volumes swing with macro cycles, shifting negotiation power; downturns see buyers squeeze rates and cut requisitions while upcycles demand rapid scaling and fill speed without proportional price increases, creating margin pressure for TrueBlue (TBI). Volatility complicates capacity planning and scheduling across contingent workforce channels; US staffing industry revenue was about 176 billion in 2023.

- Downturns: reduced requisitions, higher rate pressure

- Upcycles: rapid scale demands, limited price uplift

- Impact: staffing volatility complicates capacity and margins

High service expectations and SLAs

Buyers demand strict compliance, safety, and performance SLAs, with a 2024 industry survey finding 68% of large purchasers enforcing financial penalties for breaches; scorecards and penalties transfer risk to suppliers and compress margins. Custom reporting and onsite support raise cost-to-serve, and while meeting SLAs improves retention, it often reduces gross margin by several percentage points.

- Buyers enforce SLAs: 68% (2024 survey)

- Penalties shift risk and compress margins

- Custom reporting/on-site raises cost-to-serve

- Compliance aids retention but tightens profitability

MSPs control ~50%; bill rates down 3-7% and margins 150-300bps

Buyers wield strong leverage via MSPs (manage ~50% contingent spend in 2024), standardized pricing and 45–75 day terms, forcing tight bids and lower margins. RFP benchmarking cut bill rates ~3–7% in 2024, pressuring gross margins by 150–300 bps; clients rebid frequently with <12‑month terms. 68% of large buyers enforce SLA penalties, raising cost‑to‑serve and shifting risk to suppliers.

| Metric | Value |

|---|---|

| MSP share (2024) | ~50% |

| Payment terms | 45–75 days |

| Bill-rate compression (2024) | 3–7% |

| Margin pressure | 150–300 bps |

| SLA penalties (2024) | 68% |

Preview Before You Purchase

TrueBlue Porter's Five Forces Analysis

This preview displays the exact TrueBlue Porter's Five Forces Analysis you'll receive after purchase—no placeholders, no mockups. The file is fully formatted, complete, and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.