Truist Financial Business Model Canvas

Unlock bank business model canvas: retail, commercial and wealth value mapped

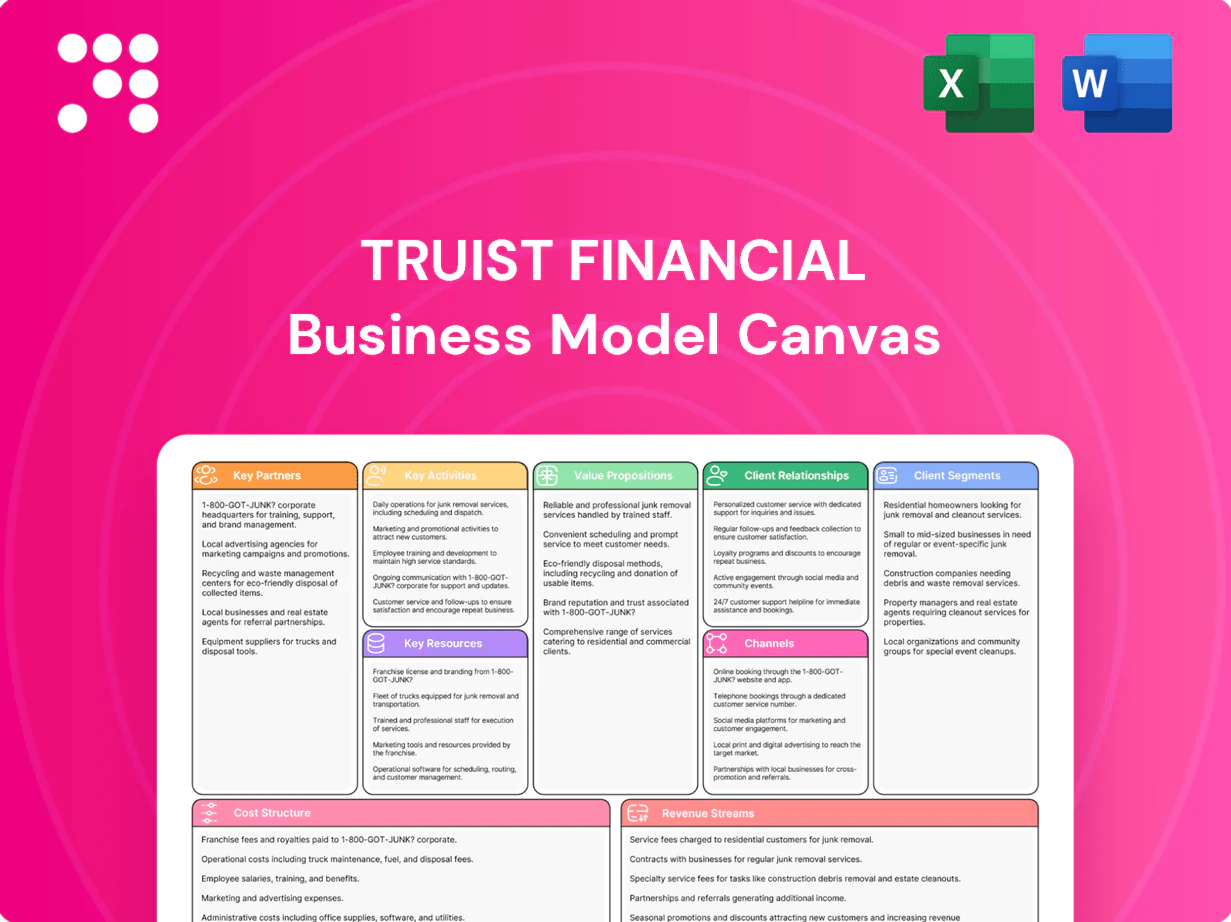

Unlock Truist Financial’s strategic blueprint with a concise Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. This 3–5 sentence snapshot highlights how Truist creates and captures value across retail, commercial and wealth channels. Ready for investors, advisors and strategists—purchase the full, editable Word and Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Payment networks and processors

Partnerships with Visa, Mastercard and major processors enable Truist to issue cards, acquire merchants and secure transactions across networks present in 200+ countries and roughly 100 million merchant locations, expanding acceptance and speeding settlement. These relationships lower fraud through tokenization and shared data, unlock co-branded products and interchange economics, and help Truist scale consumer and small-business payments.

Fintech and core technology vendors

Alliances with digital banking, core systems, cloud, data, and cybersecurity providers boost Truist platform reliability and innovation, supporting the bank that serves about 10 million households in 2024. Integration with vendors accelerates new feature launches, lowering time-to-market and enabling faster API-driven rollouts. Vendors deliver API connectivity and analytics for personalization, letting Truist blend modern UX with bank-grade controls.

Capital markets counterparties

Broker-dealers, exchanges and institutional investors provide liquidity for underwriting, syndications and secondary trading, helping Truist price deals, distribute securities and hedge risks. In 2024 Truist leveraged these partners across its roughly $600 billion balance sheet to optimize capital and improve funding costs. These relationships underpin Truist’s investment banking and treasury solutions, supporting fee and trading activities.

Insurance carriers and reinsurance partners

Ties with carriers expand Truist’s product breadth across P&C, life and specialty lines, enabling the bank-insurance arm to offer more bundled solutions to Truist’s ~11 million clients (2024). Reinsurers help manage exposure and improve capital efficiency, supporting competitive pricing, claims handling and solvency metrics.

- Carrier breadth: expanded product suite

- Reinsurance: exposure control, capital efficiency

- Pricing & claims: improved competitiveness

- Cross-sell: drives uptake across client segments

Community, real estate, and SBA partners

Local organizations, developers and SBA lenders help Truist originate small-business and mortgage loans, leveraging SBA 7(a) guarantees (up to 85% for loans ≤150,000 and 75% thereafter, max loan size 5,000,000) and down-payment assistance to expand credit access and deepen community ties while boosting CRA-qualified activity.

- Local partners: enhanced regional presence

- Developers: housing supply and mortgage origination

- SBA: guarantee leverage (7(a) up to 5,000,000)

- Outcome: stronger CRA impact, expanded credit access

Partner network accelerates APIs, cuts fraud, boosts liquidity and SBA lending for 11M

Truist’s key partners — payments networks, cloud/data vendors, capital markets counterparties, carriers and local SBA/developer allies — expand acceptance, speed innovation, provide liquidity and manage insurance exposure, supporting ~11M clients and a ~$600B balance sheet in 2024. These ties cut fraud, accelerate API rollouts, optimize funding and deepen CRA-qualified lending via SBA 7(a) (≤5,000,000).

| Partner | Metric |

|---|---|

| Visa/Mastercard | 200+ countries; ~100M merchants |

| Balance sheet | $600B (2024) |

| Clients/Households | ~11M clients; ~10M households (2024) |

What is included in the product

A comprehensive Business Model Canvas for Truist Financial outlining customer segments, value propositions, channels, revenue streams and key partners across the 9 BMC blocks, reflecting real-world operations and competitive insights for presentations and investor discussions.

Condenses Truist Financial's strategy into a digestible one-page canvas that saves hours of structuring, makes core banking components immediately visible, and is shareable/editable to relieve forecasting, alignment, and strategy-communication pain points.

Activities

Deposit gathering and liquidity management

Truist acquires, retains and prices deposits across retail, commercial and public sectors, supporting approximately $450 billion of deposits in 2024 while focusing on stable core funding. The bank manages liquidity and interest rate risk through cash operations, securities buffers and active liability repricing. It optimizes funding mix to reduce volatile wholesale funding and supports client cash needs with sweep programs and treasury services.

Lending and credit underwriting

Truist originates consumer, mortgage, small‑business, commercial, and corporate loans across a loan portfolio exceeding $200 billion. It underwrites, prices, and monitors credit risk through cycles, targeting disciplined loss rates and capital efficiency. The bank structures syndicated and asset‑based facilities for middle‑market and corporate clients. Portfolio analytics and centralized collections support risk mitigation and recovery efforts.

Advisory, wealth, and insurance services

Truist provides financial planning, brokerage, trust, and asset management across its wealth platform. It delivers M&A, capital raising, and strategic advisory to businesses, leveraging its position as the sixth-largest U.S. bank by assets in 2024. The firm offers P&C and life insurance with formal risk assessments and integrates advice across client life stages to deepen client relationships.

Risk, compliance, and cyber resilience

Operate enterprise risk, AML/BSA, and regulatory reporting across a bank holding company subject to 2024 CCAR/DFI stress testing requirements for firms above 100 billion in assets.

Conduct stress testing, model risk management, and controls while maintaining cybersecurity, fraud prevention, and resilience programs to support audit readiness and policy adherence.

- Enterprise risk & regulatory reporting

- AML/BSA monitoring

- Stress testing & model risk

- Cybersecurity, fraud & resilience

- Policy compliance & audit readiness

Digital product development and analytics

Design mobile and web experiences, payments, and embedded finance APIs to drive digital engagement and fee income across retail and commercial segments.

Use data science for personalization, dynamic pricing, and retention modeling, automating onboarding, servicing, and credit/transaction decisioning to reduce friction and cost-to-serve.

Continuously improve via A/B testing and closed-loop feedback to lift activation and lifetime value.

- Digital UX, payments, embedded APIs

- Data science: personalization, pricing, retention

- Automation: onboarding, servicing, decisioning

- Experimentation: A/B testing, feedback loops

Bank manages $450B deposits and $200B+ loan book amid rate and liquidity risk

Truist acquires, prices and retains ~$450B deposits (2024) and manages liquidity and interest‑rate risk. It originates and services a loan portfolio >$200B with underwriting, syndications and centralized collections. The bank delivers wealth, capital markets and insurance advice while operating enterprise risk, AML, stress testing, cybersecurity and digital product development.

| Activity | 2024 metric | Notes |

|---|---|---|

| Deposits | $450B | Core funding focus |

| Loans | >$200B | Consumer, mortgage, C&I |

| Rank | 6th by assets | US banks 2024 |

Full Document Unlocks After Purchase

Business Model Canvas

The Truist Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and ready-to-use—in editable Word and Excel formats. No placeholders, no surprises: what you see here is what you’ll download and own.

Unlock bank business model canvas: retail, commercial and wealth value mapped

Unlock Truist Financial’s strategic blueprint with a concise Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. This 3–5 sentence snapshot highlights how Truist creates and captures value across retail, commercial and wealth channels. Ready for investors, advisors and strategists—purchase the full, editable Word and Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Payment networks and processors

Partnerships with Visa, Mastercard and major processors enable Truist to issue cards, acquire merchants and secure transactions across networks present in 200+ countries and roughly 100 million merchant locations, expanding acceptance and speeding settlement. These relationships lower fraud through tokenization and shared data, unlock co-branded products and interchange economics, and help Truist scale consumer and small-business payments.

Fintech and core technology vendors

Alliances with digital banking, core systems, cloud, data, and cybersecurity providers boost Truist platform reliability and innovation, supporting the bank that serves about 10 million households in 2024. Integration with vendors accelerates new feature launches, lowering time-to-market and enabling faster API-driven rollouts. Vendors deliver API connectivity and analytics for personalization, letting Truist blend modern UX with bank-grade controls.

Capital markets counterparties

Broker-dealers, exchanges and institutional investors provide liquidity for underwriting, syndications and secondary trading, helping Truist price deals, distribute securities and hedge risks. In 2024 Truist leveraged these partners across its roughly $600 billion balance sheet to optimize capital and improve funding costs. These relationships underpin Truist’s investment banking and treasury solutions, supporting fee and trading activities.

Insurance carriers and reinsurance partners

Ties with carriers expand Truist’s product breadth across P&C, life and specialty lines, enabling the bank-insurance arm to offer more bundled solutions to Truist’s ~11 million clients (2024). Reinsurers help manage exposure and improve capital efficiency, supporting competitive pricing, claims handling and solvency metrics.

- Carrier breadth: expanded product suite

- Reinsurance: exposure control, capital efficiency

- Pricing & claims: improved competitiveness

- Cross-sell: drives uptake across client segments

Community, real estate, and SBA partners

Local organizations, developers and SBA lenders help Truist originate small-business and mortgage loans, leveraging SBA 7(a) guarantees (up to 85% for loans ≤150,000 and 75% thereafter, max loan size 5,000,000) and down-payment assistance to expand credit access and deepen community ties while boosting CRA-qualified activity.

- Local partners: enhanced regional presence

- Developers: housing supply and mortgage origination

- SBA: guarantee leverage (7(a) up to 5,000,000)

- Outcome: stronger CRA impact, expanded credit access

Partner network accelerates APIs, cuts fraud, boosts liquidity and SBA lending for 11M

Truist’s key partners — payments networks, cloud/data vendors, capital markets counterparties, carriers and local SBA/developer allies — expand acceptance, speed innovation, provide liquidity and manage insurance exposure, supporting ~11M clients and a ~$600B balance sheet in 2024. These ties cut fraud, accelerate API rollouts, optimize funding and deepen CRA-qualified lending via SBA 7(a) (≤5,000,000).

| Partner | Metric |

|---|---|

| Visa/Mastercard | 200+ countries; ~100M merchants |

| Balance sheet | $600B (2024) |

| Clients/Households | ~11M clients; ~10M households (2024) |

What is included in the product

A comprehensive Business Model Canvas for Truist Financial outlining customer segments, value propositions, channels, revenue streams and key partners across the 9 BMC blocks, reflecting real-world operations and competitive insights for presentations and investor discussions.

Condenses Truist Financial's strategy into a digestible one-page canvas that saves hours of structuring, makes core banking components immediately visible, and is shareable/editable to relieve forecasting, alignment, and strategy-communication pain points.

Activities

Deposit gathering and liquidity management

Truist acquires, retains and prices deposits across retail, commercial and public sectors, supporting approximately $450 billion of deposits in 2024 while focusing on stable core funding. The bank manages liquidity and interest rate risk through cash operations, securities buffers and active liability repricing. It optimizes funding mix to reduce volatile wholesale funding and supports client cash needs with sweep programs and treasury services.

Lending and credit underwriting

Truist originates consumer, mortgage, small‑business, commercial, and corporate loans across a loan portfolio exceeding $200 billion. It underwrites, prices, and monitors credit risk through cycles, targeting disciplined loss rates and capital efficiency. The bank structures syndicated and asset‑based facilities for middle‑market and corporate clients. Portfolio analytics and centralized collections support risk mitigation and recovery efforts.

Advisory, wealth, and insurance services

Truist provides financial planning, brokerage, trust, and asset management across its wealth platform. It delivers M&A, capital raising, and strategic advisory to businesses, leveraging its position as the sixth-largest U.S. bank by assets in 2024. The firm offers P&C and life insurance with formal risk assessments and integrates advice across client life stages to deepen client relationships.

Risk, compliance, and cyber resilience

Operate enterprise risk, AML/BSA, and regulatory reporting across a bank holding company subject to 2024 CCAR/DFI stress testing requirements for firms above 100 billion in assets.

Conduct stress testing, model risk management, and controls while maintaining cybersecurity, fraud prevention, and resilience programs to support audit readiness and policy adherence.

- Enterprise risk & regulatory reporting

- AML/BSA monitoring

- Stress testing & model risk

- Cybersecurity, fraud & resilience

- Policy compliance & audit readiness

Digital product development and analytics

Design mobile and web experiences, payments, and embedded finance APIs to drive digital engagement and fee income across retail and commercial segments.

Use data science for personalization, dynamic pricing, and retention modeling, automating onboarding, servicing, and credit/transaction decisioning to reduce friction and cost-to-serve.

Continuously improve via A/B testing and closed-loop feedback to lift activation and lifetime value.

- Digital UX, payments, embedded APIs

- Data science: personalization, pricing, retention

- Automation: onboarding, servicing, decisioning

- Experimentation: A/B testing, feedback loops

Bank manages $450B deposits and $200B+ loan book amid rate and liquidity risk

Truist acquires, prices and retains ~$450B deposits (2024) and manages liquidity and interest‑rate risk. It originates and services a loan portfolio >$200B with underwriting, syndications and centralized collections. The bank delivers wealth, capital markets and insurance advice while operating enterprise risk, AML, stress testing, cybersecurity and digital product development.

| Activity | 2024 metric | Notes |

|---|---|---|

| Deposits | $450B | Core funding focus |

| Loans | >$200B | Consumer, mortgage, C&I |

| Rank | 6th by assets | US banks 2024 |

Full Document Unlocks After Purchase

Business Model Canvas

The Truist Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and ready-to-use—in editable Word and Excel formats. No placeholders, no surprises: what you see here is what you’ll download and own.

Original: $10.00

-65%$10.00

$3.50Description

Unlock bank business model canvas: retail, commercial and wealth value mapped

Unlock Truist Financial’s strategic blueprint with a concise Business Model Canvas that maps value propositions, customer segments, revenue streams and key partnerships. This 3–5 sentence snapshot highlights how Truist creates and captures value across retail, commercial and wealth channels. Ready for investors, advisors and strategists—purchase the full, editable Word and Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Payment networks and processors

Partnerships with Visa, Mastercard and major processors enable Truist to issue cards, acquire merchants and secure transactions across networks present in 200+ countries and roughly 100 million merchant locations, expanding acceptance and speeding settlement. These relationships lower fraud through tokenization and shared data, unlock co-branded products and interchange economics, and help Truist scale consumer and small-business payments.

Fintech and core technology vendors

Alliances with digital banking, core systems, cloud, data, and cybersecurity providers boost Truist platform reliability and innovation, supporting the bank that serves about 10 million households in 2024. Integration with vendors accelerates new feature launches, lowering time-to-market and enabling faster API-driven rollouts. Vendors deliver API connectivity and analytics for personalization, letting Truist blend modern UX with bank-grade controls.

Capital markets counterparties

Broker-dealers, exchanges and institutional investors provide liquidity for underwriting, syndications and secondary trading, helping Truist price deals, distribute securities and hedge risks. In 2024 Truist leveraged these partners across its roughly $600 billion balance sheet to optimize capital and improve funding costs. These relationships underpin Truist’s investment banking and treasury solutions, supporting fee and trading activities.

Insurance carriers and reinsurance partners

Ties with carriers expand Truist’s product breadth across P&C, life and specialty lines, enabling the bank-insurance arm to offer more bundled solutions to Truist’s ~11 million clients (2024). Reinsurers help manage exposure and improve capital efficiency, supporting competitive pricing, claims handling and solvency metrics.

- Carrier breadth: expanded product suite

- Reinsurance: exposure control, capital efficiency

- Pricing & claims: improved competitiveness

- Cross-sell: drives uptake across client segments

Community, real estate, and SBA partners

Local organizations, developers and SBA lenders help Truist originate small-business and mortgage loans, leveraging SBA 7(a) guarantees (up to 85% for loans ≤150,000 and 75% thereafter, max loan size 5,000,000) and down-payment assistance to expand credit access and deepen community ties while boosting CRA-qualified activity.

- Local partners: enhanced regional presence

- Developers: housing supply and mortgage origination

- SBA: guarantee leverage (7(a) up to 5,000,000)

- Outcome: stronger CRA impact, expanded credit access

Partner network accelerates APIs, cuts fraud, boosts liquidity and SBA lending for 11M

Truist’s key partners — payments networks, cloud/data vendors, capital markets counterparties, carriers and local SBA/developer allies — expand acceptance, speed innovation, provide liquidity and manage insurance exposure, supporting ~11M clients and a ~$600B balance sheet in 2024. These ties cut fraud, accelerate API rollouts, optimize funding and deepen CRA-qualified lending via SBA 7(a) (≤5,000,000).

| Partner | Metric |

|---|---|

| Visa/Mastercard | 200+ countries; ~100M merchants |

| Balance sheet | $600B (2024) |

| Clients/Households | ~11M clients; ~10M households (2024) |

What is included in the product

A comprehensive Business Model Canvas for Truist Financial outlining customer segments, value propositions, channels, revenue streams and key partners across the 9 BMC blocks, reflecting real-world operations and competitive insights for presentations and investor discussions.

Condenses Truist Financial's strategy into a digestible one-page canvas that saves hours of structuring, makes core banking components immediately visible, and is shareable/editable to relieve forecasting, alignment, and strategy-communication pain points.

Activities

Deposit gathering and liquidity management

Truist acquires, retains and prices deposits across retail, commercial and public sectors, supporting approximately $450 billion of deposits in 2024 while focusing on stable core funding. The bank manages liquidity and interest rate risk through cash operations, securities buffers and active liability repricing. It optimizes funding mix to reduce volatile wholesale funding and supports client cash needs with sweep programs and treasury services.

Lending and credit underwriting

Truist originates consumer, mortgage, small‑business, commercial, and corporate loans across a loan portfolio exceeding $200 billion. It underwrites, prices, and monitors credit risk through cycles, targeting disciplined loss rates and capital efficiency. The bank structures syndicated and asset‑based facilities for middle‑market and corporate clients. Portfolio analytics and centralized collections support risk mitigation and recovery efforts.

Advisory, wealth, and insurance services

Truist provides financial planning, brokerage, trust, and asset management across its wealth platform. It delivers M&A, capital raising, and strategic advisory to businesses, leveraging its position as the sixth-largest U.S. bank by assets in 2024. The firm offers P&C and life insurance with formal risk assessments and integrates advice across client life stages to deepen client relationships.

Risk, compliance, and cyber resilience

Operate enterprise risk, AML/BSA, and regulatory reporting across a bank holding company subject to 2024 CCAR/DFI stress testing requirements for firms above 100 billion in assets.

Conduct stress testing, model risk management, and controls while maintaining cybersecurity, fraud prevention, and resilience programs to support audit readiness and policy adherence.

- Enterprise risk & regulatory reporting

- AML/BSA monitoring

- Stress testing & model risk

- Cybersecurity, fraud & resilience

- Policy compliance & audit readiness

Digital product development and analytics

Design mobile and web experiences, payments, and embedded finance APIs to drive digital engagement and fee income across retail and commercial segments.

Use data science for personalization, dynamic pricing, and retention modeling, automating onboarding, servicing, and credit/transaction decisioning to reduce friction and cost-to-serve.

Continuously improve via A/B testing and closed-loop feedback to lift activation and lifetime value.

- Digital UX, payments, embedded APIs

- Data science: personalization, pricing, retention

- Automation: onboarding, servicing, decisioning

- Experimentation: A/B testing, feedback loops

Bank manages $450B deposits and $200B+ loan book amid rate and liquidity risk

Truist acquires, prices and retains ~$450B deposits (2024) and manages liquidity and interest‑rate risk. It originates and services a loan portfolio >$200B with underwriting, syndications and centralized collections. The bank delivers wealth, capital markets and insurance advice while operating enterprise risk, AML, stress testing, cybersecurity and digital product development.

| Activity | 2024 metric | Notes |

|---|---|---|

| Deposits | $450B | Core funding focus |

| Loans | >$200B | Consumer, mortgage, C&I |

| Rank | 6th by assets | US banks 2024 |

Full Document Unlocks After Purchase

Business Model Canvas

The Truist Financial Business Model Canvas you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and ready-to-use—in editable Word and Excel formats. No placeholders, no surprises: what you see here is what you’ll download and own.