Trustpilot Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

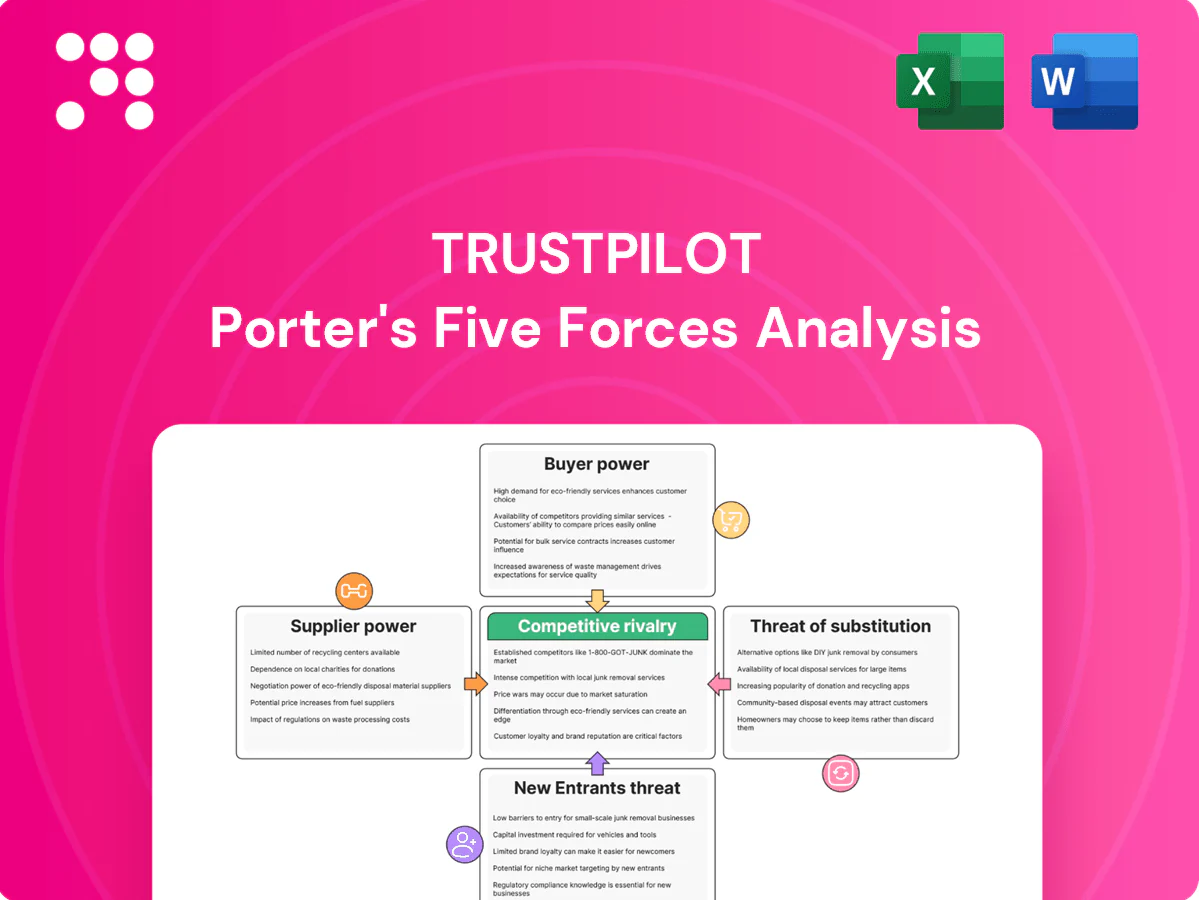

Trustpilot faces intense competitive rivalry, strong buyer influence via platform choice, modest supplier leverage, and notable substitute threats from alternative review channels; network effects and reputation risk heighten strategic sensitivity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trustpilot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consumer reviewers as content suppliers

Trustpilot depends on a steady flow of genuine reviews to sustain relevance and SEO, hosting over 100 million reviews and attracting roughly 38 million monthly unique visitors (2023 data). Individual reviewers have low direct bargaining power, yet collectively they determine platform value and credibility. Incentive design and public trust initiatives alongside transparency reports must balance volume with authenticity; rising review fatigue or distrust would tighten content quality and raise effective supplier power.

Search engines as traffic gatekeepers

Google and other search engines—with Google holding about 92% global search market share in 2024 per StatCounter—function as critical distribution suppliers through rankings and rich snippets. Organic search drives roughly 53% of website traffic (BrightEdge), so algorithm shifts can materially alter referral volumes and acquisition costs for review platforms. Limited viable alternatives give search platforms high leverage, forcing Trustpilot to invest in SEO, schema compliance, and content quality to mitigate dependency.

Cloud, data, and tooling vendors

Hosting, CDN, AI/ML moderation and analytics vendors underpin Trustpilot’s uptime and fraud detection. The top three cloud providers control roughly 66% of the global market (Canalys/Gartner 2024), giving suppliers scope to raise prices or impose usage caps. Multi‑cloud, in‑house models and long‑term contracts reduce that leverage. Switching remains hard due to performance, latency and costly model retraining.

Payment and identity verification partners

Payment processors and KYC/verification providers shape onboarding friction and fraud control; compliance regimes like 2024 EU PSD2 SCA and global AML requirements keep them moderately powerful despite commoditization. Redundancy and negotiated fees reduce dependence, but localized payment preferences and alternative rails limit switches. Outages or policy shifts can halt collections and spike chargebacks.

- Moderate power: compliance+chargeback risk

- Mitigants: redundancy, negotiated fees

- Constraint: localized payment preferences

- Risk: outages/policy shifts disrupt revenue

App stores and browser ecosystems

App stores and browser ecosystem policies shape mobile reach, push notifications, and cross‑site tracking; Apple and Google app commissions remain 15–30% (2024) and platform rules tightened review, data access, and attribution controls after iOS privacy changes. Compliance costs and revenue sharing create supplier leverage over pricing and features, while web‑first approaches and PWAs reduce but do not eliminate dependency.

- Distribution control: app stores dominate mobile installs

- Monetary leverage: 15–30% commission (2024)

- Privacy rules: tighter review, data, attribution limits

- Mitigation: PWAs/web‑first partially offset dependency

Review platform faces concentrated search dependency and cloud/app vendor leverage

Trustpilot faces moderate supplier power: individual reviewers low power but collectively decisive; Google search (≈92% share in 2024) drives ~53% organic traffic, creating high distribution leverage. Cloud vendors (top‑3 ≈66% market share, 2024) and app stores (15–30% commission, 2024) add pricing and policy constraints mitigated via redundancy and SEO investment.

| Supplier | Metric |

|---|---|

| Google/search | 92% share (2024); ~53% traffic |

| Cloud providers | Top‑3 ≈66% (2024) |

| App stores | 15–30% commission (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Trustpilot that uncovers key competitive drivers, customer influence, supplier dynamics and entry barriers, while identifying disruptive threats and substitutes impacting pricing, profitability and market share—fully editable for incorporation into reports or investor materials.

A one-sheet Porter's Five Forces for Trustpilot that clarifies competitive pressures at a glance, with customizable pressure sliders and an instant radar chart—easy to drop into decks, adapt to new data, and share with non-finance stakeholders.

Customers Bargaining Power

SMBs with price sensitivity

SMBs buy Trustpilot subscriptions to manage profiles and collect reviews, but with SMEs representing roughly 99% of businesses in the EU/UK (Eurostat/ONS), customer volume is large yet highly price-sensitive. Abundant alternatives and freemium tiers amplify sensitivity, driving churn risk. Switching costs are moderate—integrations and historical reviews raise costs but are typically not prohibitive. Promotions and tiered packaging are therefore essential to defend ARPU.

Enterprises with negotiation leverage

Larger enterprise customers demand advanced analytics, SLAs and integrations, often negotiating discounts up to 20% and custom security reviews that can extend sales cycles by 30–90 days. Their volume and reference value drive roadmap influence and can concentrate >40% of ARR in top-tier accounts. Landing-and-expanding lowers churn but increases buyer power at the top end, shifting pricing leverage toward enterprises.

Multi-homing across platforms

Businesses commonly publish reviews across Google (Google Maps has over 1 billion monthly users), Yelp and marketplace review systems, so multi-homing lowers dependency on any single provider and widens buyer options. This raises customer bargaining power as firms can pick platforms for visibility and SEO lift. Trustpilot must compete on credibility, search-engine impact and integrations. Stronger moderation policies and deeper APIs reduce direct comparability.

Outcome-driven purchasing

Buyers now make outcome-driven purchases, prioritizing traffic, conversion lift, and reputation defense; 2024 case studies report conversion uplifts up to 60% when review signals are shown, and clear ROI evidence strengthens sellers ability to hold premium pricing while weak attribution erodes it. Verified badges, case studies, and on-site widgets quantify impact and reduce churn risk; without measurable outcomes churn exposure rises sharply.

- Traffic: on-site review widgets increase sessions and time on site

- Conversion lift: case studies report up to 60% uplift (2024)

- Reputation: verified badges improve trust and repeat purchase

- Risk: weak attribution = higher churn

Switching and data portability

Exportable reviews, widgets and APIs boost Trustpilot stickiness, while rivals offering seamless import tools and CSV/API migration reduce switching barriers.

- Exportability: enables merchant exit

- Imports: lowers switching costs

- Exclusive badges/ecosystem: increases lock-in

- Regulation: GDPR Article 20 and EU DMA enforcement in 2024 strengthen portability

SMEs ~99% of firms; enterprises get up to 20% discounts

Customer bargaining power is high: SMEs (~99% of EU/UK firms) are price-sensitive and multi-home, while enterprises negotiate up to 20% discounts and can represent >40% of ARR. Multi-platform publishing (Google Maps ~1B monthly users) and exportability lower switching costs; verified badges and measured ROI (case studies show up to 60% conversion uplift in 2024) help retain pricing power.

| Metric | 2024 Value |

|---|---|

| SME share (EU/UK) | ~99% |

| Enterprise discount ceiling | up to 20% |

| Top-account ARR concentration | >40% |

| Conversion uplift (case studies) | up to 60% |

Same Document Delivered

Trustpilot Porter's Five Forces Analysis

This preview is the exact Trustpilot Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use the moment you complete payment. What you see here is the final deliverable, complete and professional.

A Must-Have Tool for Decision-Makers

Trustpilot faces intense competitive rivalry, strong buyer influence via platform choice, modest supplier leverage, and notable substitute threats from alternative review channels; network effects and reputation risk heighten strategic sensitivity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trustpilot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consumer reviewers as content suppliers

Trustpilot depends on a steady flow of genuine reviews to sustain relevance and SEO, hosting over 100 million reviews and attracting roughly 38 million monthly unique visitors (2023 data). Individual reviewers have low direct bargaining power, yet collectively they determine platform value and credibility. Incentive design and public trust initiatives alongside transparency reports must balance volume with authenticity; rising review fatigue or distrust would tighten content quality and raise effective supplier power.

Search engines as traffic gatekeepers

Google and other search engines—with Google holding about 92% global search market share in 2024 per StatCounter—function as critical distribution suppliers through rankings and rich snippets. Organic search drives roughly 53% of website traffic (BrightEdge), so algorithm shifts can materially alter referral volumes and acquisition costs for review platforms. Limited viable alternatives give search platforms high leverage, forcing Trustpilot to invest in SEO, schema compliance, and content quality to mitigate dependency.

Cloud, data, and tooling vendors

Hosting, CDN, AI/ML moderation and analytics vendors underpin Trustpilot’s uptime and fraud detection. The top three cloud providers control roughly 66% of the global market (Canalys/Gartner 2024), giving suppliers scope to raise prices or impose usage caps. Multi‑cloud, in‑house models and long‑term contracts reduce that leverage. Switching remains hard due to performance, latency and costly model retraining.

Payment and identity verification partners

Payment processors and KYC/verification providers shape onboarding friction and fraud control; compliance regimes like 2024 EU PSD2 SCA and global AML requirements keep them moderately powerful despite commoditization. Redundancy and negotiated fees reduce dependence, but localized payment preferences and alternative rails limit switches. Outages or policy shifts can halt collections and spike chargebacks.

- Moderate power: compliance+chargeback risk

- Mitigants: redundancy, negotiated fees

- Constraint: localized payment preferences

- Risk: outages/policy shifts disrupt revenue

App stores and browser ecosystems

App stores and browser ecosystem policies shape mobile reach, push notifications, and cross‑site tracking; Apple and Google app commissions remain 15–30% (2024) and platform rules tightened review, data access, and attribution controls after iOS privacy changes. Compliance costs and revenue sharing create supplier leverage over pricing and features, while web‑first approaches and PWAs reduce but do not eliminate dependency.

- Distribution control: app stores dominate mobile installs

- Monetary leverage: 15–30% commission (2024)

- Privacy rules: tighter review, data, attribution limits

- Mitigation: PWAs/web‑first partially offset dependency

Review platform faces concentrated search dependency and cloud/app vendor leverage

Trustpilot faces moderate supplier power: individual reviewers low power but collectively decisive; Google search (≈92% share in 2024) drives ~53% organic traffic, creating high distribution leverage. Cloud vendors (top‑3 ≈66% market share, 2024) and app stores (15–30% commission, 2024) add pricing and policy constraints mitigated via redundancy and SEO investment.

| Supplier | Metric |

|---|---|

| Google/search | 92% share (2024); ~53% traffic |

| Cloud providers | Top‑3 ≈66% (2024) |

| App stores | 15–30% commission (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Trustpilot that uncovers key competitive drivers, customer influence, supplier dynamics and entry barriers, while identifying disruptive threats and substitutes impacting pricing, profitability and market share—fully editable for incorporation into reports or investor materials.

A one-sheet Porter's Five Forces for Trustpilot that clarifies competitive pressures at a glance, with customizable pressure sliders and an instant radar chart—easy to drop into decks, adapt to new data, and share with non-finance stakeholders.

Customers Bargaining Power

SMBs with price sensitivity

SMBs buy Trustpilot subscriptions to manage profiles and collect reviews, but with SMEs representing roughly 99% of businesses in the EU/UK (Eurostat/ONS), customer volume is large yet highly price-sensitive. Abundant alternatives and freemium tiers amplify sensitivity, driving churn risk. Switching costs are moderate—integrations and historical reviews raise costs but are typically not prohibitive. Promotions and tiered packaging are therefore essential to defend ARPU.

Enterprises with negotiation leverage

Larger enterprise customers demand advanced analytics, SLAs and integrations, often negotiating discounts up to 20% and custom security reviews that can extend sales cycles by 30–90 days. Their volume and reference value drive roadmap influence and can concentrate >40% of ARR in top-tier accounts. Landing-and-expanding lowers churn but increases buyer power at the top end, shifting pricing leverage toward enterprises.

Multi-homing across platforms

Businesses commonly publish reviews across Google (Google Maps has over 1 billion monthly users), Yelp and marketplace review systems, so multi-homing lowers dependency on any single provider and widens buyer options. This raises customer bargaining power as firms can pick platforms for visibility and SEO lift. Trustpilot must compete on credibility, search-engine impact and integrations. Stronger moderation policies and deeper APIs reduce direct comparability.

Outcome-driven purchasing

Buyers now make outcome-driven purchases, prioritizing traffic, conversion lift, and reputation defense; 2024 case studies report conversion uplifts up to 60% when review signals are shown, and clear ROI evidence strengthens sellers ability to hold premium pricing while weak attribution erodes it. Verified badges, case studies, and on-site widgets quantify impact and reduce churn risk; without measurable outcomes churn exposure rises sharply.

- Traffic: on-site review widgets increase sessions and time on site

- Conversion lift: case studies report up to 60% uplift (2024)

- Reputation: verified badges improve trust and repeat purchase

- Risk: weak attribution = higher churn

Switching and data portability

Exportable reviews, widgets and APIs boost Trustpilot stickiness, while rivals offering seamless import tools and CSV/API migration reduce switching barriers.

- Exportability: enables merchant exit

- Imports: lowers switching costs

- Exclusive badges/ecosystem: increases lock-in

- Regulation: GDPR Article 20 and EU DMA enforcement in 2024 strengthen portability

SMEs ~99% of firms; enterprises get up to 20% discounts

Customer bargaining power is high: SMEs (~99% of EU/UK firms) are price-sensitive and multi-home, while enterprises negotiate up to 20% discounts and can represent >40% of ARR. Multi-platform publishing (Google Maps ~1B monthly users) and exportability lower switching costs; verified badges and measured ROI (case studies show up to 60% conversion uplift in 2024) help retain pricing power.

| Metric | 2024 Value |

|---|---|

| SME share (EU/UK) | ~99% |

| Enterprise discount ceiling | up to 20% |

| Top-account ARR concentration | >40% |

| Conversion uplift (case studies) | up to 60% |

Same Document Delivered

Trustpilot Porter's Five Forces Analysis

This preview is the exact Trustpilot Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use the moment you complete payment. What you see here is the final deliverable, complete and professional.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Trustpilot faces intense competitive rivalry, strong buyer influence via platform choice, modest supplier leverage, and notable substitute threats from alternative review channels; network effects and reputation risk heighten strategic sensitivity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trustpilot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consumer reviewers as content suppliers

Trustpilot depends on a steady flow of genuine reviews to sustain relevance and SEO, hosting over 100 million reviews and attracting roughly 38 million monthly unique visitors (2023 data). Individual reviewers have low direct bargaining power, yet collectively they determine platform value and credibility. Incentive design and public trust initiatives alongside transparency reports must balance volume with authenticity; rising review fatigue or distrust would tighten content quality and raise effective supplier power.

Search engines as traffic gatekeepers

Google and other search engines—with Google holding about 92% global search market share in 2024 per StatCounter—function as critical distribution suppliers through rankings and rich snippets. Organic search drives roughly 53% of website traffic (BrightEdge), so algorithm shifts can materially alter referral volumes and acquisition costs for review platforms. Limited viable alternatives give search platforms high leverage, forcing Trustpilot to invest in SEO, schema compliance, and content quality to mitigate dependency.

Cloud, data, and tooling vendors

Hosting, CDN, AI/ML moderation and analytics vendors underpin Trustpilot’s uptime and fraud detection. The top three cloud providers control roughly 66% of the global market (Canalys/Gartner 2024), giving suppliers scope to raise prices or impose usage caps. Multi‑cloud, in‑house models and long‑term contracts reduce that leverage. Switching remains hard due to performance, latency and costly model retraining.

Payment and identity verification partners

Payment processors and KYC/verification providers shape onboarding friction and fraud control; compliance regimes like 2024 EU PSD2 SCA and global AML requirements keep them moderately powerful despite commoditization. Redundancy and negotiated fees reduce dependence, but localized payment preferences and alternative rails limit switches. Outages or policy shifts can halt collections and spike chargebacks.

- Moderate power: compliance+chargeback risk

- Mitigants: redundancy, negotiated fees

- Constraint: localized payment preferences

- Risk: outages/policy shifts disrupt revenue

App stores and browser ecosystems

App stores and browser ecosystem policies shape mobile reach, push notifications, and cross‑site tracking; Apple and Google app commissions remain 15–30% (2024) and platform rules tightened review, data access, and attribution controls after iOS privacy changes. Compliance costs and revenue sharing create supplier leverage over pricing and features, while web‑first approaches and PWAs reduce but do not eliminate dependency.

- Distribution control: app stores dominate mobile installs

- Monetary leverage: 15–30% commission (2024)

- Privacy rules: tighter review, data, attribution limits

- Mitigation: PWAs/web‑first partially offset dependency

Review platform faces concentrated search dependency and cloud/app vendor leverage

Trustpilot faces moderate supplier power: individual reviewers low power but collectively decisive; Google search (≈92% share in 2024) drives ~53% organic traffic, creating high distribution leverage. Cloud vendors (top‑3 ≈66% market share, 2024) and app stores (15–30% commission, 2024) add pricing and policy constraints mitigated via redundancy and SEO investment.

| Supplier | Metric |

|---|---|

| Google/search | 92% share (2024); ~53% traffic |

| Cloud providers | Top‑3 ≈66% (2024) |

| App stores | 15–30% commission (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Trustpilot that uncovers key competitive drivers, customer influence, supplier dynamics and entry barriers, while identifying disruptive threats and substitutes impacting pricing, profitability and market share—fully editable for incorporation into reports or investor materials.

A one-sheet Porter's Five Forces for Trustpilot that clarifies competitive pressures at a glance, with customizable pressure sliders and an instant radar chart—easy to drop into decks, adapt to new data, and share with non-finance stakeholders.

Customers Bargaining Power

SMBs with price sensitivity

SMBs buy Trustpilot subscriptions to manage profiles and collect reviews, but with SMEs representing roughly 99% of businesses in the EU/UK (Eurostat/ONS), customer volume is large yet highly price-sensitive. Abundant alternatives and freemium tiers amplify sensitivity, driving churn risk. Switching costs are moderate—integrations and historical reviews raise costs but are typically not prohibitive. Promotions and tiered packaging are therefore essential to defend ARPU.

Enterprises with negotiation leverage

Larger enterprise customers demand advanced analytics, SLAs and integrations, often negotiating discounts up to 20% and custom security reviews that can extend sales cycles by 30–90 days. Their volume and reference value drive roadmap influence and can concentrate >40% of ARR in top-tier accounts. Landing-and-expanding lowers churn but increases buyer power at the top end, shifting pricing leverage toward enterprises.

Multi-homing across platforms

Businesses commonly publish reviews across Google (Google Maps has over 1 billion monthly users), Yelp and marketplace review systems, so multi-homing lowers dependency on any single provider and widens buyer options. This raises customer bargaining power as firms can pick platforms for visibility and SEO lift. Trustpilot must compete on credibility, search-engine impact and integrations. Stronger moderation policies and deeper APIs reduce direct comparability.

Outcome-driven purchasing

Buyers now make outcome-driven purchases, prioritizing traffic, conversion lift, and reputation defense; 2024 case studies report conversion uplifts up to 60% when review signals are shown, and clear ROI evidence strengthens sellers ability to hold premium pricing while weak attribution erodes it. Verified badges, case studies, and on-site widgets quantify impact and reduce churn risk; without measurable outcomes churn exposure rises sharply.

- Traffic: on-site review widgets increase sessions and time on site

- Conversion lift: case studies report up to 60% uplift (2024)

- Reputation: verified badges improve trust and repeat purchase

- Risk: weak attribution = higher churn

Switching and data portability

Exportable reviews, widgets and APIs boost Trustpilot stickiness, while rivals offering seamless import tools and CSV/API migration reduce switching barriers.

- Exportability: enables merchant exit

- Imports: lowers switching costs

- Exclusive badges/ecosystem: increases lock-in

- Regulation: GDPR Article 20 and EU DMA enforcement in 2024 strengthen portability

SMEs ~99% of firms; enterprises get up to 20% discounts

Customer bargaining power is high: SMEs (~99% of EU/UK firms) are price-sensitive and multi-home, while enterprises negotiate up to 20% discounts and can represent >40% of ARR. Multi-platform publishing (Google Maps ~1B monthly users) and exportability lower switching costs; verified badges and measured ROI (case studies show up to 60% conversion uplift in 2024) help retain pricing power.

| Metric | 2024 Value |

|---|---|

| SME share (EU/UK) | ~99% |

| Enterprise discount ceiling | up to 20% |

| Top-account ARR concentration | >40% |

| Conversion uplift (case studies) | up to 60% |

Same Document Delivered

Trustpilot Porter's Five Forces Analysis

This preview is the exact Trustpilot Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use the moment you complete payment. What you see here is the final deliverable, complete and professional.