TSRC Porter's Five Forces Analysis

Don't Miss the Bigger Picture

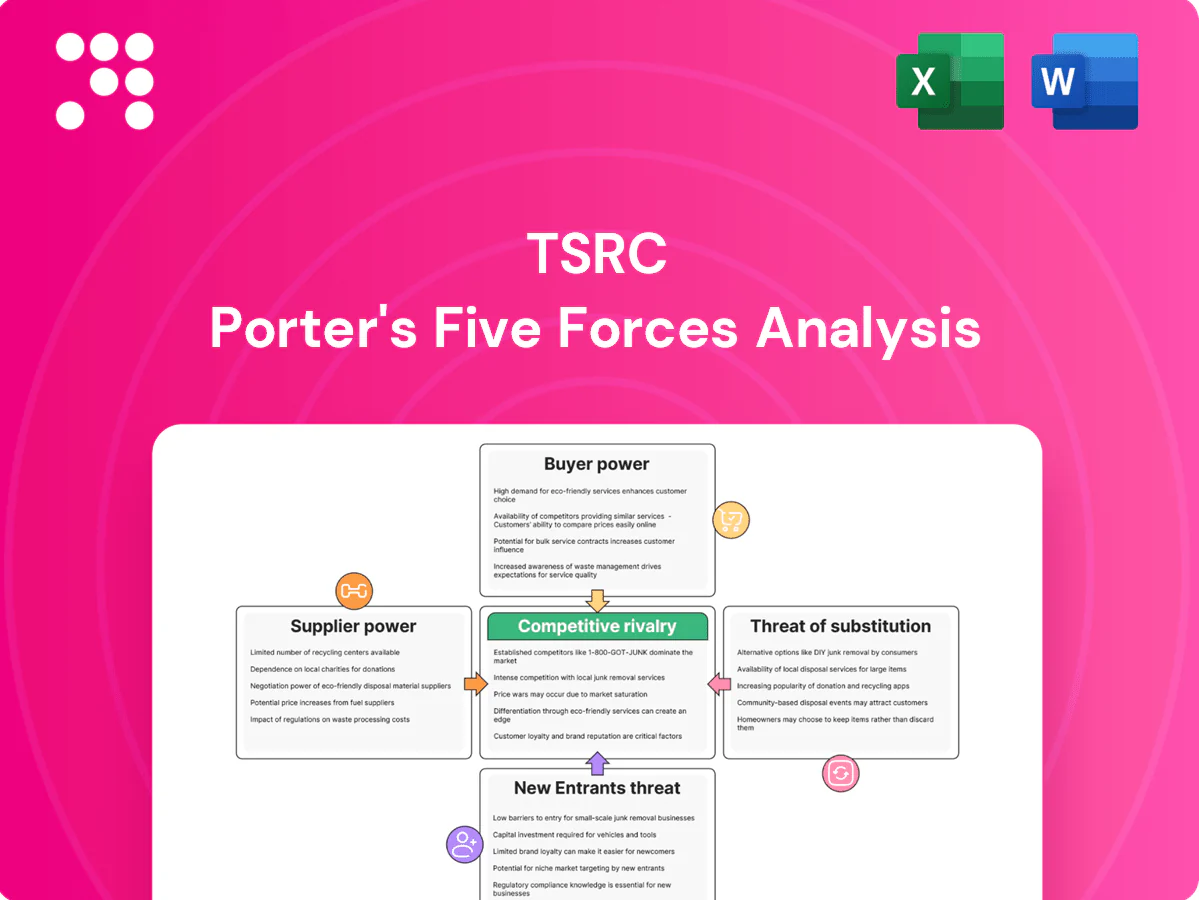

TSRC faces evolving competitive dynamics driven by raw-material costs, concentrated suppliers, and increasing downstream buyer sophistication; this snapshot highlights key pressures but skips detailed intensities and implications. The full Porter's Five Forces Analysis quantifies each force, includes visuals and scenario impacts, and maps strategic responses. Unlock the complete report for consultant-grade insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Feedstock concentration (butadiene, styrene)

TSRC relies on a concentrated upstream base—roughly three major petrochemical producers supply most butadiene and styrene needs, so 2024 regional cracker outages and sub-90% utilization spikes tightened availability and lifted spot premiums. Integrated suppliers gained pricing leverage, while TSRC partially mitigates risk through multi-sourcing and geographic diversification, though exposure to feedstock volatility remains.

Price volatility and oil/NAF linkage

Monomer prices track crude and naphtha dynamics — Brent averaged roughly 85 USD/bbl in 2024 — driving sharp input-cost swings for TSRC. Suppliers can pass spikes through quickly, squeezing margins when customer pass-through lags. Hedging and formula pricing mitigate but do not eliminate exposure, and when naphtha spreads tighten in 2024 tight markets amplified supplier bargaining power.

Logistics and regional proximity

Elastomer feedstocks are bulk chemicals highly sensitive to freight and storage constraints, a vulnerability TSRC faced in 2024. Suppliers located close to TSRC plants or owning captive pipelines/terminals gain bargaining clout via reliability and lower logistics cost. Port congestion or geopolitical disruptions can force premium sourcing, and TSRC’s global footprint helps rebalance supply but switching suppliers entails material friction and lead times.

Limited spec flexibility, qualification needs

Process recipes demand tightly controlled monomer specs, so qualifying new suppliers typically takes 6–12 months and often costs in the hundreds of thousands of dollars, raising switching costs and giving incumbents leverage; any supplier change risks product-performance drift despite dual-qualification efforts and finite qualified-supplier capacity.

- Consistent monomer specs required

- Qualification: 6–12 months, ~hundreds k$

- High switching costs, incumbent influence

- Dual-qualification mitigates but capacity limited

Integration and ESG compliance pressure

Integrated petrochemical majors can leverage broader portfolios and robust sustainability documentation to differentiate; EU CSRD coverage expanded to large firms in 2024, raising formal reporting expectations. Stricter ESG and emissions reporting increases reliance on suppliers with traceability, adding dependency, while compliance premiums and certification costs tilt negotiating power toward well‑capitalized upstream players.

- Portfolio scale advantage

- CSRD 2024: higher reporting bar

- Traceability raises supplier dependency

- Compliance premiums favor large suppliers

Supply squeeze: ~3 upstreams, crackers sub-90%, Brent ~85 USD/bbl

TSRC relies on roughly three upstream petrochemical majors; 2024 regional cracker outages and sub-90% utilization tightened availability and raised spot premiums. Brent averaged ~85 USD/bbl in 2024, amplifying feedstock cost pass-through and squeezing margins despite hedging. Supplier qualification takes 6–12 months and ~100–500k USD, creating high switching costs and sustained supplier leverage.

| Metric | 2024 value |

|---|---|

| Major suppliers | ~3 |

| Brent avg | ~85 USD/bbl |

| Cracker util. | <90% (regional outages) |

| Qualification time | 6–12 months |

| Qualification cost | 100–500k USD |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes tailored exclusively for TSRC; identifies disruptive forces and emerging threats that affect market share and pricing. Fully editable in Word for easy inclusion in investor materials, strategy decks, or academic projects.

One-sheet TSRC Porter’s Five Forces synthesizes competitive pressure into actionable insights for faster strategic decisions, reducing time spent piecing disparate analyses together. Drag-and-drop inputs and a radar visualization make it simple to update scenarios and communicate risk to stakeholders.

Customers Bargaining Power

Large tire and OEM buyers with scale

TSRC serves global tire makers and auto supply chains that purchase in very high volumes; the global tire market was valued at about $266 billion in 2024, underpinning large OEM buying power. These customers drive strong price and terms pressure through competitive tenders that have compressed supplier margins. Their scale enables multi-sourcing across global elastomer producers, forcing TSRC to compete on service, quality, and technical support as well as price to defend share.

Demand cyclicality and price sensitivity

Automotive and industrial cycles swing volumes sharply, intensifying buyer pushes for discounts in downturns and order delays with demands for shorter lead times when inventories pile up. Even in upcycles buyers retain leverage and price negotiations remain tough. TSRC mitigates swings via long-term contracts and surcharge mechanisms. IMF projected world GDP growth of 3.1% in 2024, underpinning uneven demand recovery.

Strict performance and consistency specs

High-performance tires and TPE applications require tight property windows, with supplier qualification often taking 12–24 months, which limits short-term buyer switching; however, buyers commonly dual-source once materials are qualified. TSRC’s technical service—through co-development, customized compound tuning and on-site support—can embed specification knowledge and logistical integration, tempering buyer power and raising the effective cost and time of switching.

Backward integration and R&D partnerships

Backward integration and R&D partnerships let large tire makers and TSRC reduce dependence on commodity elastomer grades by developing proprietary compounds, securing volume commitments but giving buyers technical visibility that strengthens negotiation leverage; joint testing can lock TSRC into supply for specific formulations while tying buyers to those specs, with the trade-off hinging on IP protection and exclusivity clauses.

- Proprietary compounds reduce commodity exposure

- Co-development secures volumes but aids buyer bargaining

- Joint testing creates lock-in vs buyer dependence

- Outcome depends on IP/exclusivity terms

Global sourcing options

Buyers can source SBR/BR/TPE from producers across Asia, Europe and the Americas, and the 2024 global synthetic rubber market (~$20B) raises supplier substitutability through widely available comparable grades. Logistics bottlenecks and average chemical tariffs (~3–5%) limit instant switching but do not erase buyers’ strategic leverage. TSRC differentiates on delivery reliability, total cost and ESG credentials to retain customers.

- Global market 2024: ~$20B

- Comparable grades ↑ substitutability

- Tariffs/logistics ~3–5% constrain speed

- TSRC focus: delivery, total cost, ESG

Global tire OEMs wield strong bargaining power; suppliers rely on service, ESG and delivery

TSRC customers (global tire OEMs) exert high bargaining power via large-volume tenders; global tire market ~$266B (2024) and synthetic rubber ~$20B (2024) amplify buyer leverage. Long qualification (12–24 months) limits rapid switching but dual-sourcing is common; TSRC competes on technical service, delivery, ESG and contract surcharges.

| Metric | 2024 |

|---|---|

| Global tire market | $266B |

| Synthetic rubber market | $20B |

| Qualification time | 12–24 months |

| Avg tariffs/logistics | 3–5% |

Preview Before You Purchase

TSRC Porter's Five Forces Analysis

This TSRC Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete strategic assessment—no placeholders, no excerpts. Download and use this same file right after payment; it’s ready for practical application. The analysis is final and professionally prepared for immediate use.

Don't Miss the Bigger Picture

TSRC faces evolving competitive dynamics driven by raw-material costs, concentrated suppliers, and increasing downstream buyer sophistication; this snapshot highlights key pressures but skips detailed intensities and implications. The full Porter's Five Forces Analysis quantifies each force, includes visuals and scenario impacts, and maps strategic responses. Unlock the complete report for consultant-grade insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Feedstock concentration (butadiene, styrene)

TSRC relies on a concentrated upstream base—roughly three major petrochemical producers supply most butadiene and styrene needs, so 2024 regional cracker outages and sub-90% utilization spikes tightened availability and lifted spot premiums. Integrated suppliers gained pricing leverage, while TSRC partially mitigates risk through multi-sourcing and geographic diversification, though exposure to feedstock volatility remains.

Price volatility and oil/NAF linkage

Monomer prices track crude and naphtha dynamics — Brent averaged roughly 85 USD/bbl in 2024 — driving sharp input-cost swings for TSRC. Suppliers can pass spikes through quickly, squeezing margins when customer pass-through lags. Hedging and formula pricing mitigate but do not eliminate exposure, and when naphtha spreads tighten in 2024 tight markets amplified supplier bargaining power.

Logistics and regional proximity

Elastomer feedstocks are bulk chemicals highly sensitive to freight and storage constraints, a vulnerability TSRC faced in 2024. Suppliers located close to TSRC plants or owning captive pipelines/terminals gain bargaining clout via reliability and lower logistics cost. Port congestion or geopolitical disruptions can force premium sourcing, and TSRC’s global footprint helps rebalance supply but switching suppliers entails material friction and lead times.

Limited spec flexibility, qualification needs

Process recipes demand tightly controlled monomer specs, so qualifying new suppliers typically takes 6–12 months and often costs in the hundreds of thousands of dollars, raising switching costs and giving incumbents leverage; any supplier change risks product-performance drift despite dual-qualification efforts and finite qualified-supplier capacity.

- Consistent monomer specs required

- Qualification: 6–12 months, ~hundreds k$

- High switching costs, incumbent influence

- Dual-qualification mitigates but capacity limited

Integration and ESG compliance pressure

Integrated petrochemical majors can leverage broader portfolios and robust sustainability documentation to differentiate; EU CSRD coverage expanded to large firms in 2024, raising formal reporting expectations. Stricter ESG and emissions reporting increases reliance on suppliers with traceability, adding dependency, while compliance premiums and certification costs tilt negotiating power toward well‑capitalized upstream players.

- Portfolio scale advantage

- CSRD 2024: higher reporting bar

- Traceability raises supplier dependency

- Compliance premiums favor large suppliers

Supply squeeze: ~3 upstreams, crackers sub-90%, Brent ~85 USD/bbl

TSRC relies on roughly three upstream petrochemical majors; 2024 regional cracker outages and sub-90% utilization tightened availability and raised spot premiums. Brent averaged ~85 USD/bbl in 2024, amplifying feedstock cost pass-through and squeezing margins despite hedging. Supplier qualification takes 6–12 months and ~100–500k USD, creating high switching costs and sustained supplier leverage.

| Metric | 2024 value |

|---|---|

| Major suppliers | ~3 |

| Brent avg | ~85 USD/bbl |

| Cracker util. | <90% (regional outages) |

| Qualification time | 6–12 months |

| Qualification cost | 100–500k USD |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes tailored exclusively for TSRC; identifies disruptive forces and emerging threats that affect market share and pricing. Fully editable in Word for easy inclusion in investor materials, strategy decks, or academic projects.

One-sheet TSRC Porter’s Five Forces synthesizes competitive pressure into actionable insights for faster strategic decisions, reducing time spent piecing disparate analyses together. Drag-and-drop inputs and a radar visualization make it simple to update scenarios and communicate risk to stakeholders.

Customers Bargaining Power

Large tire and OEM buyers with scale

TSRC serves global tire makers and auto supply chains that purchase in very high volumes; the global tire market was valued at about $266 billion in 2024, underpinning large OEM buying power. These customers drive strong price and terms pressure through competitive tenders that have compressed supplier margins. Their scale enables multi-sourcing across global elastomer producers, forcing TSRC to compete on service, quality, and technical support as well as price to defend share.

Demand cyclicality and price sensitivity

Automotive and industrial cycles swing volumes sharply, intensifying buyer pushes for discounts in downturns and order delays with demands for shorter lead times when inventories pile up. Even in upcycles buyers retain leverage and price negotiations remain tough. TSRC mitigates swings via long-term contracts and surcharge mechanisms. IMF projected world GDP growth of 3.1% in 2024, underpinning uneven demand recovery.

Strict performance and consistency specs

High-performance tires and TPE applications require tight property windows, with supplier qualification often taking 12–24 months, which limits short-term buyer switching; however, buyers commonly dual-source once materials are qualified. TSRC’s technical service—through co-development, customized compound tuning and on-site support—can embed specification knowledge and logistical integration, tempering buyer power and raising the effective cost and time of switching.

Backward integration and R&D partnerships

Backward integration and R&D partnerships let large tire makers and TSRC reduce dependence on commodity elastomer grades by developing proprietary compounds, securing volume commitments but giving buyers technical visibility that strengthens negotiation leverage; joint testing can lock TSRC into supply for specific formulations while tying buyers to those specs, with the trade-off hinging on IP protection and exclusivity clauses.

- Proprietary compounds reduce commodity exposure

- Co-development secures volumes but aids buyer bargaining

- Joint testing creates lock-in vs buyer dependence

- Outcome depends on IP/exclusivity terms

Global sourcing options

Buyers can source SBR/BR/TPE from producers across Asia, Europe and the Americas, and the 2024 global synthetic rubber market (~$20B) raises supplier substitutability through widely available comparable grades. Logistics bottlenecks and average chemical tariffs (~3–5%) limit instant switching but do not erase buyers’ strategic leverage. TSRC differentiates on delivery reliability, total cost and ESG credentials to retain customers.

- Global market 2024: ~$20B

- Comparable grades ↑ substitutability

- Tariffs/logistics ~3–5% constrain speed

- TSRC focus: delivery, total cost, ESG

Global tire OEMs wield strong bargaining power; suppliers rely on service, ESG and delivery

TSRC customers (global tire OEMs) exert high bargaining power via large-volume tenders; global tire market ~$266B (2024) and synthetic rubber ~$20B (2024) amplify buyer leverage. Long qualification (12–24 months) limits rapid switching but dual-sourcing is common; TSRC competes on technical service, delivery, ESG and contract surcharges.

| Metric | 2024 |

|---|---|

| Global tire market | $266B |

| Synthetic rubber market | $20B |

| Qualification time | 12–24 months |

| Avg tariffs/logistics | 3–5% |

Preview Before You Purchase

TSRC Porter's Five Forces Analysis

This TSRC Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete strategic assessment—no placeholders, no excerpts. Download and use this same file right after payment; it’s ready for practical application. The analysis is final and professionally prepared for immediate use.

Description

Don't Miss the Bigger Picture

TSRC faces evolving competitive dynamics driven by raw-material costs, concentrated suppliers, and increasing downstream buyer sophistication; this snapshot highlights key pressures but skips detailed intensities and implications. The full Porter's Five Forces Analysis quantifies each force, includes visuals and scenario impacts, and maps strategic responses. Unlock the complete report for consultant-grade insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Feedstock concentration (butadiene, styrene)

TSRC relies on a concentrated upstream base—roughly three major petrochemical producers supply most butadiene and styrene needs, so 2024 regional cracker outages and sub-90% utilization spikes tightened availability and lifted spot premiums. Integrated suppliers gained pricing leverage, while TSRC partially mitigates risk through multi-sourcing and geographic diversification, though exposure to feedstock volatility remains.

Price volatility and oil/NAF linkage

Monomer prices track crude and naphtha dynamics — Brent averaged roughly 85 USD/bbl in 2024 — driving sharp input-cost swings for TSRC. Suppliers can pass spikes through quickly, squeezing margins when customer pass-through lags. Hedging and formula pricing mitigate but do not eliminate exposure, and when naphtha spreads tighten in 2024 tight markets amplified supplier bargaining power.

Logistics and regional proximity

Elastomer feedstocks are bulk chemicals highly sensitive to freight and storage constraints, a vulnerability TSRC faced in 2024. Suppliers located close to TSRC plants or owning captive pipelines/terminals gain bargaining clout via reliability and lower logistics cost. Port congestion or geopolitical disruptions can force premium sourcing, and TSRC’s global footprint helps rebalance supply but switching suppliers entails material friction and lead times.

Limited spec flexibility, qualification needs

Process recipes demand tightly controlled monomer specs, so qualifying new suppliers typically takes 6–12 months and often costs in the hundreds of thousands of dollars, raising switching costs and giving incumbents leverage; any supplier change risks product-performance drift despite dual-qualification efforts and finite qualified-supplier capacity.

- Consistent monomer specs required

- Qualification: 6–12 months, ~hundreds k$

- High switching costs, incumbent influence

- Dual-qualification mitigates but capacity limited

Integration and ESG compliance pressure

Integrated petrochemical majors can leverage broader portfolios and robust sustainability documentation to differentiate; EU CSRD coverage expanded to large firms in 2024, raising formal reporting expectations. Stricter ESG and emissions reporting increases reliance on suppliers with traceability, adding dependency, while compliance premiums and certification costs tilt negotiating power toward well‑capitalized upstream players.

- Portfolio scale advantage

- CSRD 2024: higher reporting bar

- Traceability raises supplier dependency

- Compliance premiums favor large suppliers

Supply squeeze: ~3 upstreams, crackers sub-90%, Brent ~85 USD/bbl

TSRC relies on roughly three upstream petrochemical majors; 2024 regional cracker outages and sub-90% utilization tightened availability and raised spot premiums. Brent averaged ~85 USD/bbl in 2024, amplifying feedstock cost pass-through and squeezing margins despite hedging. Supplier qualification takes 6–12 months and ~100–500k USD, creating high switching costs and sustained supplier leverage.

| Metric | 2024 value |

|---|---|

| Major suppliers | ~3 |

| Brent avg | ~85 USD/bbl |

| Cracker util. | <90% (regional outages) |

| Qualification time | 6–12 months |

| Qualification cost | 100–500k USD |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes tailored exclusively for TSRC; identifies disruptive forces and emerging threats that affect market share and pricing. Fully editable in Word for easy inclusion in investor materials, strategy decks, or academic projects.

One-sheet TSRC Porter’s Five Forces synthesizes competitive pressure into actionable insights for faster strategic decisions, reducing time spent piecing disparate analyses together. Drag-and-drop inputs and a radar visualization make it simple to update scenarios and communicate risk to stakeholders.

Customers Bargaining Power

Large tire and OEM buyers with scale

TSRC serves global tire makers and auto supply chains that purchase in very high volumes; the global tire market was valued at about $266 billion in 2024, underpinning large OEM buying power. These customers drive strong price and terms pressure through competitive tenders that have compressed supplier margins. Their scale enables multi-sourcing across global elastomer producers, forcing TSRC to compete on service, quality, and technical support as well as price to defend share.

Demand cyclicality and price sensitivity

Automotive and industrial cycles swing volumes sharply, intensifying buyer pushes for discounts in downturns and order delays with demands for shorter lead times when inventories pile up. Even in upcycles buyers retain leverage and price negotiations remain tough. TSRC mitigates swings via long-term contracts and surcharge mechanisms. IMF projected world GDP growth of 3.1% in 2024, underpinning uneven demand recovery.

Strict performance and consistency specs

High-performance tires and TPE applications require tight property windows, with supplier qualification often taking 12–24 months, which limits short-term buyer switching; however, buyers commonly dual-source once materials are qualified. TSRC’s technical service—through co-development, customized compound tuning and on-site support—can embed specification knowledge and logistical integration, tempering buyer power and raising the effective cost and time of switching.

Backward integration and R&D partnerships

Backward integration and R&D partnerships let large tire makers and TSRC reduce dependence on commodity elastomer grades by developing proprietary compounds, securing volume commitments but giving buyers technical visibility that strengthens negotiation leverage; joint testing can lock TSRC into supply for specific formulations while tying buyers to those specs, with the trade-off hinging on IP protection and exclusivity clauses.

- Proprietary compounds reduce commodity exposure

- Co-development secures volumes but aids buyer bargaining

- Joint testing creates lock-in vs buyer dependence

- Outcome depends on IP/exclusivity terms

Global sourcing options

Buyers can source SBR/BR/TPE from producers across Asia, Europe and the Americas, and the 2024 global synthetic rubber market (~$20B) raises supplier substitutability through widely available comparable grades. Logistics bottlenecks and average chemical tariffs (~3–5%) limit instant switching but do not erase buyers’ strategic leverage. TSRC differentiates on delivery reliability, total cost and ESG credentials to retain customers.

- Global market 2024: ~$20B

- Comparable grades ↑ substitutability

- Tariffs/logistics ~3–5% constrain speed

- TSRC focus: delivery, total cost, ESG

Global tire OEMs wield strong bargaining power; suppliers rely on service, ESG and delivery

TSRC customers (global tire OEMs) exert high bargaining power via large-volume tenders; global tire market ~$266B (2024) and synthetic rubber ~$20B (2024) amplify buyer leverage. Long qualification (12–24 months) limits rapid switching but dual-sourcing is common; TSRC competes on technical service, delivery, ESG and contract surcharges.

| Metric | 2024 |

|---|---|

| Global tire market | $266B |

| Synthetic rubber market | $20B |

| Qualification time | 12–24 months |

| Avg tariffs/logistics | 3–5% |

Preview Before You Purchase

TSRC Porter's Five Forces Analysis

This TSRC Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete strategic assessment—no placeholders, no excerpts. Download and use this same file right after payment; it’s ready for practical application. The analysis is final and professionally prepared for immediate use.