TMBThanachart Bank Business Model Canvas

Business Model Canvas: concise bank strategy, customer segments, revenue levers

Unlock the strategic engine behind TMBThanachart Bank with our concise Business Model Canvas—three to five sentences that map customer segments, revenue levers, and competitive advantages in a clear, actionable format. Perfect for investors, consultants, and executives seeking practical insights; download the full Word/Excel canvas to benchmark, adapt, and execute winning strategies today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Thailand and regulatory agencies ensures compliance and systemic stability, aligning TMBThanachart with Basel III minima such as an 8% minimum CAR and a 2.5% capital conservation buffer. Collaboration helps shape risk standards, capital adequacy and consumer protection practices across the group. Participation in national payment networks like PromptPay (processing over 1 billion transactions in 2023) and industry associations enhances interoperability and reduces regulatory friction, supporting faster product approvals.

Payment networks and fintechs

Alliances with Visa, Mastercard, PromptPay (over 60 million IDs nationwide in 2024) and local rails enable seamless transactions and higher authorization rates; fintech partnerships accelerate digital onboarding and eKYC, cutting account-opening time to minutes in pilots. Co-built APIs extend merchant and consumer reach, boosting transaction volumes and lowering card/processing costs by improving automation and dispute resolution, thereby enhancing overall user experience.

Insurance and asset management partners

Bancassurance providers and fund managers expand protection and investment suites through TMBThanachart’s channels, leveraging Thailand’s ~71.5 million population (2024) to scale retail and SME reach. Joint product design tailors coverage and portfolios to Thai retail and SME needs. Revenue-sharing models align incentives across distribution and servicing. These partnerships deepen wallet share and fee income.

SME and corporate alliances

Cooperation with supply-chain anchors, chambers and industry clusters improves SME credit data and underwriting, especially in Thailand where SMEs account for over 99% of enterprises and contributed about 43% of GDP in 2024. Vendor financing and payroll partnerships embed banking into business operations; treasury and cash-management integrations raise customer stickiness and create stable deposit bases and lending pipelines.

- Supply-chain data: better SME credit files

- Vendor/payroll tie-ins: embedded payments and recurring deposits

- Treasury integrations: higher wallet share and predictable lending flow

Technology and data vendors

Cloud, cybersecurity, and core-banking providers underpin TMBThanachart Bank’s scalable operations by enabling elastic capacity, secure transaction processing, and rapid deployment of new services.

Data bureaus and analytics firms enhance credit risk modeling and personalization, while outsourced service partners shorten time-to-market and lower operating costs, together supporting resilient, compliant, and innovative platforms.

- Cloud scalability

- Cybersecurity & compliance

- Core banking continuity

- Advanced risk analytics

- Outsourced delivery for speed/cost

Regulatory & rails accelerate SME growth — 8% CAR 1B+ tx

Regulatory ties secure Basel III compliance (8% CAR, 2.5% buffer) and faster approvals. Payment partners (PromptPay: >1B tx 2023; 60M IDs 2024) boost volumes and authorization. Bancassurance and fund partners scale retail/SME sales; SMEs (>99% firms; ~43% GDP 2024) drive lending. Cloud, cyber and analytics cut costs and speed launches.

| Partner | Role | 2023-24 metric |

|---|---|---|

| Regulators | Compliance | 8% CAR; 2.5% buffer |

| Payments | Rails | PromptPay 1B tx; 60M IDs |

| Bancassurance | Distribution | Population 71.5M |

| SME anchors | Credit data | SMEs 99% firms; 43% GDP |

| Cloud/cyber | Ops | Scalability & security |

What is included in the product

A comprehensive Business Model Canvas for TMBThanachart Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights—ideal for presentations, investor discussions and strategic planning.

High-level TMBThanachart Bank Business Model Canvas that condenses strategy into a single editable page, saving hours of structuring while quickly revealing core components and pain points for boardrooms or team collaboration.

Activities

Retail and SME lending

Originating, underwriting, and servicing personal, mortgage, auto, and SME loans drive TMBThanachart Bank’s growth by expanding fee and interest income across retail and small-business segments. Risk-based pricing and automated policy engines speed approvals while preserving credit quality through tiered scoring and collateral rules. Robust collections, early-warning restructuring, and write-off frameworks sustain portfolio health. Continuous analytics refine approval thresholds, limits, and cross-sell strategies.

Deposit and payments management

Acquiring stable CASA deposits (CASA ratio 56% in 2024) lowers TMBThanachart Bank’s funding costs versus term deposits, boosting NIM. Operating current accounts, cards and real-time transfers lifts engagement and transaction fee income. Business cash management embeds daily usage and unlocks float, while active liquidity optimization supports profitability and CET1/regulatory ratios.

Wealth and insurance distribution

Selling funds, structured notes and protection products diversifies fee income and reduces reliance on net interest margin. Rigorous suitability checks and advisory processes boost client trust and ensure regulatory compliance. Regular portfolio reviews and targeted cross-sell campaigns increase AUM per client, while streamlined digital subscription and claims journeys cut processing friction and improve retention.

Digital platform development

Building mobile and internet banking strengthens acquisition and servicing by streamlining onboarding, transactions, and self-service across channels. API integrations extend services to merchant and ecosystem partners, enabling cardless payments, wallets, and lending partnerships. Continuous UX, security, and performance upgrades raise active user adoption, while data-driven personalization improves conversion and retention through tailored offers and journeys.

- Digital onboarding and servicing

- API-led merchant & ecosystem integration

- UX, security, performance optimization

- Data-driven personalization for conversion & retention

Risk, compliance, and operations

Risk, compliance, and operations at TMBThanachart focus on credit, market and operational risk controls to safeguard capital, maintaining a CET1 ratio around 15.0% and NPL near 2.1% in 2024; AML/KYC, cybersecurity and data-privacy programs support legal adherence and customer trust; process automation cut error rates and cost-to-serve by ~40%; business continuity and stress testing underpin resilience.

- CET1 ~15.0% (2024)

- NPL ~2.1% (2024)

- Automation reduced errors/costs ~40%

- LCR / stress tests ensure continuity

High CASA, digital scaling and automation boost margins while preserving credit quality

Originating, underwriting and servicing retail, mortgage, auto and SME loans drive interest and fee income while risk-based pricing and analytics preserve credit quality. CASA 56% (2024) lowers funding cost and boosts NIM; cash management and liquidity optimization support profitability. Digital, API integrations and cross-sell increase transactions, AUM and fee diversification. Risk/compliance sustain CET1 ~15.0% and NPL ~2.1%; automation cut costs ~40%.

| Metric | 2024 |

|---|---|

| CASA ratio | 56% |

| CET1 | ~15.0% |

| NPL | ~2.1% |

| Automation cost reduction | ~40% |

What You See Is What You Get

Business Model Canvas

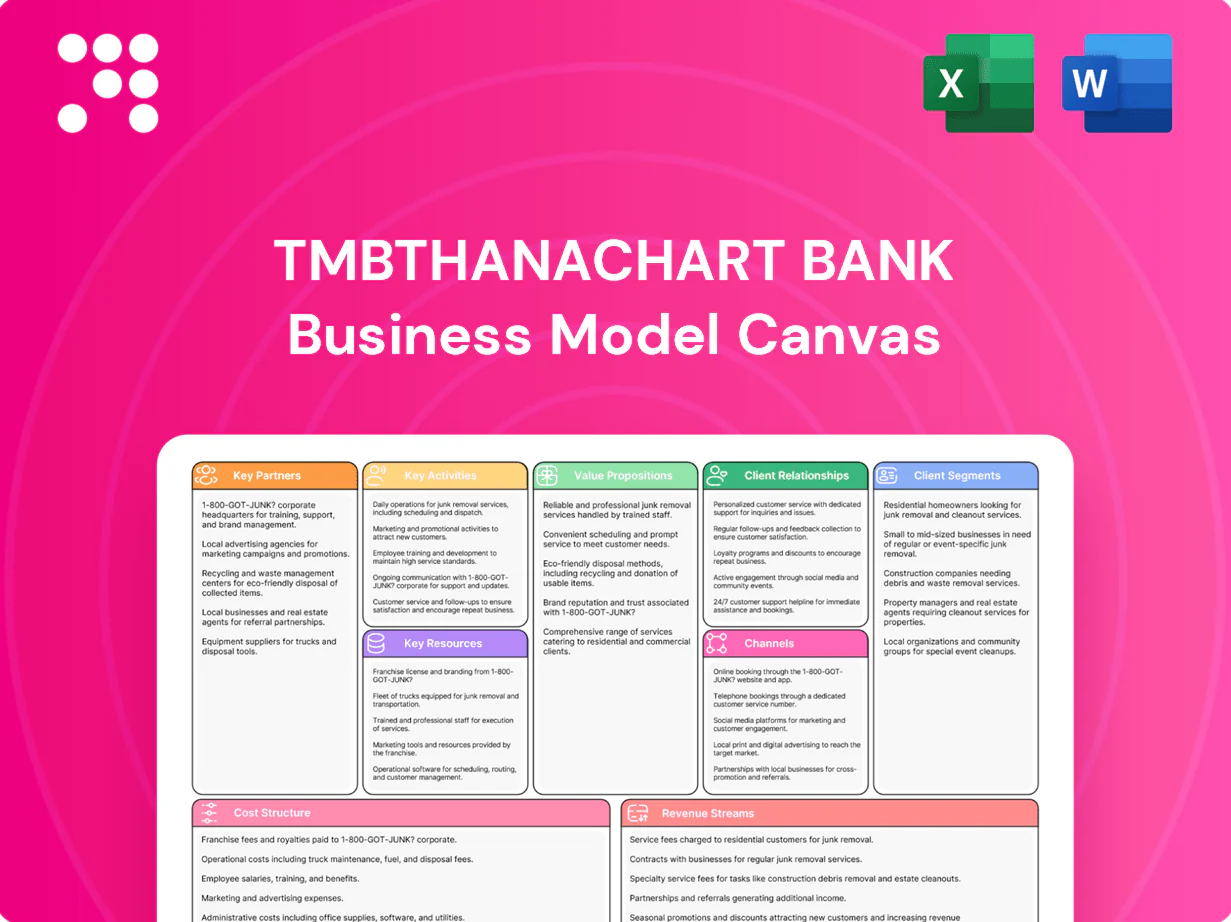

The TMBThanachart Bank Business Model Canvas shown here is the actual deliverable, not a mockup. This preview reflects the exact content and structure you will receive after purchase. Once ordered, you’ll download the same complete, editable document ready for use. No substitutions or hidden pages—what you see is what you get.

Business Model Canvas: concise bank strategy, customer segments, revenue levers

Unlock the strategic engine behind TMBThanachart Bank with our concise Business Model Canvas—three to five sentences that map customer segments, revenue levers, and competitive advantages in a clear, actionable format. Perfect for investors, consultants, and executives seeking practical insights; download the full Word/Excel canvas to benchmark, adapt, and execute winning strategies today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Thailand and regulatory agencies ensures compliance and systemic stability, aligning TMBThanachart with Basel III minima such as an 8% minimum CAR and a 2.5% capital conservation buffer. Collaboration helps shape risk standards, capital adequacy and consumer protection practices across the group. Participation in national payment networks like PromptPay (processing over 1 billion transactions in 2023) and industry associations enhances interoperability and reduces regulatory friction, supporting faster product approvals.

Payment networks and fintechs

Alliances with Visa, Mastercard, PromptPay (over 60 million IDs nationwide in 2024) and local rails enable seamless transactions and higher authorization rates; fintech partnerships accelerate digital onboarding and eKYC, cutting account-opening time to minutes in pilots. Co-built APIs extend merchant and consumer reach, boosting transaction volumes and lowering card/processing costs by improving automation and dispute resolution, thereby enhancing overall user experience.

Insurance and asset management partners

Bancassurance providers and fund managers expand protection and investment suites through TMBThanachart’s channels, leveraging Thailand’s ~71.5 million population (2024) to scale retail and SME reach. Joint product design tailors coverage and portfolios to Thai retail and SME needs. Revenue-sharing models align incentives across distribution and servicing. These partnerships deepen wallet share and fee income.

SME and corporate alliances

Cooperation with supply-chain anchors, chambers and industry clusters improves SME credit data and underwriting, especially in Thailand where SMEs account for over 99% of enterprises and contributed about 43% of GDP in 2024. Vendor financing and payroll partnerships embed banking into business operations; treasury and cash-management integrations raise customer stickiness and create stable deposit bases and lending pipelines.

- Supply-chain data: better SME credit files

- Vendor/payroll tie-ins: embedded payments and recurring deposits

- Treasury integrations: higher wallet share and predictable lending flow

Technology and data vendors

Cloud, cybersecurity, and core-banking providers underpin TMBThanachart Bank’s scalable operations by enabling elastic capacity, secure transaction processing, and rapid deployment of new services.

Data bureaus and analytics firms enhance credit risk modeling and personalization, while outsourced service partners shorten time-to-market and lower operating costs, together supporting resilient, compliant, and innovative platforms.

- Cloud scalability

- Cybersecurity & compliance

- Core banking continuity

- Advanced risk analytics

- Outsourced delivery for speed/cost

Regulatory & rails accelerate SME growth — 8% CAR 1B+ tx

Regulatory ties secure Basel III compliance (8% CAR, 2.5% buffer) and faster approvals. Payment partners (PromptPay: >1B tx 2023; 60M IDs 2024) boost volumes and authorization. Bancassurance and fund partners scale retail/SME sales; SMEs (>99% firms; ~43% GDP 2024) drive lending. Cloud, cyber and analytics cut costs and speed launches.

| Partner | Role | 2023-24 metric |

|---|---|---|

| Regulators | Compliance | 8% CAR; 2.5% buffer |

| Payments | Rails | PromptPay 1B tx; 60M IDs |

| Bancassurance | Distribution | Population 71.5M |

| SME anchors | Credit data | SMEs 99% firms; 43% GDP |

| Cloud/cyber | Ops | Scalability & security |

What is included in the product

A comprehensive Business Model Canvas for TMBThanachart Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights—ideal for presentations, investor discussions and strategic planning.

High-level TMBThanachart Bank Business Model Canvas that condenses strategy into a single editable page, saving hours of structuring while quickly revealing core components and pain points for boardrooms or team collaboration.

Activities

Retail and SME lending

Originating, underwriting, and servicing personal, mortgage, auto, and SME loans drive TMBThanachart Bank’s growth by expanding fee and interest income across retail and small-business segments. Risk-based pricing and automated policy engines speed approvals while preserving credit quality through tiered scoring and collateral rules. Robust collections, early-warning restructuring, and write-off frameworks sustain portfolio health. Continuous analytics refine approval thresholds, limits, and cross-sell strategies.

Deposit and payments management

Acquiring stable CASA deposits (CASA ratio 56% in 2024) lowers TMBThanachart Bank’s funding costs versus term deposits, boosting NIM. Operating current accounts, cards and real-time transfers lifts engagement and transaction fee income. Business cash management embeds daily usage and unlocks float, while active liquidity optimization supports profitability and CET1/regulatory ratios.

Wealth and insurance distribution

Selling funds, structured notes and protection products diversifies fee income and reduces reliance on net interest margin. Rigorous suitability checks and advisory processes boost client trust and ensure regulatory compliance. Regular portfolio reviews and targeted cross-sell campaigns increase AUM per client, while streamlined digital subscription and claims journeys cut processing friction and improve retention.

Digital platform development

Building mobile and internet banking strengthens acquisition and servicing by streamlining onboarding, transactions, and self-service across channels. API integrations extend services to merchant and ecosystem partners, enabling cardless payments, wallets, and lending partnerships. Continuous UX, security, and performance upgrades raise active user adoption, while data-driven personalization improves conversion and retention through tailored offers and journeys.

- Digital onboarding and servicing

- API-led merchant & ecosystem integration

- UX, security, performance optimization

- Data-driven personalization for conversion & retention

Risk, compliance, and operations

Risk, compliance, and operations at TMBThanachart focus on credit, market and operational risk controls to safeguard capital, maintaining a CET1 ratio around 15.0% and NPL near 2.1% in 2024; AML/KYC, cybersecurity and data-privacy programs support legal adherence and customer trust; process automation cut error rates and cost-to-serve by ~40%; business continuity and stress testing underpin resilience.

- CET1 ~15.0% (2024)

- NPL ~2.1% (2024)

- Automation reduced errors/costs ~40%

- LCR / stress tests ensure continuity

High CASA, digital scaling and automation boost margins while preserving credit quality

Originating, underwriting and servicing retail, mortgage, auto and SME loans drive interest and fee income while risk-based pricing and analytics preserve credit quality. CASA 56% (2024) lowers funding cost and boosts NIM; cash management and liquidity optimization support profitability. Digital, API integrations and cross-sell increase transactions, AUM and fee diversification. Risk/compliance sustain CET1 ~15.0% and NPL ~2.1%; automation cut costs ~40%.

| Metric | 2024 |

|---|---|

| CASA ratio | 56% |

| CET1 | ~15.0% |

| NPL | ~2.1% |

| Automation cost reduction | ~40% |

What You See Is What You Get

Business Model Canvas

The TMBThanachart Bank Business Model Canvas shown here is the actual deliverable, not a mockup. This preview reflects the exact content and structure you will receive after purchase. Once ordered, you’ll download the same complete, editable document ready for use. No substitutions or hidden pages—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: concise bank strategy, customer segments, revenue levers

Unlock the strategic engine behind TMBThanachart Bank with our concise Business Model Canvas—three to five sentences that map customer segments, revenue levers, and competitive advantages in a clear, actionable format. Perfect for investors, consultants, and executives seeking practical insights; download the full Word/Excel canvas to benchmark, adapt, and execute winning strategies today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Thailand and regulatory agencies ensures compliance and systemic stability, aligning TMBThanachart with Basel III minima such as an 8% minimum CAR and a 2.5% capital conservation buffer. Collaboration helps shape risk standards, capital adequacy and consumer protection practices across the group. Participation in national payment networks like PromptPay (processing over 1 billion transactions in 2023) and industry associations enhances interoperability and reduces regulatory friction, supporting faster product approvals.

Payment networks and fintechs

Alliances with Visa, Mastercard, PromptPay (over 60 million IDs nationwide in 2024) and local rails enable seamless transactions and higher authorization rates; fintech partnerships accelerate digital onboarding and eKYC, cutting account-opening time to minutes in pilots. Co-built APIs extend merchant and consumer reach, boosting transaction volumes and lowering card/processing costs by improving automation and dispute resolution, thereby enhancing overall user experience.

Insurance and asset management partners

Bancassurance providers and fund managers expand protection and investment suites through TMBThanachart’s channels, leveraging Thailand’s ~71.5 million population (2024) to scale retail and SME reach. Joint product design tailors coverage and portfolios to Thai retail and SME needs. Revenue-sharing models align incentives across distribution and servicing. These partnerships deepen wallet share and fee income.

SME and corporate alliances

Cooperation with supply-chain anchors, chambers and industry clusters improves SME credit data and underwriting, especially in Thailand where SMEs account for over 99% of enterprises and contributed about 43% of GDP in 2024. Vendor financing and payroll partnerships embed banking into business operations; treasury and cash-management integrations raise customer stickiness and create stable deposit bases and lending pipelines.

- Supply-chain data: better SME credit files

- Vendor/payroll tie-ins: embedded payments and recurring deposits

- Treasury integrations: higher wallet share and predictable lending flow

Technology and data vendors

Cloud, cybersecurity, and core-banking providers underpin TMBThanachart Bank’s scalable operations by enabling elastic capacity, secure transaction processing, and rapid deployment of new services.

Data bureaus and analytics firms enhance credit risk modeling and personalization, while outsourced service partners shorten time-to-market and lower operating costs, together supporting resilient, compliant, and innovative platforms.

- Cloud scalability

- Cybersecurity & compliance

- Core banking continuity

- Advanced risk analytics

- Outsourced delivery for speed/cost

Regulatory & rails accelerate SME growth — 8% CAR 1B+ tx

Regulatory ties secure Basel III compliance (8% CAR, 2.5% buffer) and faster approvals. Payment partners (PromptPay: >1B tx 2023; 60M IDs 2024) boost volumes and authorization. Bancassurance and fund partners scale retail/SME sales; SMEs (>99% firms; ~43% GDP 2024) drive lending. Cloud, cyber and analytics cut costs and speed launches.

| Partner | Role | 2023-24 metric |

|---|---|---|

| Regulators | Compliance | 8% CAR; 2.5% buffer |

| Payments | Rails | PromptPay 1B tx; 60M IDs |

| Bancassurance | Distribution | Population 71.5M |

| SME anchors | Credit data | SMEs 99% firms; 43% GDP |

| Cloud/cyber | Ops | Scalability & security |

What is included in the product

A comprehensive Business Model Canvas for TMBThanachart Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights—ideal for presentations, investor discussions and strategic planning.

High-level TMBThanachart Bank Business Model Canvas that condenses strategy into a single editable page, saving hours of structuring while quickly revealing core components and pain points for boardrooms or team collaboration.

Activities

Retail and SME lending

Originating, underwriting, and servicing personal, mortgage, auto, and SME loans drive TMBThanachart Bank’s growth by expanding fee and interest income across retail and small-business segments. Risk-based pricing and automated policy engines speed approvals while preserving credit quality through tiered scoring and collateral rules. Robust collections, early-warning restructuring, and write-off frameworks sustain portfolio health. Continuous analytics refine approval thresholds, limits, and cross-sell strategies.

Deposit and payments management

Acquiring stable CASA deposits (CASA ratio 56% in 2024) lowers TMBThanachart Bank’s funding costs versus term deposits, boosting NIM. Operating current accounts, cards and real-time transfers lifts engagement and transaction fee income. Business cash management embeds daily usage and unlocks float, while active liquidity optimization supports profitability and CET1/regulatory ratios.

Wealth and insurance distribution

Selling funds, structured notes and protection products diversifies fee income and reduces reliance on net interest margin. Rigorous suitability checks and advisory processes boost client trust and ensure regulatory compliance. Regular portfolio reviews and targeted cross-sell campaigns increase AUM per client, while streamlined digital subscription and claims journeys cut processing friction and improve retention.

Digital platform development

Building mobile and internet banking strengthens acquisition and servicing by streamlining onboarding, transactions, and self-service across channels. API integrations extend services to merchant and ecosystem partners, enabling cardless payments, wallets, and lending partnerships. Continuous UX, security, and performance upgrades raise active user adoption, while data-driven personalization improves conversion and retention through tailored offers and journeys.

- Digital onboarding and servicing

- API-led merchant & ecosystem integration

- UX, security, performance optimization

- Data-driven personalization for conversion & retention

Risk, compliance, and operations

Risk, compliance, and operations at TMBThanachart focus on credit, market and operational risk controls to safeguard capital, maintaining a CET1 ratio around 15.0% and NPL near 2.1% in 2024; AML/KYC, cybersecurity and data-privacy programs support legal adherence and customer trust; process automation cut error rates and cost-to-serve by ~40%; business continuity and stress testing underpin resilience.

- CET1 ~15.0% (2024)

- NPL ~2.1% (2024)

- Automation reduced errors/costs ~40%

- LCR / stress tests ensure continuity

High CASA, digital scaling and automation boost margins while preserving credit quality

Originating, underwriting and servicing retail, mortgage, auto and SME loans drive interest and fee income while risk-based pricing and analytics preserve credit quality. CASA 56% (2024) lowers funding cost and boosts NIM; cash management and liquidity optimization support profitability. Digital, API integrations and cross-sell increase transactions, AUM and fee diversification. Risk/compliance sustain CET1 ~15.0% and NPL ~2.1%; automation cut costs ~40%.

| Metric | 2024 |

|---|---|

| CASA ratio | 56% |

| CET1 | ~15.0% |

| NPL | ~2.1% |

| Automation cost reduction | ~40% |

What You See Is What You Get

Business Model Canvas

The TMBThanachart Bank Business Model Canvas shown here is the actual deliverable, not a mockup. This preview reflects the exact content and structure you will receive after purchase. Once ordered, you’ll download the same complete, editable document ready for use. No substitutions or hidden pages—what you see is what you get.