Tubos Reunidos Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Tubos Reunidos faces moderate supplier leverage, intense rivalry in steel tubes, and evolving buyer demands that compress margins; barriers to entry are significant but substitutes and cyclicality pose persistent threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications for Tubos Reunidos.

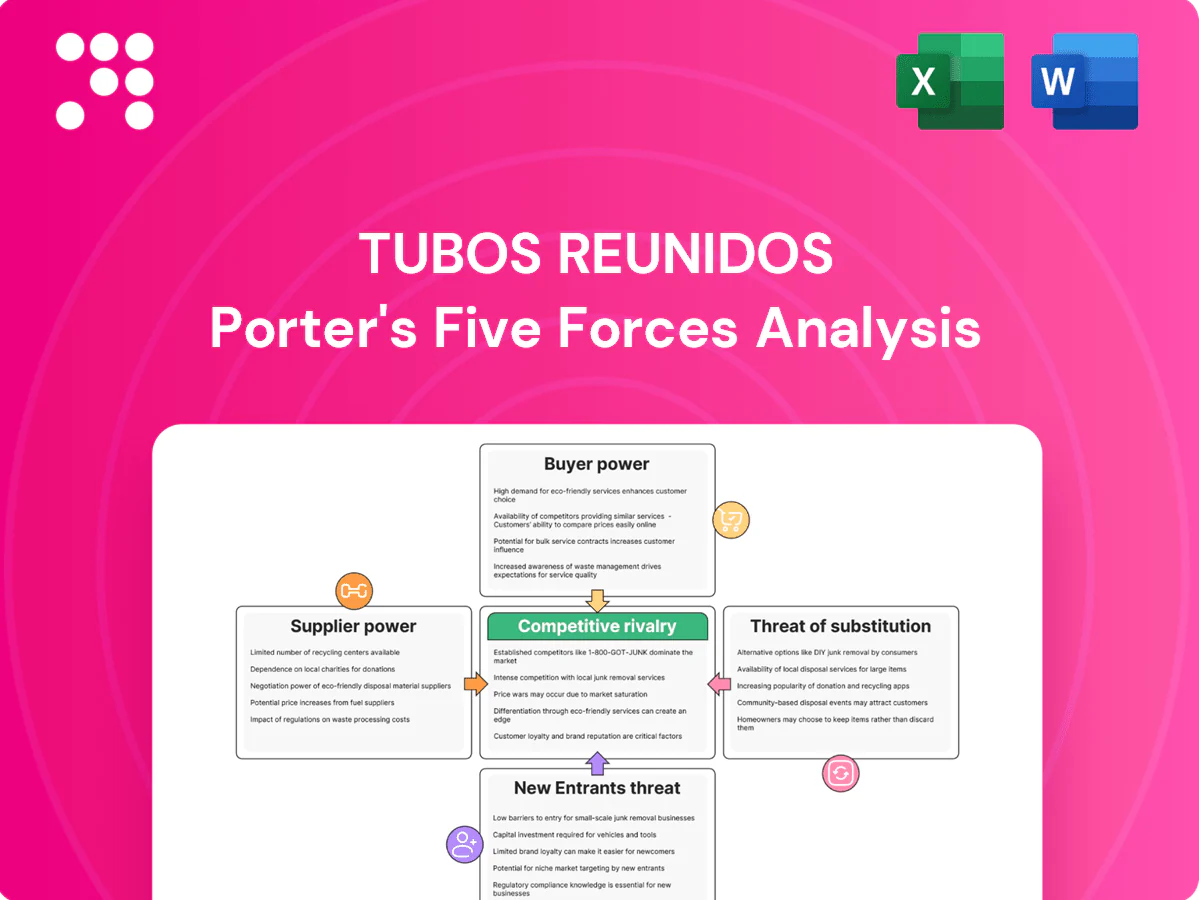

Suppliers Bargaining Power

Concentrated alloy suppliers

Seamless tube grades need nickel, molybdenum and chromium sourced from a concentrated set of miners and refiners, with Indonesia, Philippines and Russia prominent for nickel, China dominant in molybdenum processing, and South Africa/Kazakhstan key for chromium. This concentration elevates suppliers’ pricing power and risks bottlenecks. Tubos Reunidos uses multi-sourcing and hedging but constraints persist. Export controls or disruptions can quickly push up costs and extend lead times.

Energy-intensive production

Hot finishing, heat treatment and cold drawing are highly energy-intensive, with metals-processing energy shares often cited at 20-30% of operating costs; industrial gas in Europe averaged roughly €30-40/MWh in 2024. Volatile European markets and utilities/energy traders thus wield pricing power, while long-term contracts reduce spot risk but lock cost structures. EU ETS carbon prices averaged about €85/tCO2 in 2024, further increasing supplier influence on total cost.

Capital equipment and maintenance

Specialized mills, piercers, pilger lines and NDT systems for tubulars are sourced from very few OEMs; in 2024 the top 5 suppliers still supply over 70% of such capital equipment, giving suppliers pricing and scheduling power. Spare parts, service contracts and upgrades routinely command premiums (often 15–30%) and vendor-specific know-how raises switching costs. Preventive maintenance windows can be dictated by supplier availability, exposing operations to downtime risk.

Quality-certified billets and hollows

Input OCTG/petrochem billets and hollows must meet strict chemistry and cleanliness standards, concentrating qualified sources and giving those certified mills outsized leverage; in 2024 roughly 60% of certified OCTG-grade billets were sourced from the top five regional producers. Qualification audits and limited certified capacity raise supplier bargaining power, though Tubos Reunidos can partially offset this via backward integration and long-term offtakes. These mitigants reduce but do not eliminate upstream pricing and delivery risk.

- Concentration: top five suppliers ~60% (2024)

- Key lever: supplier audits enable price/policy control

- Mitigation: backward integration and long-term contracts

Logistics and port services

Heavy tubulars rely on dependable port and inland freight capacity; carrier scarcity or terminal congestion in 2024 pushed spot transport rates and caused multi-week delays, with global fleet utilization often above 85% and schedule reliability under pressure.

- Carrier scarcity → higher rates

- IMO targets 50% CO2 reduction by 2050 → upstream cost shifts

- Diversified routes cut risk but add complexity

Suppliers hold elevated leverage, driving premiums and lead-time risk

Suppliers hold elevated leverage: top-5 raw material suppliers ~60% (2024) and specialized equipment >70% share, driving premiums and lead-time risk. Energy and industrial gas costs (€30–40/MWh) plus EU ETS ~€85/tCO2 in 2024 raise input volatility. Tubos Reunidos mitigates with multi-sourcing, long-term contracts and selective backward integration, but switching costs remain high.

| Metric | 2024 Value |

|---|---|

| Top-5 raw material share | ~60% |

| Specialized equipment top-5 | >70% |

| Industrial gas/energy | €30–40/MWh |

| EU ETS price | ~€85/tCO2 |

| Global fleet utilization | >85% |

What is included in the product

Tailored Porter's Five Forces analysis for Tubos Reunidos, uncovering competitive intensity, supplier and buyer power, threat of substitutes and entrants, and strategic levers to defend margins and market share.

A concise one-sheet Porter's Five Forces for Tubos Reunidos—instantly reveals competitive pressure and supplier/buyer leverage to speed strategic decisions. Clean, customizable radar visualization and copy-ready layout let teams swap scenarios, update inputs, and drop into decks without specialist skills.

Customers Bargaining Power

Large, sophisticated buyers

Large buyers — oil & gas majors, petrochemical EPCs and industrial OEMs — control scale: global oil & gas capex was about $500bn in 2024, driving tenders often exceeding $10m and enabling bundled regional orders to extract price concessions. Their engineering specs and approved vendor lists limit suppliers and increase negotiation leverage. Performance penalties and on-time clauses, typically 1–3% of contract value, further squeeze margins.

High qualification and switching costs

High qualification and lengthy requalification processes—often lasting several months to over a year—raise switching costs for mills and temper buyer power, favoring Tubos Reunidos incumbents with proven QA records. Buyers can still dual-source to retain leverage, but long approval cycles and supplier audits boost the incumbent’s negotiating position. This dynamic reduces price pressure while preserving buyer options through parallel sourcing.

Cyclic demand and price sensitivity

Energy and petrochemical cycles drive tight budgets and price focus for Tubos Reunidos; Brent crude averaged about $86/bbl in 2024, intensifying cost pressure. In downturns buyers extracted discounts and extended payment terms, while in the 2024 upcycle lead times stretched to roughly 6–9 months, softening buyer leverage. Index-linked pricing formulas partly offset raw-material volatility and protect margins.

Custom specs and service needs

Custom specs—non-standard sizes, premium grades and short lead times—raise Tubos Reunidos’ value-add by shifting buyer focus from unit price to total-cost and uptime; reliance on technical support, traceable documentation and logistics reliability lowers pure price bargaining. After-sales service and responsive engineering become key differentiators that moderate buyer power.

Global alternatives

Buyers can source OCTG and welded pipe from global players Tenaris, Vallourec, TMK, Sumitomo and qualified Chinese mills, giving purchasers leverage through cross‑region price comparisons and alternative lead times.

Trade measures and tariffs intermittently restrict access—cycling buyer power—while long‑term supply agreements and strategic partnerships often lock volumes and mitigate spot bargaining.

- Multiple suppliers: increased competitive quotes

- Tariffs/trade measures: cyclical limit on options

- Strategic partnerships: volume lock, reduced buyer leverage

Major buyers, long lead times, and price pressure reshape oil & gas supply dynamics

Large buyers (majors, EPCs, OEMs) wield strong scale—global oil & gas capex ~ $500bn in 2024—driving large tenders and price concessions. Lengthy qualification (months–>1 year) and 6–9 month lead times boost incumbents’ position, despite buyers’ dual‑sourcing. Performance penalties (1–3% of contract) and Brent ~ $86/bbl in 2024 increase price sensitivity. Custom specs and after‑sales cut pure price bargaining.

| Metric | 2024 |

|---|---|

| Oil & gas capex | $500bn |

| Brent crude | $86/bbl |

| Lead times | 6–9 months |

| Performance penalties | 1–3% contract |

Same Document Delivered

Tubos Reunidos Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tubos Reunidos examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to assess industry profitability and strategic positioning. It highlights steel input dependence, key customer concentration, aftermarket pressure, and regulatory/capacity constraints shaping the firm's leverage. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

Go Beyond the Preview—Access the Full Strategic Report

Tubos Reunidos faces moderate supplier leverage, intense rivalry in steel tubes, and evolving buyer demands that compress margins; barriers to entry are significant but substitutes and cyclicality pose persistent threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications for Tubos Reunidos.

Suppliers Bargaining Power

Concentrated alloy suppliers

Seamless tube grades need nickel, molybdenum and chromium sourced from a concentrated set of miners and refiners, with Indonesia, Philippines and Russia prominent for nickel, China dominant in molybdenum processing, and South Africa/Kazakhstan key for chromium. This concentration elevates suppliers’ pricing power and risks bottlenecks. Tubos Reunidos uses multi-sourcing and hedging but constraints persist. Export controls or disruptions can quickly push up costs and extend lead times.

Energy-intensive production

Hot finishing, heat treatment and cold drawing are highly energy-intensive, with metals-processing energy shares often cited at 20-30% of operating costs; industrial gas in Europe averaged roughly €30-40/MWh in 2024. Volatile European markets and utilities/energy traders thus wield pricing power, while long-term contracts reduce spot risk but lock cost structures. EU ETS carbon prices averaged about €85/tCO2 in 2024, further increasing supplier influence on total cost.

Capital equipment and maintenance

Specialized mills, piercers, pilger lines and NDT systems for tubulars are sourced from very few OEMs; in 2024 the top 5 suppliers still supply over 70% of such capital equipment, giving suppliers pricing and scheduling power. Spare parts, service contracts and upgrades routinely command premiums (often 15–30%) and vendor-specific know-how raises switching costs. Preventive maintenance windows can be dictated by supplier availability, exposing operations to downtime risk.

Quality-certified billets and hollows

Input OCTG/petrochem billets and hollows must meet strict chemistry and cleanliness standards, concentrating qualified sources and giving those certified mills outsized leverage; in 2024 roughly 60% of certified OCTG-grade billets were sourced from the top five regional producers. Qualification audits and limited certified capacity raise supplier bargaining power, though Tubos Reunidos can partially offset this via backward integration and long-term offtakes. These mitigants reduce but do not eliminate upstream pricing and delivery risk.

- Concentration: top five suppliers ~60% (2024)

- Key lever: supplier audits enable price/policy control

- Mitigation: backward integration and long-term contracts

Logistics and port services

Heavy tubulars rely on dependable port and inland freight capacity; carrier scarcity or terminal congestion in 2024 pushed spot transport rates and caused multi-week delays, with global fleet utilization often above 85% and schedule reliability under pressure.

- Carrier scarcity → higher rates

- IMO targets 50% CO2 reduction by 2050 → upstream cost shifts

- Diversified routes cut risk but add complexity

Suppliers hold elevated leverage, driving premiums and lead-time risk

Suppliers hold elevated leverage: top-5 raw material suppliers ~60% (2024) and specialized equipment >70% share, driving premiums and lead-time risk. Energy and industrial gas costs (€30–40/MWh) plus EU ETS ~€85/tCO2 in 2024 raise input volatility. Tubos Reunidos mitigates with multi-sourcing, long-term contracts and selective backward integration, but switching costs remain high.

| Metric | 2024 Value |

|---|---|

| Top-5 raw material share | ~60% |

| Specialized equipment top-5 | >70% |

| Industrial gas/energy | €30–40/MWh |

| EU ETS price | ~€85/tCO2 |

| Global fleet utilization | >85% |

What is included in the product

Tailored Porter's Five Forces analysis for Tubos Reunidos, uncovering competitive intensity, supplier and buyer power, threat of substitutes and entrants, and strategic levers to defend margins and market share.

A concise one-sheet Porter's Five Forces for Tubos Reunidos—instantly reveals competitive pressure and supplier/buyer leverage to speed strategic decisions. Clean, customizable radar visualization and copy-ready layout let teams swap scenarios, update inputs, and drop into decks without specialist skills.

Customers Bargaining Power

Large, sophisticated buyers

Large buyers — oil & gas majors, petrochemical EPCs and industrial OEMs — control scale: global oil & gas capex was about $500bn in 2024, driving tenders often exceeding $10m and enabling bundled regional orders to extract price concessions. Their engineering specs and approved vendor lists limit suppliers and increase negotiation leverage. Performance penalties and on-time clauses, typically 1–3% of contract value, further squeeze margins.

High qualification and switching costs

High qualification and lengthy requalification processes—often lasting several months to over a year—raise switching costs for mills and temper buyer power, favoring Tubos Reunidos incumbents with proven QA records. Buyers can still dual-source to retain leverage, but long approval cycles and supplier audits boost the incumbent’s negotiating position. This dynamic reduces price pressure while preserving buyer options through parallel sourcing.

Cyclic demand and price sensitivity

Energy and petrochemical cycles drive tight budgets and price focus for Tubos Reunidos; Brent crude averaged about $86/bbl in 2024, intensifying cost pressure. In downturns buyers extracted discounts and extended payment terms, while in the 2024 upcycle lead times stretched to roughly 6–9 months, softening buyer leverage. Index-linked pricing formulas partly offset raw-material volatility and protect margins.

Custom specs and service needs

Custom specs—non-standard sizes, premium grades and short lead times—raise Tubos Reunidos’ value-add by shifting buyer focus from unit price to total-cost and uptime; reliance on technical support, traceable documentation and logistics reliability lowers pure price bargaining. After-sales service and responsive engineering become key differentiators that moderate buyer power.

Global alternatives

Buyers can source OCTG and welded pipe from global players Tenaris, Vallourec, TMK, Sumitomo and qualified Chinese mills, giving purchasers leverage through cross‑region price comparisons and alternative lead times.

Trade measures and tariffs intermittently restrict access—cycling buyer power—while long‑term supply agreements and strategic partnerships often lock volumes and mitigate spot bargaining.

- Multiple suppliers: increased competitive quotes

- Tariffs/trade measures: cyclical limit on options

- Strategic partnerships: volume lock, reduced buyer leverage

Major buyers, long lead times, and price pressure reshape oil & gas supply dynamics

Large buyers (majors, EPCs, OEMs) wield strong scale—global oil & gas capex ~ $500bn in 2024—driving large tenders and price concessions. Lengthy qualification (months–>1 year) and 6–9 month lead times boost incumbents’ position, despite buyers’ dual‑sourcing. Performance penalties (1–3% of contract) and Brent ~ $86/bbl in 2024 increase price sensitivity. Custom specs and after‑sales cut pure price bargaining.

| Metric | 2024 |

|---|---|

| Oil & gas capex | $500bn |

| Brent crude | $86/bbl |

| Lead times | 6–9 months |

| Performance penalties | 1–3% contract |

Same Document Delivered

Tubos Reunidos Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tubos Reunidos examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to assess industry profitability and strategic positioning. It highlights steel input dependence, key customer concentration, aftermarket pressure, and regulatory/capacity constraints shaping the firm's leverage. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Tubos Reunidos faces moderate supplier leverage, intense rivalry in steel tubes, and evolving buyer demands that compress margins; barriers to entry are significant but substitutes and cyclicality pose persistent threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications for Tubos Reunidos.

Suppliers Bargaining Power

Concentrated alloy suppliers

Seamless tube grades need nickel, molybdenum and chromium sourced from a concentrated set of miners and refiners, with Indonesia, Philippines and Russia prominent for nickel, China dominant in molybdenum processing, and South Africa/Kazakhstan key for chromium. This concentration elevates suppliers’ pricing power and risks bottlenecks. Tubos Reunidos uses multi-sourcing and hedging but constraints persist. Export controls or disruptions can quickly push up costs and extend lead times.

Energy-intensive production

Hot finishing, heat treatment and cold drawing are highly energy-intensive, with metals-processing energy shares often cited at 20-30% of operating costs; industrial gas in Europe averaged roughly €30-40/MWh in 2024. Volatile European markets and utilities/energy traders thus wield pricing power, while long-term contracts reduce spot risk but lock cost structures. EU ETS carbon prices averaged about €85/tCO2 in 2024, further increasing supplier influence on total cost.

Capital equipment and maintenance

Specialized mills, piercers, pilger lines and NDT systems for tubulars are sourced from very few OEMs; in 2024 the top 5 suppliers still supply over 70% of such capital equipment, giving suppliers pricing and scheduling power. Spare parts, service contracts and upgrades routinely command premiums (often 15–30%) and vendor-specific know-how raises switching costs. Preventive maintenance windows can be dictated by supplier availability, exposing operations to downtime risk.

Quality-certified billets and hollows

Input OCTG/petrochem billets and hollows must meet strict chemistry and cleanliness standards, concentrating qualified sources and giving those certified mills outsized leverage; in 2024 roughly 60% of certified OCTG-grade billets were sourced from the top five regional producers. Qualification audits and limited certified capacity raise supplier bargaining power, though Tubos Reunidos can partially offset this via backward integration and long-term offtakes. These mitigants reduce but do not eliminate upstream pricing and delivery risk.

- Concentration: top five suppliers ~60% (2024)

- Key lever: supplier audits enable price/policy control

- Mitigation: backward integration and long-term contracts

Logistics and port services

Heavy tubulars rely on dependable port and inland freight capacity; carrier scarcity or terminal congestion in 2024 pushed spot transport rates and caused multi-week delays, with global fleet utilization often above 85% and schedule reliability under pressure.

- Carrier scarcity → higher rates

- IMO targets 50% CO2 reduction by 2050 → upstream cost shifts

- Diversified routes cut risk but add complexity

Suppliers hold elevated leverage, driving premiums and lead-time risk

Suppliers hold elevated leverage: top-5 raw material suppliers ~60% (2024) and specialized equipment >70% share, driving premiums and lead-time risk. Energy and industrial gas costs (€30–40/MWh) plus EU ETS ~€85/tCO2 in 2024 raise input volatility. Tubos Reunidos mitigates with multi-sourcing, long-term contracts and selective backward integration, but switching costs remain high.

| Metric | 2024 Value |

|---|---|

| Top-5 raw material share | ~60% |

| Specialized equipment top-5 | >70% |

| Industrial gas/energy | €30–40/MWh |

| EU ETS price | ~€85/tCO2 |

| Global fleet utilization | >85% |

What is included in the product

Tailored Porter's Five Forces analysis for Tubos Reunidos, uncovering competitive intensity, supplier and buyer power, threat of substitutes and entrants, and strategic levers to defend margins and market share.

A concise one-sheet Porter's Five Forces for Tubos Reunidos—instantly reveals competitive pressure and supplier/buyer leverage to speed strategic decisions. Clean, customizable radar visualization and copy-ready layout let teams swap scenarios, update inputs, and drop into decks without specialist skills.

Customers Bargaining Power

Large, sophisticated buyers

Large buyers — oil & gas majors, petrochemical EPCs and industrial OEMs — control scale: global oil & gas capex was about $500bn in 2024, driving tenders often exceeding $10m and enabling bundled regional orders to extract price concessions. Their engineering specs and approved vendor lists limit suppliers and increase negotiation leverage. Performance penalties and on-time clauses, typically 1–3% of contract value, further squeeze margins.

High qualification and switching costs

High qualification and lengthy requalification processes—often lasting several months to over a year—raise switching costs for mills and temper buyer power, favoring Tubos Reunidos incumbents with proven QA records. Buyers can still dual-source to retain leverage, but long approval cycles and supplier audits boost the incumbent’s negotiating position. This dynamic reduces price pressure while preserving buyer options through parallel sourcing.

Cyclic demand and price sensitivity

Energy and petrochemical cycles drive tight budgets and price focus for Tubos Reunidos; Brent crude averaged about $86/bbl in 2024, intensifying cost pressure. In downturns buyers extracted discounts and extended payment terms, while in the 2024 upcycle lead times stretched to roughly 6–9 months, softening buyer leverage. Index-linked pricing formulas partly offset raw-material volatility and protect margins.

Custom specs and service needs

Custom specs—non-standard sizes, premium grades and short lead times—raise Tubos Reunidos’ value-add by shifting buyer focus from unit price to total-cost and uptime; reliance on technical support, traceable documentation and logistics reliability lowers pure price bargaining. After-sales service and responsive engineering become key differentiators that moderate buyer power.

Global alternatives

Buyers can source OCTG and welded pipe from global players Tenaris, Vallourec, TMK, Sumitomo and qualified Chinese mills, giving purchasers leverage through cross‑region price comparisons and alternative lead times.

Trade measures and tariffs intermittently restrict access—cycling buyer power—while long‑term supply agreements and strategic partnerships often lock volumes and mitigate spot bargaining.

- Multiple suppliers: increased competitive quotes

- Tariffs/trade measures: cyclical limit on options

- Strategic partnerships: volume lock, reduced buyer leverage

Major buyers, long lead times, and price pressure reshape oil & gas supply dynamics

Large buyers (majors, EPCs, OEMs) wield strong scale—global oil & gas capex ~ $500bn in 2024—driving large tenders and price concessions. Lengthy qualification (months–>1 year) and 6–9 month lead times boost incumbents’ position, despite buyers’ dual‑sourcing. Performance penalties (1–3% of contract) and Brent ~ $86/bbl in 2024 increase price sensitivity. Custom specs and after‑sales cut pure price bargaining.

| Metric | 2024 |

|---|---|

| Oil & gas capex | $500bn |

| Brent crude | $86/bbl |

| Lead times | 6–9 months |

| Performance penalties | 1–3% contract |

Same Document Delivered

Tubos Reunidos Porter's Five Forces Analysis

This Porter's Five Forces analysis of Tubos Reunidos examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to assess industry profitability and strategic positioning. It highlights steel input dependence, key customer concentration, aftermarket pressure, and regulatory/capacity constraints shaping the firm's leverage. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready for use.