TWFG Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

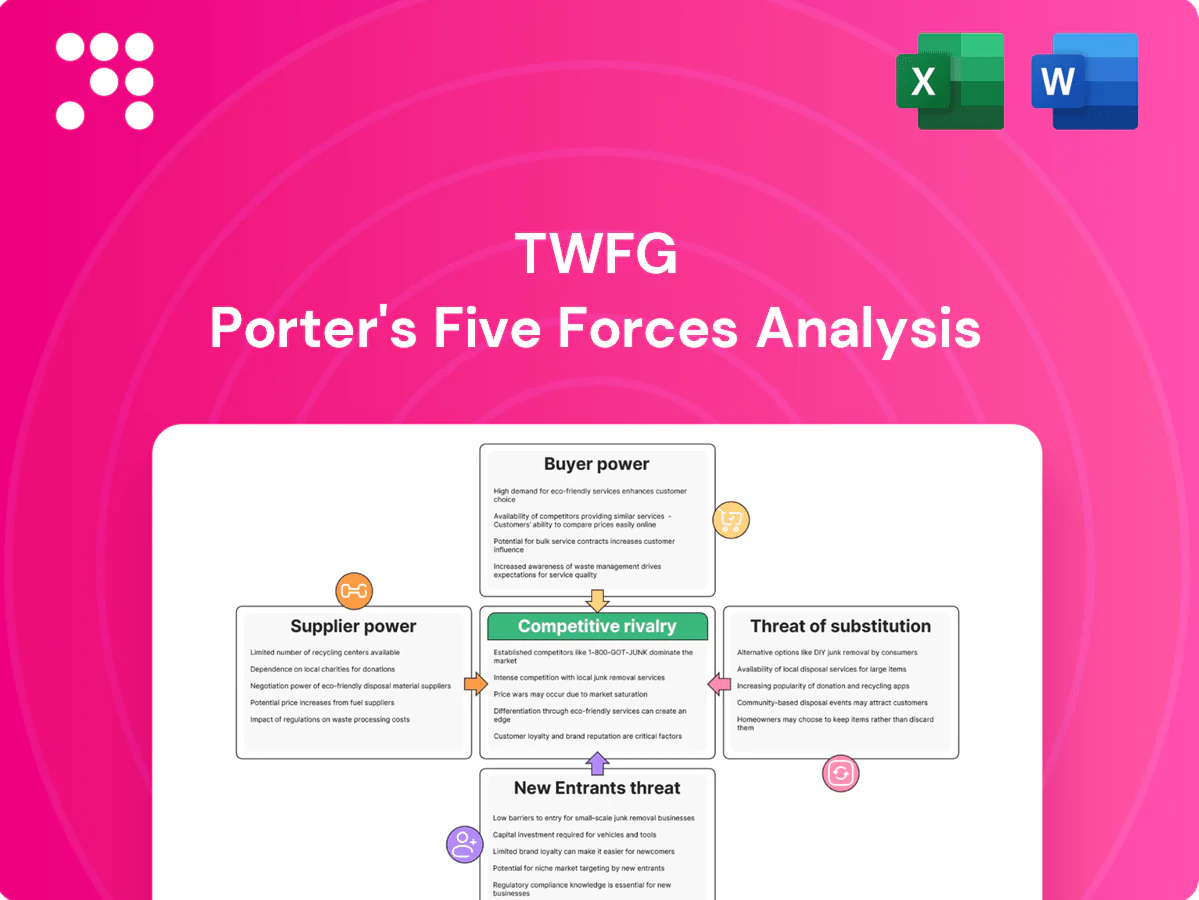

TWFG’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier pressures, and potential substitute threats shaping its insurance market position. It outlines strategic advantages and areas of vulnerability for management and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated carrier relationships

Major national carriers control underwriting capacity and desirable products, giving them leverage over appointments and commission terms; in many commercial lines a handful of carriers provide over 50% of available capacity, concentrating bargaining power. When a few carriers dominate key lines TWFG’s switching options narrow and carriers’ underwriting appetites can sharply constrain placement flexibility. Diversifying carrier panels reduces but does not eliminate this supplier power.

Commission and incentive dependence

Carrier-driven commission schedules, contingent bonuses and profit-sharing programs—often representing 1–5% of premium portfolios and base commissions typically between 8–20%—directly compress TWFG broker margins. Adjustments to volume thresholds or contingent payouts can materially swing profitability quarter-to-quarter. In hard markets carriers frequently tighten incentives, reducing payout frequency and size. TWFG must balance production across carriers to stabilize economics and preserve EBITDA.

Underwriting cycle and capacity

Hard market conditions—with industry-wide commercial rate increases of roughly 10–20% in 2023–24—raise premiums, restrict capacity and tighten underwriting, boosting supplier power. TWFG faces tougher placements and client dissatisfaction as carriers demand higher retentions and stricter terms. In softer phases carriers compete on coverage and price, easing pressure. Cycle management and niche carrier access are key strategic hedges.

Tech, data, and API access

Carrier rating engines, APIs and data feeds are often proprietary, creating integration dependence that, according to 2024 industry surveys, drives 60% of brokers to rely on vendor rater modules and increases switching costs. Limited interoperability slows quoting, reduces broker differentiation, and pressures TWFG to build multi-carrier tech depth to mitigate vendor power.

- Proprietary rater dominance

- High switching costs

- Quoting delays cut competitiveness

- Need multi-carrier integration

Reinsurance and specialty markets

Reinsurers and MGAs determine availability for complex and catastrophe-exposed risks; 2024 saw reinsurance rate-on-line increases roughly 15–25% in many catastrophe-exposed lines, tightening capacity. Capacity withdrawals cascade to primary carriers, forcing stricter terms to brokers and contributing to ~20% longer placement timelines in specialty segments in 2024. TWFG’s broad carrier panel helps preserve client placement options and mitigate fee shocks.

- Reinsurance rate inflation: 15–25% (2024)

- Placement timelines up ~20% (2024)

- TWFG mitigates through wide carrier relationships

>50% carrier share and 60% rater reliance squeeze margins

Carrier concentration limits TWFG placement flexibility as top carriers supply >50% capacity in key commercial lines; commission structures (base 8–20%, contingent 1–5%) compress margins. 2024 reinsurance rate-on-line rose ~15–25%, lengthening specialty placement ~20%. Proprietary raters drive ~60% broker reliance, increasing switching costs.

| Metric | 2024 Value |

|---|---|

| Top-carrier share | >50% |

| Base commissions | 8–20% |

| Contingent payouts | 1–5% |

| Reinsurance ROL | +15–25% |

| Placement delay (specialty) | +20% |

| Rater reliance | 60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to TWFG, assessing rivalry, supplier and buyer power, substitutes and entrant threats, with strategic implications for pricing, profitability and growth defenses—editable for reports and presentations.

A concise Porter's Five Forces one-sheet for TWFG that quantifies insurer-specific pressures—ideal for rapid strategic decisions, investor briefings, and slide-ready executive summaries.

Customers Bargaining Power

High price transparency

Online comparison and multi-quote workflows let clients benchmark instantly; a 2024 survey found 58% of insurance shoppers use comparison tools, increasing price sensitivity. With low perceived differentiation, buyers push for lower premiums and fees, compressing brokerage margins and raising churn risk—industry retention fell to 72% in 2024. TWFG counters with tailored coverage and advisory value to protect margins and client loyalty.

Low switching costs

Policyholders can move at renewal with minimal friction, with industry renewal-shopping rising to about 45% in 2024, increasing buyer leverage as competing brokers readily re-market accounts. Retention increasingly hinges on service quality, claims advocacy, and niche expertise; TWFG emphasizes these to protect commissions. TWFG’s relationship model and local agent footprint aim to raise switching pain and counteract price-driven churn.

Commercial RFP discipline

Commercial RFP discipline: mid-market and enterprise buyers run formal RFPs to extract concessions and service guarantees, unbundling coverages and demanding loss-control programs and granular data reporting. Multi-year broking agreements are frequently re-contested, so TWFG must demonstrate measurable outcomes beyond price, showing retention, loss-ratio improvement and reporting cadence to win renewals.

Product commoditization risk

Personal lines and standard small-commercial policies often appear interchangeable to buyers, compressing broker advisory premiums as coverage is perceived as a commodity. Educating clients on endorsements and uncovered risk gaps repositions brokers as advisors and preserves margin. TWFG’s tailored solutions and risk-mapping tools help de-commoditize offerings by emphasizing bespoke coverages and service value.

- Commoditization pressure on advisory fees

- Client education lifts perceived value

- Tailored TWFG solutions de-commoditize

Agent network expectations

Independent agents affiliated with TWFG act as buyers of carrier access and services, negotiating revenue splits, support levels, or switching aggregators; strong enablement and back-office efficiency are therefore critical to retain agent loyalty. This internal buyer power forces TWFG to allocate more margin to agent commissions and service platforms, shaping its cost structure and margin volatility. Retention depends on seamless onboarding, tech integrations, and responsive field support.

- Agent bargaining: access, splits, support

- Retention levers: enablement, back-office efficiency

- Financial impact: higher commissions and platform costs

Customers wield leverage: 58% compare, 45% shop renewals — retention pressure and margin squeeze

Customers wield rising leverage: 58% used comparison tools in 2024 and renewal-shopping hit ~45%, driving price sensitivity and pushing industry retention to 72%—compressing TWFG brokerage margins. Commercial buyers run RFPs demanding loss-control and reporting, forcing service and outcomes focus. Agent partners also negotiate splits and support, raising commission and platform cost pressure on TWFG.

| Metric | 2024 Value | Impact on TWFG |

|---|---|---|

| Comparison tool usage | 58% | Higher price sensitivity |

| Renewal-shopping | 45% | Higher churn risk |

| Industry retention | 72% | Margin compression |

Preview Before You Purchase

TWFG Porter's Five Forces Analysis

This preview shows the exact TWFG Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for use the moment you buy. You’re viewing the final deliverable and will get this same file instantly upon payment.

Go Beyond the Preview—Access the Full Strategic Report

TWFG’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier pressures, and potential substitute threats shaping its insurance market position. It outlines strategic advantages and areas of vulnerability for management and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated carrier relationships

Major national carriers control underwriting capacity and desirable products, giving them leverage over appointments and commission terms; in many commercial lines a handful of carriers provide over 50% of available capacity, concentrating bargaining power. When a few carriers dominate key lines TWFG’s switching options narrow and carriers’ underwriting appetites can sharply constrain placement flexibility. Diversifying carrier panels reduces but does not eliminate this supplier power.

Commission and incentive dependence

Carrier-driven commission schedules, contingent bonuses and profit-sharing programs—often representing 1–5% of premium portfolios and base commissions typically between 8–20%—directly compress TWFG broker margins. Adjustments to volume thresholds or contingent payouts can materially swing profitability quarter-to-quarter. In hard markets carriers frequently tighten incentives, reducing payout frequency and size. TWFG must balance production across carriers to stabilize economics and preserve EBITDA.

Underwriting cycle and capacity

Hard market conditions—with industry-wide commercial rate increases of roughly 10–20% in 2023–24—raise premiums, restrict capacity and tighten underwriting, boosting supplier power. TWFG faces tougher placements and client dissatisfaction as carriers demand higher retentions and stricter terms. In softer phases carriers compete on coverage and price, easing pressure. Cycle management and niche carrier access are key strategic hedges.

Tech, data, and API access

Carrier rating engines, APIs and data feeds are often proprietary, creating integration dependence that, according to 2024 industry surveys, drives 60% of brokers to rely on vendor rater modules and increases switching costs. Limited interoperability slows quoting, reduces broker differentiation, and pressures TWFG to build multi-carrier tech depth to mitigate vendor power.

- Proprietary rater dominance

- High switching costs

- Quoting delays cut competitiveness

- Need multi-carrier integration

Reinsurance and specialty markets

Reinsurers and MGAs determine availability for complex and catastrophe-exposed risks; 2024 saw reinsurance rate-on-line increases roughly 15–25% in many catastrophe-exposed lines, tightening capacity. Capacity withdrawals cascade to primary carriers, forcing stricter terms to brokers and contributing to ~20% longer placement timelines in specialty segments in 2024. TWFG’s broad carrier panel helps preserve client placement options and mitigate fee shocks.

- Reinsurance rate inflation: 15–25% (2024)

- Placement timelines up ~20% (2024)

- TWFG mitigates through wide carrier relationships

>50% carrier share and 60% rater reliance squeeze margins

Carrier concentration limits TWFG placement flexibility as top carriers supply >50% capacity in key commercial lines; commission structures (base 8–20%, contingent 1–5%) compress margins. 2024 reinsurance rate-on-line rose ~15–25%, lengthening specialty placement ~20%. Proprietary raters drive ~60% broker reliance, increasing switching costs.

| Metric | 2024 Value |

|---|---|

| Top-carrier share | >50% |

| Base commissions | 8–20% |

| Contingent payouts | 1–5% |

| Reinsurance ROL | +15–25% |

| Placement delay (specialty) | +20% |

| Rater reliance | 60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to TWFG, assessing rivalry, supplier and buyer power, substitutes and entrant threats, with strategic implications for pricing, profitability and growth defenses—editable for reports and presentations.

A concise Porter's Five Forces one-sheet for TWFG that quantifies insurer-specific pressures—ideal for rapid strategic decisions, investor briefings, and slide-ready executive summaries.

Customers Bargaining Power

High price transparency

Online comparison and multi-quote workflows let clients benchmark instantly; a 2024 survey found 58% of insurance shoppers use comparison tools, increasing price sensitivity. With low perceived differentiation, buyers push for lower premiums and fees, compressing brokerage margins and raising churn risk—industry retention fell to 72% in 2024. TWFG counters with tailored coverage and advisory value to protect margins and client loyalty.

Low switching costs

Policyholders can move at renewal with minimal friction, with industry renewal-shopping rising to about 45% in 2024, increasing buyer leverage as competing brokers readily re-market accounts. Retention increasingly hinges on service quality, claims advocacy, and niche expertise; TWFG emphasizes these to protect commissions. TWFG’s relationship model and local agent footprint aim to raise switching pain and counteract price-driven churn.

Commercial RFP discipline

Commercial RFP discipline: mid-market and enterprise buyers run formal RFPs to extract concessions and service guarantees, unbundling coverages and demanding loss-control programs and granular data reporting. Multi-year broking agreements are frequently re-contested, so TWFG must demonstrate measurable outcomes beyond price, showing retention, loss-ratio improvement and reporting cadence to win renewals.

Product commoditization risk

Personal lines and standard small-commercial policies often appear interchangeable to buyers, compressing broker advisory premiums as coverage is perceived as a commodity. Educating clients on endorsements and uncovered risk gaps repositions brokers as advisors and preserves margin. TWFG’s tailored solutions and risk-mapping tools help de-commoditize offerings by emphasizing bespoke coverages and service value.

- Commoditization pressure on advisory fees

- Client education lifts perceived value

- Tailored TWFG solutions de-commoditize

Agent network expectations

Independent agents affiliated with TWFG act as buyers of carrier access and services, negotiating revenue splits, support levels, or switching aggregators; strong enablement and back-office efficiency are therefore critical to retain agent loyalty. This internal buyer power forces TWFG to allocate more margin to agent commissions and service platforms, shaping its cost structure and margin volatility. Retention depends on seamless onboarding, tech integrations, and responsive field support.

- Agent bargaining: access, splits, support

- Retention levers: enablement, back-office efficiency

- Financial impact: higher commissions and platform costs

Customers wield leverage: 58% compare, 45% shop renewals — retention pressure and margin squeeze

Customers wield rising leverage: 58% used comparison tools in 2024 and renewal-shopping hit ~45%, driving price sensitivity and pushing industry retention to 72%—compressing TWFG brokerage margins. Commercial buyers run RFPs demanding loss-control and reporting, forcing service and outcomes focus. Agent partners also negotiate splits and support, raising commission and platform cost pressure on TWFG.

| Metric | 2024 Value | Impact on TWFG |

|---|---|---|

| Comparison tool usage | 58% | Higher price sensitivity |

| Renewal-shopping | 45% | Higher churn risk |

| Industry retention | 72% | Margin compression |

Preview Before You Purchase

TWFG Porter's Five Forces Analysis

This preview shows the exact TWFG Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for use the moment you buy. You’re viewing the final deliverable and will get this same file instantly upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

TWFG’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier pressures, and potential substitute threats shaping its insurance market position. It outlines strategic advantages and areas of vulnerability for management and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated carrier relationships

Major national carriers control underwriting capacity and desirable products, giving them leverage over appointments and commission terms; in many commercial lines a handful of carriers provide over 50% of available capacity, concentrating bargaining power. When a few carriers dominate key lines TWFG’s switching options narrow and carriers’ underwriting appetites can sharply constrain placement flexibility. Diversifying carrier panels reduces but does not eliminate this supplier power.

Commission and incentive dependence

Carrier-driven commission schedules, contingent bonuses and profit-sharing programs—often representing 1–5% of premium portfolios and base commissions typically between 8–20%—directly compress TWFG broker margins. Adjustments to volume thresholds or contingent payouts can materially swing profitability quarter-to-quarter. In hard markets carriers frequently tighten incentives, reducing payout frequency and size. TWFG must balance production across carriers to stabilize economics and preserve EBITDA.

Underwriting cycle and capacity

Hard market conditions—with industry-wide commercial rate increases of roughly 10–20% in 2023–24—raise premiums, restrict capacity and tighten underwriting, boosting supplier power. TWFG faces tougher placements and client dissatisfaction as carriers demand higher retentions and stricter terms. In softer phases carriers compete on coverage and price, easing pressure. Cycle management and niche carrier access are key strategic hedges.

Tech, data, and API access

Carrier rating engines, APIs and data feeds are often proprietary, creating integration dependence that, according to 2024 industry surveys, drives 60% of brokers to rely on vendor rater modules and increases switching costs. Limited interoperability slows quoting, reduces broker differentiation, and pressures TWFG to build multi-carrier tech depth to mitigate vendor power.

- Proprietary rater dominance

- High switching costs

- Quoting delays cut competitiveness

- Need multi-carrier integration

Reinsurance and specialty markets

Reinsurers and MGAs determine availability for complex and catastrophe-exposed risks; 2024 saw reinsurance rate-on-line increases roughly 15–25% in many catastrophe-exposed lines, tightening capacity. Capacity withdrawals cascade to primary carriers, forcing stricter terms to brokers and contributing to ~20% longer placement timelines in specialty segments in 2024. TWFG’s broad carrier panel helps preserve client placement options and mitigate fee shocks.

- Reinsurance rate inflation: 15–25% (2024)

- Placement timelines up ~20% (2024)

- TWFG mitigates through wide carrier relationships

>50% carrier share and 60% rater reliance squeeze margins

Carrier concentration limits TWFG placement flexibility as top carriers supply >50% capacity in key commercial lines; commission structures (base 8–20%, contingent 1–5%) compress margins. 2024 reinsurance rate-on-line rose ~15–25%, lengthening specialty placement ~20%. Proprietary raters drive ~60% broker reliance, increasing switching costs.

| Metric | 2024 Value |

|---|---|

| Top-carrier share | >50% |

| Base commissions | 8–20% |

| Contingent payouts | 1–5% |

| Reinsurance ROL | +15–25% |

| Placement delay (specialty) | +20% |

| Rater reliance | 60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to TWFG, assessing rivalry, supplier and buyer power, substitutes and entrant threats, with strategic implications for pricing, profitability and growth defenses—editable for reports and presentations.

A concise Porter's Five Forces one-sheet for TWFG that quantifies insurer-specific pressures—ideal for rapid strategic decisions, investor briefings, and slide-ready executive summaries.

Customers Bargaining Power

High price transparency

Online comparison and multi-quote workflows let clients benchmark instantly; a 2024 survey found 58% of insurance shoppers use comparison tools, increasing price sensitivity. With low perceived differentiation, buyers push for lower premiums and fees, compressing brokerage margins and raising churn risk—industry retention fell to 72% in 2024. TWFG counters with tailored coverage and advisory value to protect margins and client loyalty.

Low switching costs

Policyholders can move at renewal with minimal friction, with industry renewal-shopping rising to about 45% in 2024, increasing buyer leverage as competing brokers readily re-market accounts. Retention increasingly hinges on service quality, claims advocacy, and niche expertise; TWFG emphasizes these to protect commissions. TWFG’s relationship model and local agent footprint aim to raise switching pain and counteract price-driven churn.

Commercial RFP discipline

Commercial RFP discipline: mid-market and enterprise buyers run formal RFPs to extract concessions and service guarantees, unbundling coverages and demanding loss-control programs and granular data reporting. Multi-year broking agreements are frequently re-contested, so TWFG must demonstrate measurable outcomes beyond price, showing retention, loss-ratio improvement and reporting cadence to win renewals.

Product commoditization risk

Personal lines and standard small-commercial policies often appear interchangeable to buyers, compressing broker advisory premiums as coverage is perceived as a commodity. Educating clients on endorsements and uncovered risk gaps repositions brokers as advisors and preserves margin. TWFG’s tailored solutions and risk-mapping tools help de-commoditize offerings by emphasizing bespoke coverages and service value.

- Commoditization pressure on advisory fees

- Client education lifts perceived value

- Tailored TWFG solutions de-commoditize

Agent network expectations

Independent agents affiliated with TWFG act as buyers of carrier access and services, negotiating revenue splits, support levels, or switching aggregators; strong enablement and back-office efficiency are therefore critical to retain agent loyalty. This internal buyer power forces TWFG to allocate more margin to agent commissions and service platforms, shaping its cost structure and margin volatility. Retention depends on seamless onboarding, tech integrations, and responsive field support.

- Agent bargaining: access, splits, support

- Retention levers: enablement, back-office efficiency

- Financial impact: higher commissions and platform costs

Customers wield leverage: 58% compare, 45% shop renewals — retention pressure and margin squeeze

Customers wield rising leverage: 58% used comparison tools in 2024 and renewal-shopping hit ~45%, driving price sensitivity and pushing industry retention to 72%—compressing TWFG brokerage margins. Commercial buyers run RFPs demanding loss-control and reporting, forcing service and outcomes focus. Agent partners also negotiate splits and support, raising commission and platform cost pressure on TWFG.

| Metric | 2024 Value | Impact on TWFG |

|---|---|---|

| Comparison tool usage | 58% | Higher price sensitivity |

| Renewal-shopping | 45% | Higher churn risk |

| Industry retention | 72% | Margin compression |

Preview Before You Purchase

TWFG Porter's Five Forces Analysis

This preview shows the exact TWFG Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for use the moment you buy. You’re viewing the final deliverable and will get this same file instantly upon payment.