Twin Disc Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

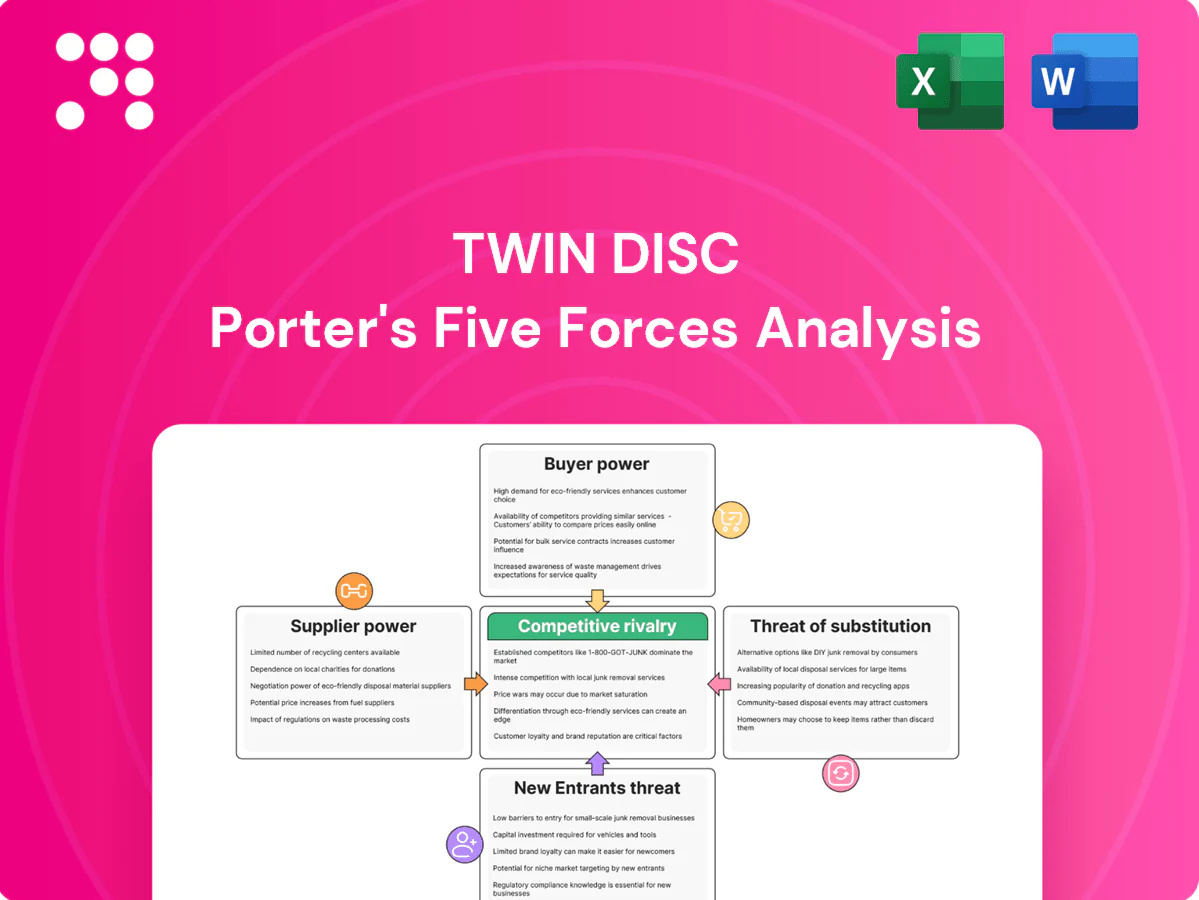

This snapshot highlights key pressures on Twin Disc — supplier bargaining, buyer power, competitive rivalry and substitute threats. It outlines how scale, niche markets and distribution shape profitability. Ready for actionable, data-driven strategy? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and tailored implications.

Suppliers Bargaining Power

Specialty metals and castings concentration

High-spec alloys, precision castings and heat-treated components for Twin Disc come from a small, qualified supplier base where ISO/AS9100 and metallurgy traceability limit alternatives. This concentration gives foundries and forge shops significant leverage over pricing and lead times. Dual-sourcing is technically feasible but requires lengthy, resource-intensive qualification and certification cycles. Supply disruptions thus materially raise supplier bargaining power.

Long lead times and capacity constraints

Critical inputs such as large housings, gears and shafts commonly have long cycle times of 8–20 weeks and machining tolerances often down to ±0.01 mm, creating testing-slot bottlenecks; during upcycles suppliers frequently operate at or near 100% capacity, exerting pricing and delivery power. Inventory buffers (typical 60–120 days) mitigate shortages but lock up working capital and raise carrying costs.

Input cost volatility

Steel, copper and energy price swings in 2024 drove supplier quotes and index-linked surcharges, with commodity cost movements often in the mid-teens percent range year-over-year, pushing risk upstream. Surcharges and index-linked contracts allowed suppliers to shift volatility, leaving Twin Disc exposed to short windows of margin pressure before pass-through. Hedging programs and design-to-cost efforts reduced but did not eliminate exposure to those swings.

Electronics and controls dependency

Sensors, PLCs and drives depend on global semiconductor and controls vendors, with the global semiconductor market about $600 billion in 2024, concentrating bargaining power among key suppliers.

Component obsolescence and allocation periods often exceed 26 weeks in 2024, raising switching costs; deep software and firmware integration increases technical lock-in, and approved vendor lists restrict rapid substitution.

- Concentration: top suppliers control critical chips

- Market size: ~$600B (2024)

- Lead times: allocation >26 weeks (2024)

- Lock-in: software/firmware integration

- Procurement: approved vendor lists limit alternatives

Qualification and quality regimes

Marine-class and OEM standards force extensive supplier audits and PPAP-like validations, typically taking 6–12 months and often costing suppliers from low six figures to over $500k in complex systems, which makes requalifying a new source time-consuming and expensive and therefore strengthens incumbent suppliers’ bargaining power; conversely, a single high-profile quality lapse can rapidly reverse that leverage.

- Typical validation time: 6–12 months (2024 industry reports)

- Typical cost: $100k–$500k+ per complex supplier

- Requalification delays raise switching costs

- Quality failures quickly erode supplier power

Concentrated suppliers drive pricing power as lead times exceed 26 weeks

High-spec suppliers are concentrated and certified, giving foundries/forges and semiconductor vendors strong pricing and delivery leverage; critical lead times often exceed 8–20 weeks and allocations >26 weeks (2024). Dual-sourcing and requalification take 6–12 months and $100k–$500k, raising switching costs. Inventory buffers (60–120 days) and index-linked surcharges transfer commodity (mid-teens % YoY) and energy risks upstream.

| Metric | Value (2024) |

|---|---|

| Semiconductor market | $600B |

| Lead times (critical parts) | 8–20 weeks; allocation >26 weeks |

| Requalification | 6–12 months; $100k–$500k+ |

| Inventory buffer | 60–120 days |

| Commodity swings | Mid-teens % YoY |

What is included in the product

Tailored exclusively for Twin Disc, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, substitutes and entry threats, evaluating impacts on pricing, profitability and strategic positioning while highlighting disruptive forces and market dynamics.

A concise, single-sheet Porter's Five Forces for Twin Disc that visualizes competitive pressures and strategic levers—ideal for fast boardroom decisions. Editable inputs and radar chart let you model scenarios (new entrants, regulation) without coding, ready to drop into decks.

Customers Bargaining Power

Large OEMs and shipyards negotiate hard

As of 2024 Twin Disc customers include major shipbuilders, engine makers and industrial OEMs with professional procurement teams. They leverage volume, frame agreements and global benchmarking to extract price concessions and strict delivery schedules. This buying power creates margin pressure, which Twin Disc offsets with value-added packaging, integrated service contracts and performance guarantees.

High switching costs in installed base

Replacements must match engine interfaces, class rules and vessel layouts, so operators face technical constraints that limit vendor substitutes. Downtime can cost tens of thousands of USD per day and retraining/certification adds further expense and delay, increasing switch friction. This installed-base lock-in materially reduces buyer bargaining power post-installation, though pre-sale buyers still solicit competing bids to pressure prices.

Project-based, cyclical demand

Orders for Twin Disc are lumpy and tied to vessel programs and capital projects, with 2024 industry order volatility exceeding 20%, so buyers can defer or cancel in downturns and force pricing pressure. During upcycles in 2024, delivery assurance and service speed became decisive, often outweighing discount demands. This cyclicality shifts bargaining power between buyers and Twin Disc throughout the economic cycle.

Total cost of ownership focus

Buyers prioritize total cost of ownership: fuel efficiency, reliability, and lifecycle service drive purchasing decisions, with proven durability and global aftermarket support allowing Twin Disc to command premium pricing. Performance data and robust warranties are key levers during negotiations; sustained poor uptime immediately increases buyer leverage and demand for concessions.

- Fuel efficiency focus

- Reliability = pricing power

- Performance data & warranties

- Poor uptime strengthens buyers

Certification and spec-in advantages

Winning class-approved specs early embeds Twin Disc into OEM designs, creating significant redesign costs for buyers and lowering buyer leverage on that program. Once specified, customers face time and certification expenses to switch suppliers, reducing their bargaining power. Competing vendors seek equivalency approvals to restore leverage and reopen procurement contests.

- Spec lock-in reduces buyer leverage

- Redesign/certification costs hinder switching

- Equivalency approvals are competitors’ strategy

Volume contracts squeeze prices; uptime services and warranties restore supplier leverage

In 2024 Twin Disc buyers (shipbuilders, engine OEMs, industrial fleets) use volume contracts and benchmarking to force price concessions, but technical fit and class approvals limit substitutes, reducing post-sale leverage. Downtime costs (typ. 20,000–100,000 USD/day) and retraining/certification (weeks–months) increase switching friction; order volatility >20% shifts power cyclically. Value-added service, warranties and proven uptime restore Twin Disc pricing power.

| Metric | 2024 |

|---|---|

| Order volatility | >20% |

| Downtime cost/day | 20,000–100,000 USD |

| Switching time | Weeks–Months |

| Buyer type | Shipbuilders, engine OEMs, fleets |

Preview Before You Purchase

Twin Disc Porter's Five Forces Analysis

This preview displays the exact Twin Disc Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights key pressures on Twin Disc — supplier bargaining, buyer power, competitive rivalry and substitute threats. It outlines how scale, niche markets and distribution shape profitability. Ready for actionable, data-driven strategy? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and tailored implications.

Suppliers Bargaining Power

Specialty metals and castings concentration

High-spec alloys, precision castings and heat-treated components for Twin Disc come from a small, qualified supplier base where ISO/AS9100 and metallurgy traceability limit alternatives. This concentration gives foundries and forge shops significant leverage over pricing and lead times. Dual-sourcing is technically feasible but requires lengthy, resource-intensive qualification and certification cycles. Supply disruptions thus materially raise supplier bargaining power.

Long lead times and capacity constraints

Critical inputs such as large housings, gears and shafts commonly have long cycle times of 8–20 weeks and machining tolerances often down to ±0.01 mm, creating testing-slot bottlenecks; during upcycles suppliers frequently operate at or near 100% capacity, exerting pricing and delivery power. Inventory buffers (typical 60–120 days) mitigate shortages but lock up working capital and raise carrying costs.

Input cost volatility

Steel, copper and energy price swings in 2024 drove supplier quotes and index-linked surcharges, with commodity cost movements often in the mid-teens percent range year-over-year, pushing risk upstream. Surcharges and index-linked contracts allowed suppliers to shift volatility, leaving Twin Disc exposed to short windows of margin pressure before pass-through. Hedging programs and design-to-cost efforts reduced but did not eliminate exposure to those swings.

Electronics and controls dependency

Sensors, PLCs and drives depend on global semiconductor and controls vendors, with the global semiconductor market about $600 billion in 2024, concentrating bargaining power among key suppliers.

Component obsolescence and allocation periods often exceed 26 weeks in 2024, raising switching costs; deep software and firmware integration increases technical lock-in, and approved vendor lists restrict rapid substitution.

- Concentration: top suppliers control critical chips

- Market size: ~$600B (2024)

- Lead times: allocation >26 weeks (2024)

- Lock-in: software/firmware integration

- Procurement: approved vendor lists limit alternatives

Qualification and quality regimes

Marine-class and OEM standards force extensive supplier audits and PPAP-like validations, typically taking 6–12 months and often costing suppliers from low six figures to over $500k in complex systems, which makes requalifying a new source time-consuming and expensive and therefore strengthens incumbent suppliers’ bargaining power; conversely, a single high-profile quality lapse can rapidly reverse that leverage.

- Typical validation time: 6–12 months (2024 industry reports)

- Typical cost: $100k–$500k+ per complex supplier

- Requalification delays raise switching costs

- Quality failures quickly erode supplier power

Concentrated suppliers drive pricing power as lead times exceed 26 weeks

High-spec suppliers are concentrated and certified, giving foundries/forges and semiconductor vendors strong pricing and delivery leverage; critical lead times often exceed 8–20 weeks and allocations >26 weeks (2024). Dual-sourcing and requalification take 6–12 months and $100k–$500k, raising switching costs. Inventory buffers (60–120 days) and index-linked surcharges transfer commodity (mid-teens % YoY) and energy risks upstream.

| Metric | Value (2024) |

|---|---|

| Semiconductor market | $600B |

| Lead times (critical parts) | 8–20 weeks; allocation >26 weeks |

| Requalification | 6–12 months; $100k–$500k+ |

| Inventory buffer | 60–120 days |

| Commodity swings | Mid-teens % YoY |

What is included in the product

Tailored exclusively for Twin Disc, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, substitutes and entry threats, evaluating impacts on pricing, profitability and strategic positioning while highlighting disruptive forces and market dynamics.

A concise, single-sheet Porter's Five Forces for Twin Disc that visualizes competitive pressures and strategic levers—ideal for fast boardroom decisions. Editable inputs and radar chart let you model scenarios (new entrants, regulation) without coding, ready to drop into decks.

Customers Bargaining Power

Large OEMs and shipyards negotiate hard

As of 2024 Twin Disc customers include major shipbuilders, engine makers and industrial OEMs with professional procurement teams. They leverage volume, frame agreements and global benchmarking to extract price concessions and strict delivery schedules. This buying power creates margin pressure, which Twin Disc offsets with value-added packaging, integrated service contracts and performance guarantees.

High switching costs in installed base

Replacements must match engine interfaces, class rules and vessel layouts, so operators face technical constraints that limit vendor substitutes. Downtime can cost tens of thousands of USD per day and retraining/certification adds further expense and delay, increasing switch friction. This installed-base lock-in materially reduces buyer bargaining power post-installation, though pre-sale buyers still solicit competing bids to pressure prices.

Project-based, cyclical demand

Orders for Twin Disc are lumpy and tied to vessel programs and capital projects, with 2024 industry order volatility exceeding 20%, so buyers can defer or cancel in downturns and force pricing pressure. During upcycles in 2024, delivery assurance and service speed became decisive, often outweighing discount demands. This cyclicality shifts bargaining power between buyers and Twin Disc throughout the economic cycle.

Total cost of ownership focus

Buyers prioritize total cost of ownership: fuel efficiency, reliability, and lifecycle service drive purchasing decisions, with proven durability and global aftermarket support allowing Twin Disc to command premium pricing. Performance data and robust warranties are key levers during negotiations; sustained poor uptime immediately increases buyer leverage and demand for concessions.

- Fuel efficiency focus

- Reliability = pricing power

- Performance data & warranties

- Poor uptime strengthens buyers

Certification and spec-in advantages

Winning class-approved specs early embeds Twin Disc into OEM designs, creating significant redesign costs for buyers and lowering buyer leverage on that program. Once specified, customers face time and certification expenses to switch suppliers, reducing their bargaining power. Competing vendors seek equivalency approvals to restore leverage and reopen procurement contests.

- Spec lock-in reduces buyer leverage

- Redesign/certification costs hinder switching

- Equivalency approvals are competitors’ strategy

Volume contracts squeeze prices; uptime services and warranties restore supplier leverage

In 2024 Twin Disc buyers (shipbuilders, engine OEMs, industrial fleets) use volume contracts and benchmarking to force price concessions, but technical fit and class approvals limit substitutes, reducing post-sale leverage. Downtime costs (typ. 20,000–100,000 USD/day) and retraining/certification (weeks–months) increase switching friction; order volatility >20% shifts power cyclically. Value-added service, warranties and proven uptime restore Twin Disc pricing power.

| Metric | 2024 |

|---|---|

| Order volatility | >20% |

| Downtime cost/day | 20,000–100,000 USD |

| Switching time | Weeks–Months |

| Buyer type | Shipbuilders, engine OEMs, fleets |

Preview Before You Purchase

Twin Disc Porter's Five Forces Analysis

This preview displays the exact Twin Disc Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights key pressures on Twin Disc — supplier bargaining, buyer power, competitive rivalry and substitute threats. It outlines how scale, niche markets and distribution shape profitability. Ready for actionable, data-driven strategy? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and tailored implications.

Suppliers Bargaining Power

Specialty metals and castings concentration

High-spec alloys, precision castings and heat-treated components for Twin Disc come from a small, qualified supplier base where ISO/AS9100 and metallurgy traceability limit alternatives. This concentration gives foundries and forge shops significant leverage over pricing and lead times. Dual-sourcing is technically feasible but requires lengthy, resource-intensive qualification and certification cycles. Supply disruptions thus materially raise supplier bargaining power.

Long lead times and capacity constraints

Critical inputs such as large housings, gears and shafts commonly have long cycle times of 8–20 weeks and machining tolerances often down to ±0.01 mm, creating testing-slot bottlenecks; during upcycles suppliers frequently operate at or near 100% capacity, exerting pricing and delivery power. Inventory buffers (typical 60–120 days) mitigate shortages but lock up working capital and raise carrying costs.

Input cost volatility

Steel, copper and energy price swings in 2024 drove supplier quotes and index-linked surcharges, with commodity cost movements often in the mid-teens percent range year-over-year, pushing risk upstream. Surcharges and index-linked contracts allowed suppliers to shift volatility, leaving Twin Disc exposed to short windows of margin pressure before pass-through. Hedging programs and design-to-cost efforts reduced but did not eliminate exposure to those swings.

Electronics and controls dependency

Sensors, PLCs and drives depend on global semiconductor and controls vendors, with the global semiconductor market about $600 billion in 2024, concentrating bargaining power among key suppliers.

Component obsolescence and allocation periods often exceed 26 weeks in 2024, raising switching costs; deep software and firmware integration increases technical lock-in, and approved vendor lists restrict rapid substitution.

- Concentration: top suppliers control critical chips

- Market size: ~$600B (2024)

- Lead times: allocation >26 weeks (2024)

- Lock-in: software/firmware integration

- Procurement: approved vendor lists limit alternatives

Qualification and quality regimes

Marine-class and OEM standards force extensive supplier audits and PPAP-like validations, typically taking 6–12 months and often costing suppliers from low six figures to over $500k in complex systems, which makes requalifying a new source time-consuming and expensive and therefore strengthens incumbent suppliers’ bargaining power; conversely, a single high-profile quality lapse can rapidly reverse that leverage.

- Typical validation time: 6–12 months (2024 industry reports)

- Typical cost: $100k–$500k+ per complex supplier

- Requalification delays raise switching costs

- Quality failures quickly erode supplier power

Concentrated suppliers drive pricing power as lead times exceed 26 weeks

High-spec suppliers are concentrated and certified, giving foundries/forges and semiconductor vendors strong pricing and delivery leverage; critical lead times often exceed 8–20 weeks and allocations >26 weeks (2024). Dual-sourcing and requalification take 6–12 months and $100k–$500k, raising switching costs. Inventory buffers (60–120 days) and index-linked surcharges transfer commodity (mid-teens % YoY) and energy risks upstream.

| Metric | Value (2024) |

|---|---|

| Semiconductor market | $600B |

| Lead times (critical parts) | 8–20 weeks; allocation >26 weeks |

| Requalification | 6–12 months; $100k–$500k+ |

| Inventory buffer | 60–120 days |

| Commodity swings | Mid-teens % YoY |

What is included in the product

Tailored exclusively for Twin Disc, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, substitutes and entry threats, evaluating impacts on pricing, profitability and strategic positioning while highlighting disruptive forces and market dynamics.

A concise, single-sheet Porter's Five Forces for Twin Disc that visualizes competitive pressures and strategic levers—ideal for fast boardroom decisions. Editable inputs and radar chart let you model scenarios (new entrants, regulation) without coding, ready to drop into decks.

Customers Bargaining Power

Large OEMs and shipyards negotiate hard

As of 2024 Twin Disc customers include major shipbuilders, engine makers and industrial OEMs with professional procurement teams. They leverage volume, frame agreements and global benchmarking to extract price concessions and strict delivery schedules. This buying power creates margin pressure, which Twin Disc offsets with value-added packaging, integrated service contracts and performance guarantees.

High switching costs in installed base

Replacements must match engine interfaces, class rules and vessel layouts, so operators face technical constraints that limit vendor substitutes. Downtime can cost tens of thousands of USD per day and retraining/certification adds further expense and delay, increasing switch friction. This installed-base lock-in materially reduces buyer bargaining power post-installation, though pre-sale buyers still solicit competing bids to pressure prices.

Project-based, cyclical demand

Orders for Twin Disc are lumpy and tied to vessel programs and capital projects, with 2024 industry order volatility exceeding 20%, so buyers can defer or cancel in downturns and force pricing pressure. During upcycles in 2024, delivery assurance and service speed became decisive, often outweighing discount demands. This cyclicality shifts bargaining power between buyers and Twin Disc throughout the economic cycle.

Total cost of ownership focus

Buyers prioritize total cost of ownership: fuel efficiency, reliability, and lifecycle service drive purchasing decisions, with proven durability and global aftermarket support allowing Twin Disc to command premium pricing. Performance data and robust warranties are key levers during negotiations; sustained poor uptime immediately increases buyer leverage and demand for concessions.

- Fuel efficiency focus

- Reliability = pricing power

- Performance data & warranties

- Poor uptime strengthens buyers

Certification and spec-in advantages

Winning class-approved specs early embeds Twin Disc into OEM designs, creating significant redesign costs for buyers and lowering buyer leverage on that program. Once specified, customers face time and certification expenses to switch suppliers, reducing their bargaining power. Competing vendors seek equivalency approvals to restore leverage and reopen procurement contests.

- Spec lock-in reduces buyer leverage

- Redesign/certification costs hinder switching

- Equivalency approvals are competitors’ strategy

Volume contracts squeeze prices; uptime services and warranties restore supplier leverage

In 2024 Twin Disc buyers (shipbuilders, engine OEMs, industrial fleets) use volume contracts and benchmarking to force price concessions, but technical fit and class approvals limit substitutes, reducing post-sale leverage. Downtime costs (typ. 20,000–100,000 USD/day) and retraining/certification (weeks–months) increase switching friction; order volatility >20% shifts power cyclically. Value-added service, warranties and proven uptime restore Twin Disc pricing power.

| Metric | 2024 |

|---|---|

| Order volatility | >20% |

| Downtime cost/day | 20,000–100,000 USD |

| Switching time | Weeks–Months |

| Buyer type | Shipbuilders, engine OEMs, fleets |

Preview Before You Purchase

Twin Disc Porter's Five Forces Analysis

This preview displays the exact Twin Disc Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.